United States

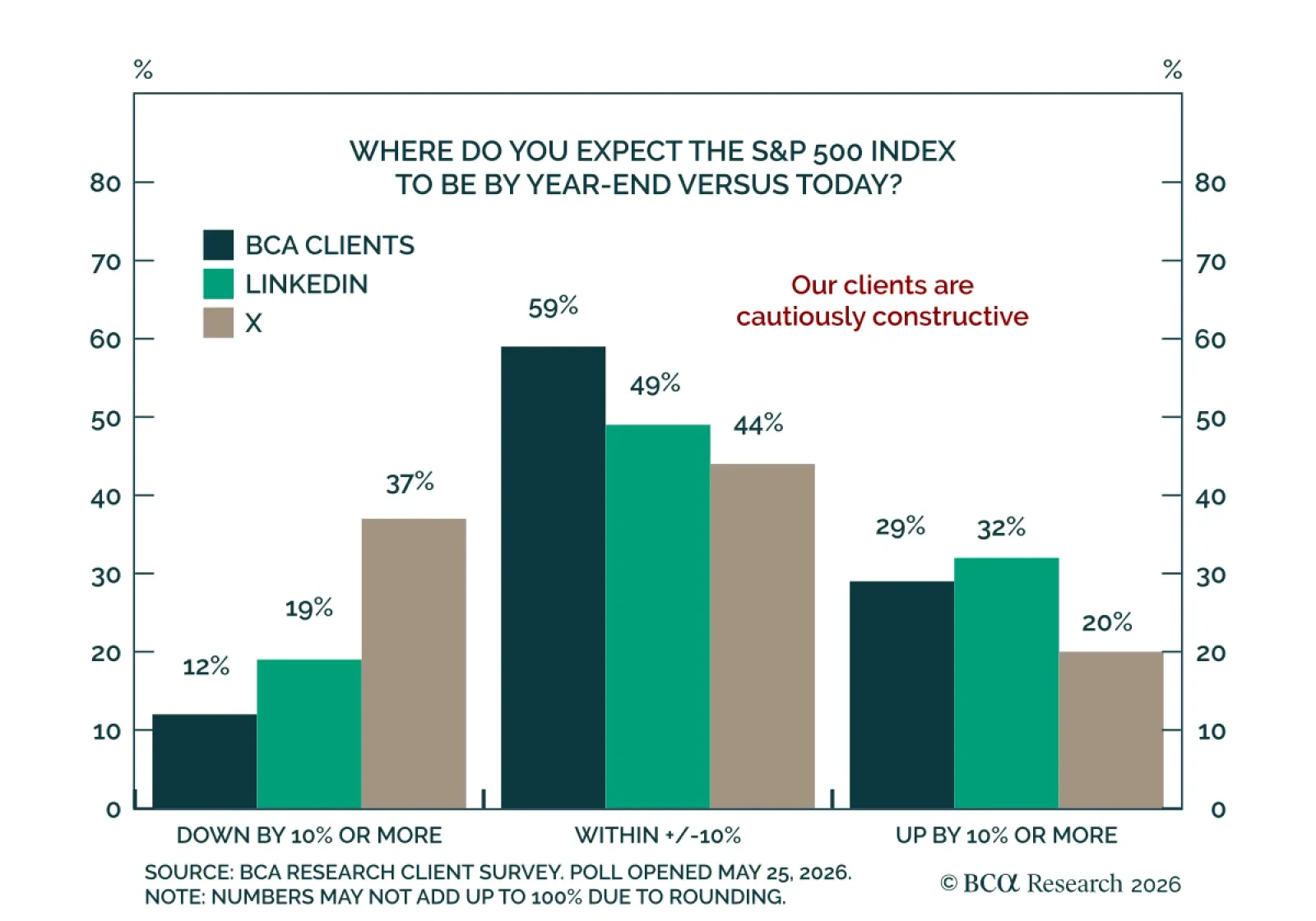

Our clients are cautiously optimistic about US equities through year-end. In last week's poll, we asked where respondents expect the S&P 500 to finish by year's end. BCA clients were the most constructive: 59% expect the index to stay within ±10% of…

