United States

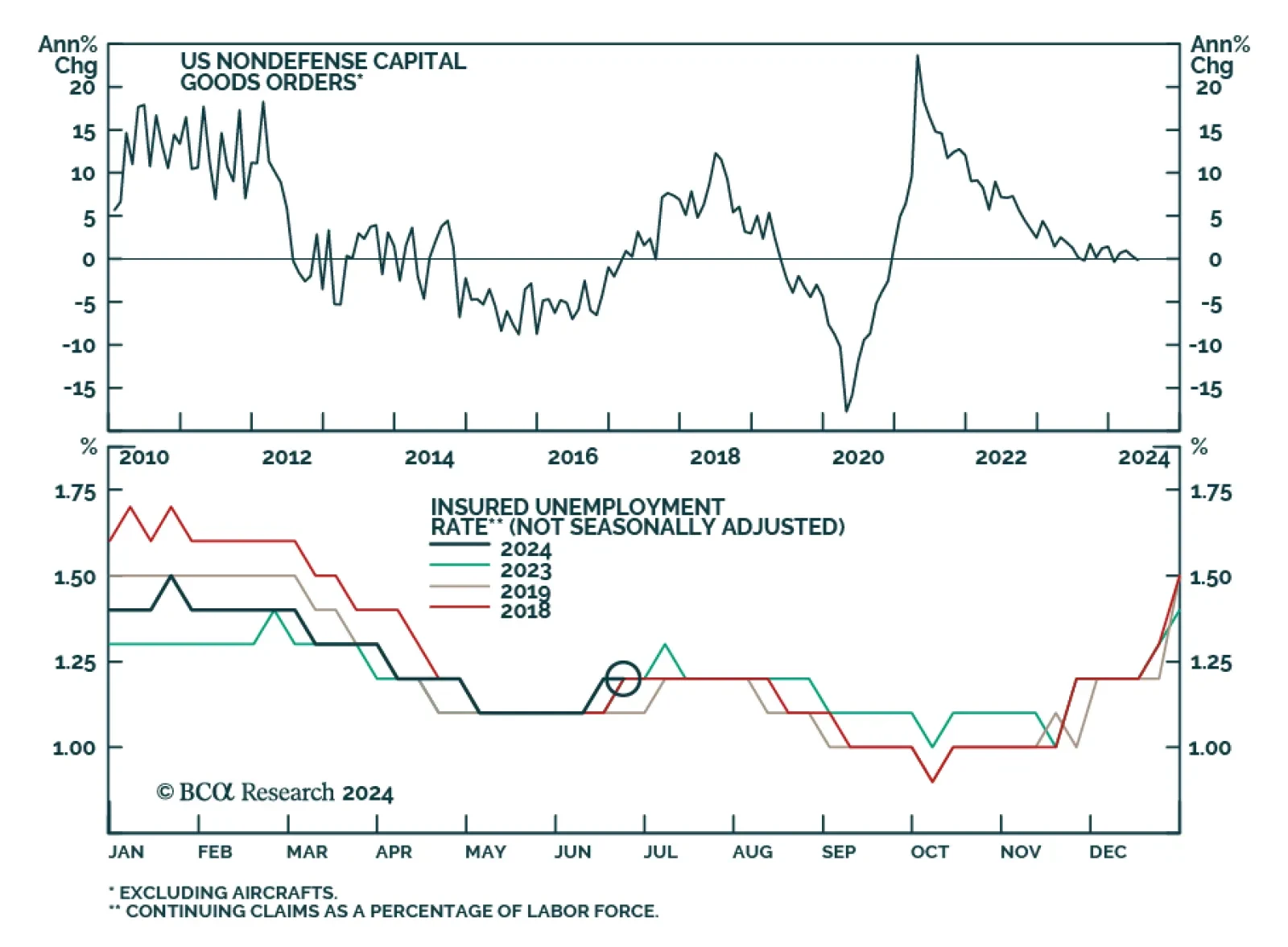

Several pieces of data were released for the US on Thursday. US durable goods orders growth slowed from 0.2% to 0.1% in May, beating expectations of a 0.5% contraction. However other components of the report disappointed consensus estimates. Durable goods…

