United States

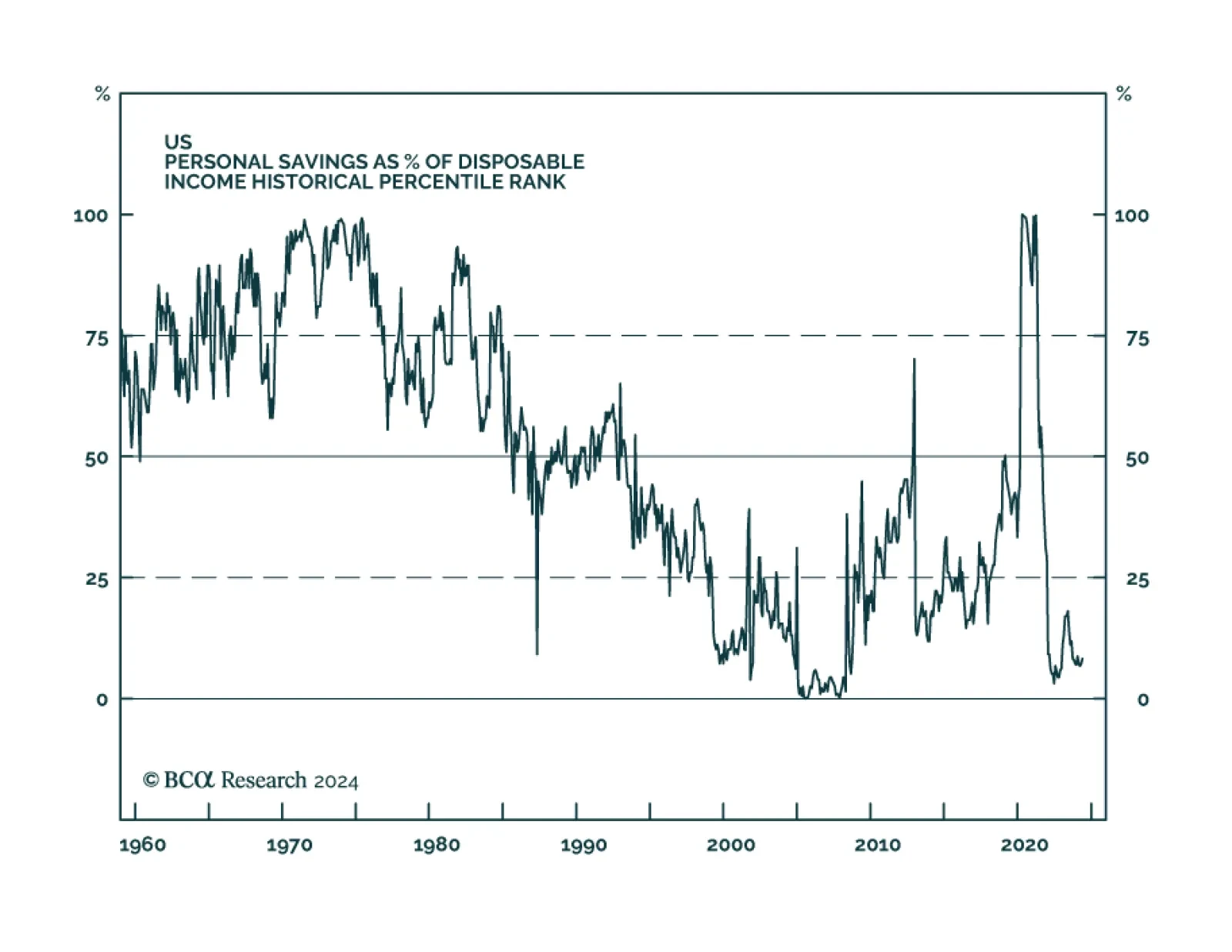

Our US Investment Strategy colleagues have kept a close eye on excess savings and their disposition since the CARES Act funds began to flow in the spring of 2020. Their conviction that the consensus failed to recognize the consumption potential inherent in…