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

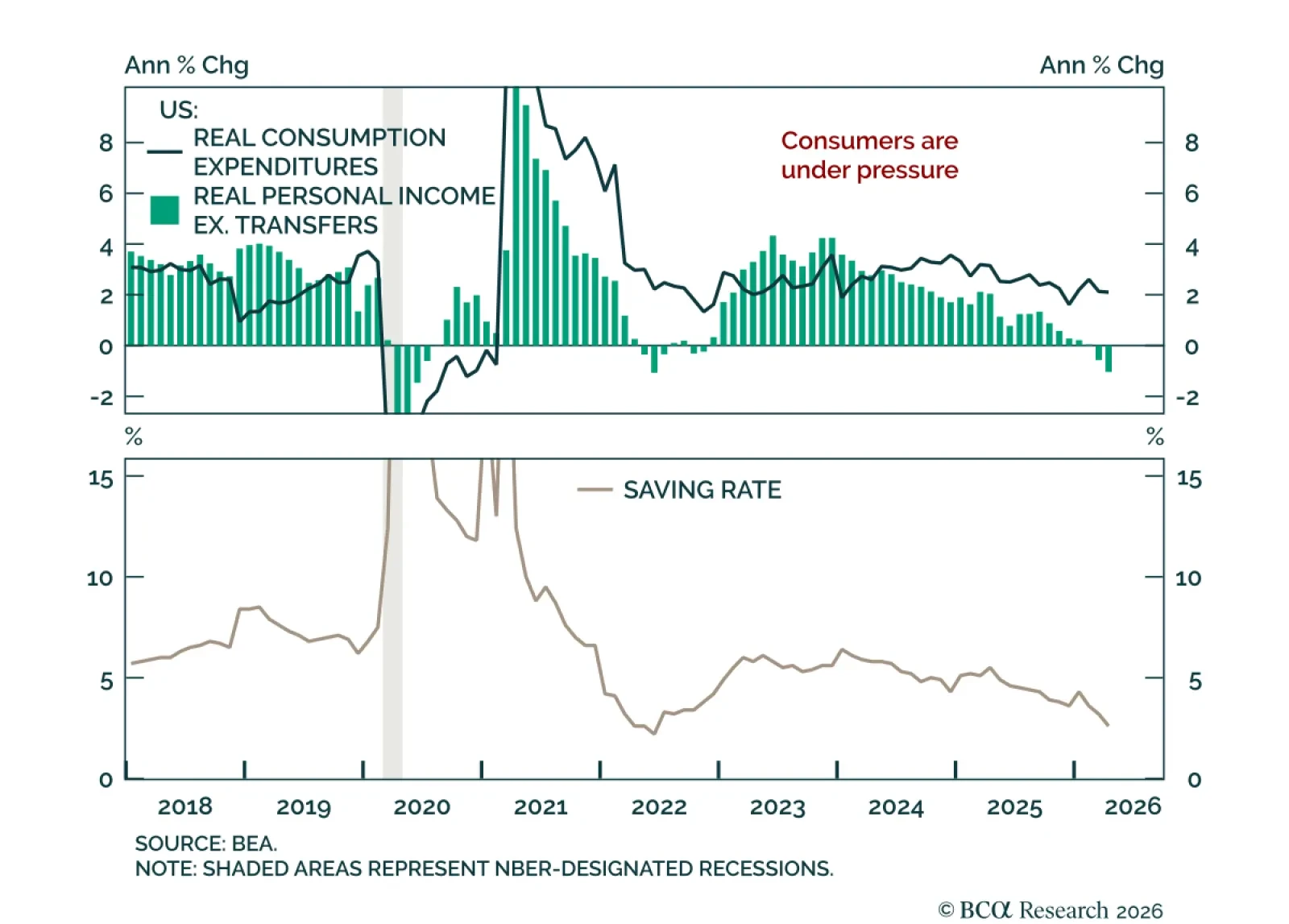

US demand is cooling as income growth falls behind spending. Q1 real GDP was revised down by 0.4 percentage points to 1.6%, mainly on weaker consumer spending and inventory investment. The April Personal Income & Outlays report confirms the softer…

