United States

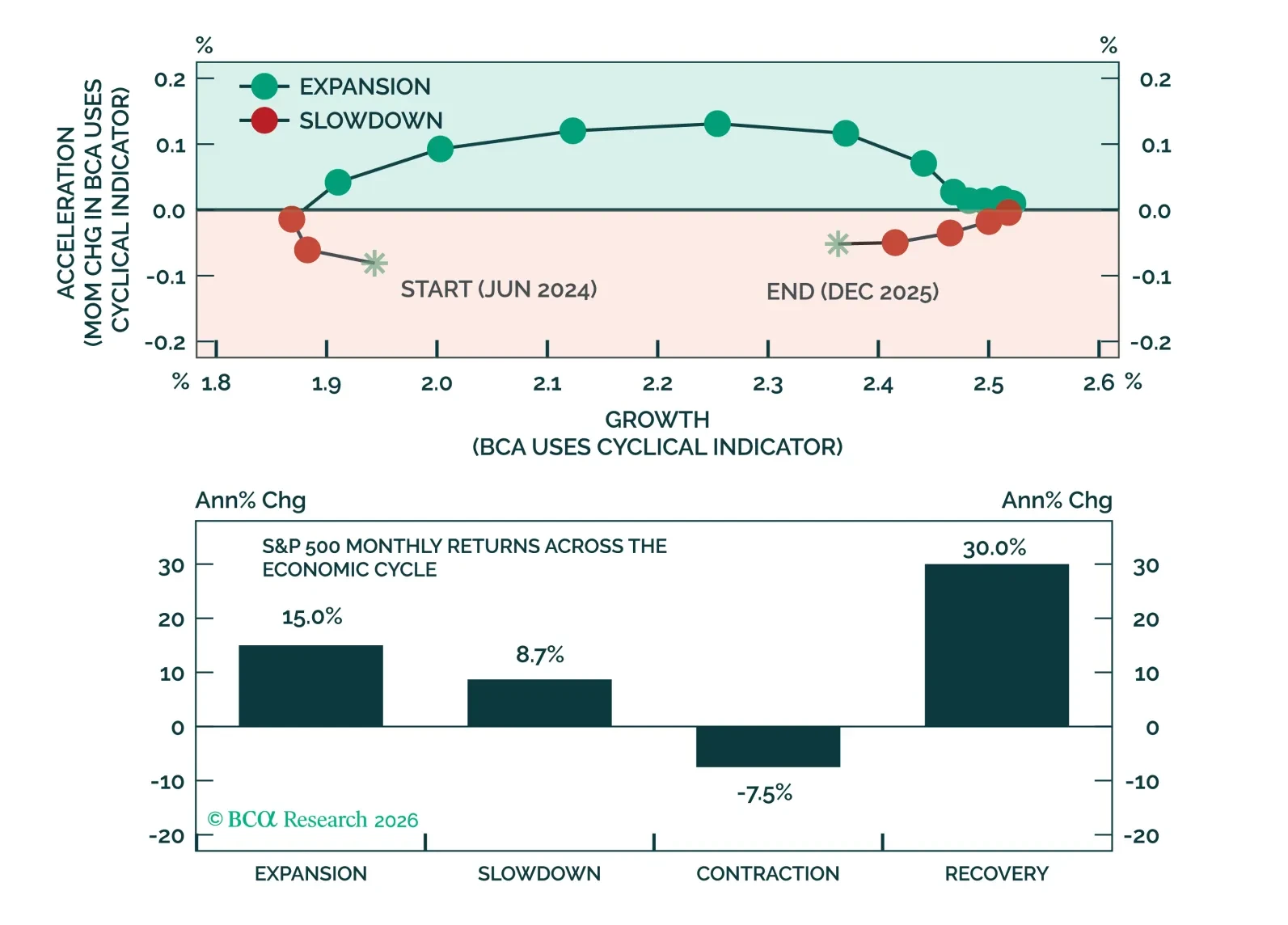

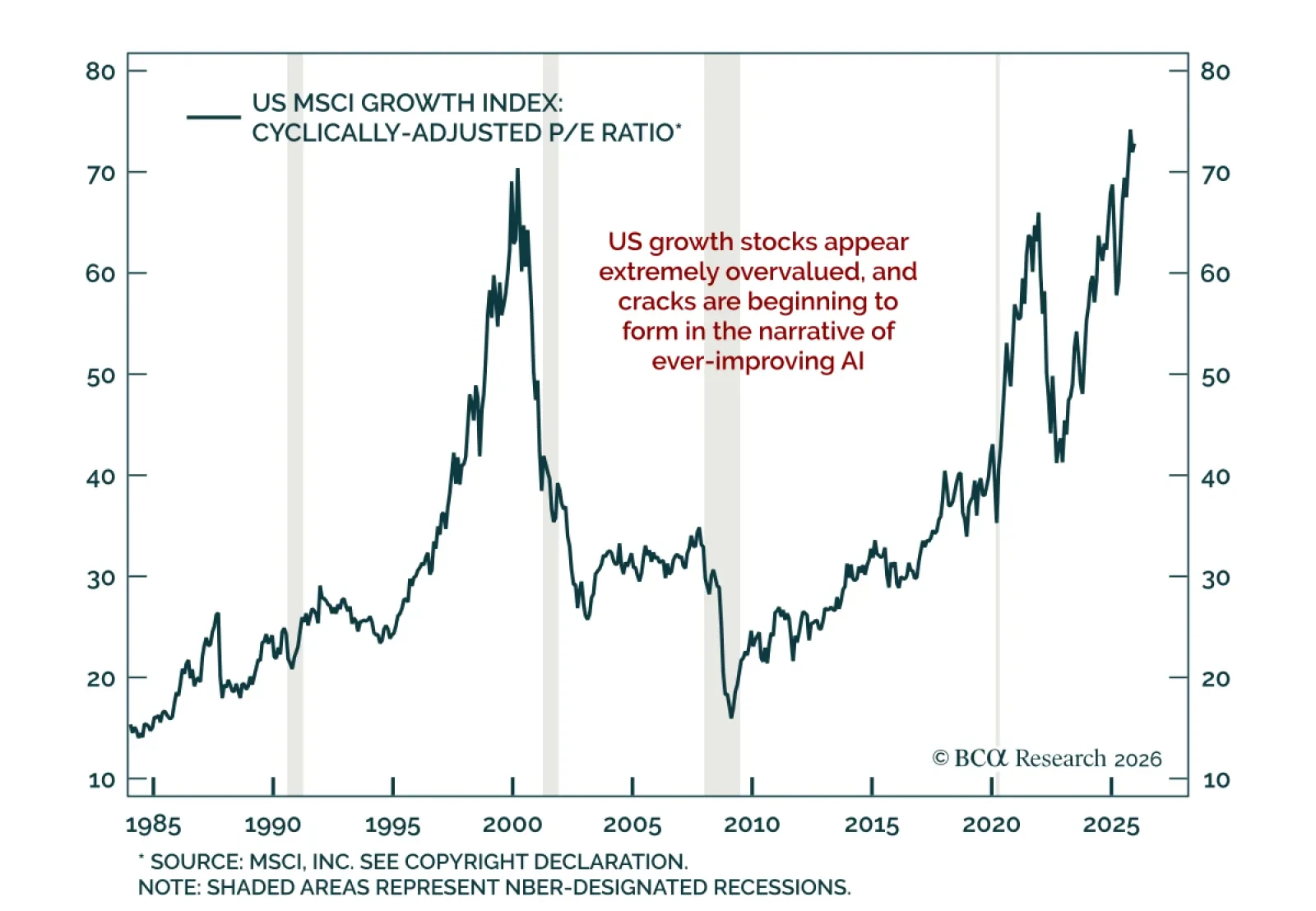

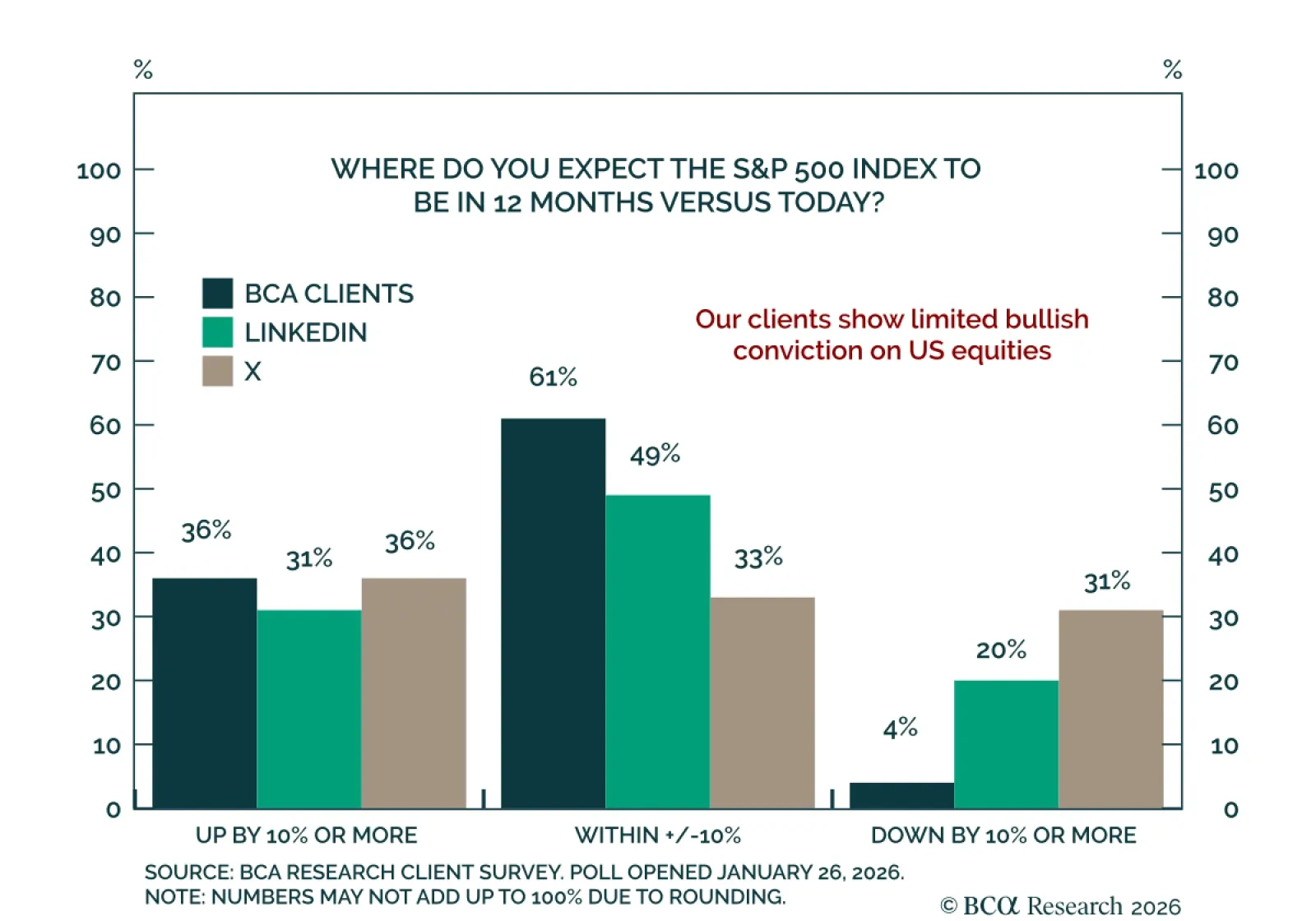

2026 should see another year of gains for the S&P 500, but, as the bull market matures and growth slows, returns will be capped by revenue growth rather than being boosted by expanding margins and multiples. We think Tech can outperform, but leadership will broaden and performance gaps will narrow.

