United States

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

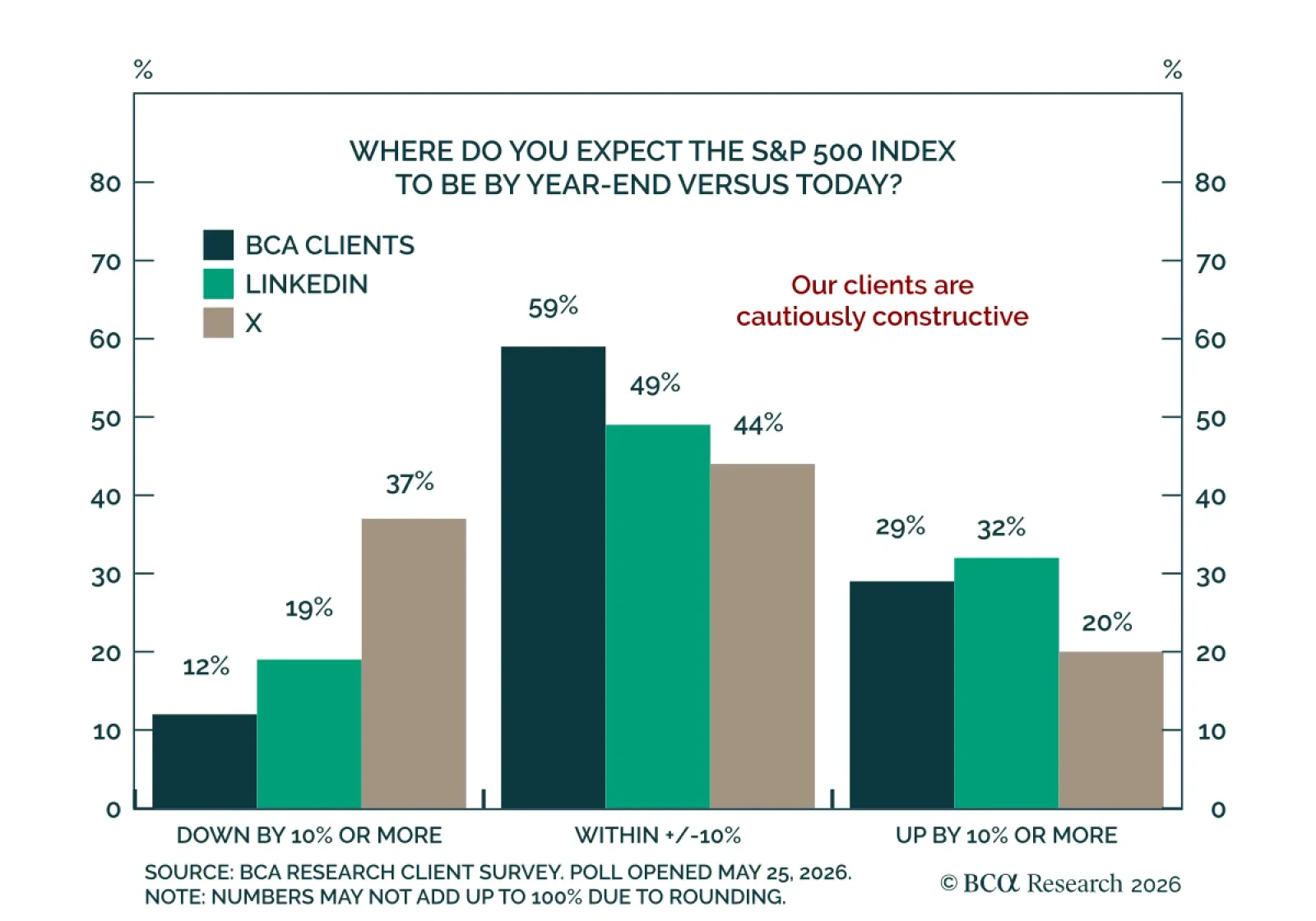

Our Portfolio Allocation Summary for June 2026.