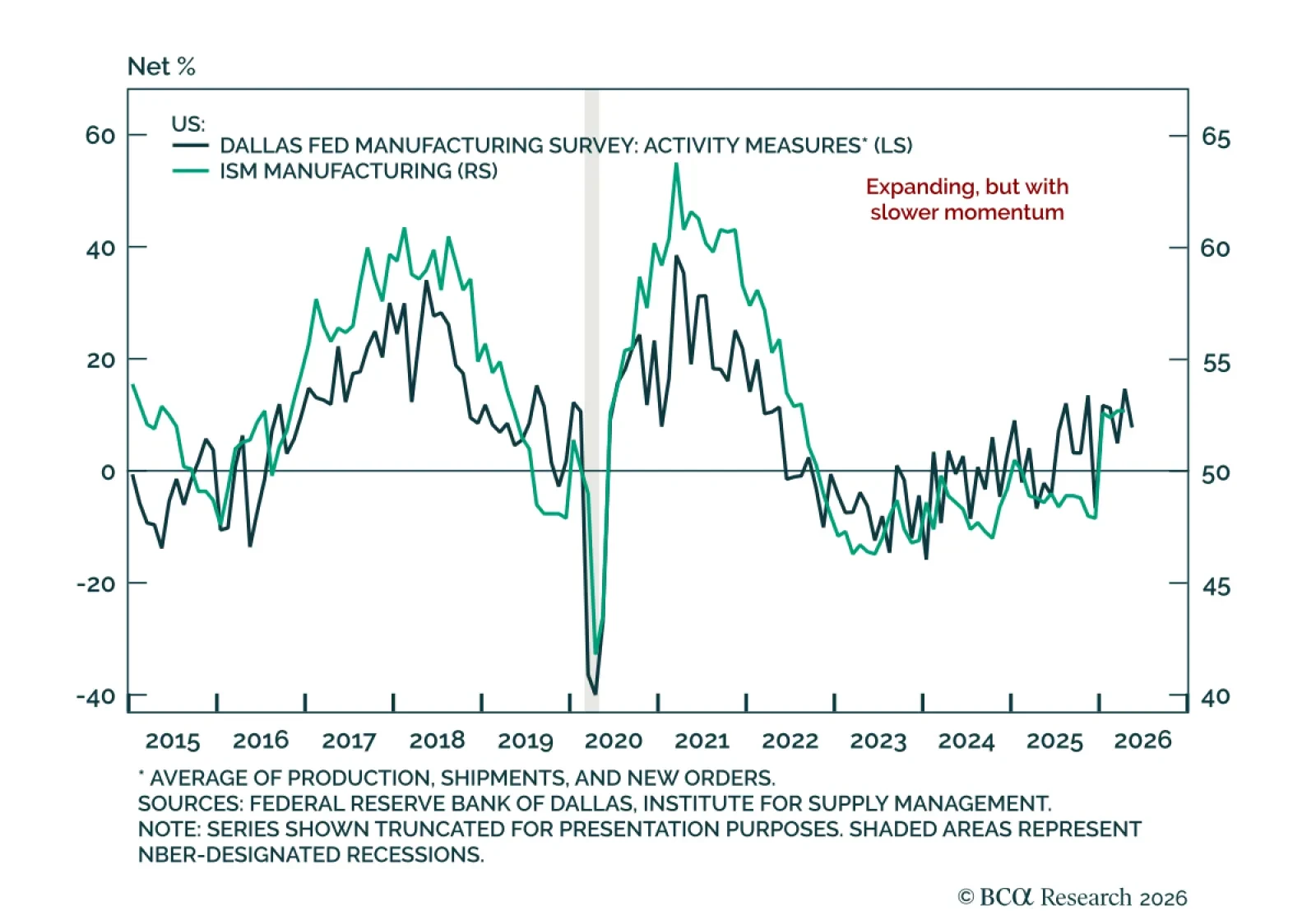

The Dallas Fed survey points to Texas manufacturing continuing to expand in May, but with slowing momentum. The production index fell 10 points to 9.4, signaling an average pace of output growth rather than a broad acceleration. The softer tone showed up…