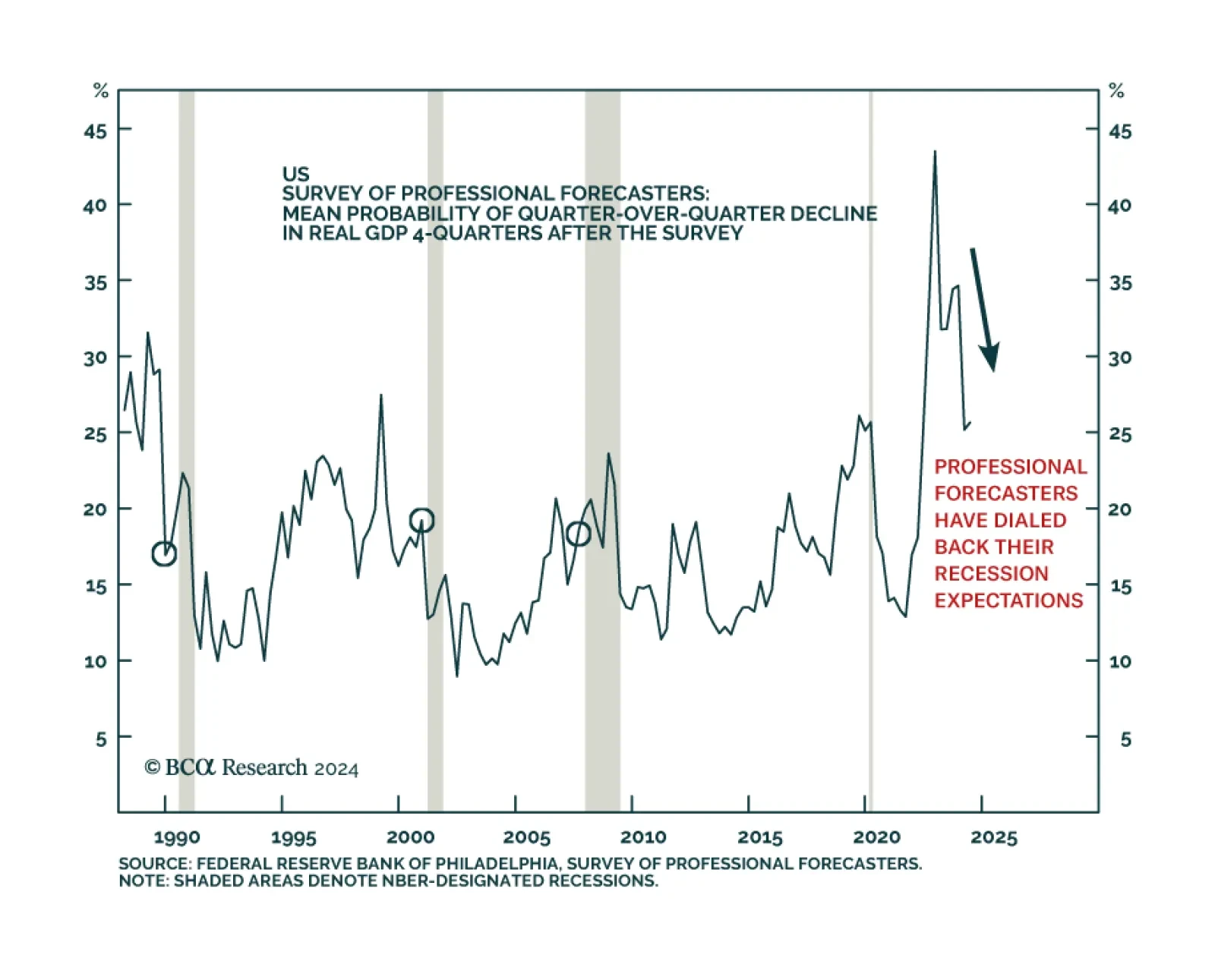

Participants in the Philly Fed’s Survey of Professional Forecasters (SPF) assign a 26% probability to a contraction in US real GDP four quarters from now, down from their 44% peak probability in 2022. The unwieldy contraction-in-four-quarters wording makes…

