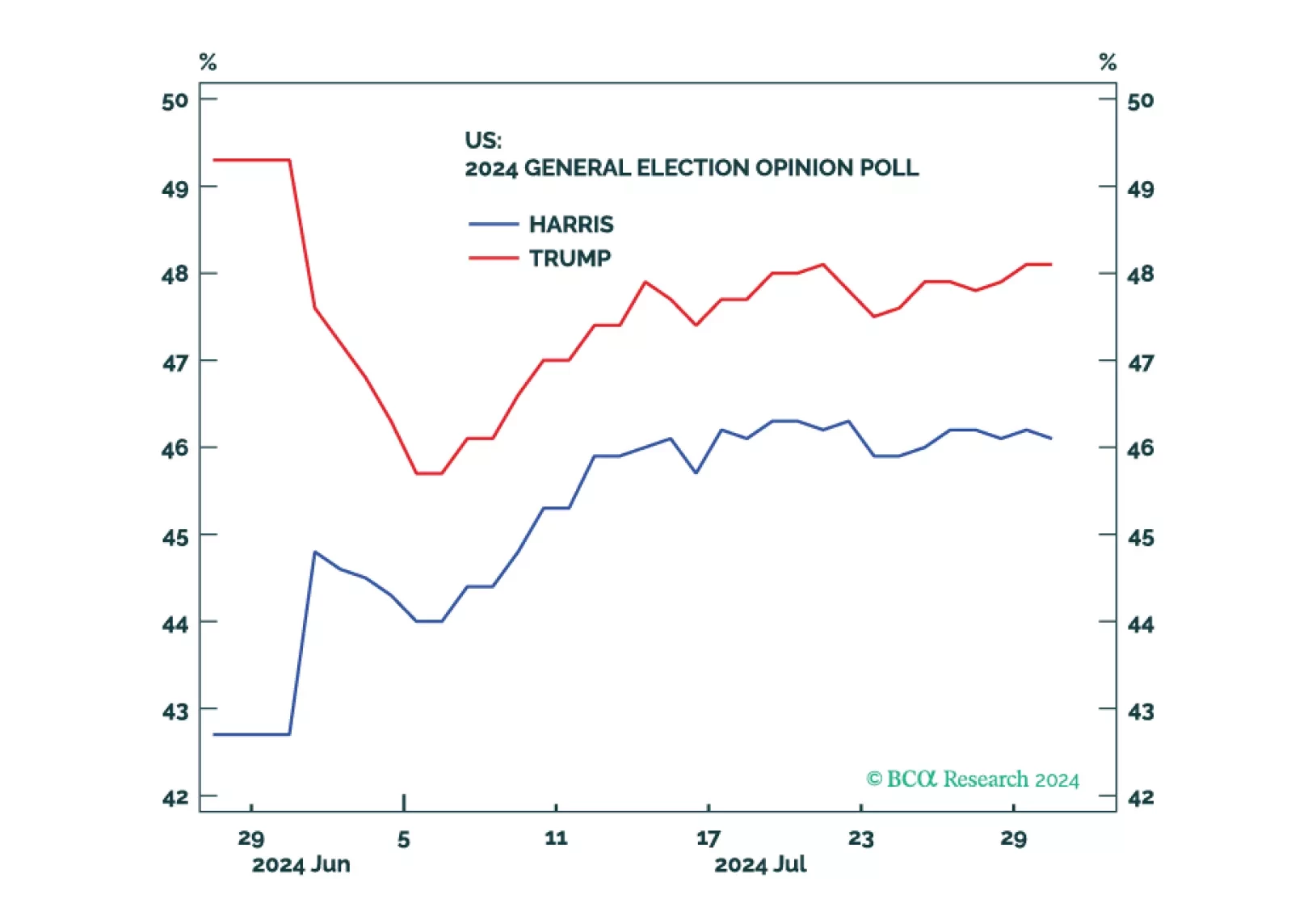

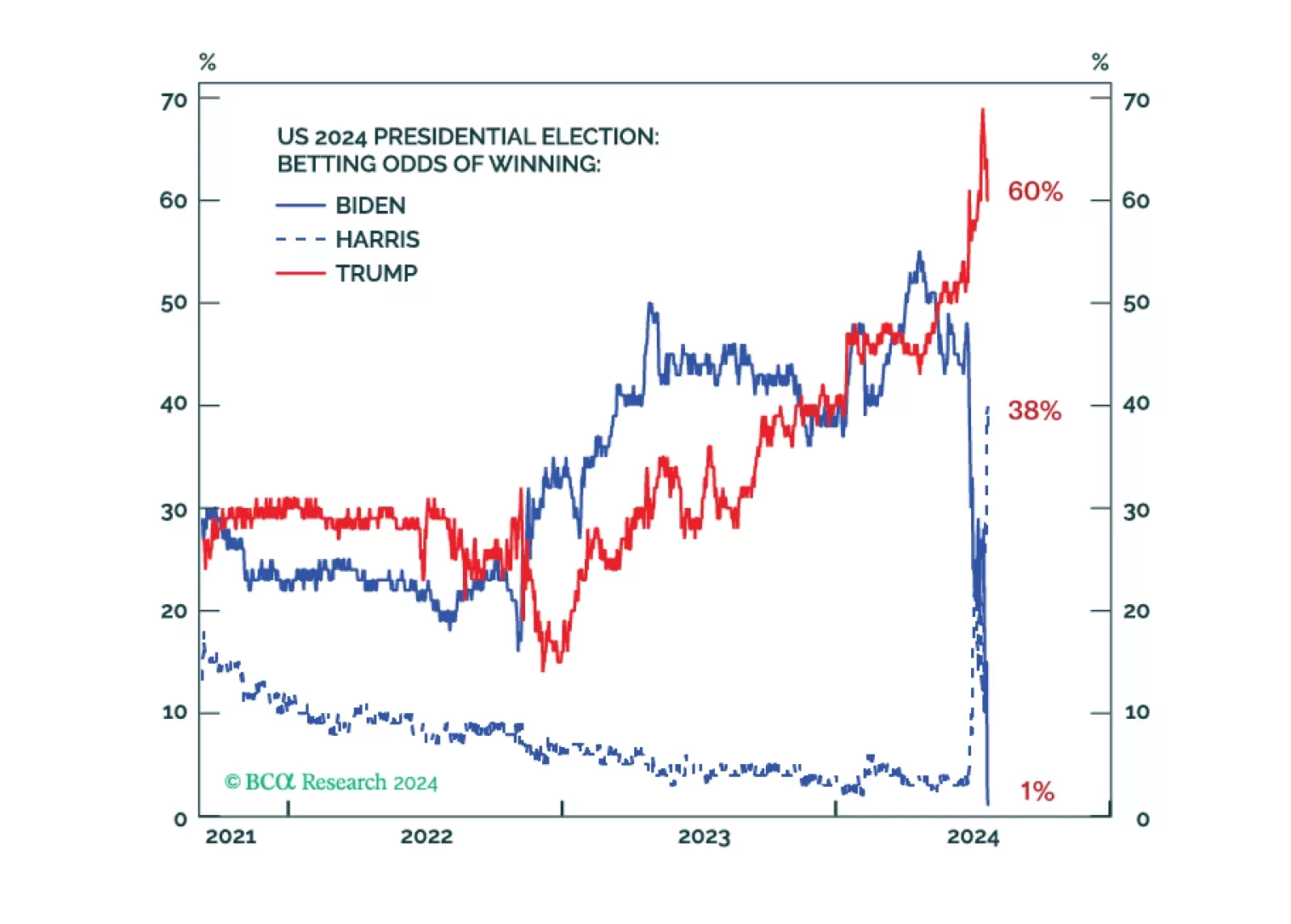

US Election

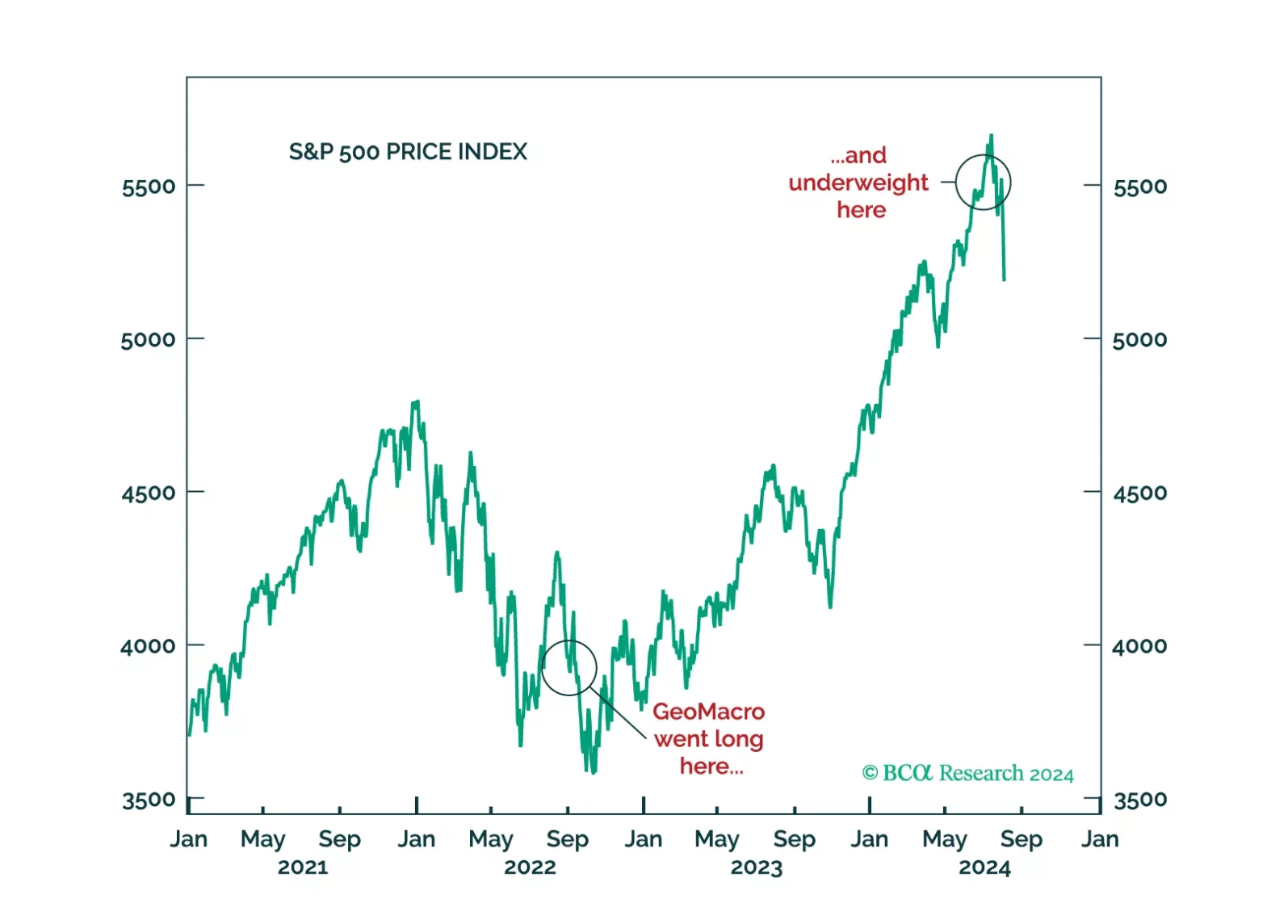

The decision by GeoMacro team on July 2 to short USDJPY and underweight equities has proven to be prescient. We still do not like the market setup from here on out. A recession would, obviously, be negative for risk assets. But even if investors avoid that scenario, the transition from cash- to leverage-driven growth is unlikely without a significant Fed rate-cutting cycle.

