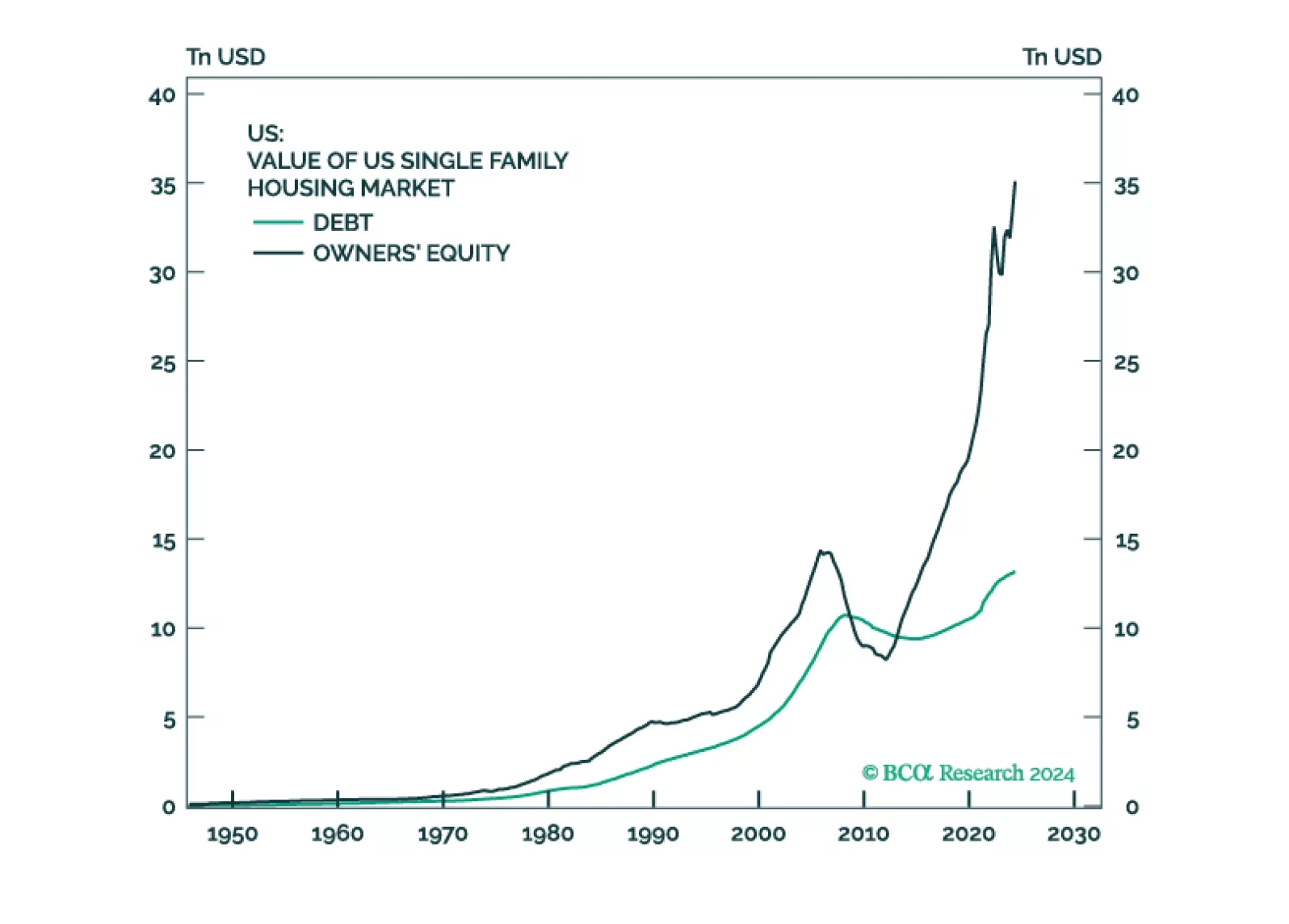

US Election

October seasonality tends to be negative for stocks in an election year. That is the only thing that has stayed our hand from shifting out of our tactical underweight on US equities, initiated – poorly – in July.

But the big macro news from September has not been bearish. The Fed has signaled jumbo cuts. Within seven weeks, the US central bank intends to cut by 100bps! Meanwhile, China appears to have reached a “policy bottom,” with its September 26 Politburo meeting signaling an extraordinary rhetorical shift towards fiscal policy. As such, we are starting to sniff out global reflation, akin to the 2015-2016 mid-cycle slowdown.

The labor market data still worries us. It is clearly deteriorating, on paper. Is it because of an imminent recession or “normalization?” It is difficult to say. We are open minded.