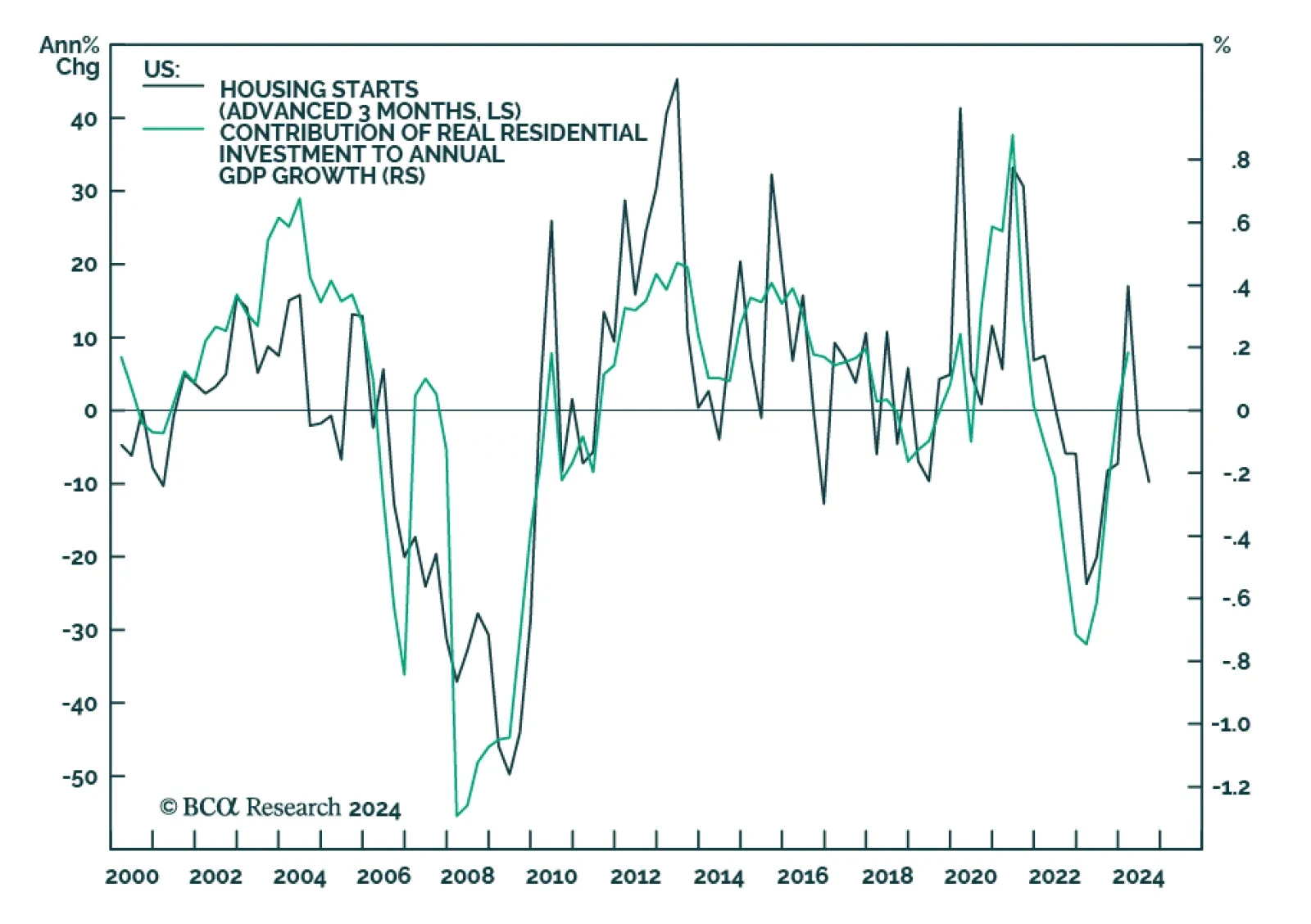

Right after the pandemic, many US homeowners locked in mortgages at extremely low rates. When interest rates rose, these homeowners refused to sell, as moving to a new home would result in an interest rate reset. In turn this resulted in a severe housing…

