United States

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

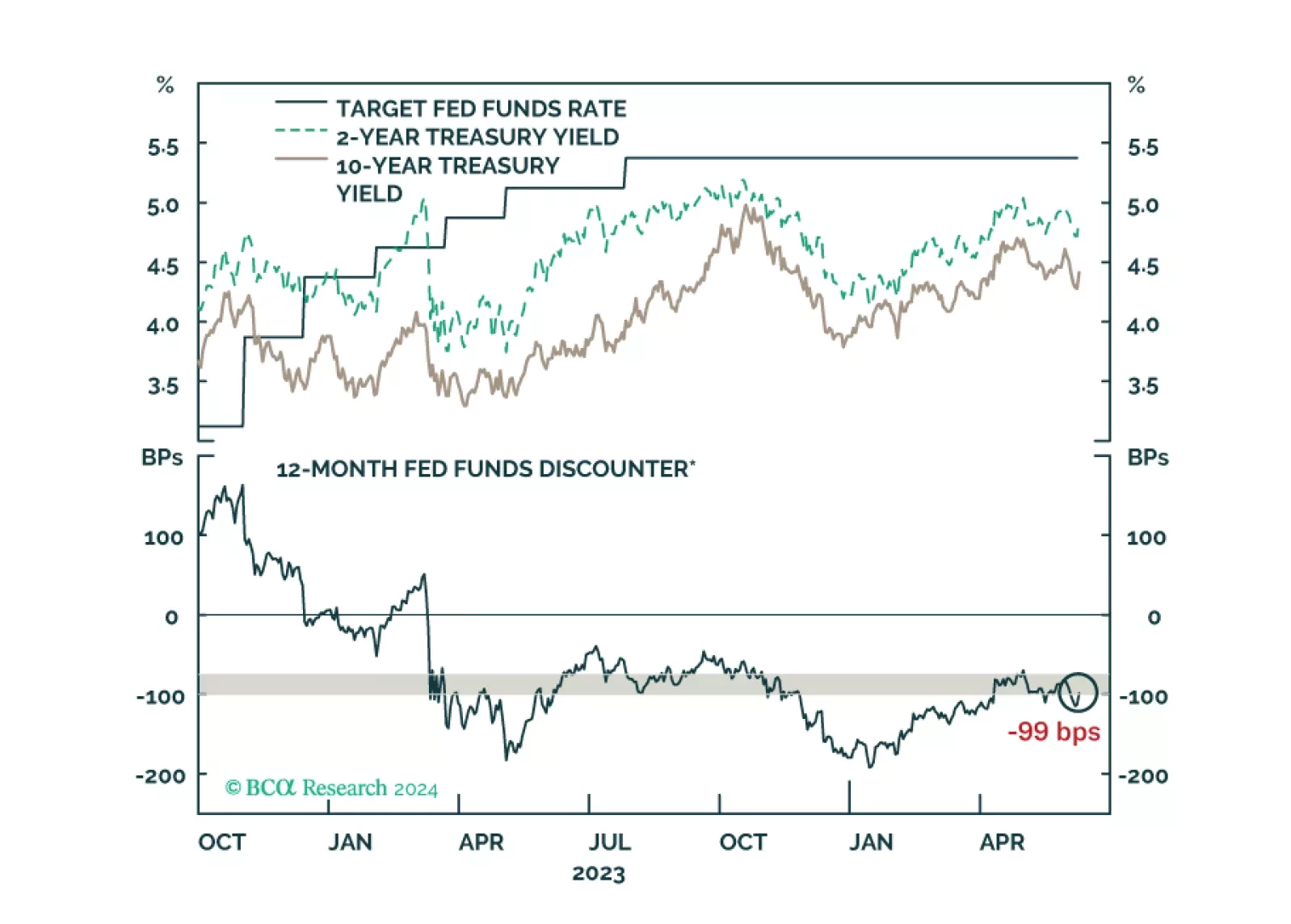

US Treasury yields bounced after this morning’s employment report. We offer our updated views about how long the recent trading range will hold.