Finally, the Middle East tensions are again on the horizon. If Iran stays its hand against Saudi energy facilities – which we expect it to continue to do – the Iran-Israel conflict is a sideshow. Nonetheless, with global reflation afoot, we went long oil last week, on September 26. As such, geopolitics is a neat tailwind to that call.

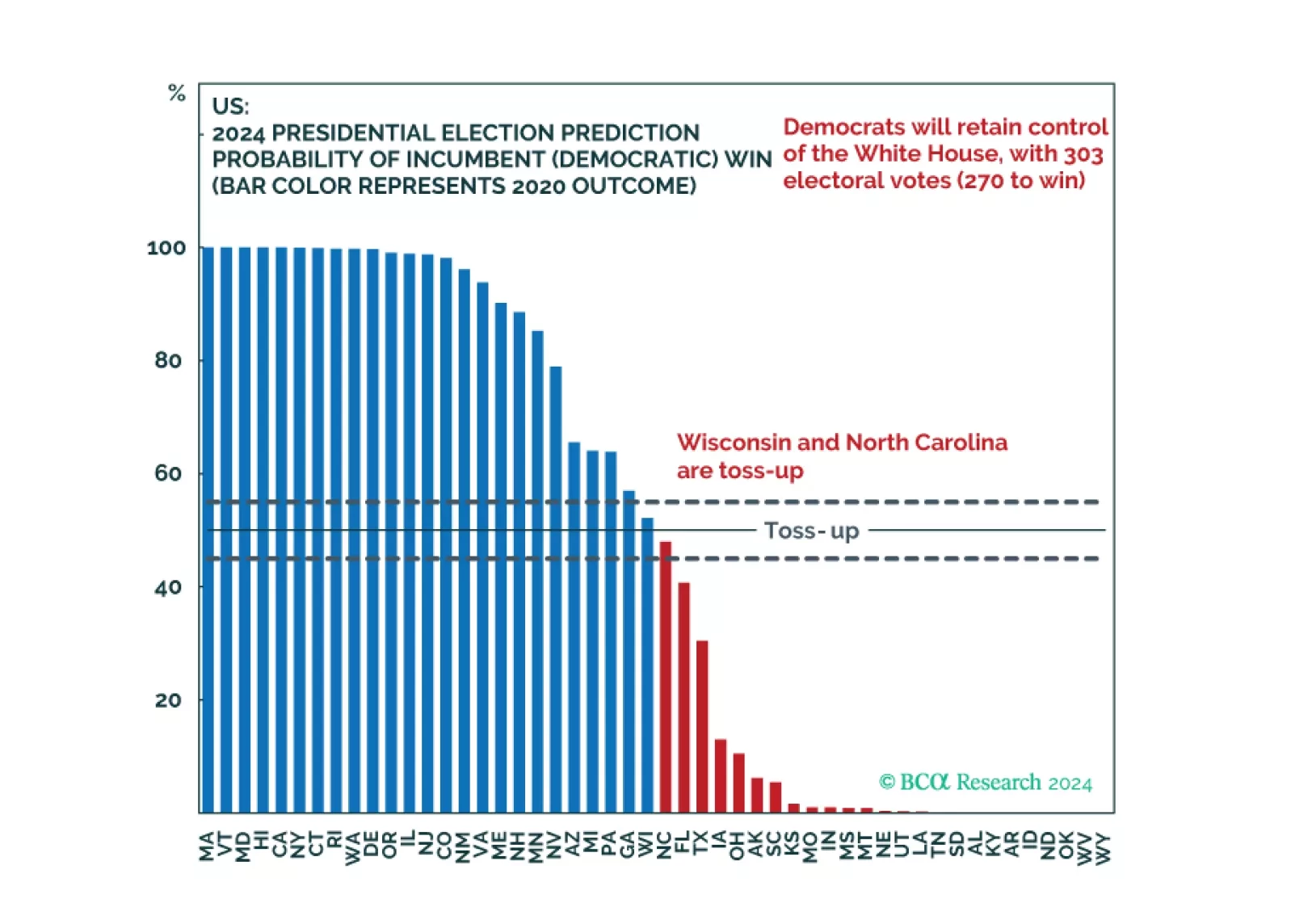

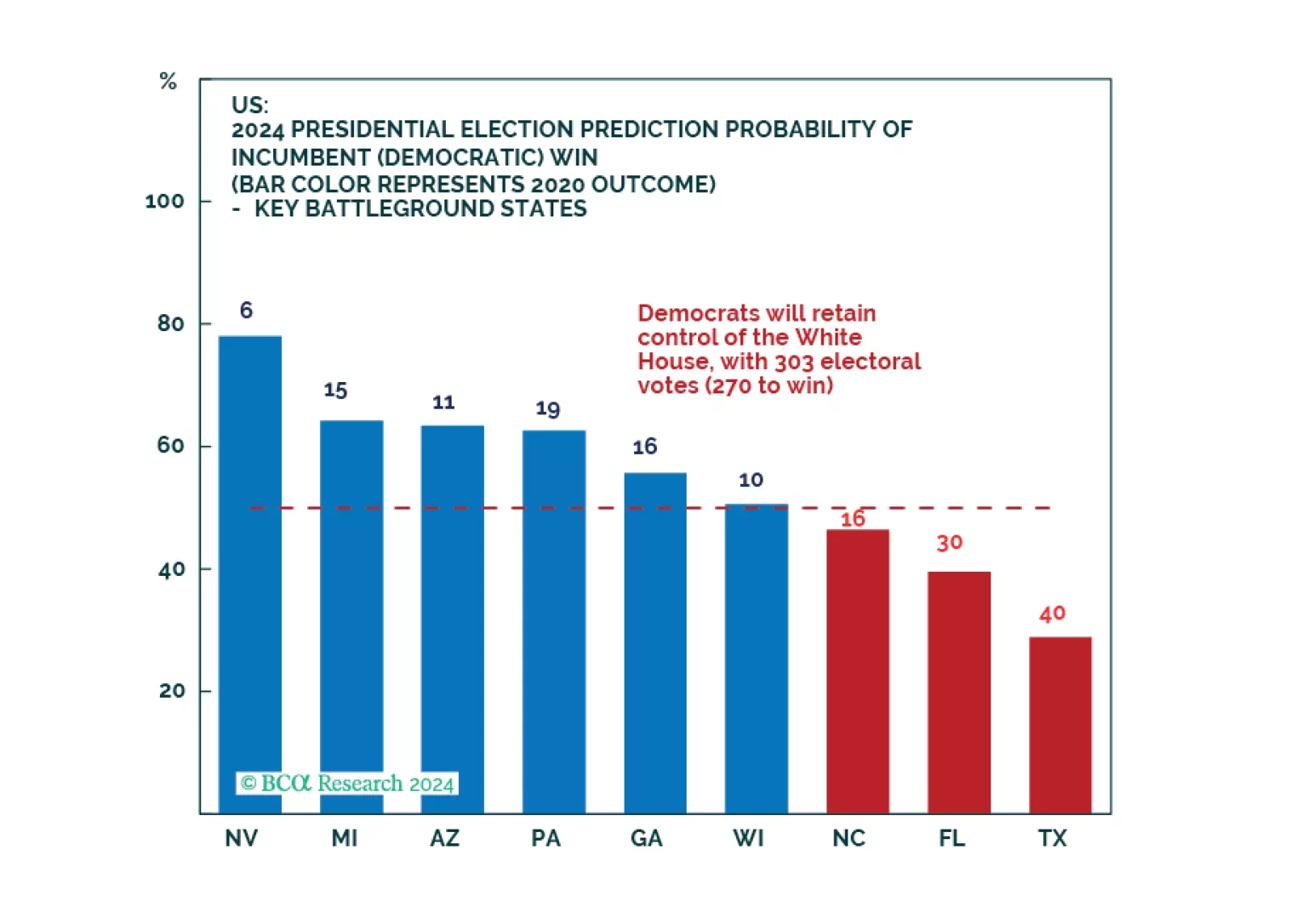

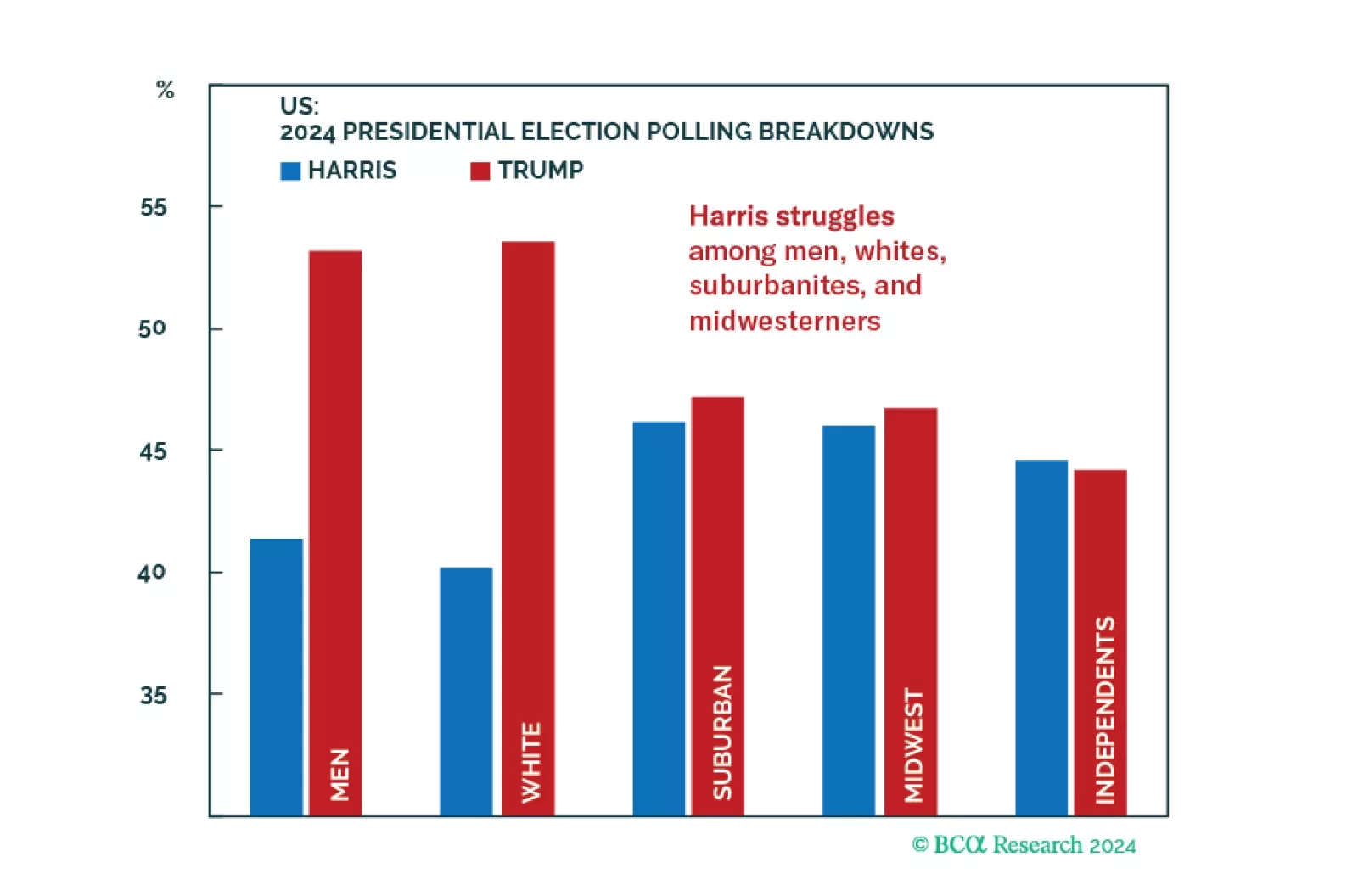

Our quant model shows Democrats winning the election at a 56% probability, with 303 electoral college votes. But swing state economies are slowing and Democrats’ odds in Michigan fell. Trump can win with Georgia, Michigan, plus one other state. Neither the Fed nor China’s stimulus should reduce one’s odds of a Republican upset.

Markets are rallying on Fed rate cuts and China stimulus but there will also be October surprises ahead of the US election, which Trump could still win. Russia’s conflict with the West is escalating and the Middle East is destabilizing further. Investors should favor US bonds but they should add some risk in emerging markets in response to China’s policy turn.