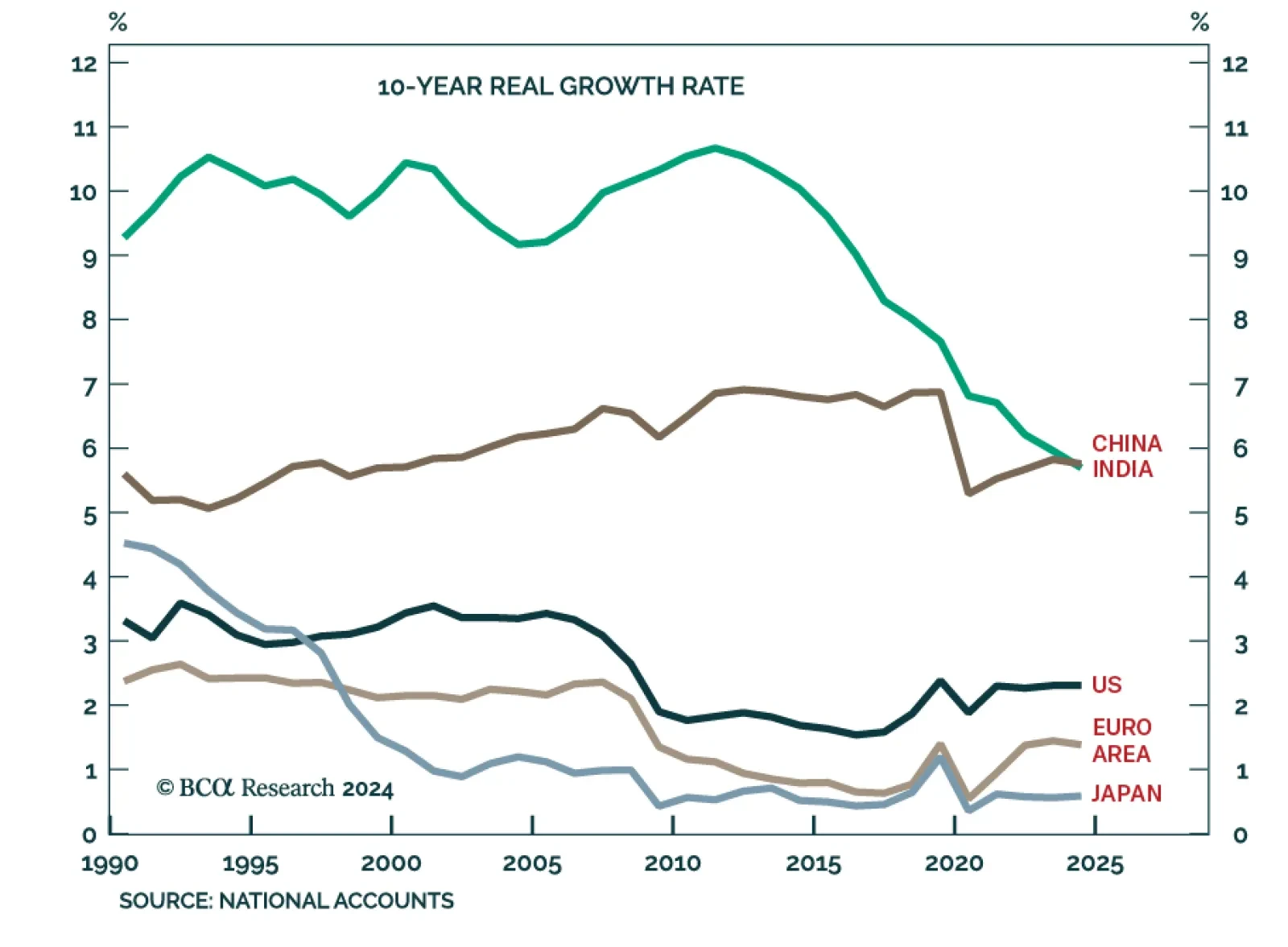

According to BCA Research’s Counterpoint service, absent China’s exponential credit growth, China’s trend growth rate will fall to 4 percent and the world’s trend growth rate will fall to sub-3 percent. This will impede structural rallies in the Chinese stock…

