United States

The ISM services PMI surprised positively in July. The headline index expanded 2.6 ppts to 51.4, reversing May’s fastest pace of contraction in four years. Notably, the business activity subcomponent increased 4.9 ppts to 54.5, new orders and new export…

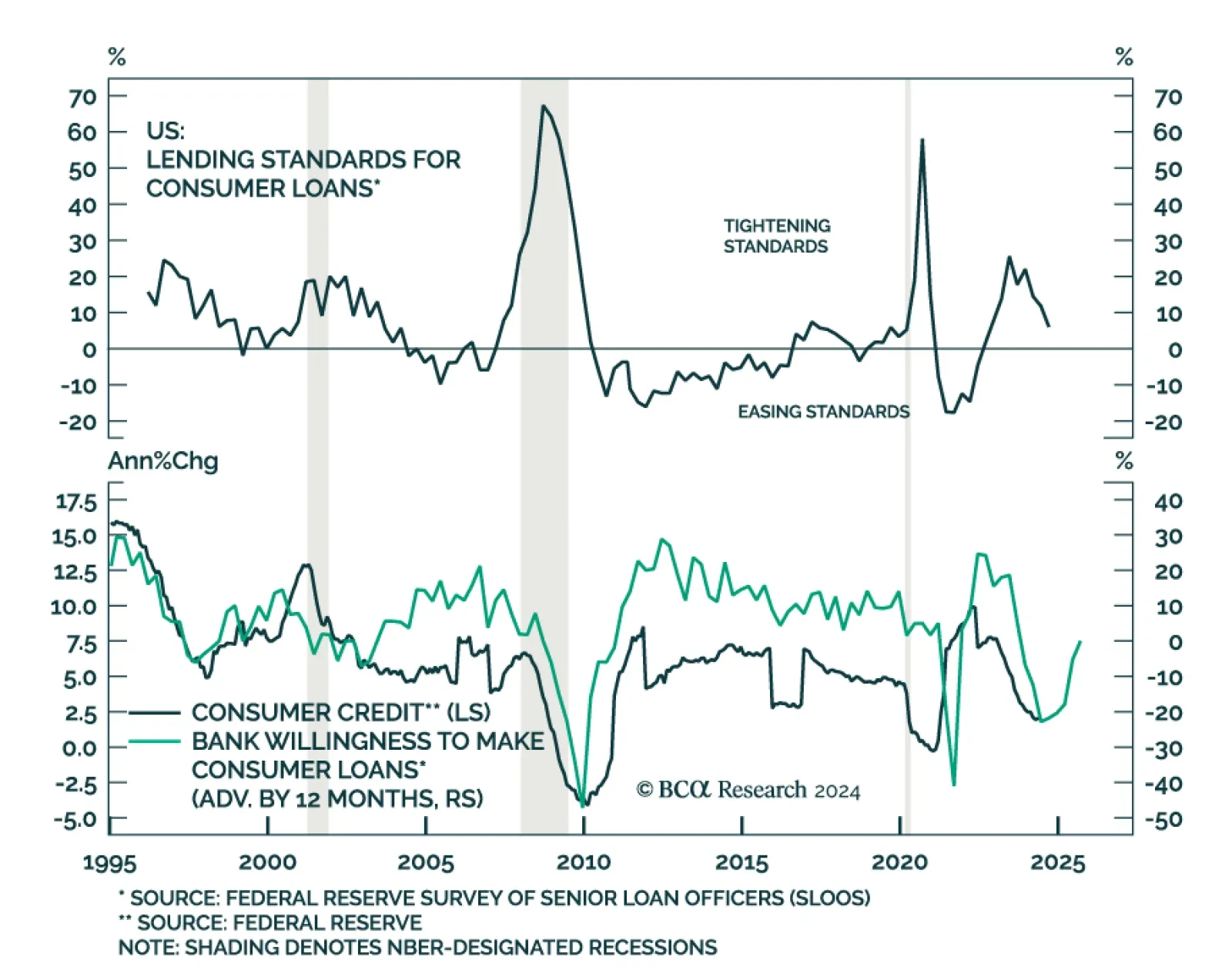

Lending standards continued to tighten for most loan categories in Q2, according to the Senior Loan Officer Survey (SLOOS). US banks reported tightening lending standards to businesses and all CRE categories. They kept standards mostly unchanged compared…