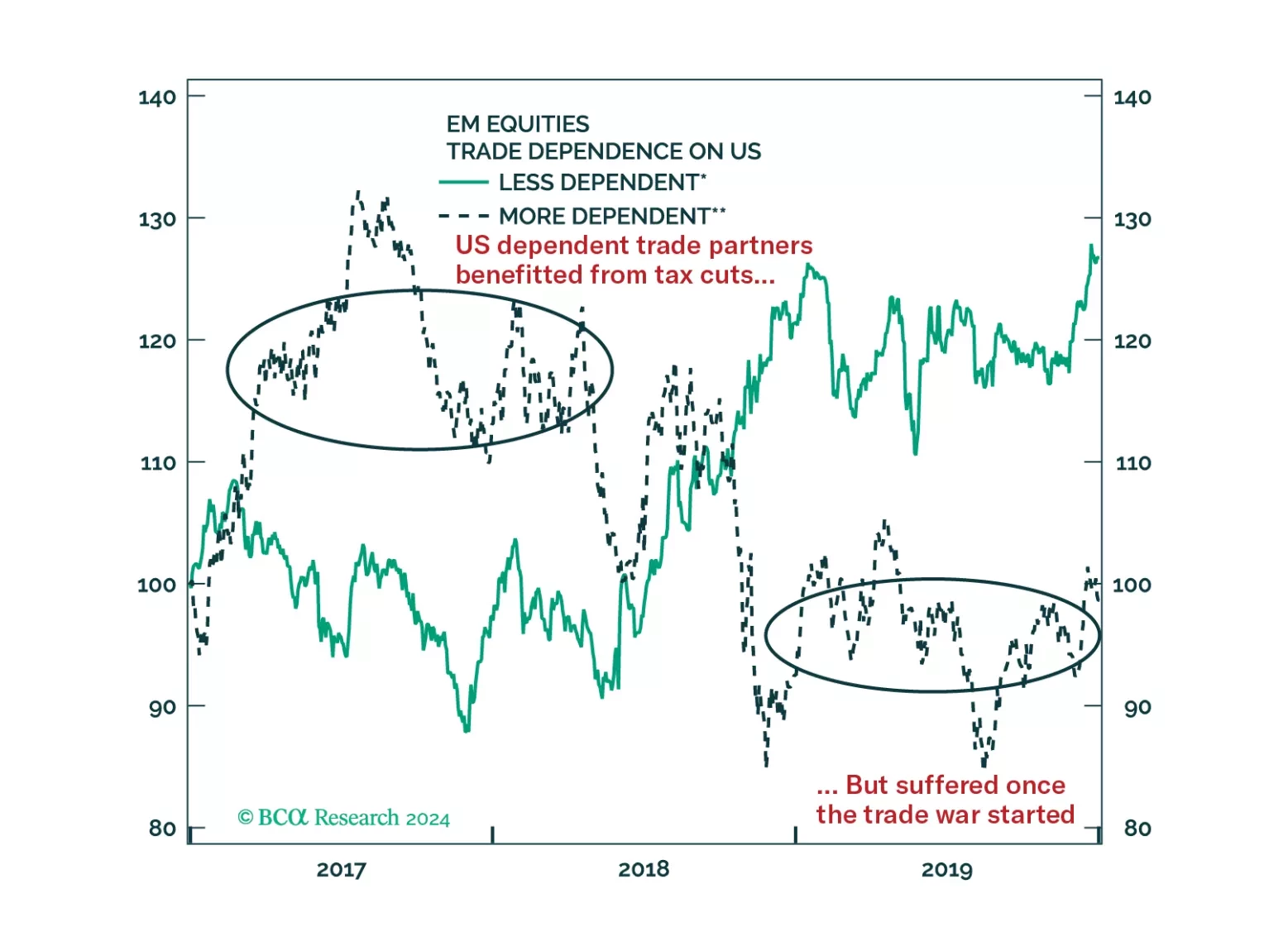

As we head into a more turbulent macroeconomic and geopolitical period, investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable region, and not so dependent on the US or China. Hence, we are introducing the Global Political Capital Index as a way to integrate these factors into a score that can help narrow down the countries with the best and worst abilities to deal with the incoming challenges.

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.