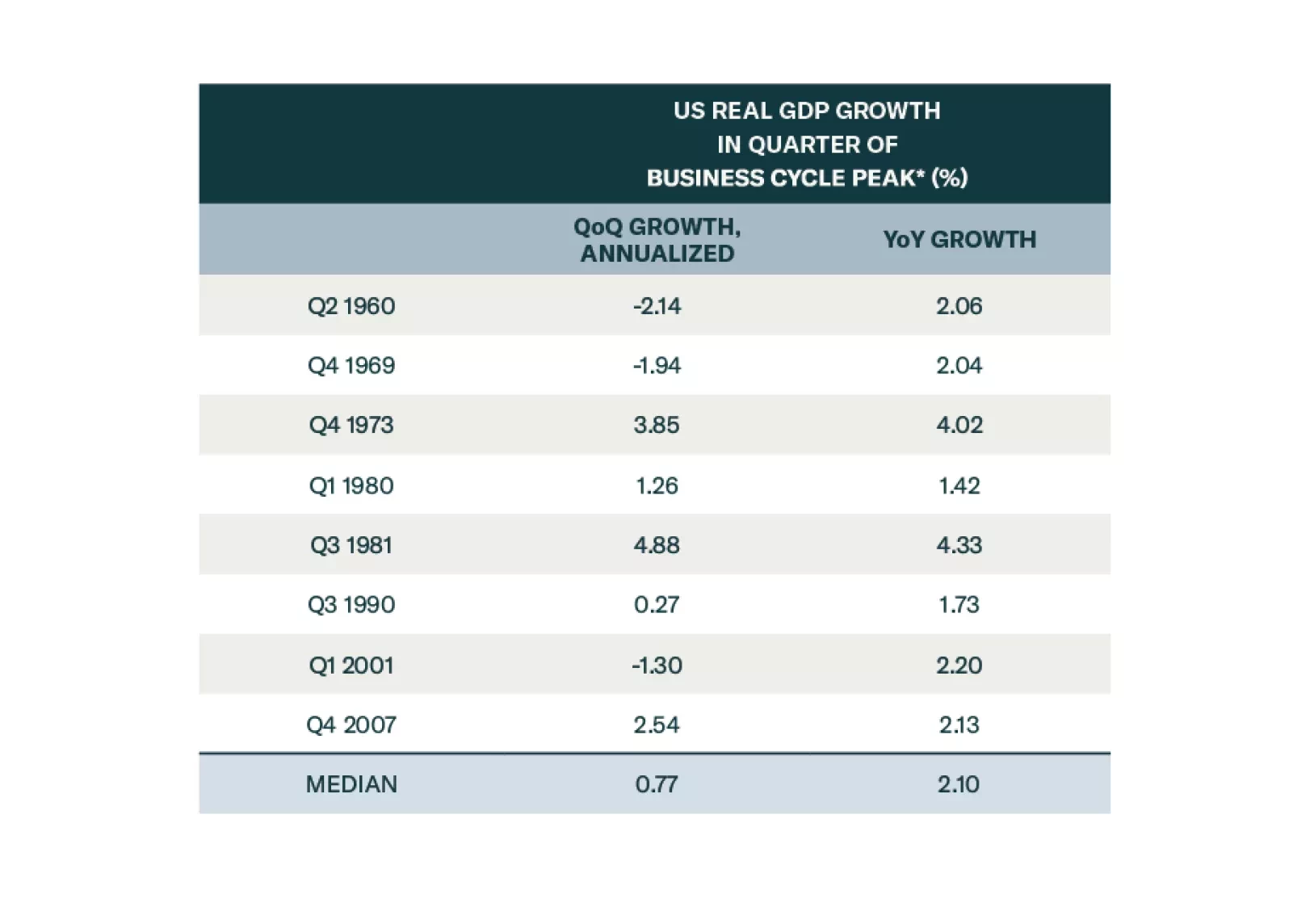

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

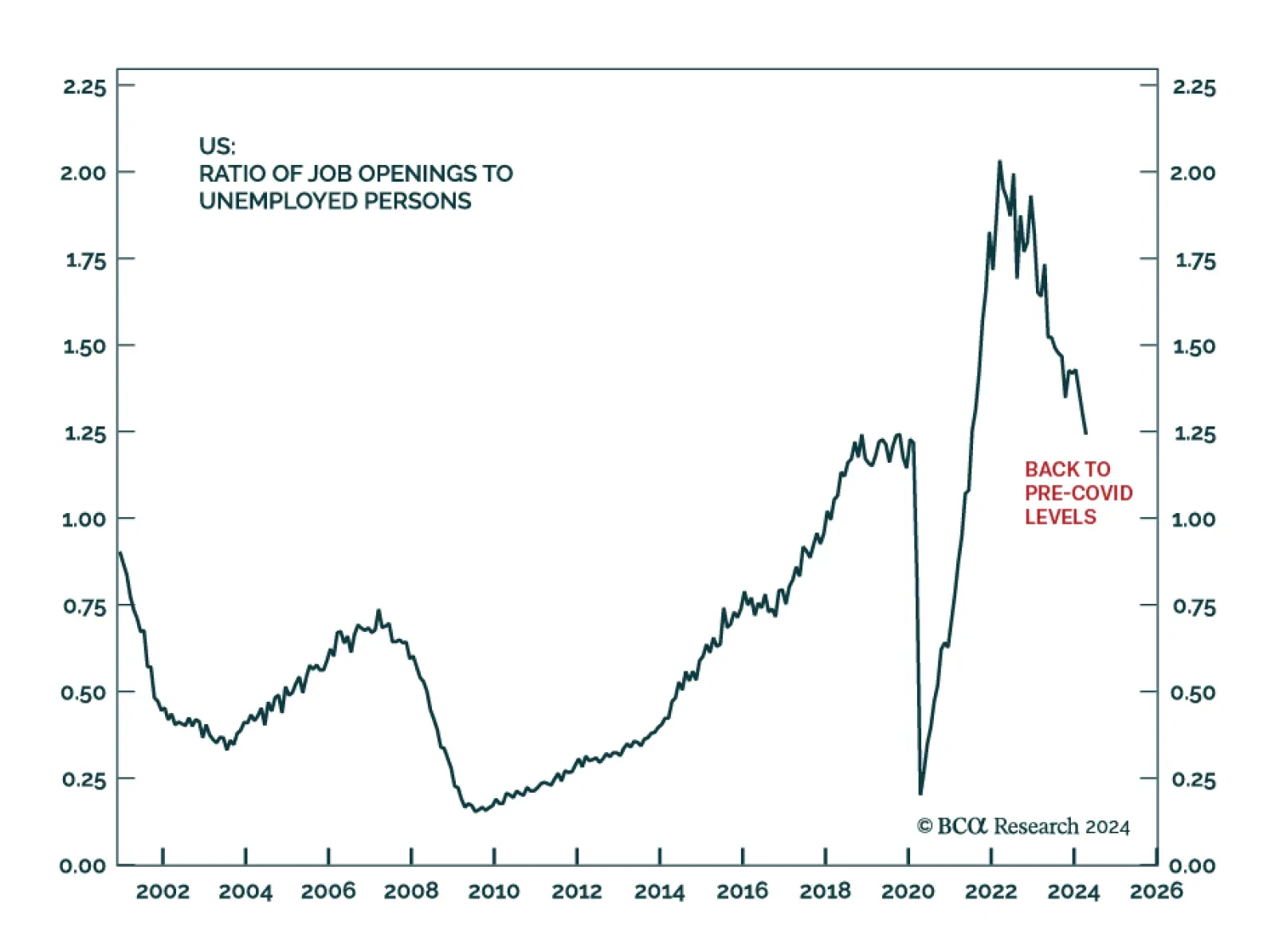

Our Global Investment Strategy team often highlights the job openings-to-unemployed ratio as a gauge of the labor market’s slack. This indicator climbed to over 2 job openings per unemployed person in 2022, as labor shortages plagued the US economy due to…

BCA Research’s US Investment Strategy service remains tactically neutral with a defensive cyclical bias. The team is resisting the impulse to turn prematurely defensive ahead of the coming recession. Our colleagues believe that fleeing for the hills at…