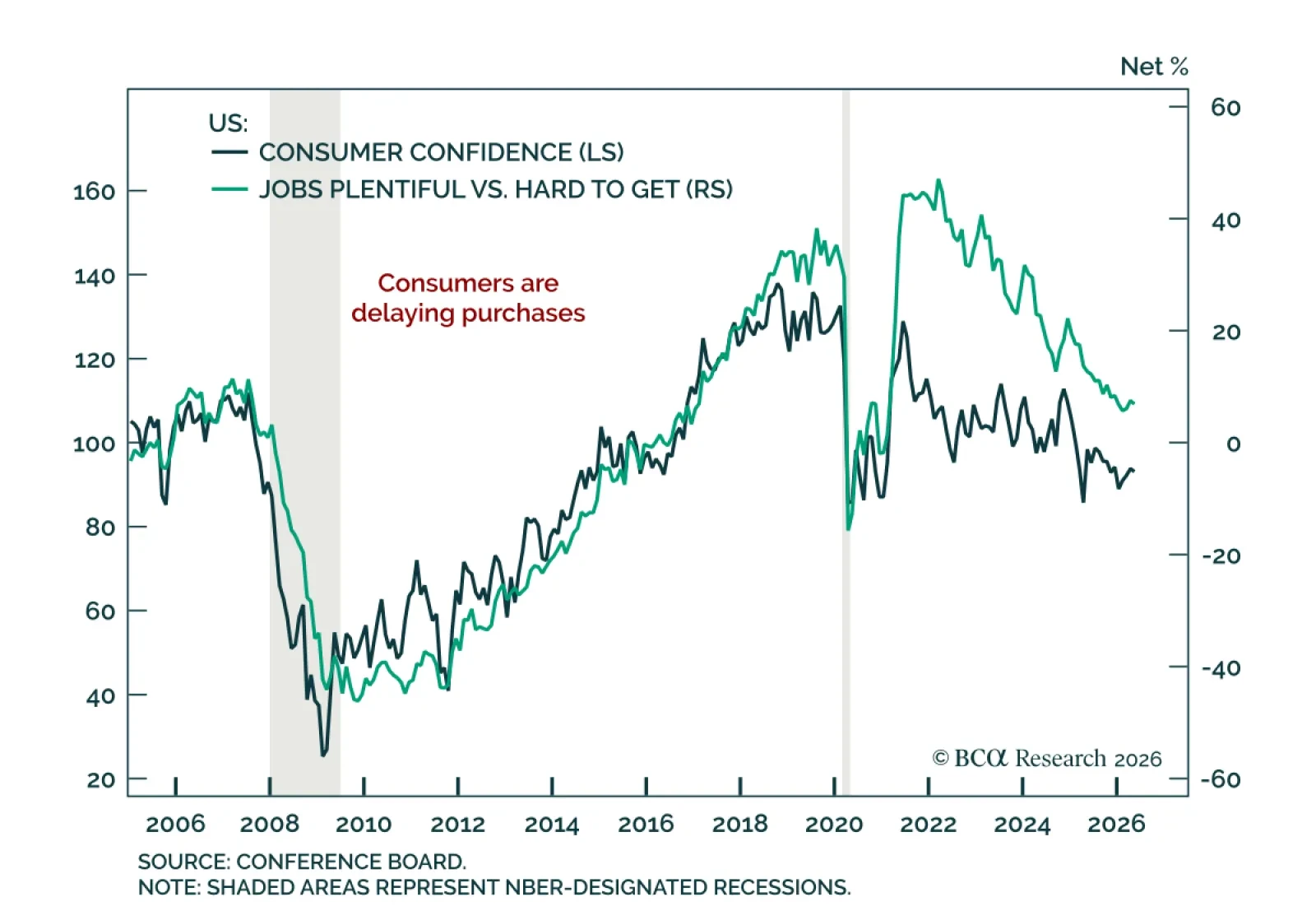

US consumer confidence softened marginally in May as high oil prices kept inflation pressure in focus. The Conference Board Consumer Confidence Index slipped to 93.1 from an upwardly revised 93.8 in April, but still came in slightly above…