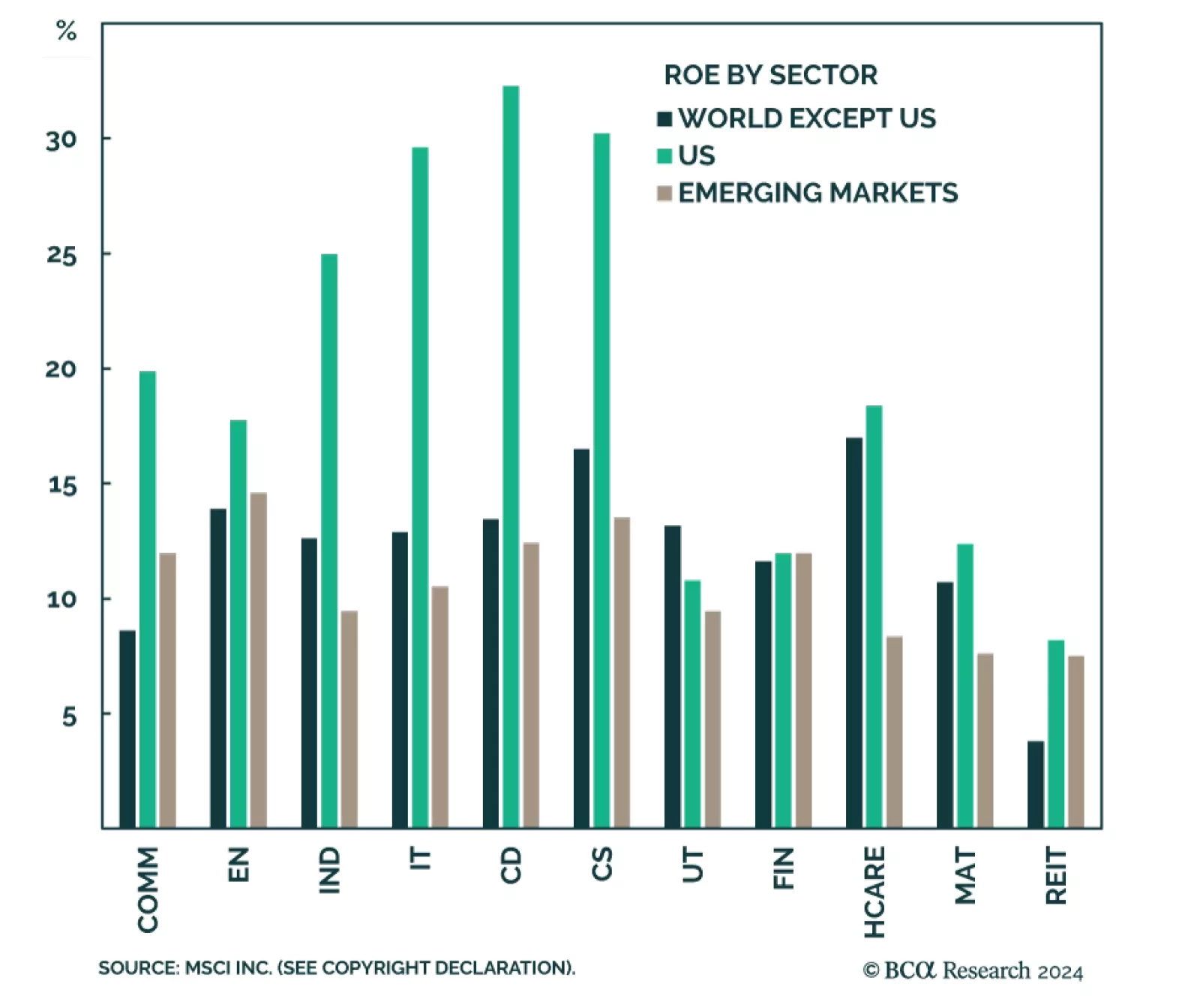

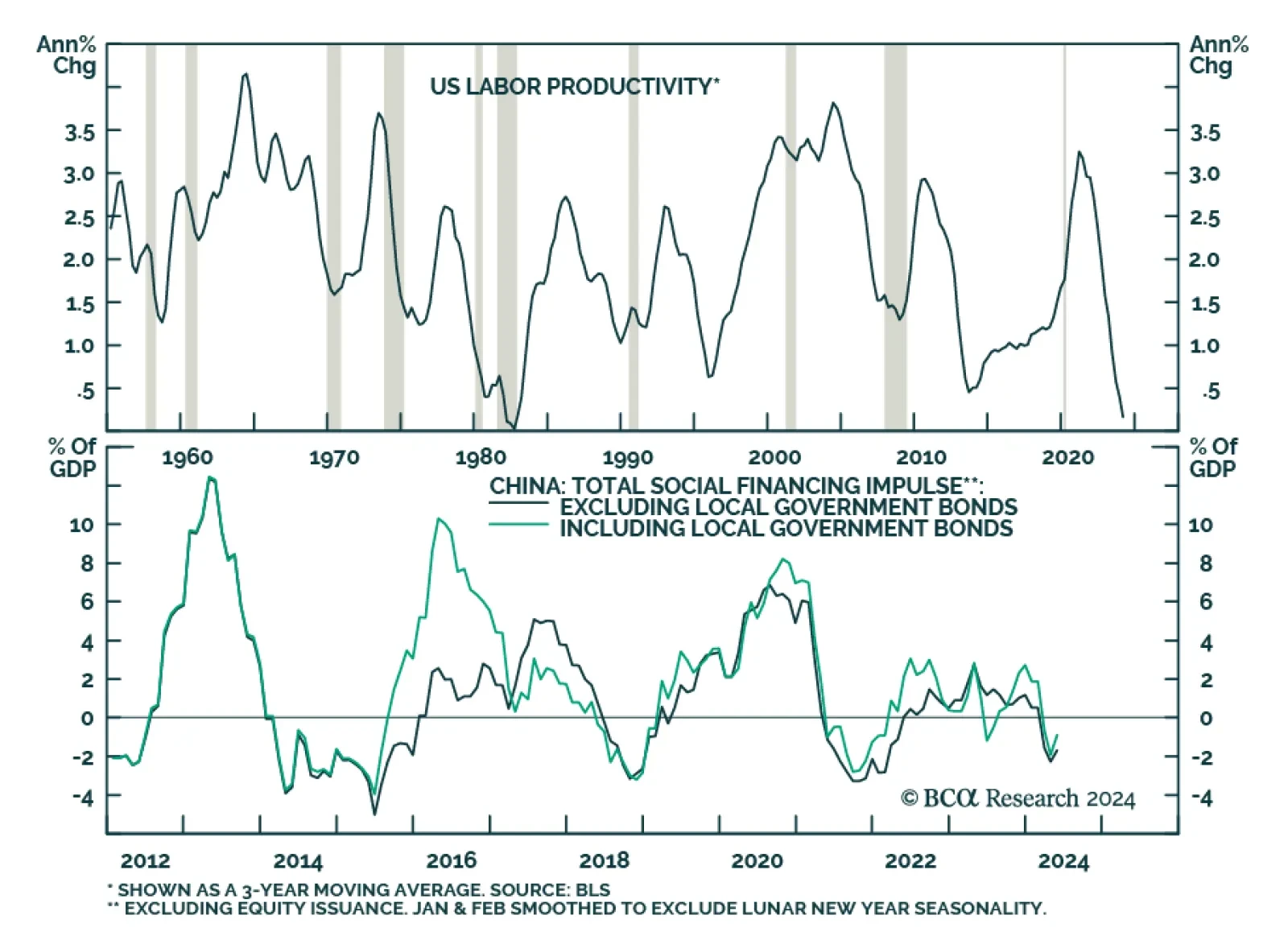

According to BCA Research’s US Equity Strategy service, post-GFC US equity outperformance can be attributed to a perfect storm of advantageous policies and a human capital edge. The topic of American exceptionalism is hotly debated in the wake of the…