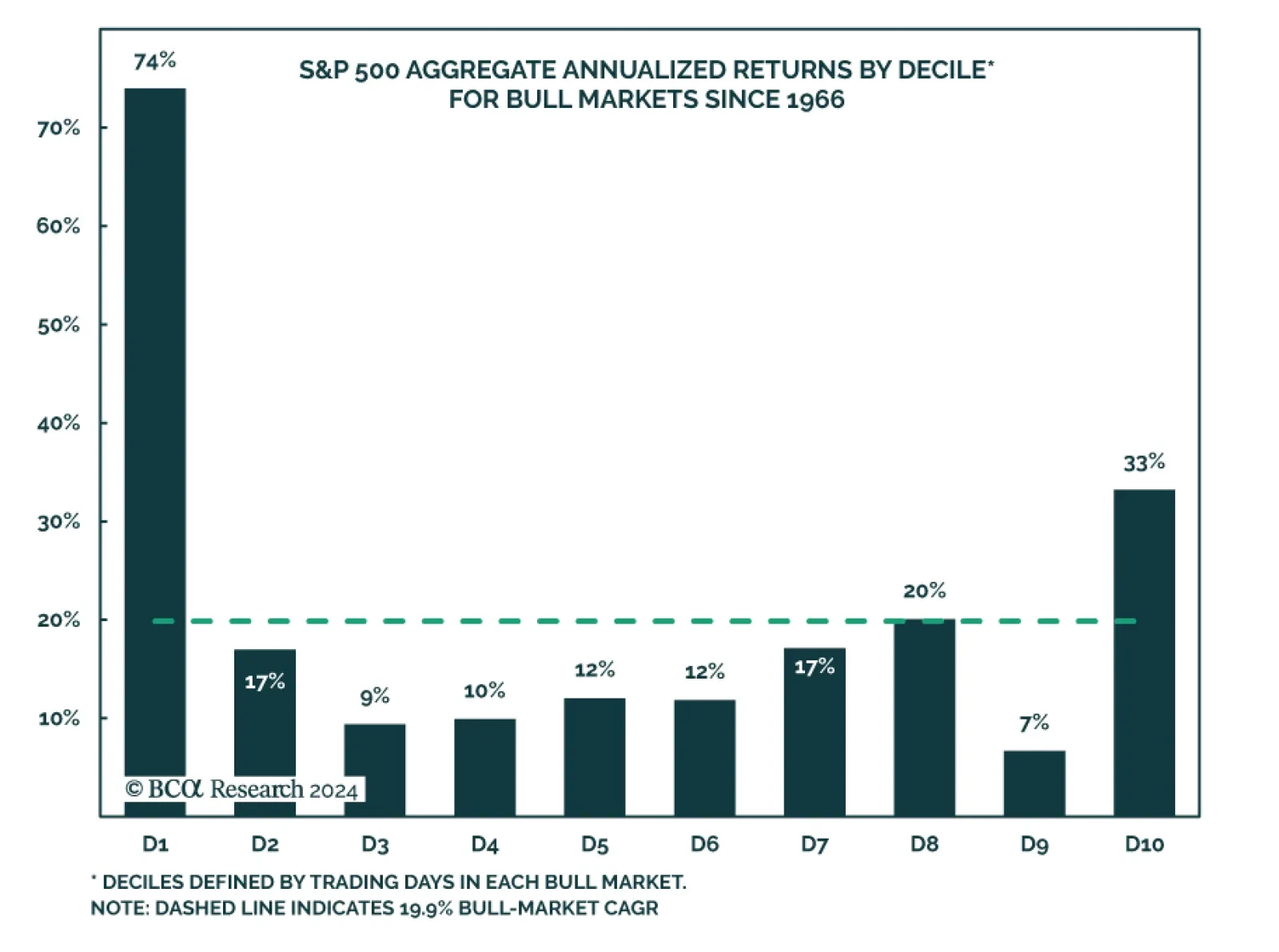

Today’s report recaps last week’s webcast and elaborates on its themes, delving into the empirical evidence underpinning our conviction that asset allocators should underweight equities sparingly and fleetingly. We remain tactically neutral and cyclically bearish.