The US economy remains on a path towards a recession, most likely starting in late 2024 or early 2025. For now, investors should maintain a benchmark allocation to equities, but employ a barbell strategy of overweighting defensives and materials.

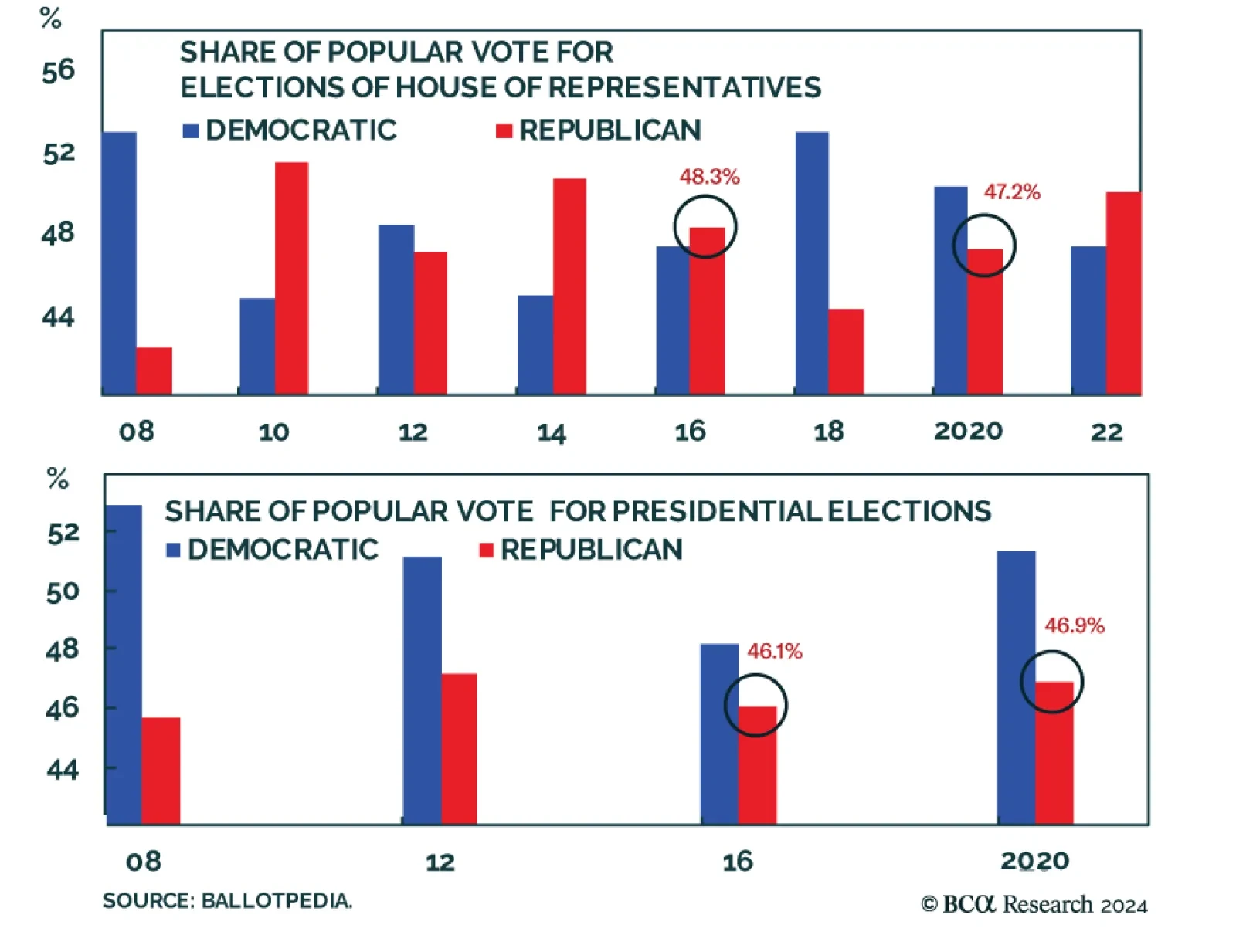

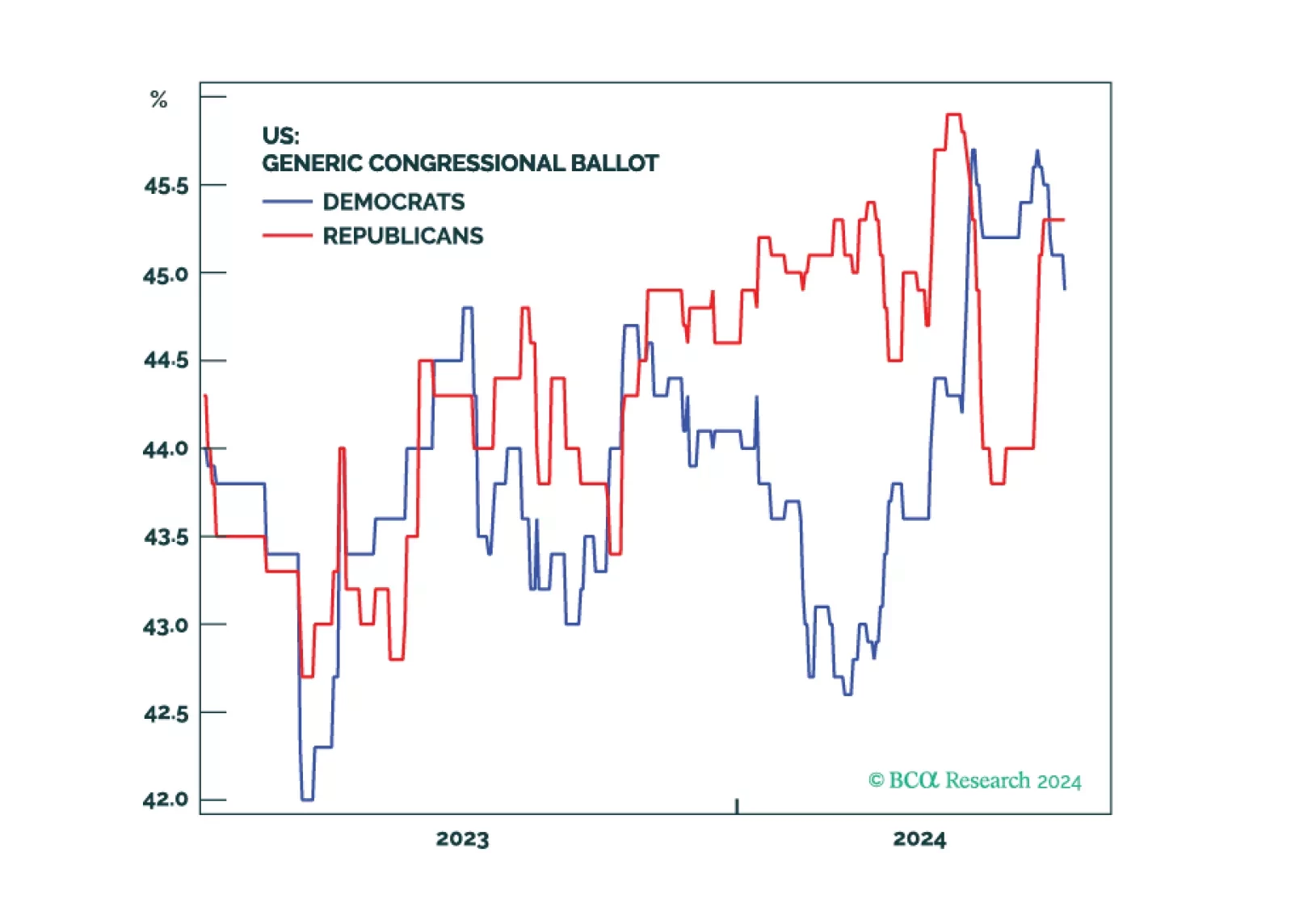

Republicans are favored in the House and Senate even if they do not win the White House. A Democratic sweep is a 20% risk. The policy implication would be inflationary, but not so much as under a Republican sweep. Election uncertainty should increasingly weigh on cyclical and high-beta assets in the second half of 2024.