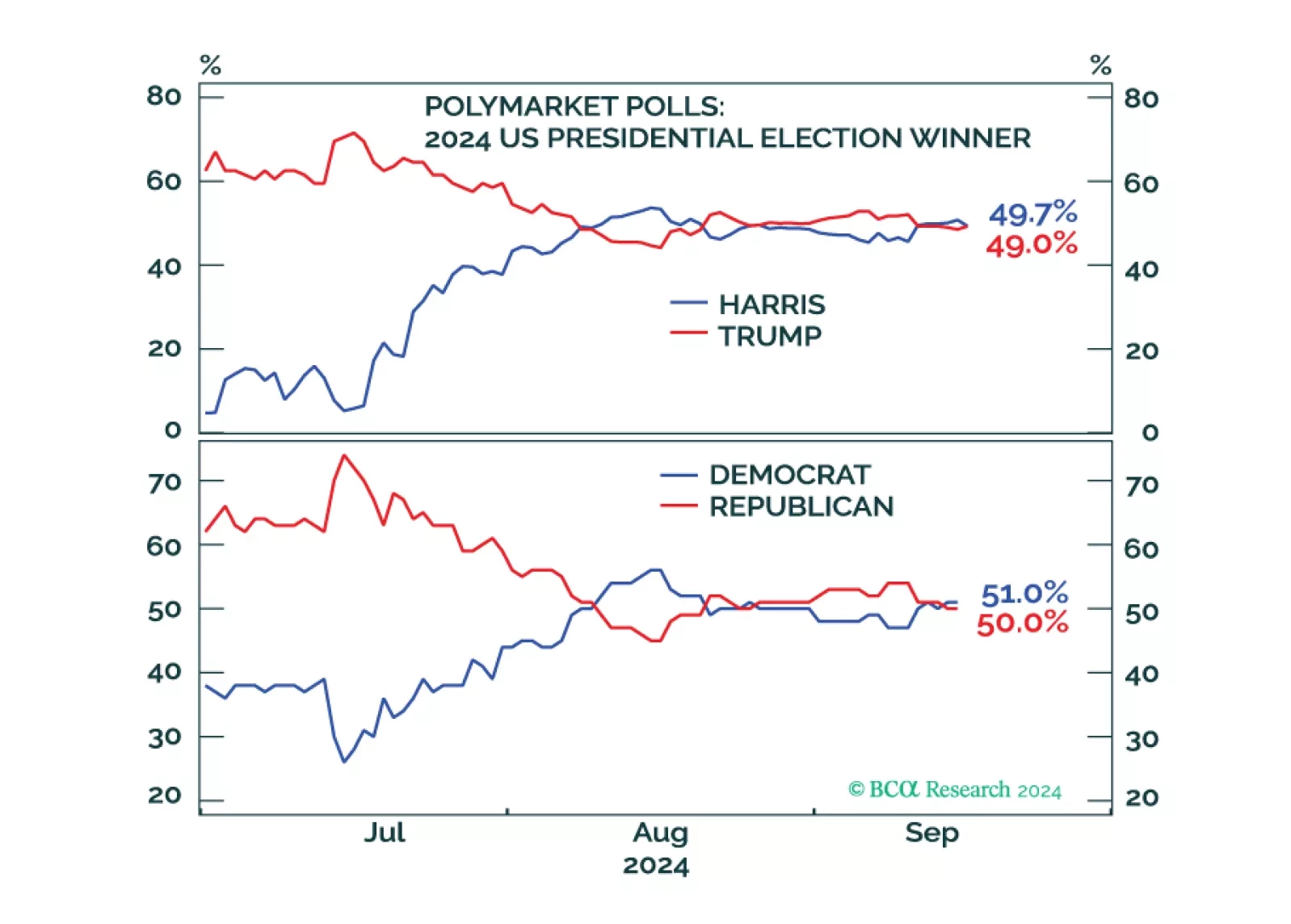

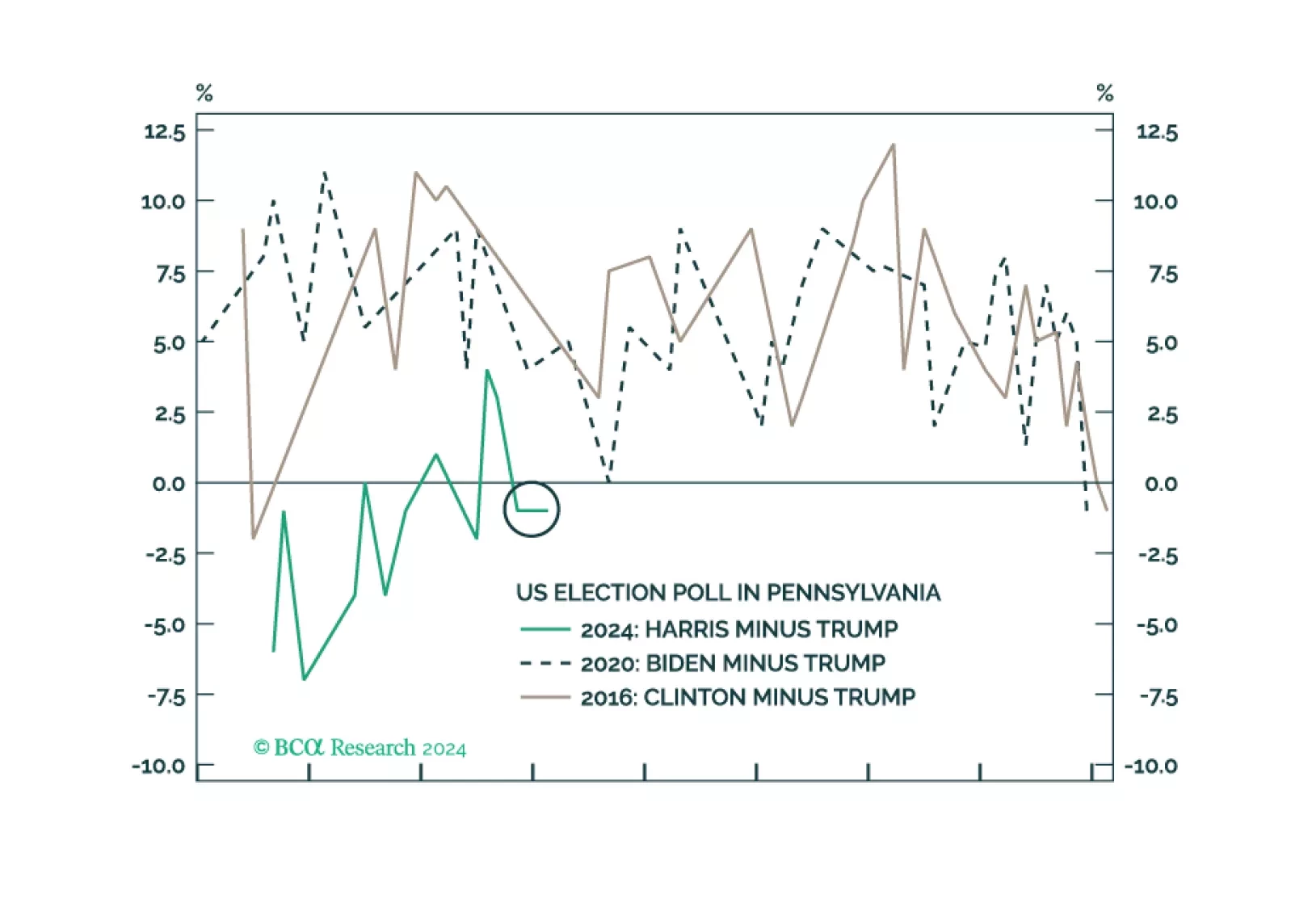

Despite the disastrous performance by former President Trump in the debate with Vice President Kamala Harris, there are still paths for him to come back to power. The economy and global instability could flare up anytime between now and election day, while quirks in the Electoral College ensure that the election will be close. The race is still competitive and policy uncertainty and volatility will be elevated.

Democrats will not win a full sweep and implement drastic new tax hikes. However, our quant model still favors them to win the White House and just upgraded their odds. While we expect equity volatility around the election, investors do not need to worry about corporate tax hikes.