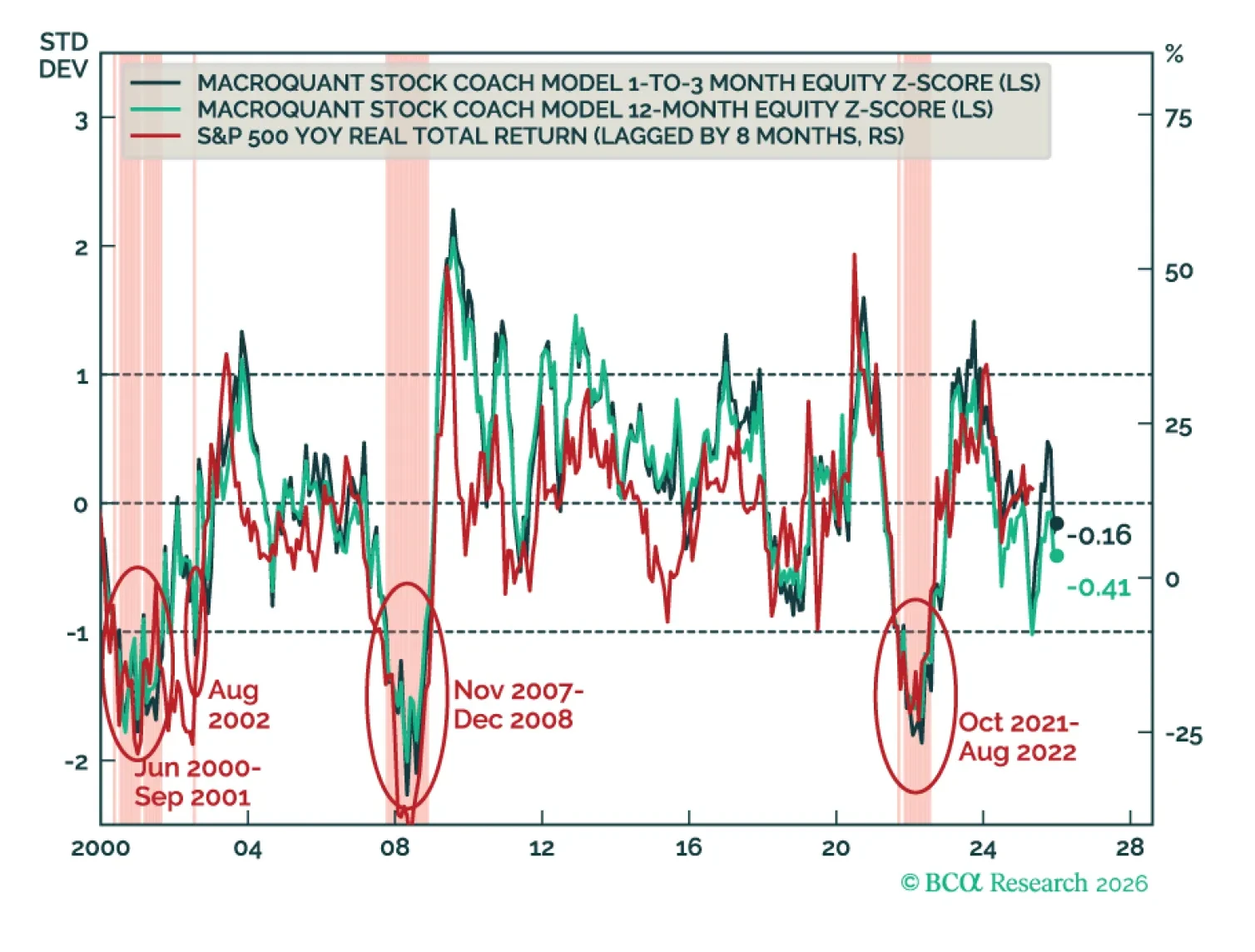

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