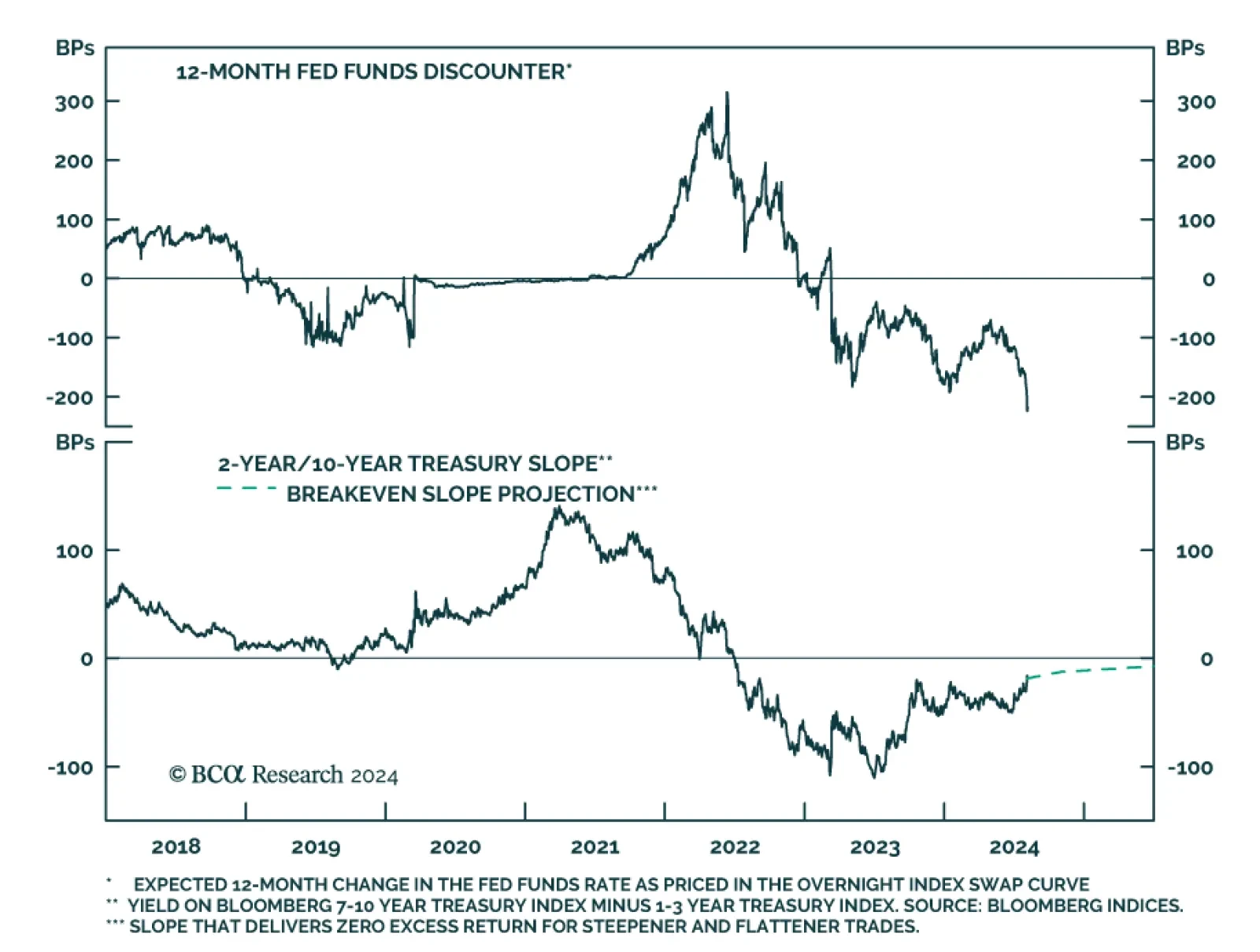

According to BCA Research’s US Bond Strategy service, Friday’s employment report caused financial markets to price-in some recession risk for the first time in months. The Treasury curve bull-steepened in July, a move that accelerated after Friday’s negative…

Our Portfolio Allocation Summary for August 2024.

