United States

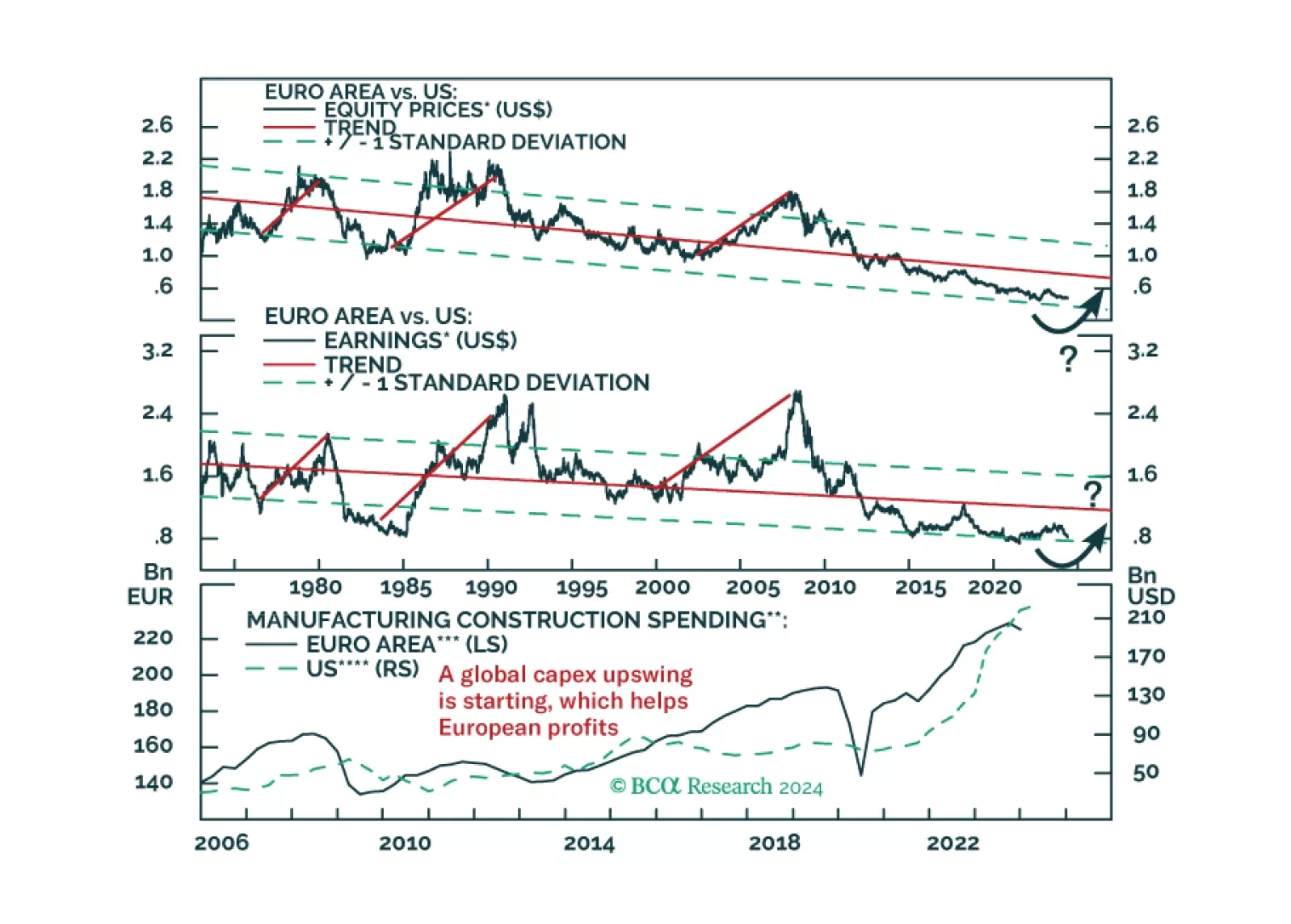

European stocks have massively underperformed US ones since the GFC. Demographics and productivity say this trend will continue, but is that really so?