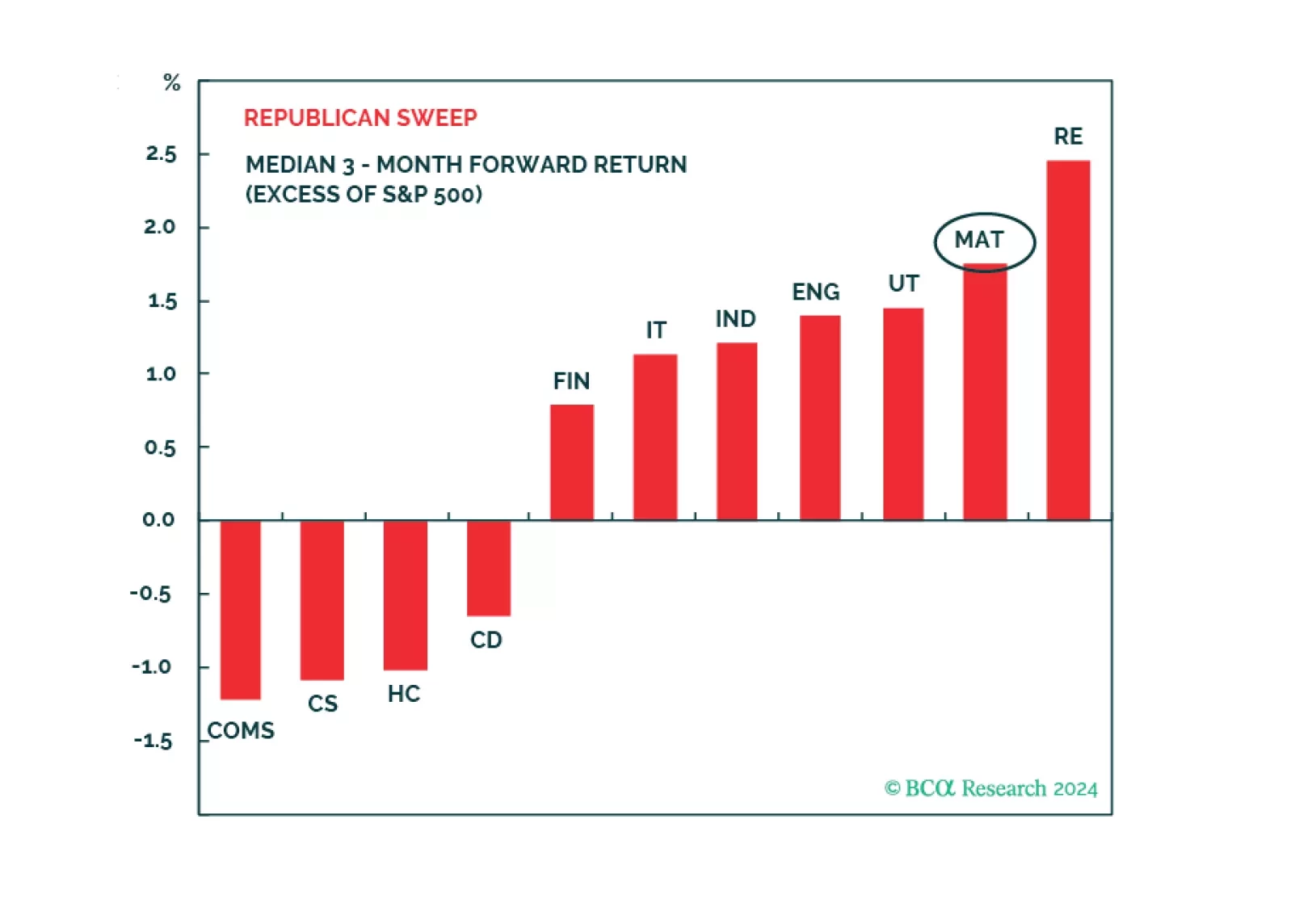

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

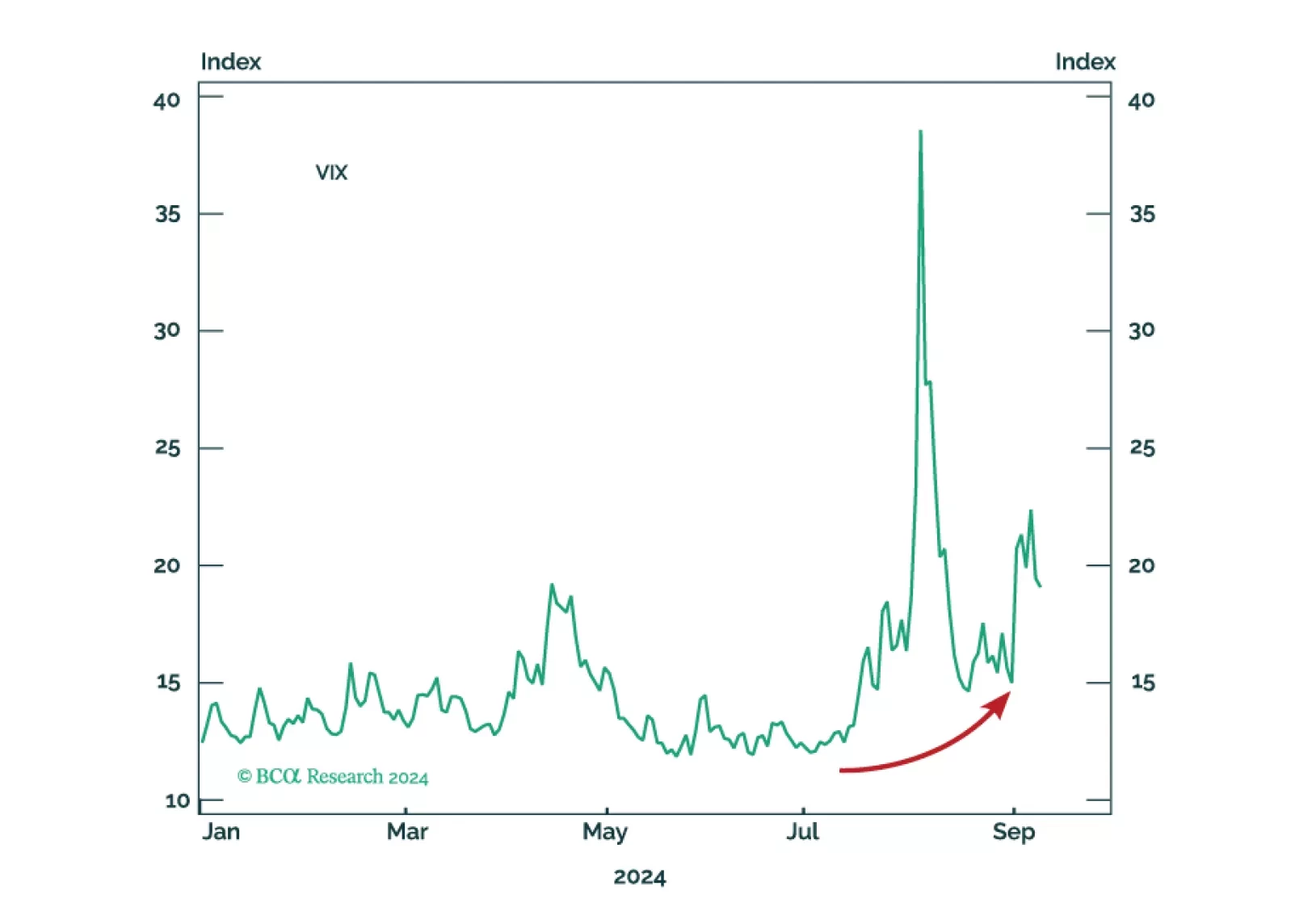

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

Harris picked Walz to patch up her weak side in the electorally vital Midwest. But the US election will continue to weigh on risk appetite, stocks, and high-beta assets because the odds of a single-party sweep are at least 50%, probably higher. Policy uncertainty and risk premiums will rise, not fall, in the coming months.