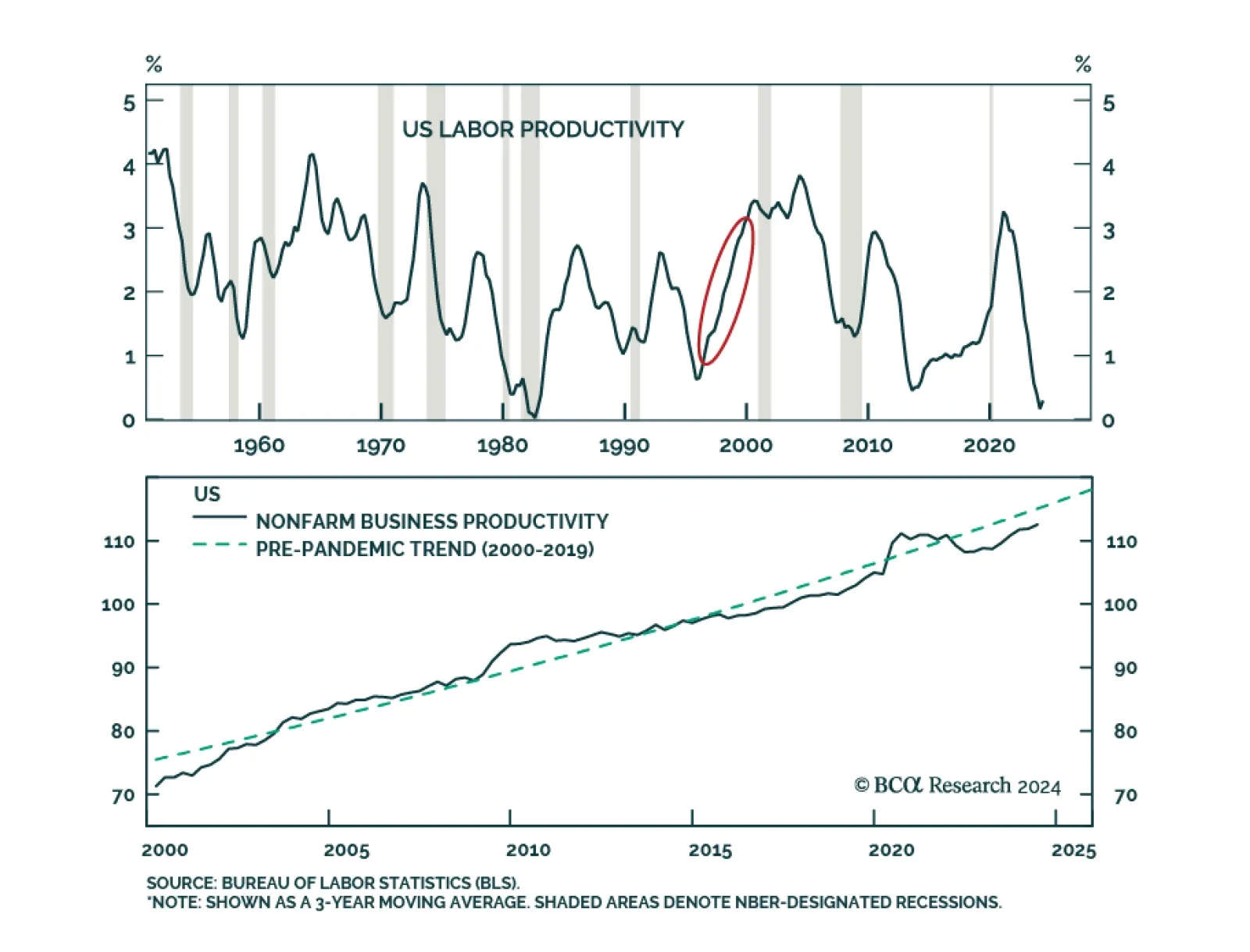

We have previously highlighted that an upside surprise in China’s fiscal stimulus as well as an AI-triggered jump in US productivity could potentially prolong the expansion, and constitute two key risks to our recession view. Recently announced government…