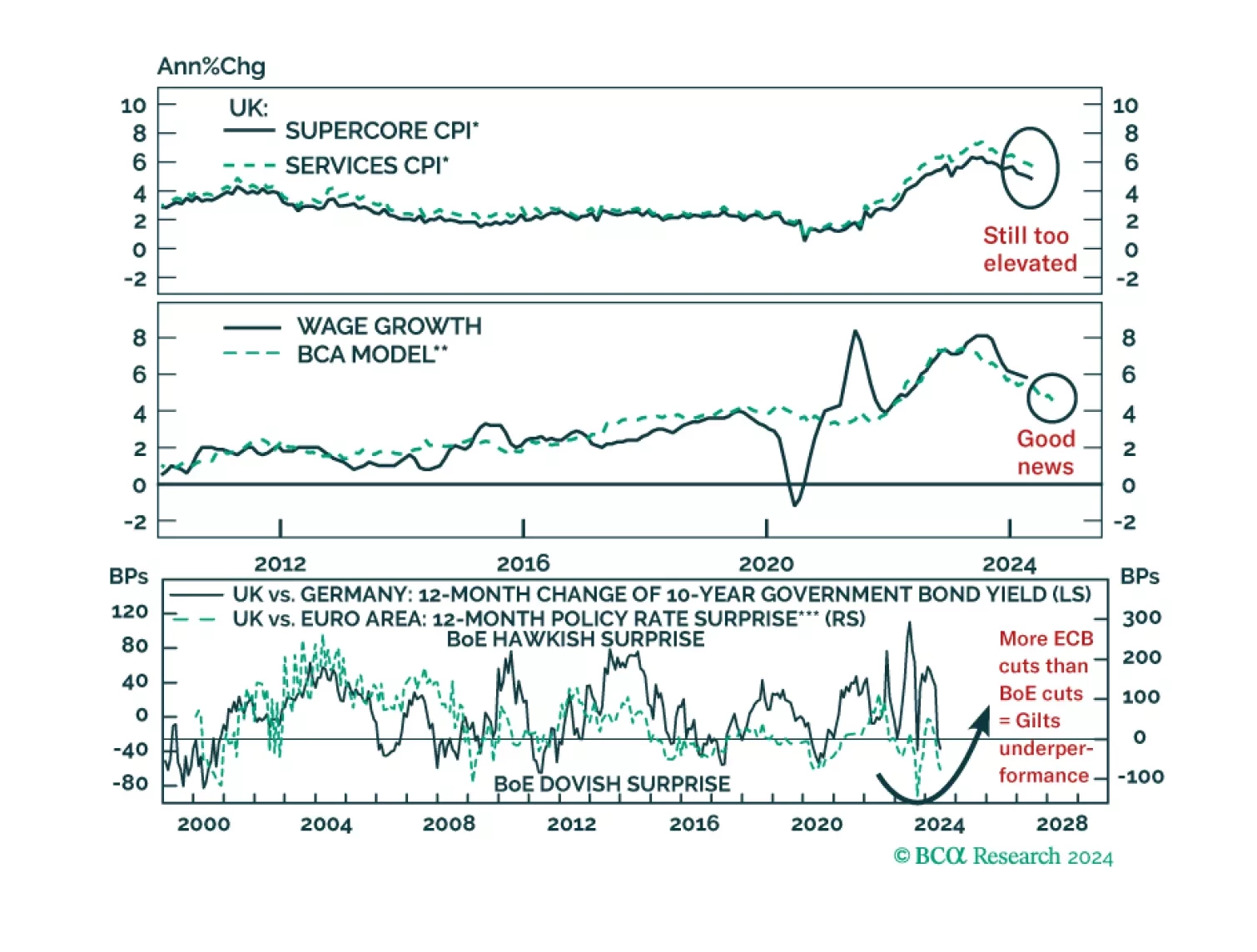

Is the BoE making a mistake moving toward rate cuts before the end of the summer? What would such a move mean for UK asset prices?

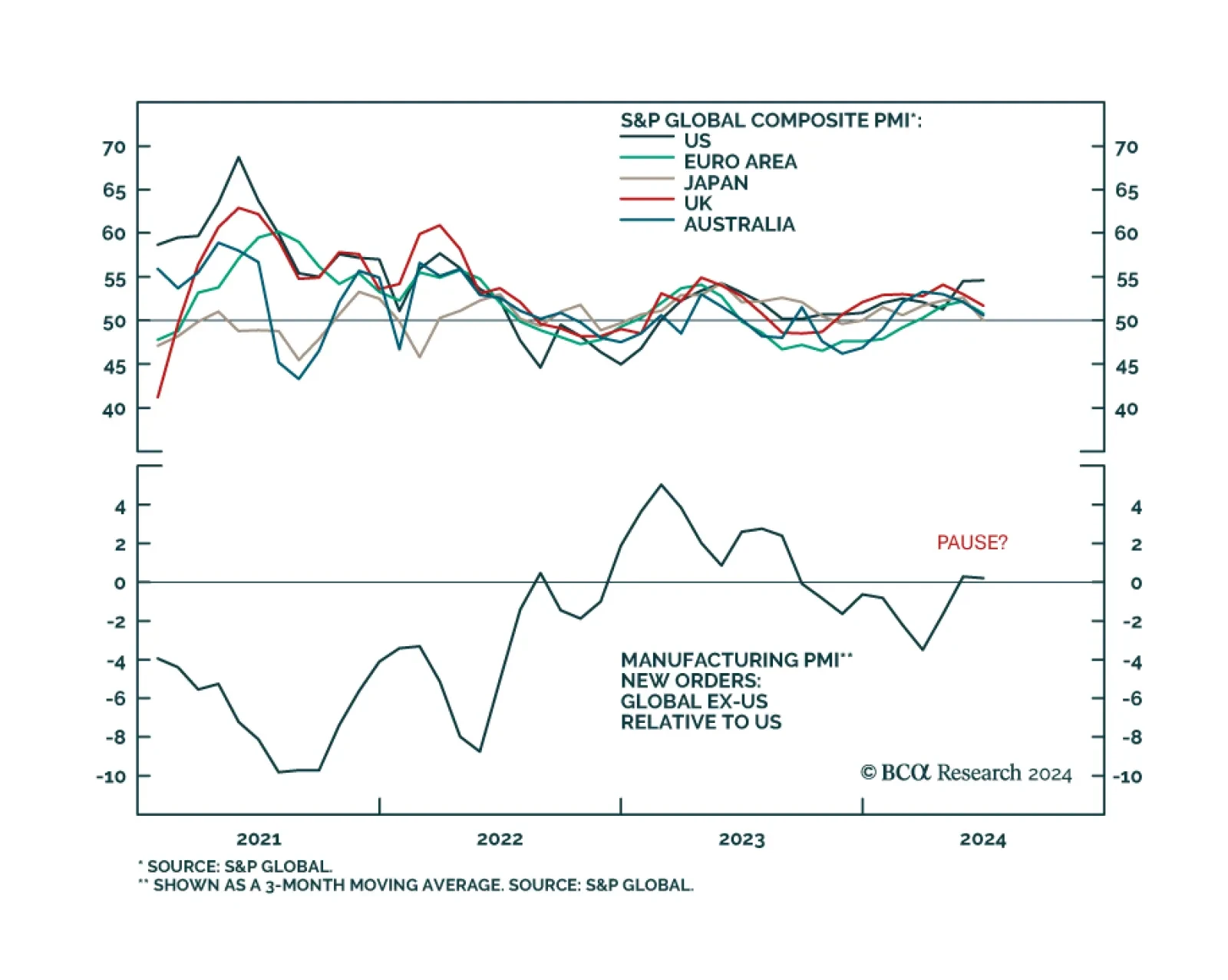

Preliminary PMI estimates suggest that US economic leadership remained intact in June, despite previous signs that it was passing the global growth baton to the rest of the world. US manufacturing, services and composite PMIs all surpassed expectations as…