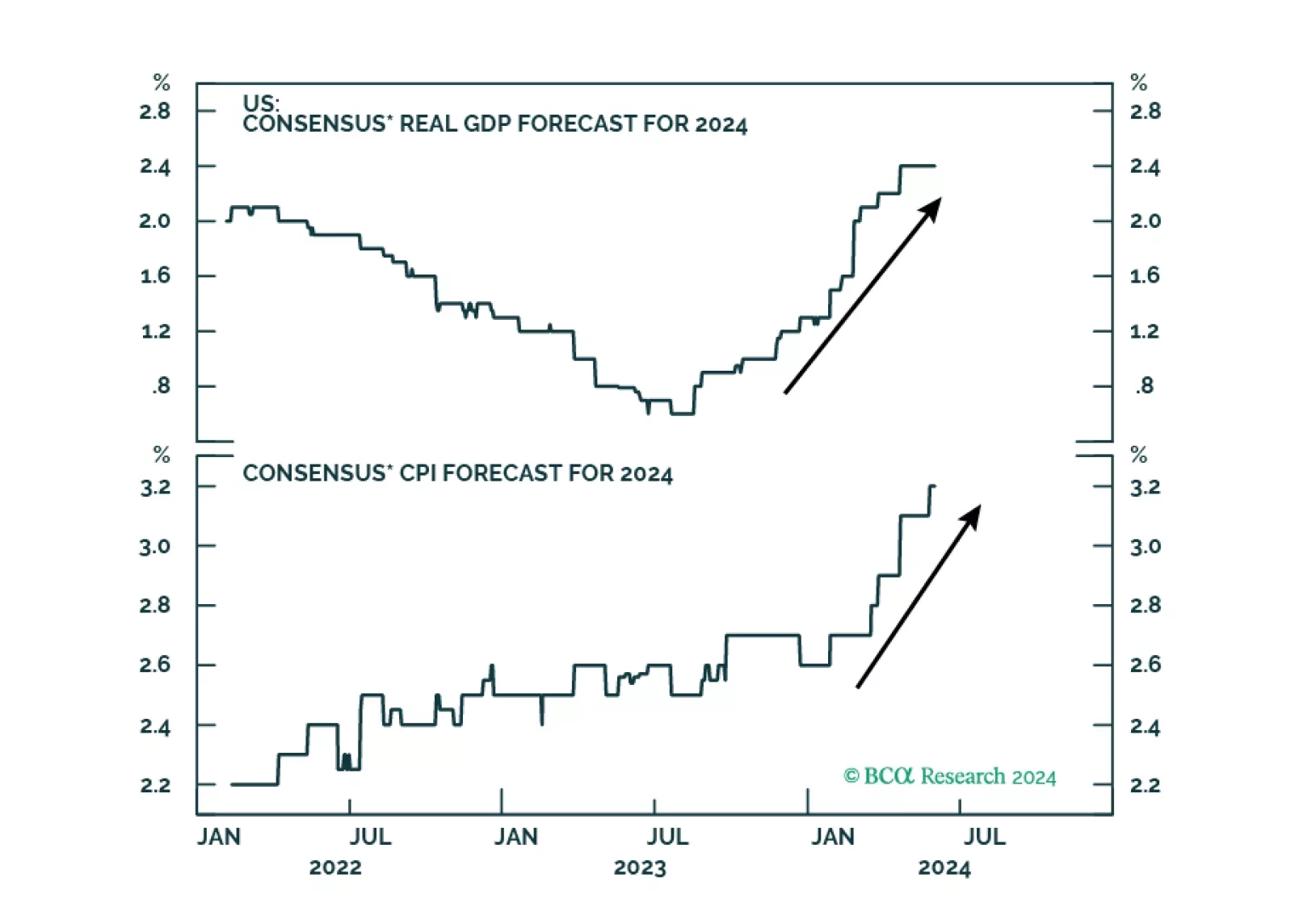