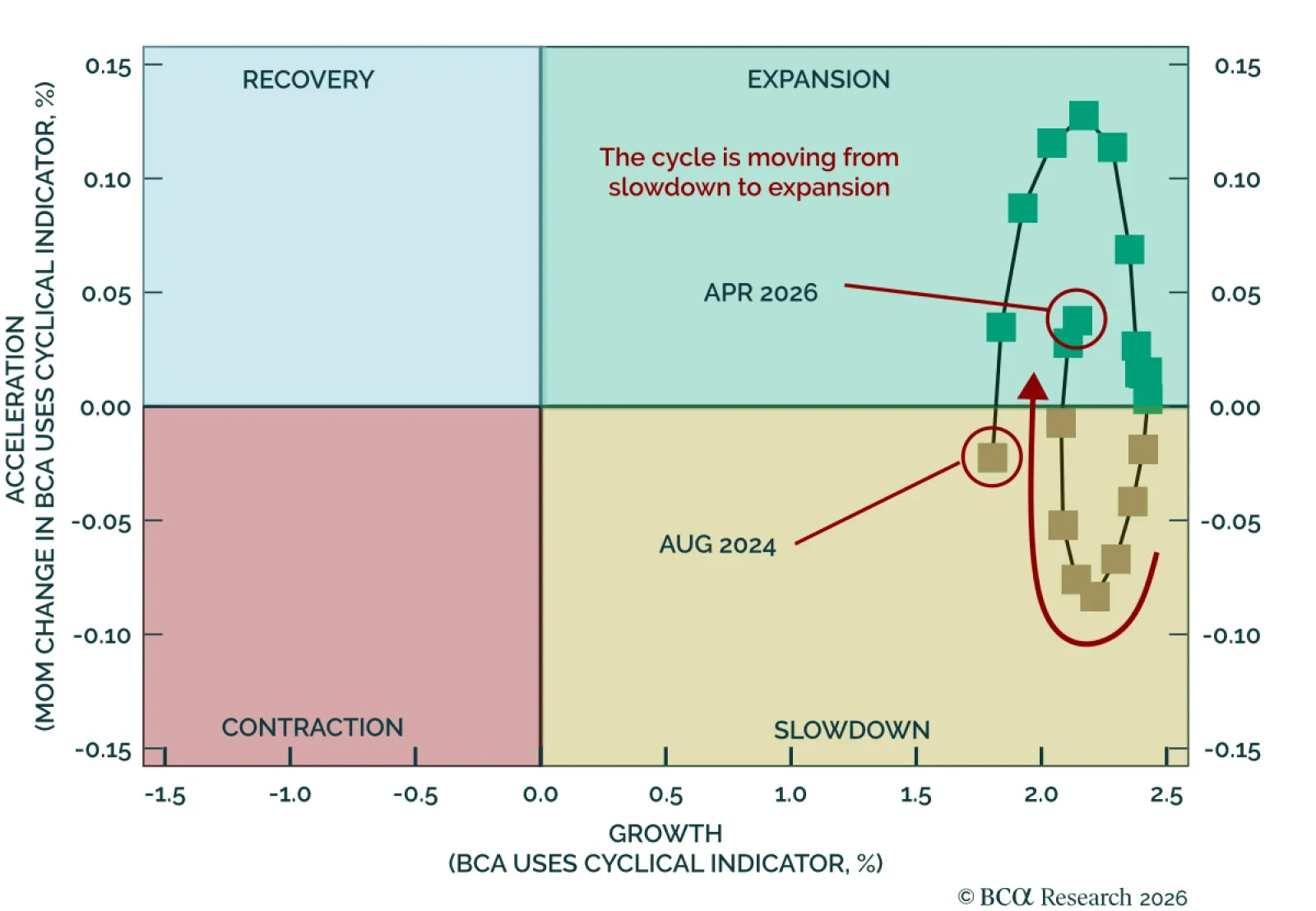

Our US Equity strategists remain bullish as their proprietary cyclical indicator shows US growth is modestly improving. The turn is being led by business-side indicators, while consumer and labor-market signals remain soft. Historically, expansion phases have…