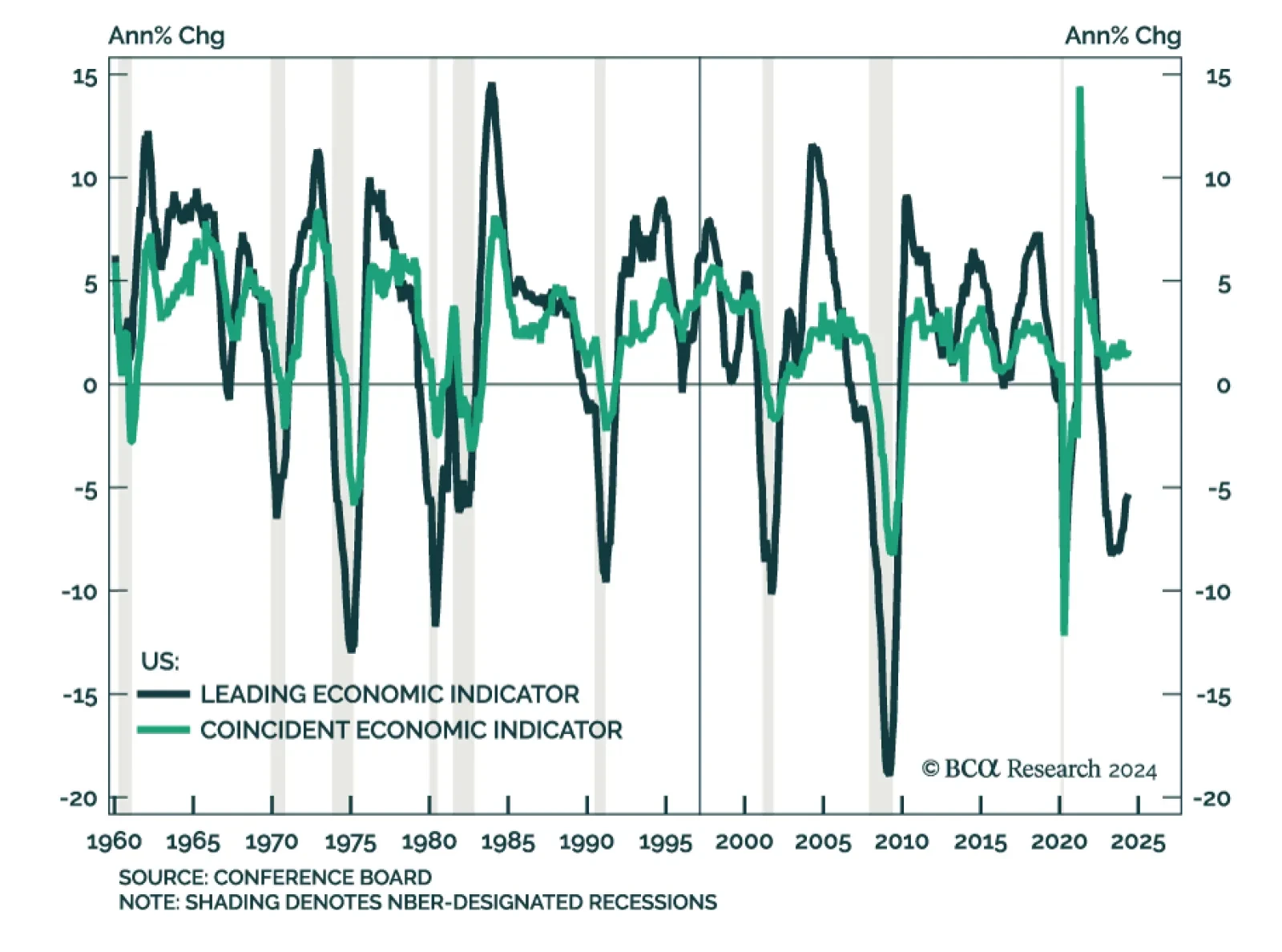

The Conference Board’s US Leading Economic Index (LEI) disappointed in May, contracting 0.5% m/m from a 0.6% decline in April. However, the Coincident Economic Index (CEI) grew 0.4% m/m in May. Year-on-year contractions in the LEI have reliably predicted…