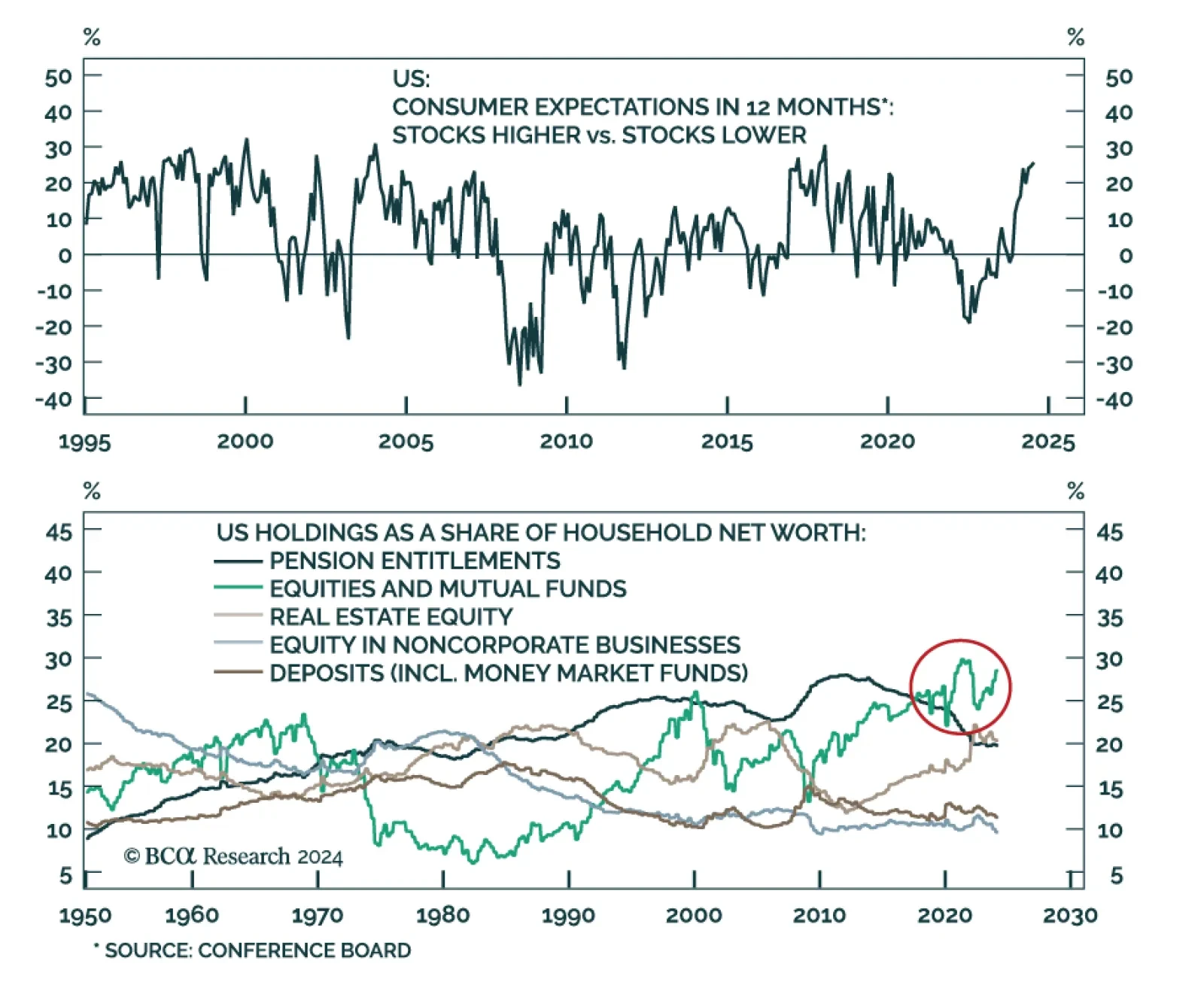

The latest Conference Board measure of consumer confidence suggested that consumers were increasingly downbeat about current economic conditions. Notably, their fading optimism about labor market conditions drove the jobs-plentiful-minus-hard-to-get measure…