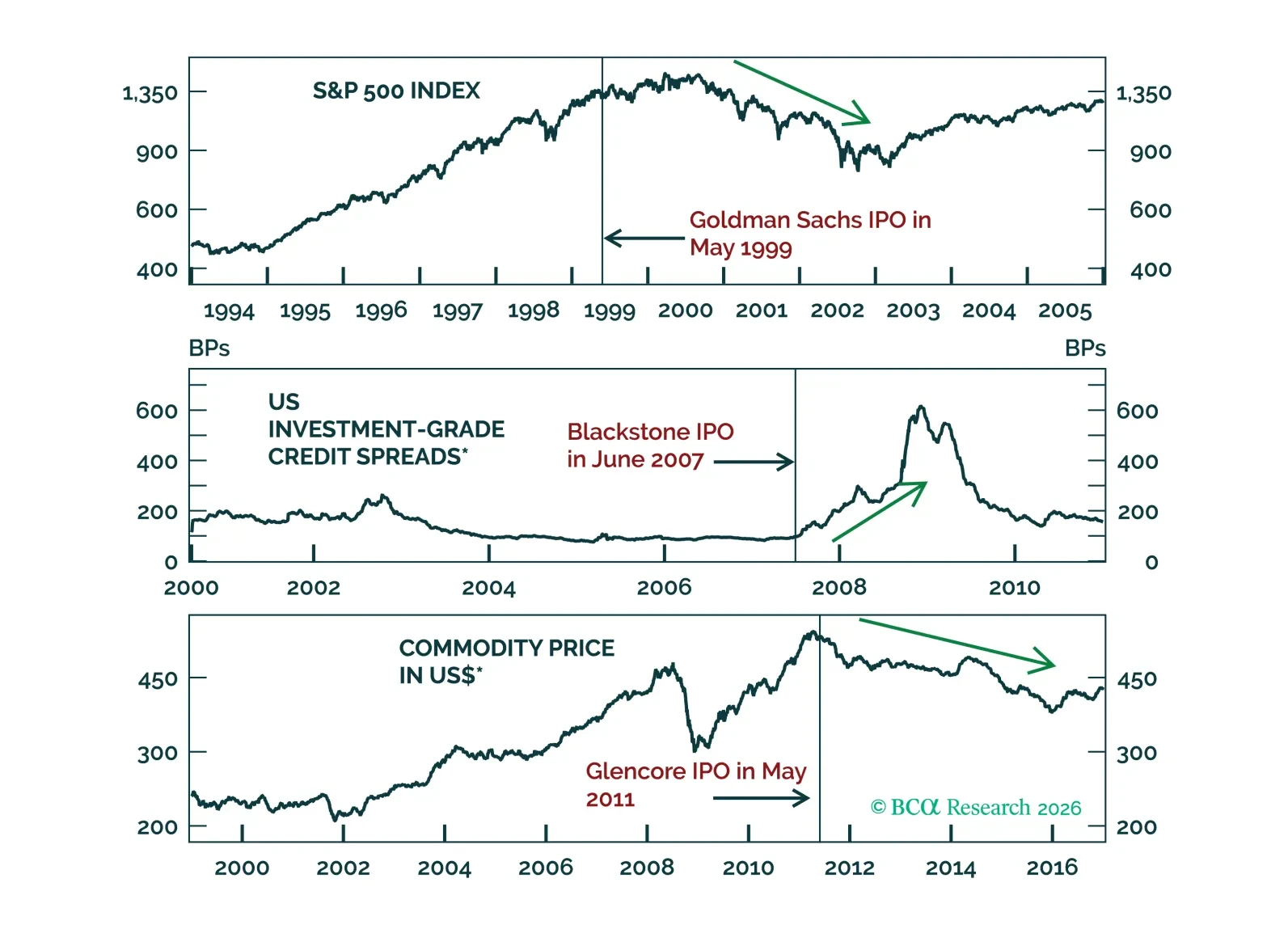

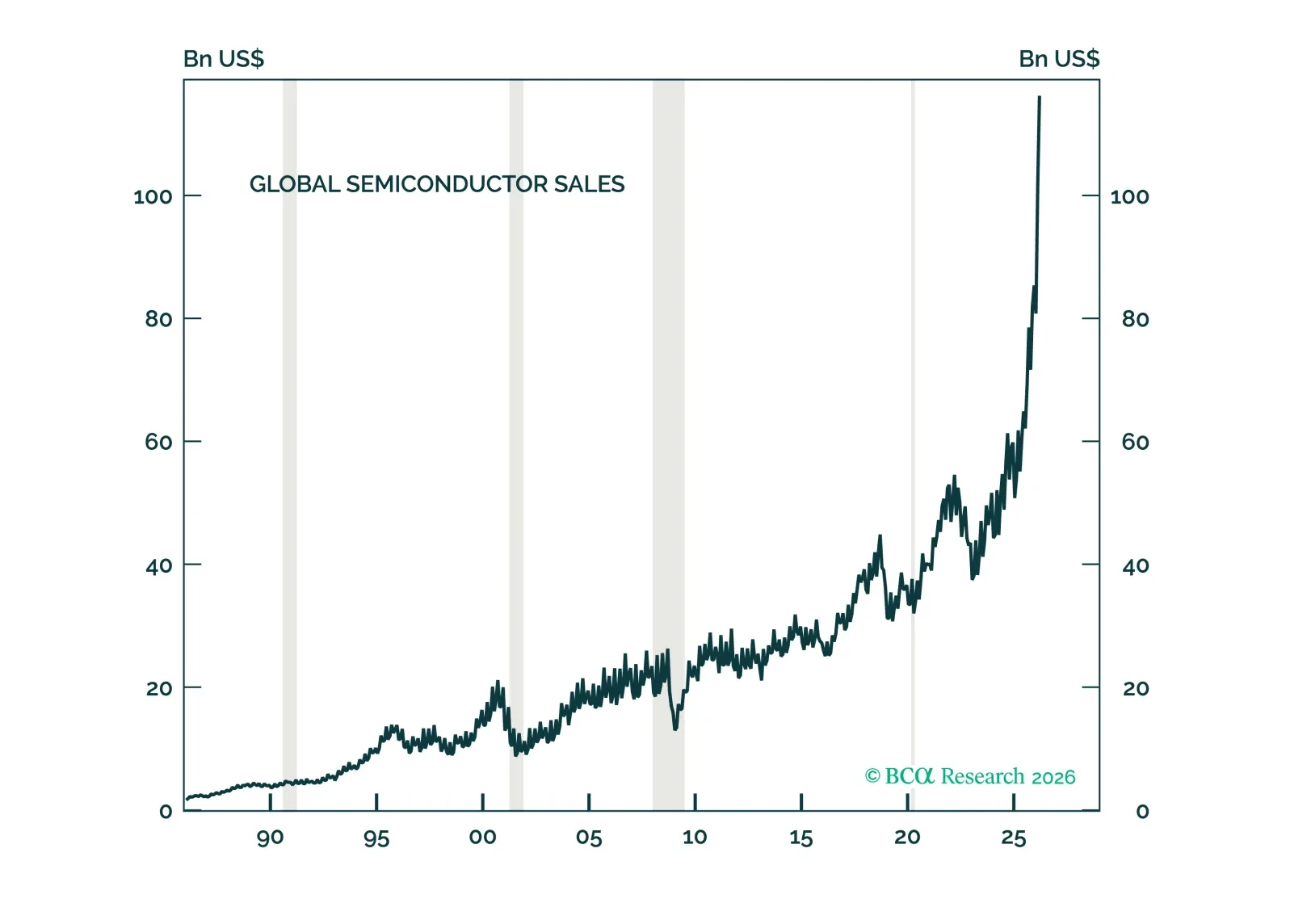

The magnitude of US tech/AI capital spending already rivals past bubble thresholds, threatening hyperscalers’ future returns on capital. There are echoes of previous market tops. Our preferred overlay strategy for equity portfolios remains long semiconductor producers / short hyperscalers.

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.