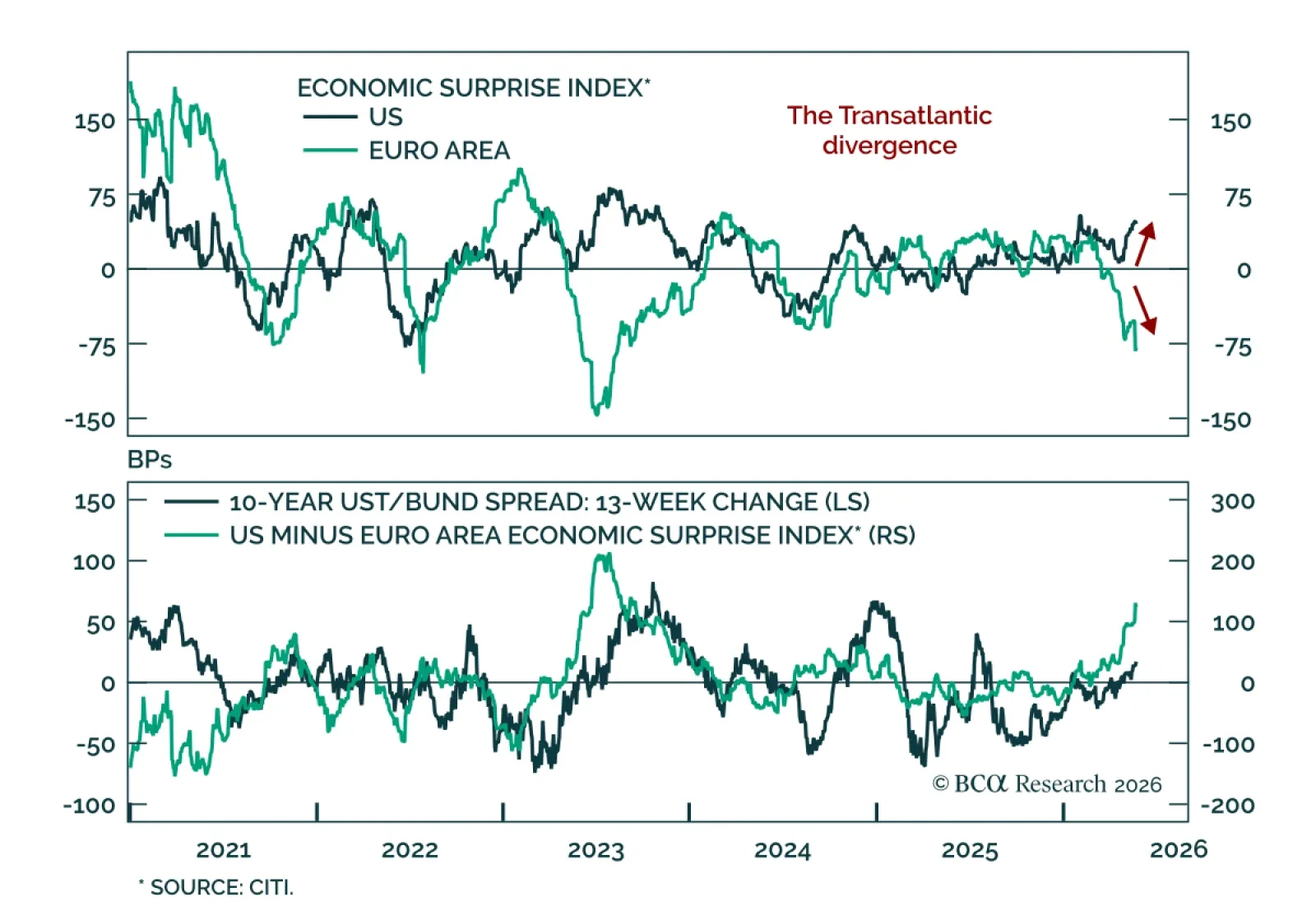

Go long German 10-year Bunds versus US 10-year Treasuries as US resilience diverges from euro area weakness. The trade is backed by a widening growth gap, with the US better insulated from rising oil prices and the euro area losing momentum. The US…

Against the earnings-versus-everything-else market backdrop, stellar earnings are easily outweighing elevated oil prices, rising yields and the increased probability that the Fed may hike rates before the year is out. US allocators should remain invested in equities.