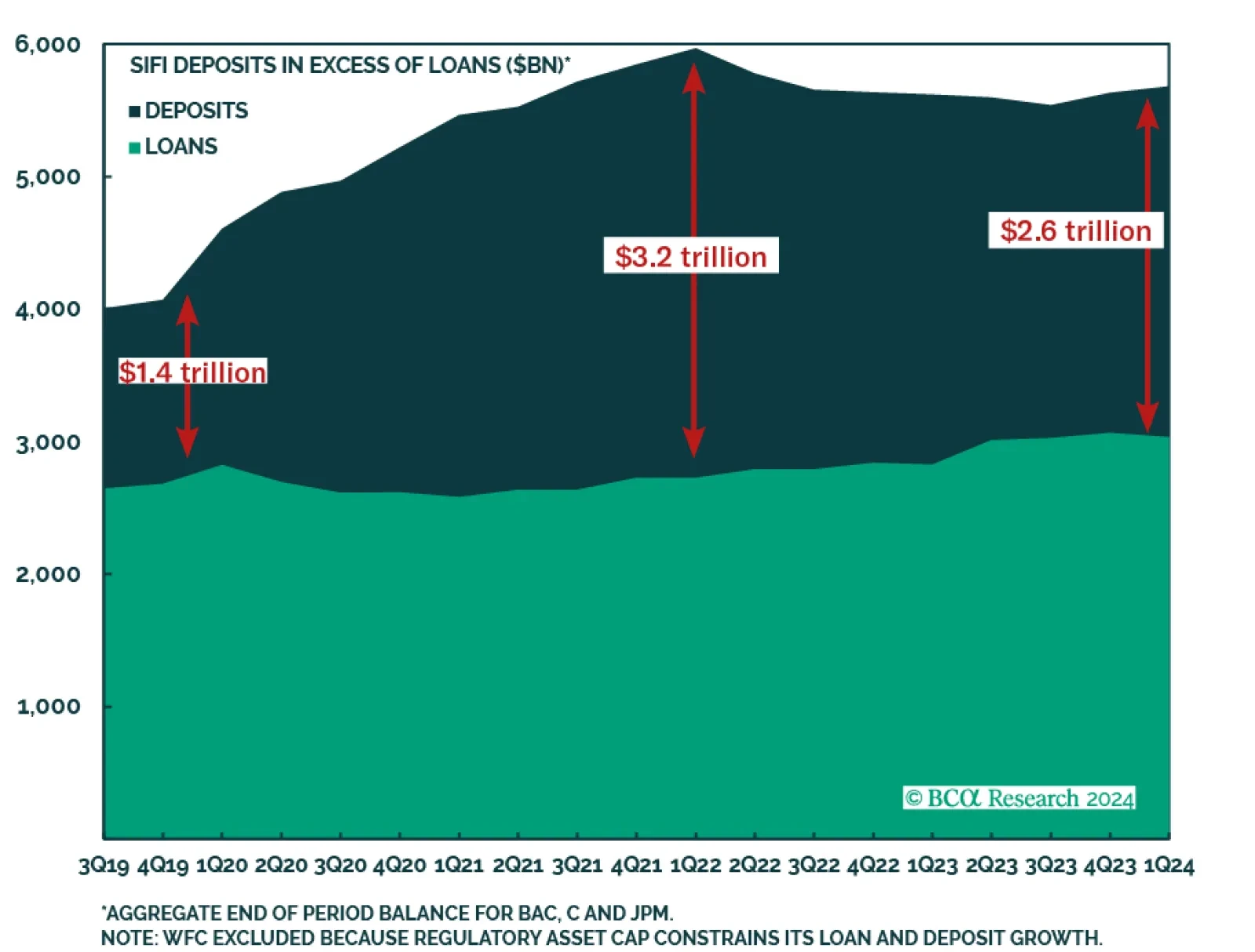

Second-quarter earnings season unofficially kicks off before the open on Friday, when Citigroup (C), JPMorgan (JPM) and Wells Fargo (WFC) report their results for the June 30 quarter. Bank of America (BAC), the other commercial banking behemoth, will round…

We expect continued softening in the US economy will lead to decelerating wage growth, muffling the principal consumption driver. Because the US has been the foremost catalyst for global growth in this cycle, a US recession will eventually morph into a global…

Although we ticked a second box on our checklist, the incoming data still do not indicate that a recession is imminent. We remain tactically equal weight equities with a strong bias to underweight them, but we’re not exiting the party just yet.