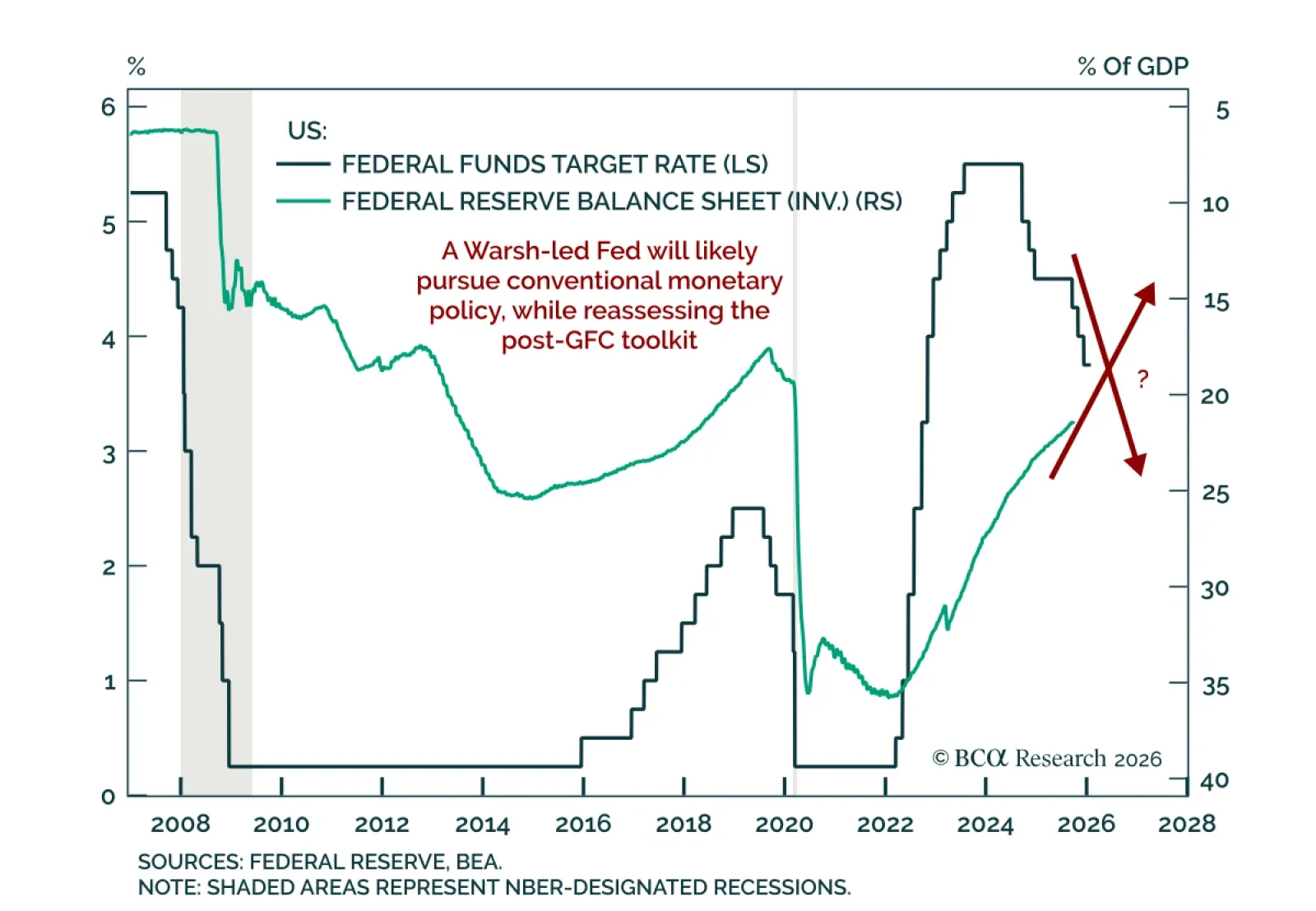

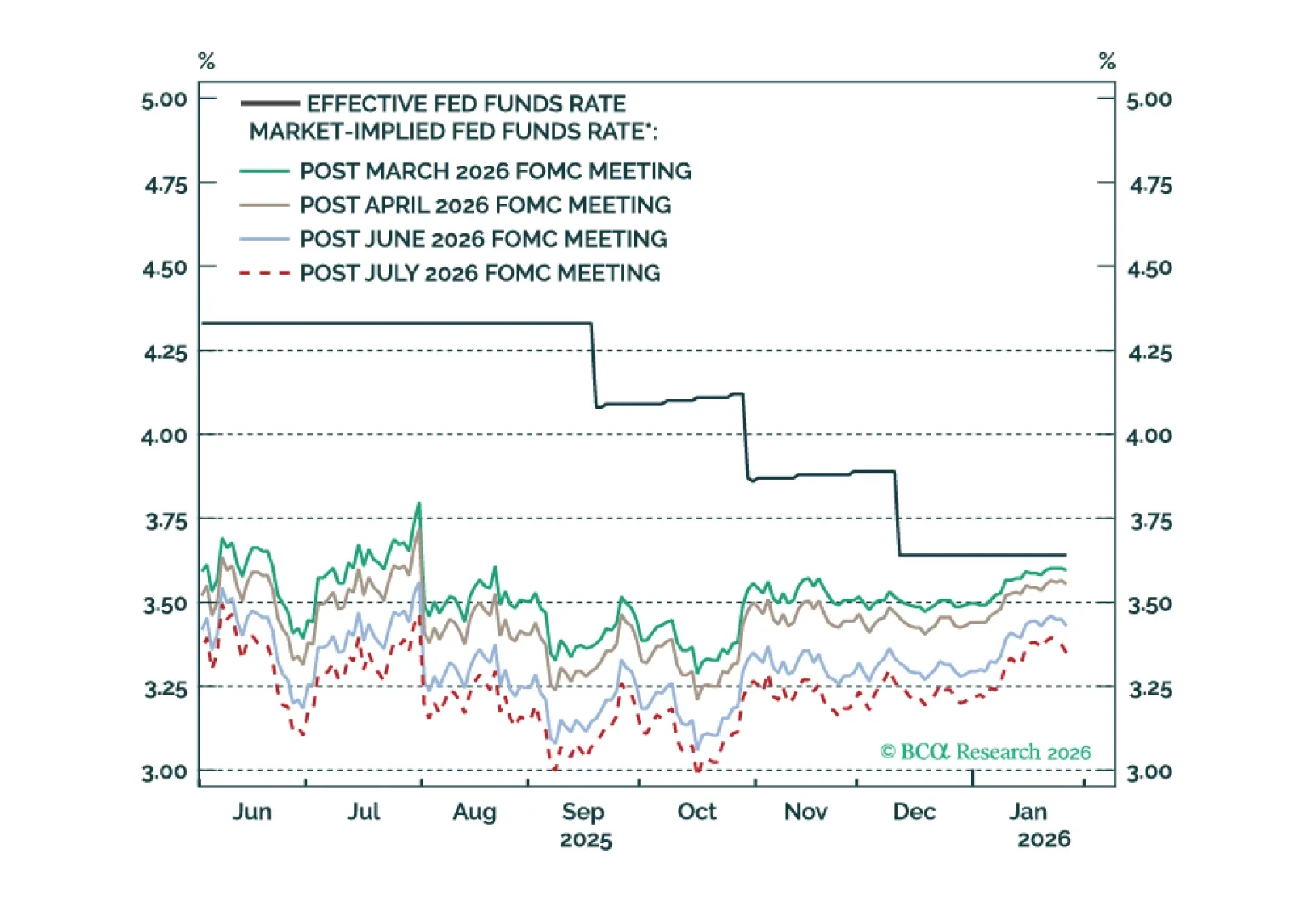