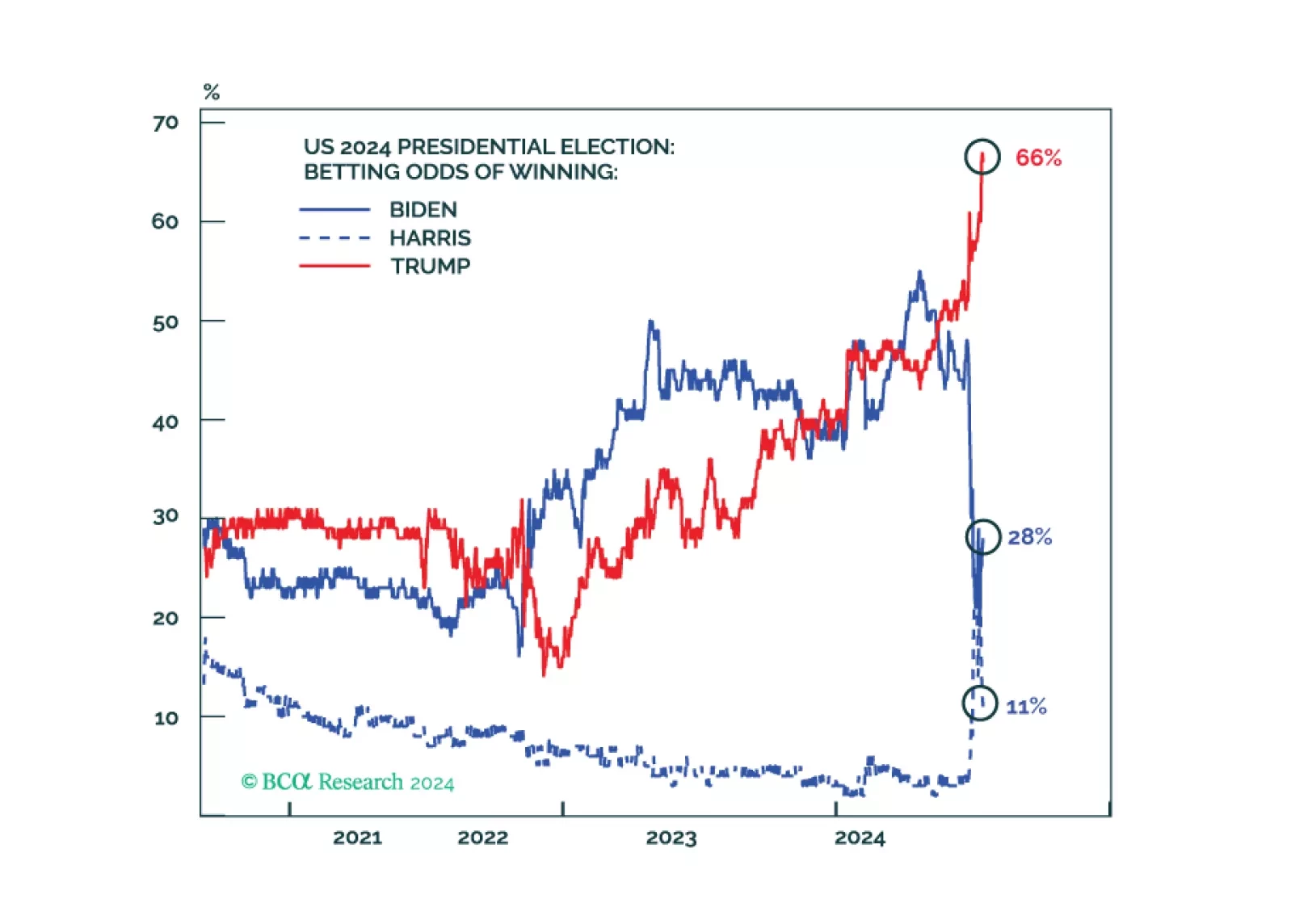

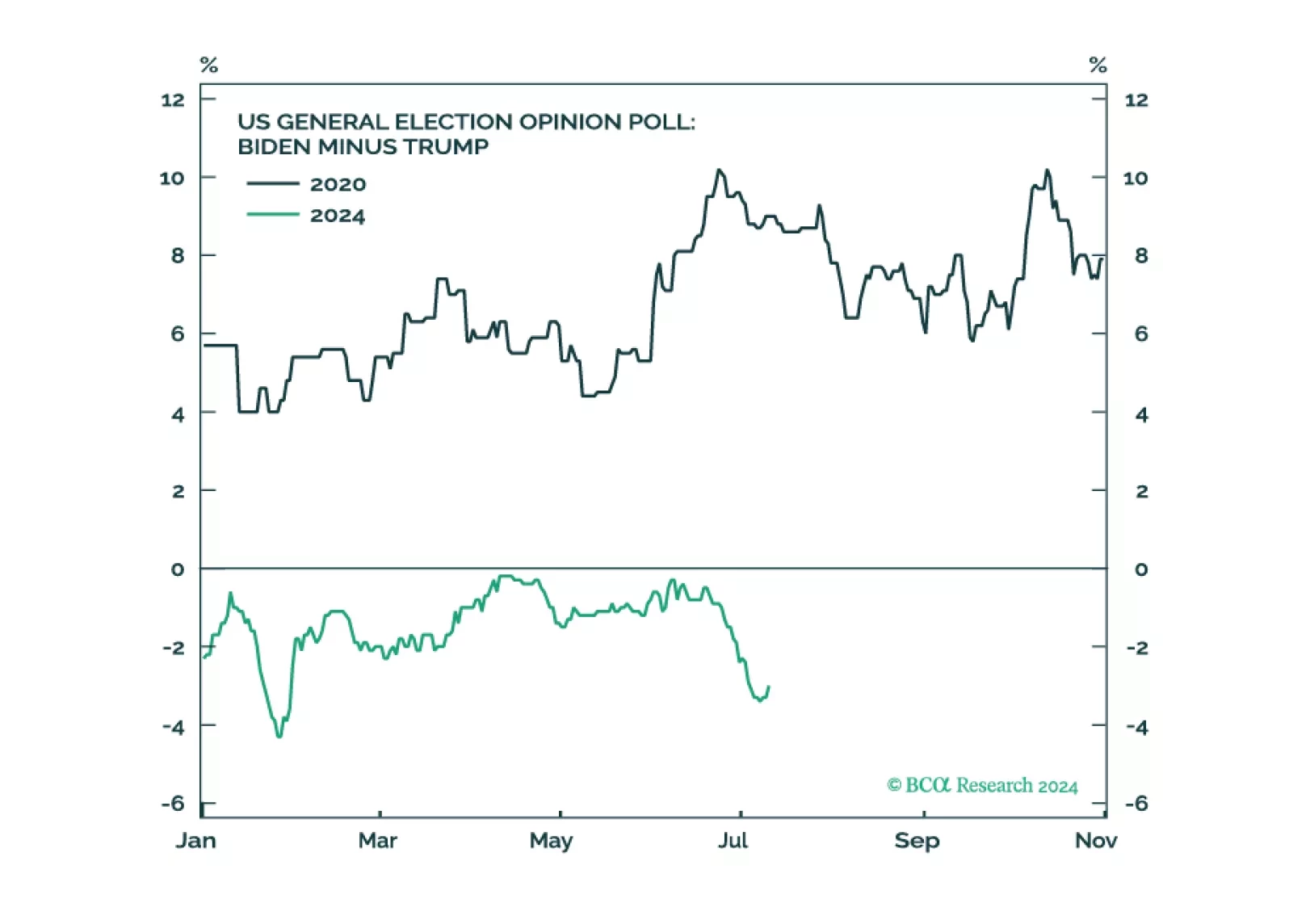

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.

President Biden has announced his withdrawal from the presidential race. The news will no doubt come to dominate the news cycle in the upcoming week of July 22, which is unfortunate as it will drown out some important developments from the preceding week.