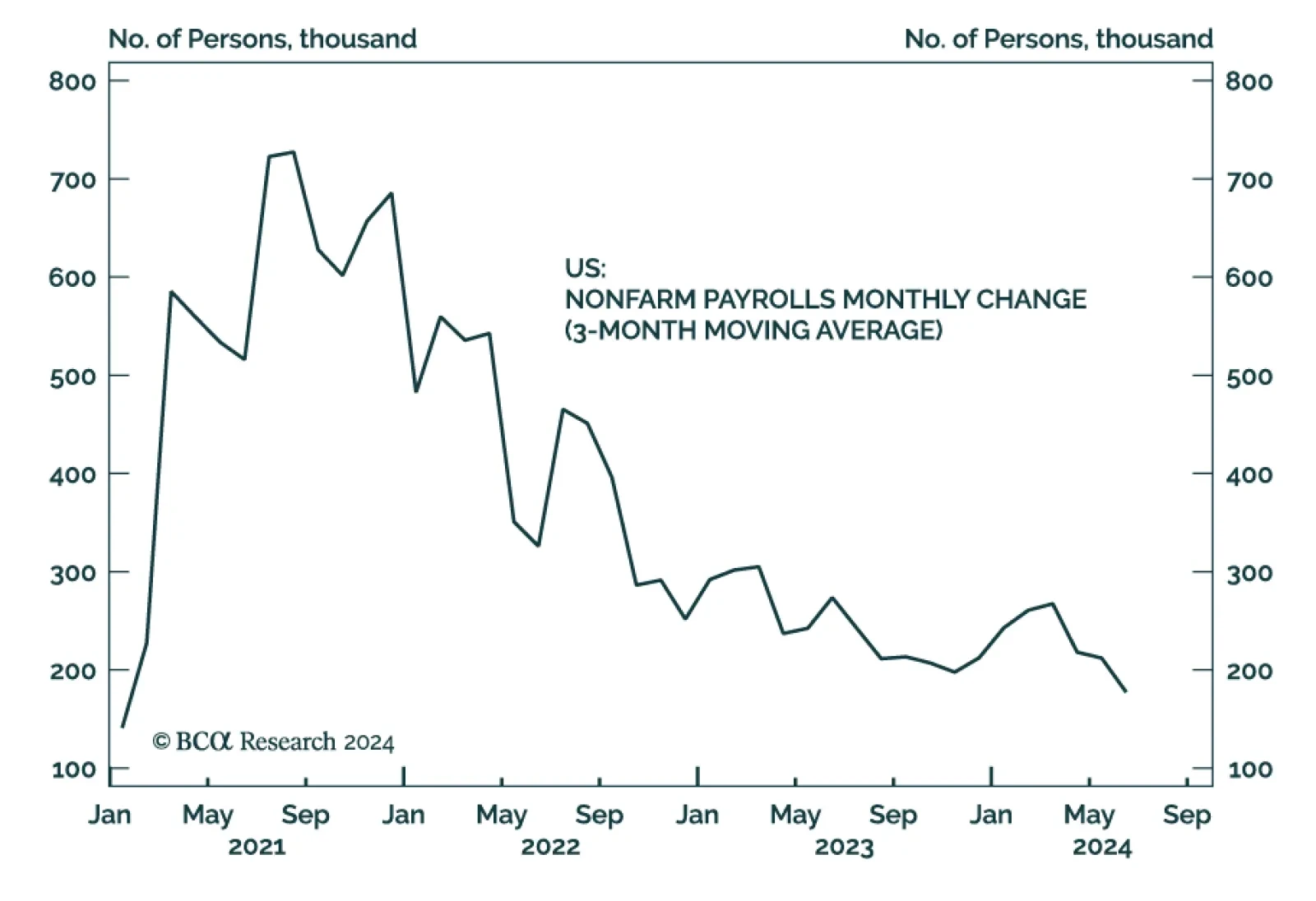

June nonfarm payrolls expanded by 206,000 workers, topping the 190,000 consensus expectation, but downward revisions of 111,000 jobs in April and May pulled the three-month moving average down to 177 thousand, its lowest level since January 2021. The…

Our labor market indicators have softened meaningfully during the past month but aren’t yet signaling an imminent recession. That said, the Fed can no longer ignore the labor market with the unemployment rate above 4% and rising.

Does the incipient slowdown in European data herald a soft landing and a goldilocks period for equities? We have our doubts.