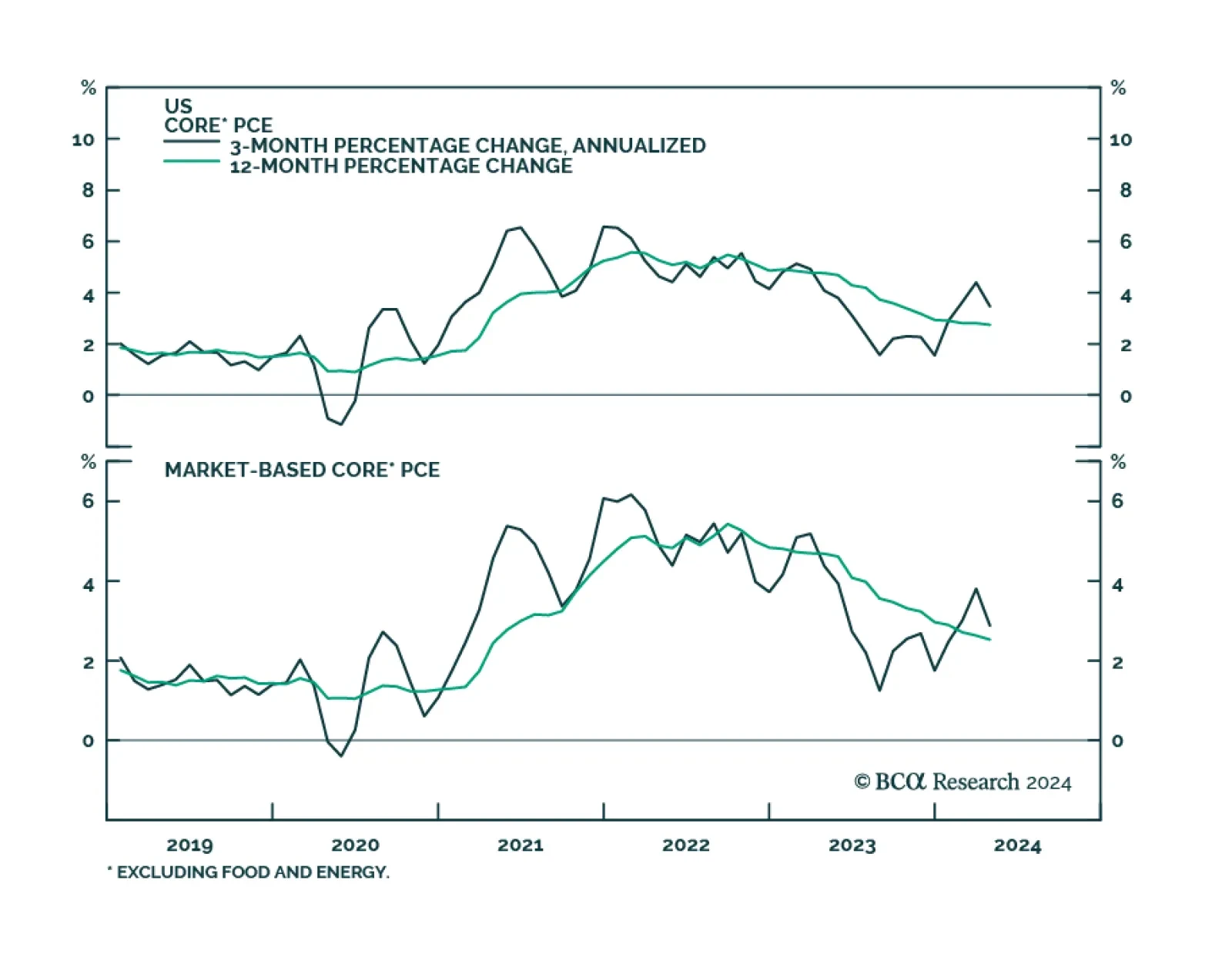