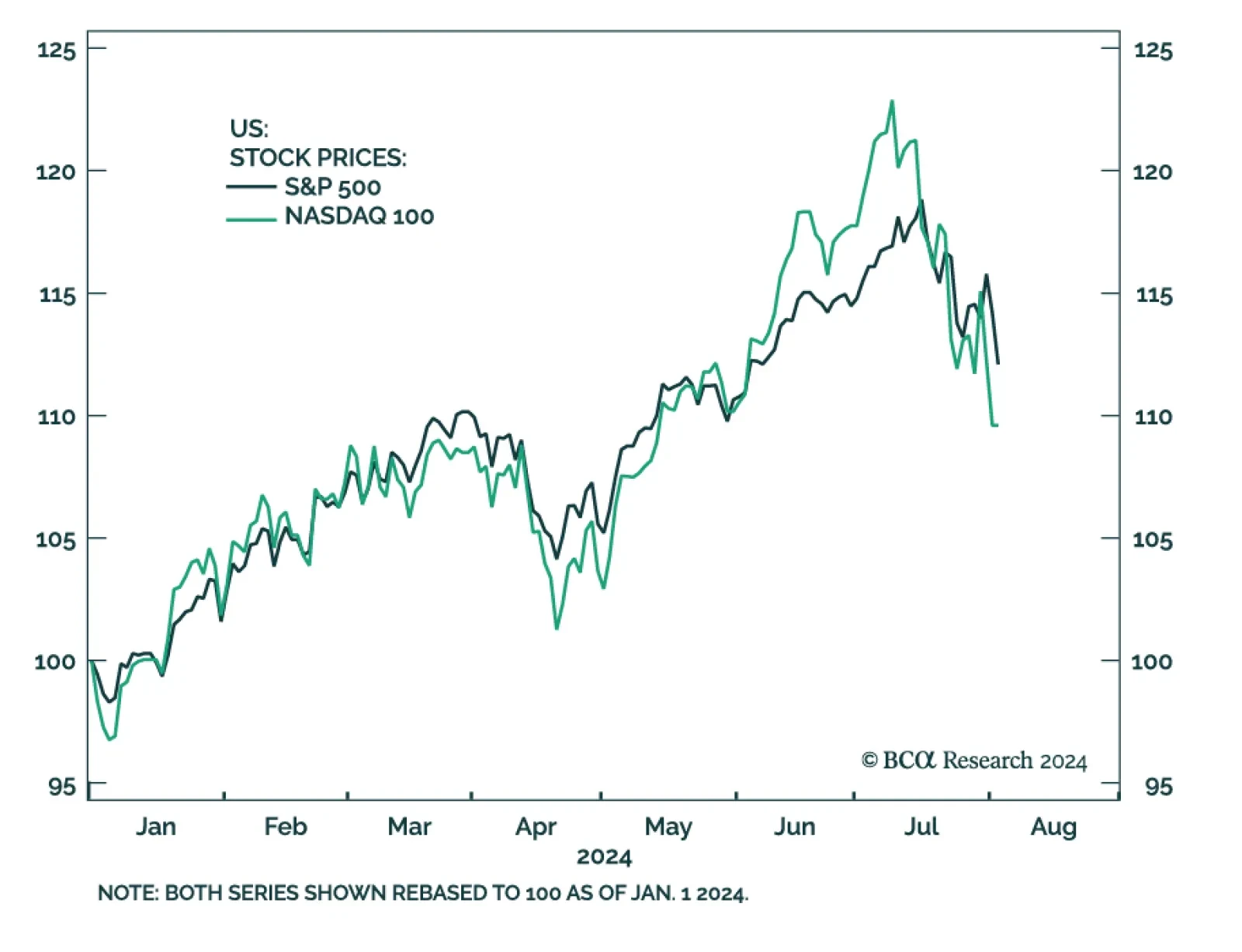

August’s selloff has featured a rotation out of Big Tech. The Nasdaq shed 8% across Thursday, Friday, and Monday, led by concentrated selling among several Mega caps. Nvidia, Tesla, Microsoft and Amazon shed 14%, 14%, 6% and 14% over the last three sessions,…