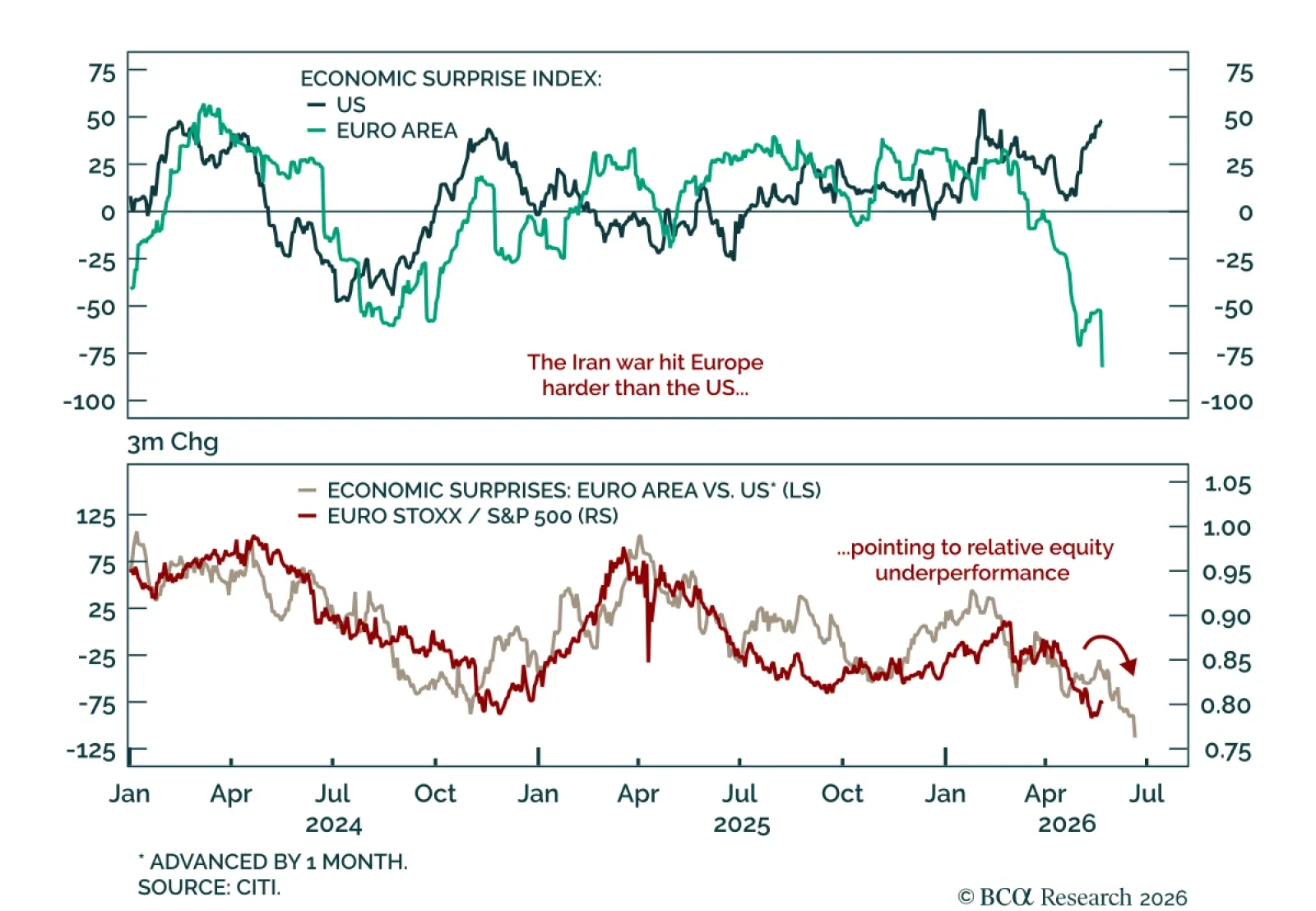

Relative macro momentum still favors the US over Europe. Our tactical framework rests on two ideas: the feedback loop between financial conditions and economic data surprises, and the impact of macro momentum on markets. In Europe, momentum had already…