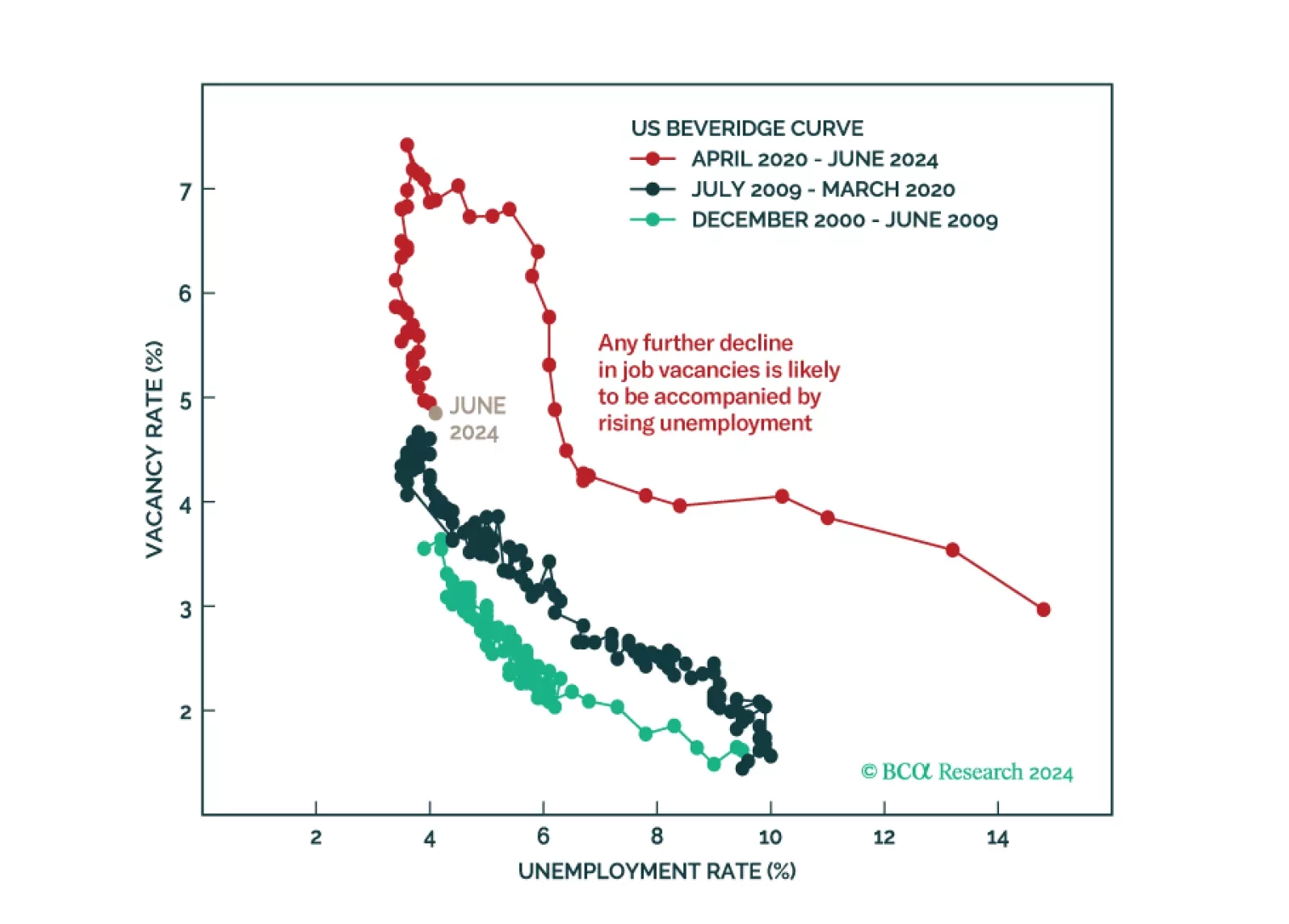

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

The cyclical economy is slowing today. Republicans are now more likely to win a full sweep, crack down on immigration and trade, and at least modestly stimulate the economy. Uncertainty and volatility will rise.

Today’s attempted assassination against President Trump challenges the consensus view. It will ensure that President Trump’s supporters are highly motivated for the upcoming general election. And it may return many supporters who had drifted away from the former president back into the fold.

The conventional wisdom is wrong: Trump is not going to substantially cut taxes once in office; he is going to raise taxes by jacking up tariffs. To the extent that this dampens economic activity, it is bad news for stocks but good news for bonds.

We have turned cautious on equities for the first time since August 2022. Our end-of-the-year target for 2024, 5,500 on the S&P 500, has been reached. From here on out, any upside is gravy. However, we worry about US – not European – politics. In fact, we think investors could profit from the recent selloff in France. The real risks are in the US.

In our Volume I – The Alpha Report – we posit that the French bond market reaction is a mere amuse bouche for what is coming to the US. All year, we have warned investors that US politics could induce a bond market riot. This moment is nigh. Act accordingly!