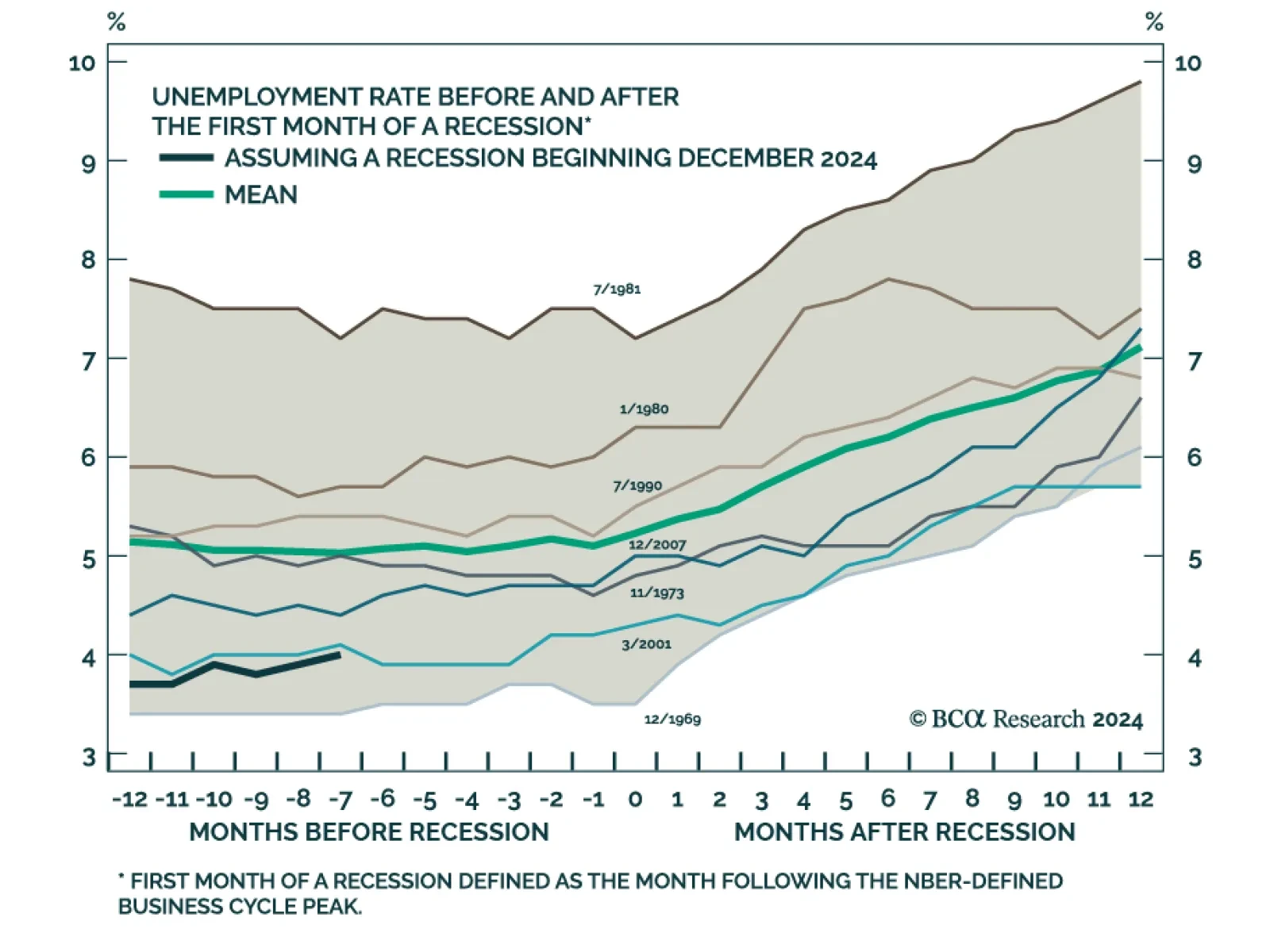

The US unemployment rate stands at just 4.0% today following 27 consecutive sub-4% readings. Does this low unemployment rate guarantee a soft landing in the US economy? Our Global Investment Strategy (GIS) team’s base case is that the US economy will fall…