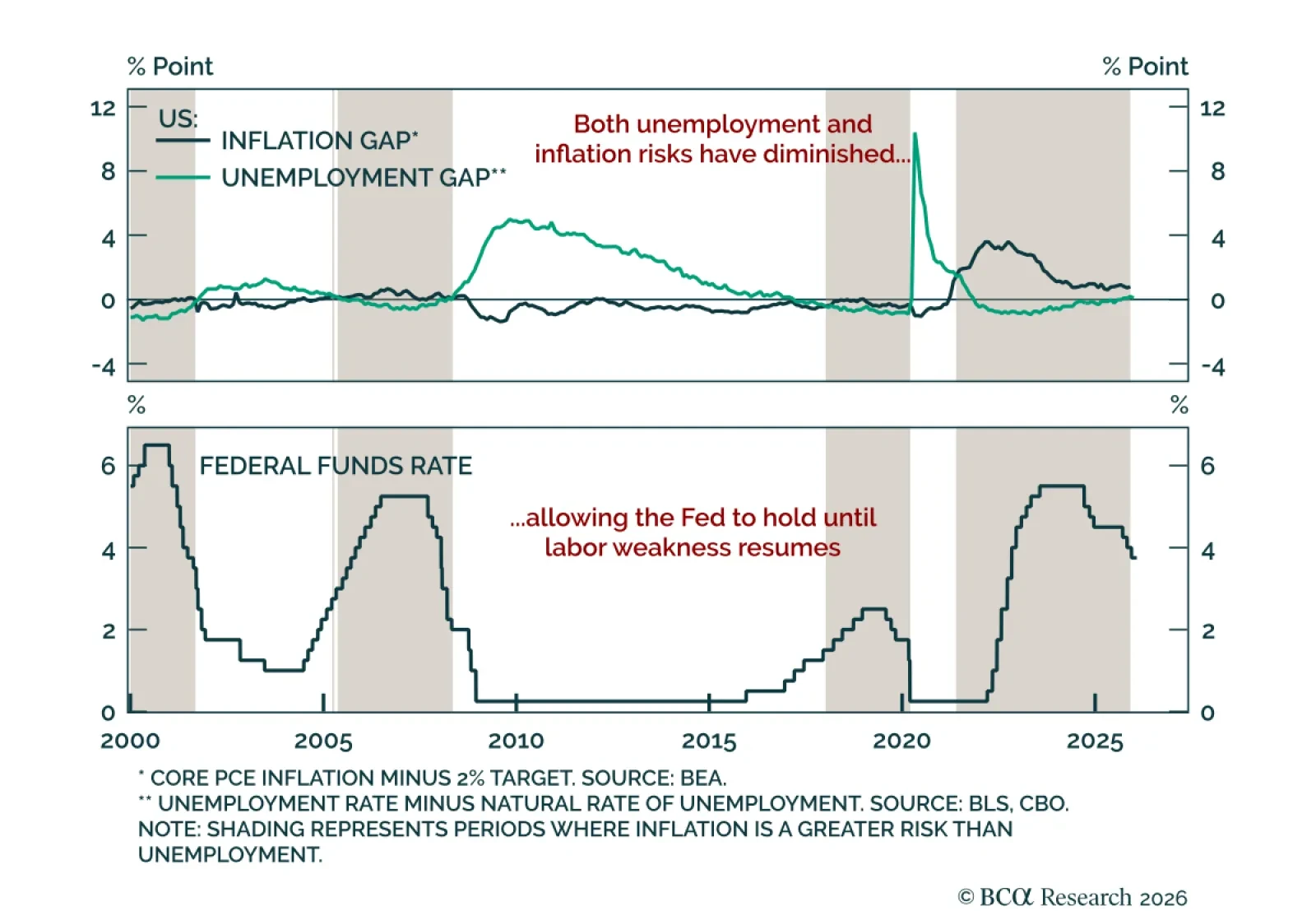

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

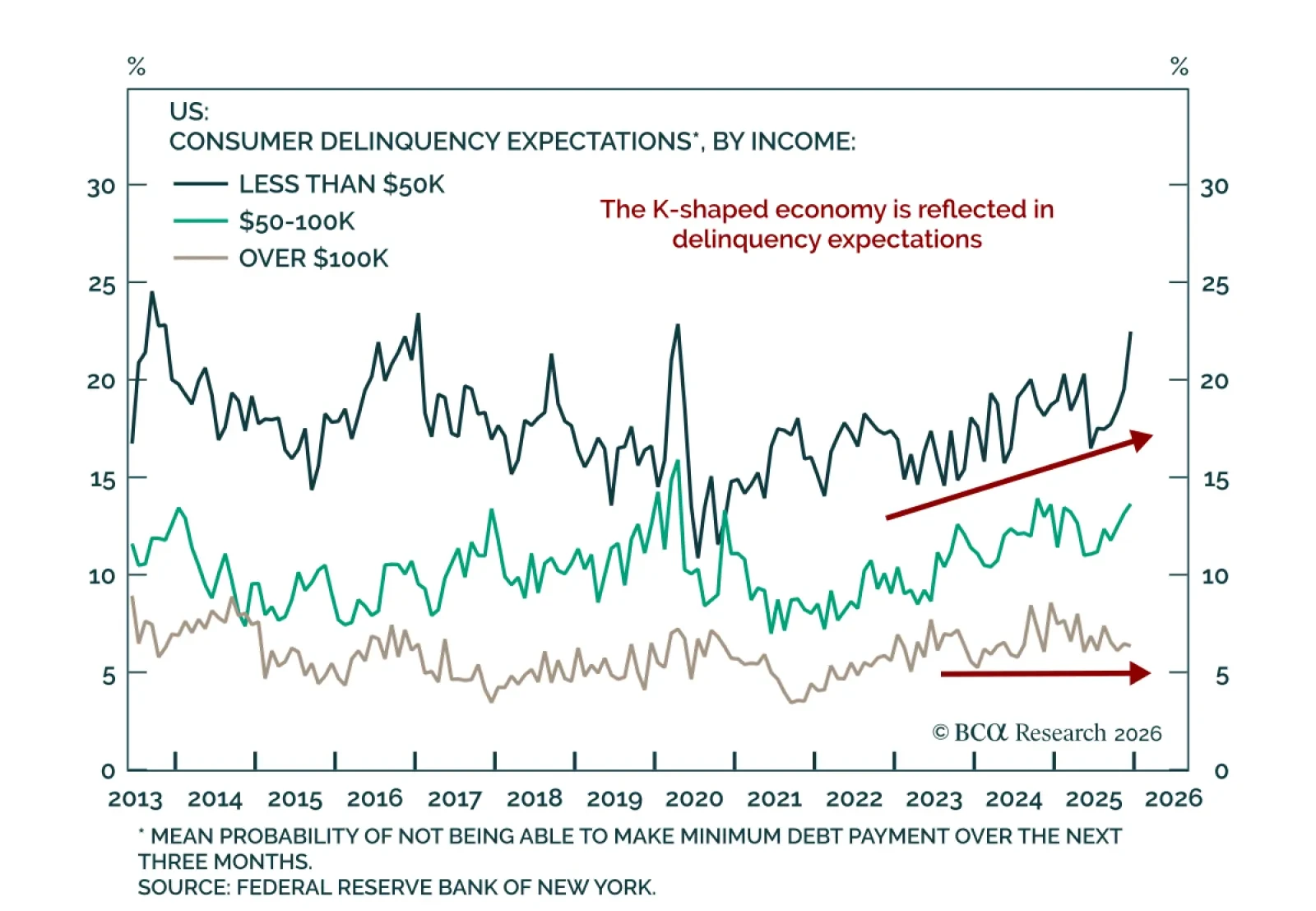