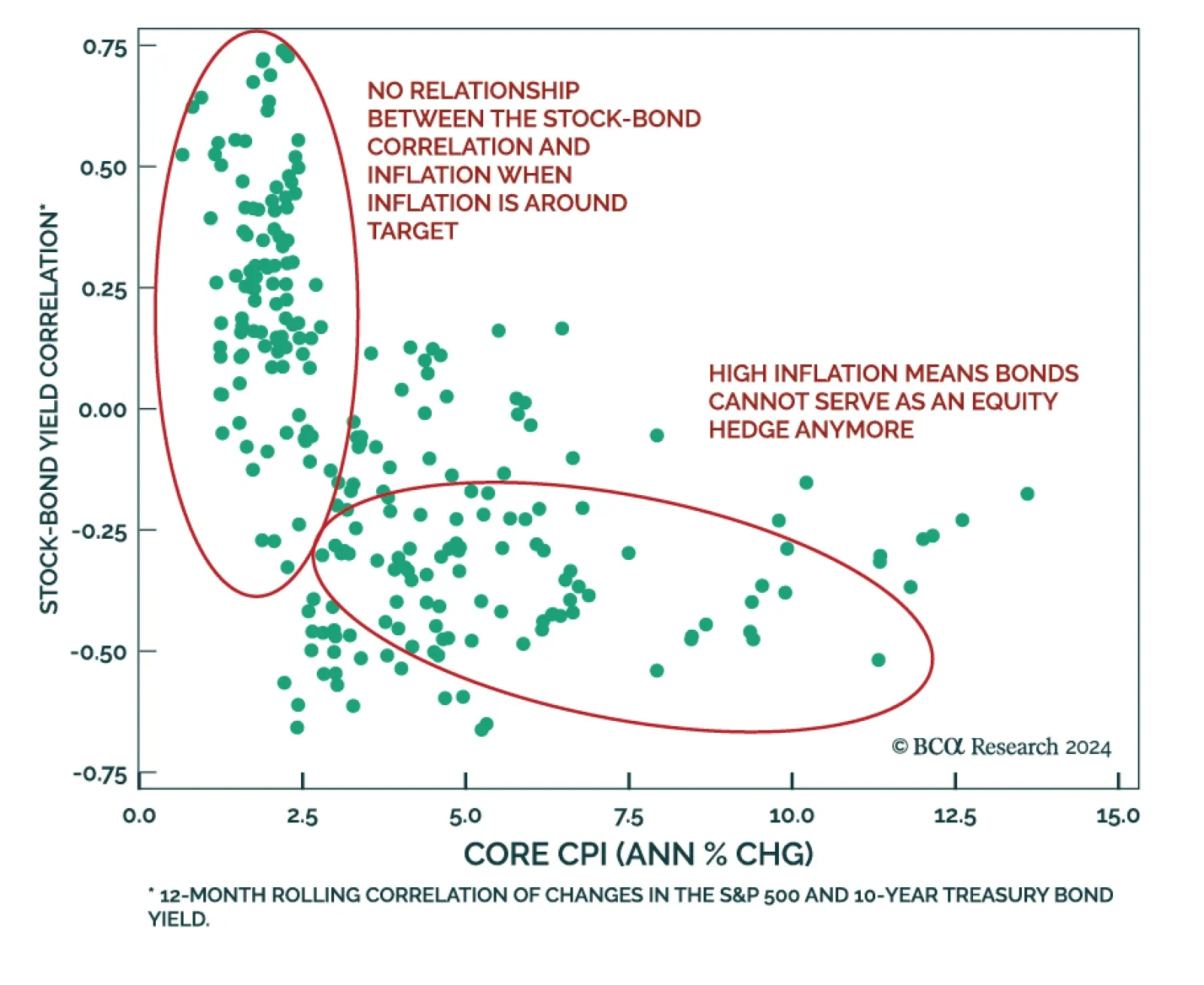

According to BCA Research’s Global Asset Allocation service, while the market action of the past few weeks is pointing to a return to a negative stock-bond correlation, more prints will be needed to confirm things are getting back to normal. The post-COVID…