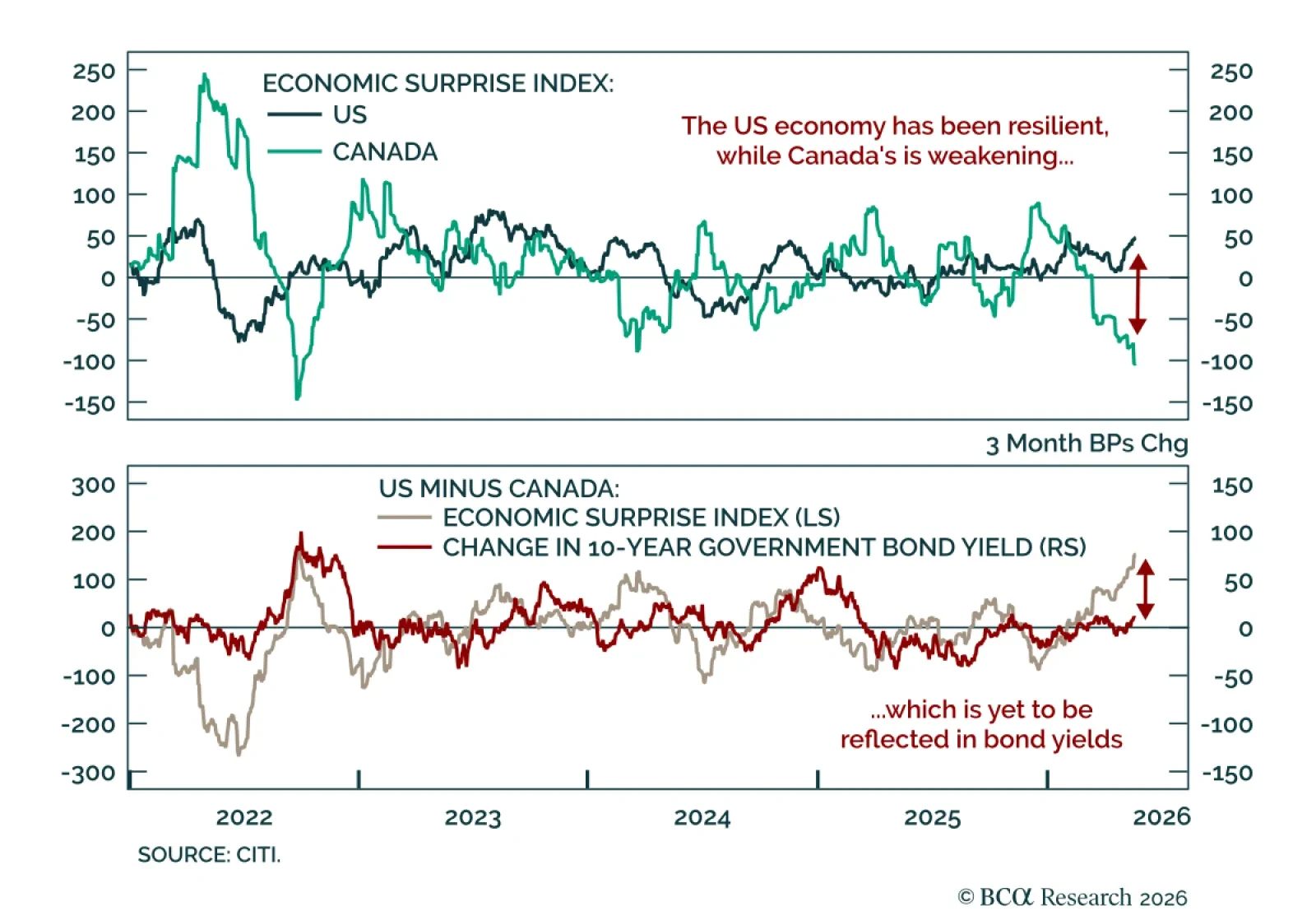

The US and Canada face increasingly different macro backdrops, and that divergence should support Canadian bonds versus Treasuries. US data has stayed resilient, surprising positively and showing growth momentum. Meanwhile, Canadian data has increasingly…