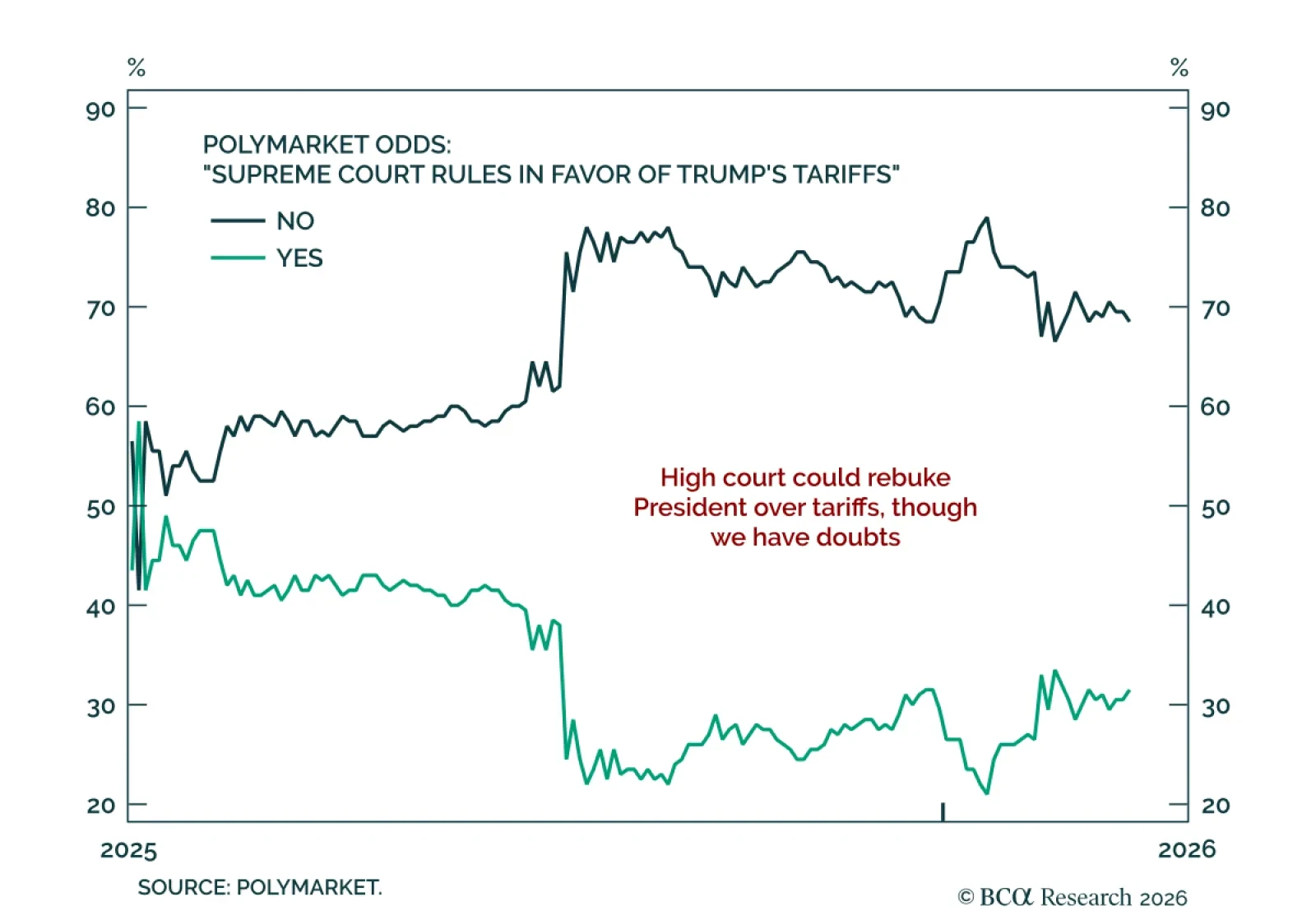

Checks and balances in the US political system are underrated. Social unrest and government shutdown will have fleeting market implications.