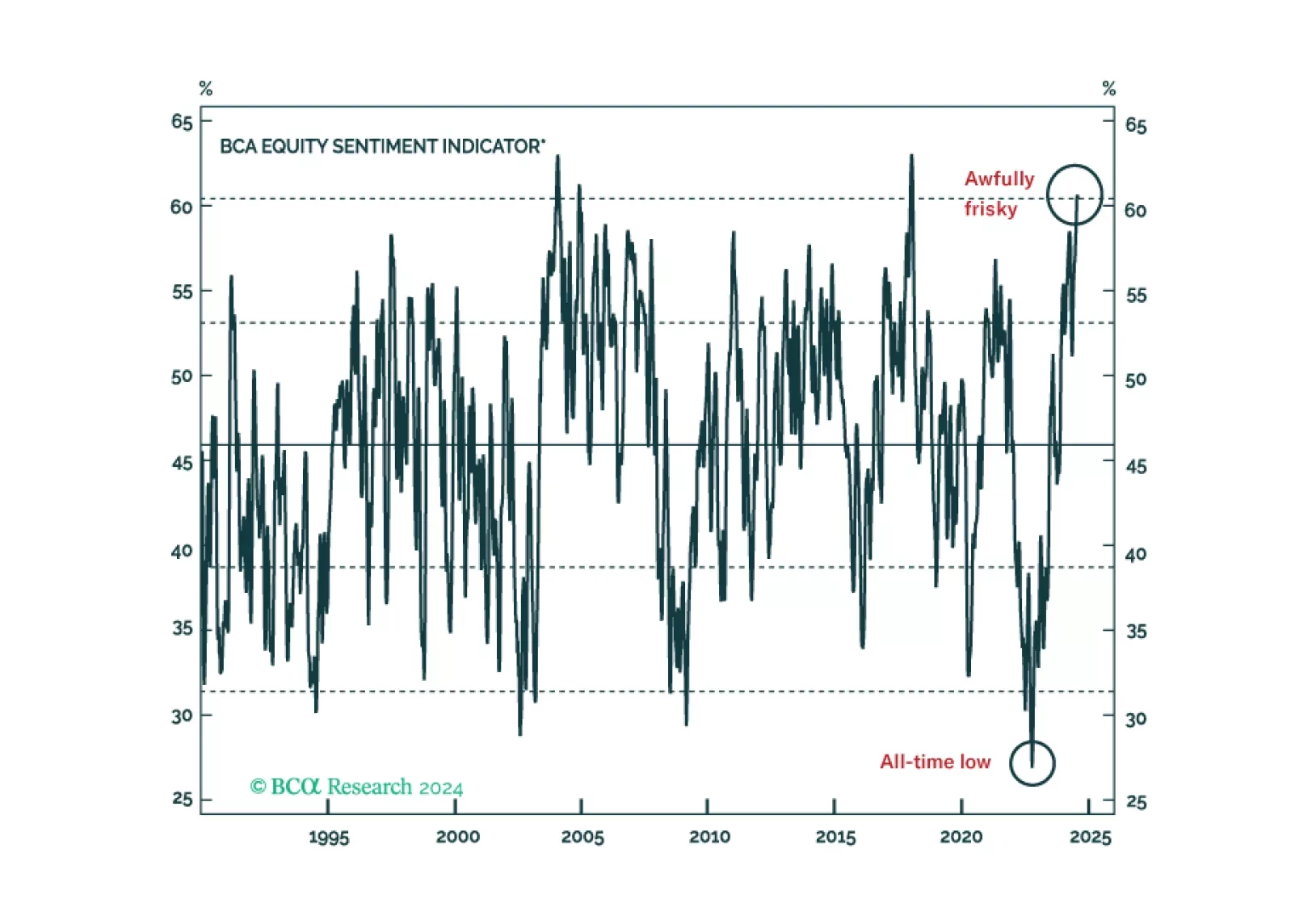

Mounting evidence that the labor market is on its way to cracking checked two more boxes on our checklist, driving us to tactically downgrade equities to underweight while upgrading fixed income to overweight. Our tactical and cyclical (6-12 months) views are now aligned as our conviction that a recession will begin before year-end has increased.

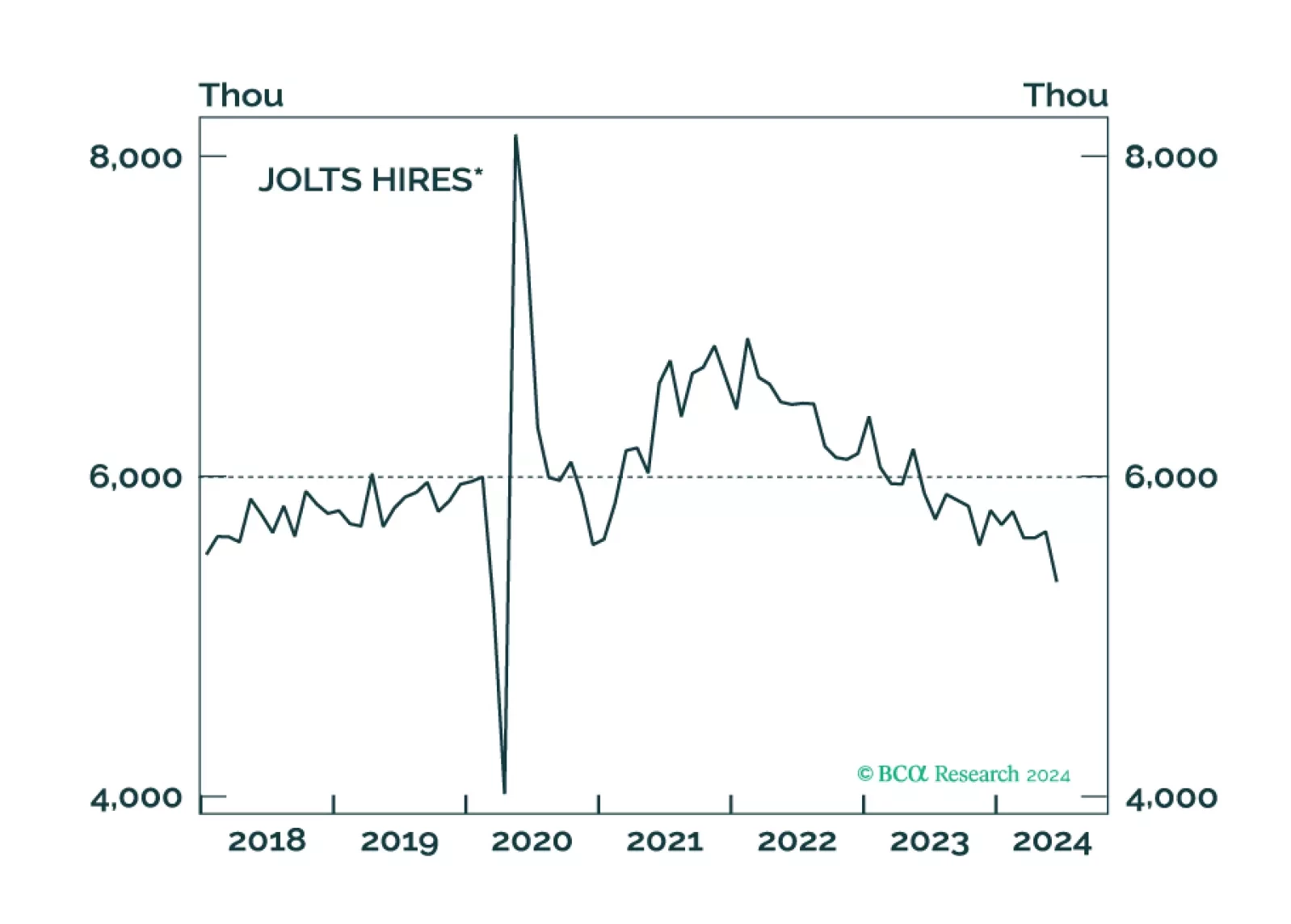

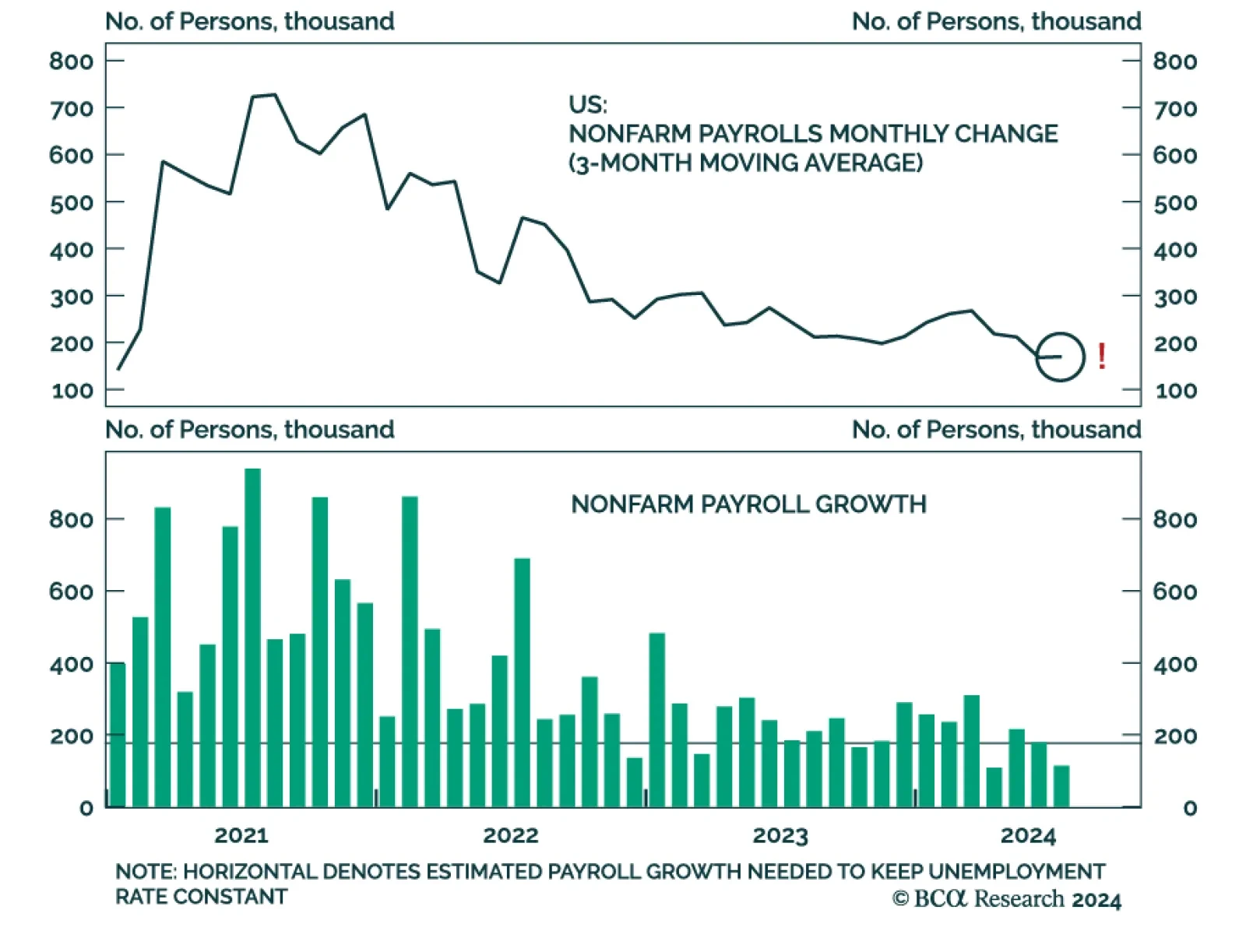

July nonfarm payrolls expanded by 114 thousand workers, a sharp slowdown from June’s downwardly revised 179 thousand, and significantly disappointing expectations of 175 thousand. The unemployment rate unexpectedly edged 0.2ppt higher to 4.3% in July,…