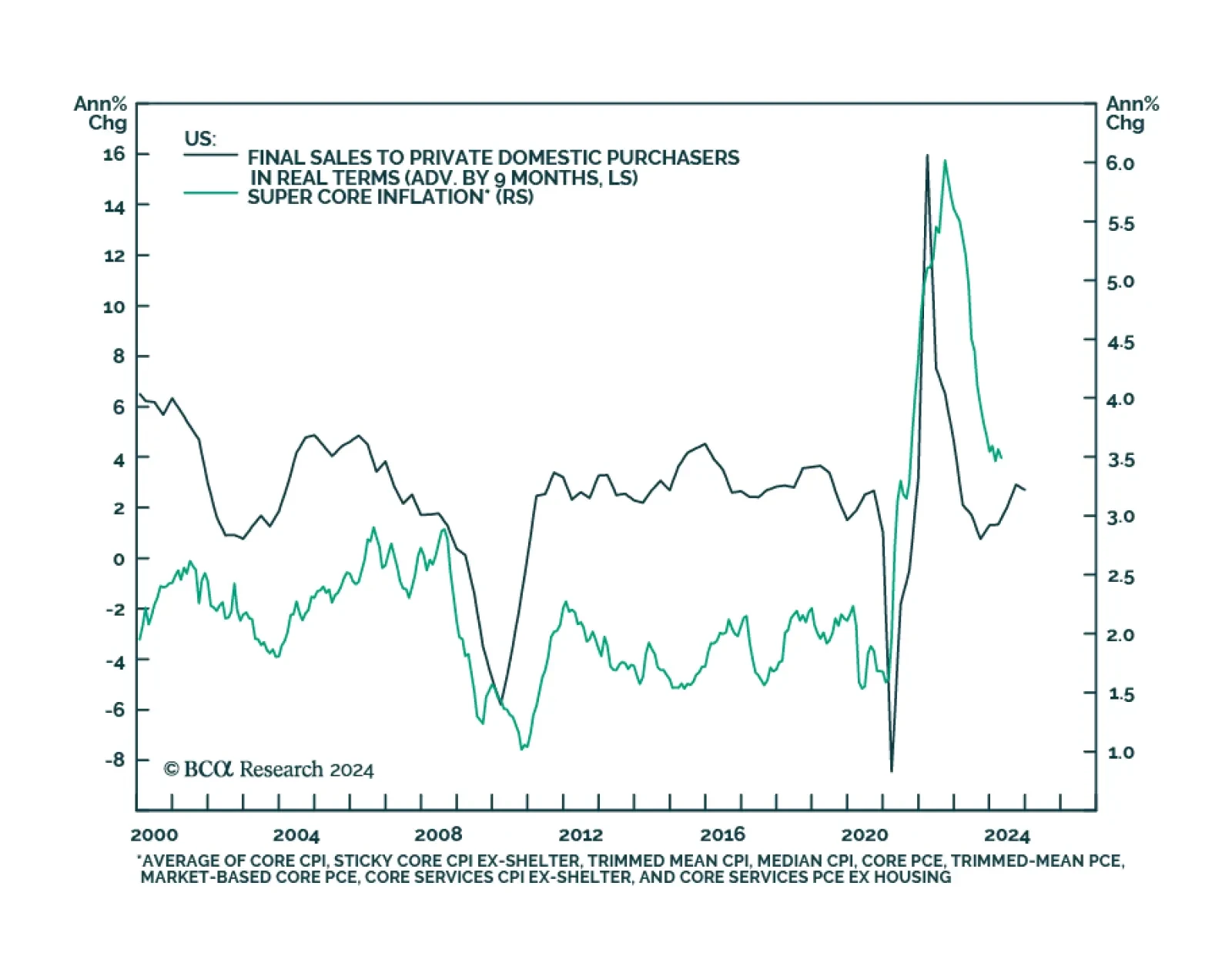

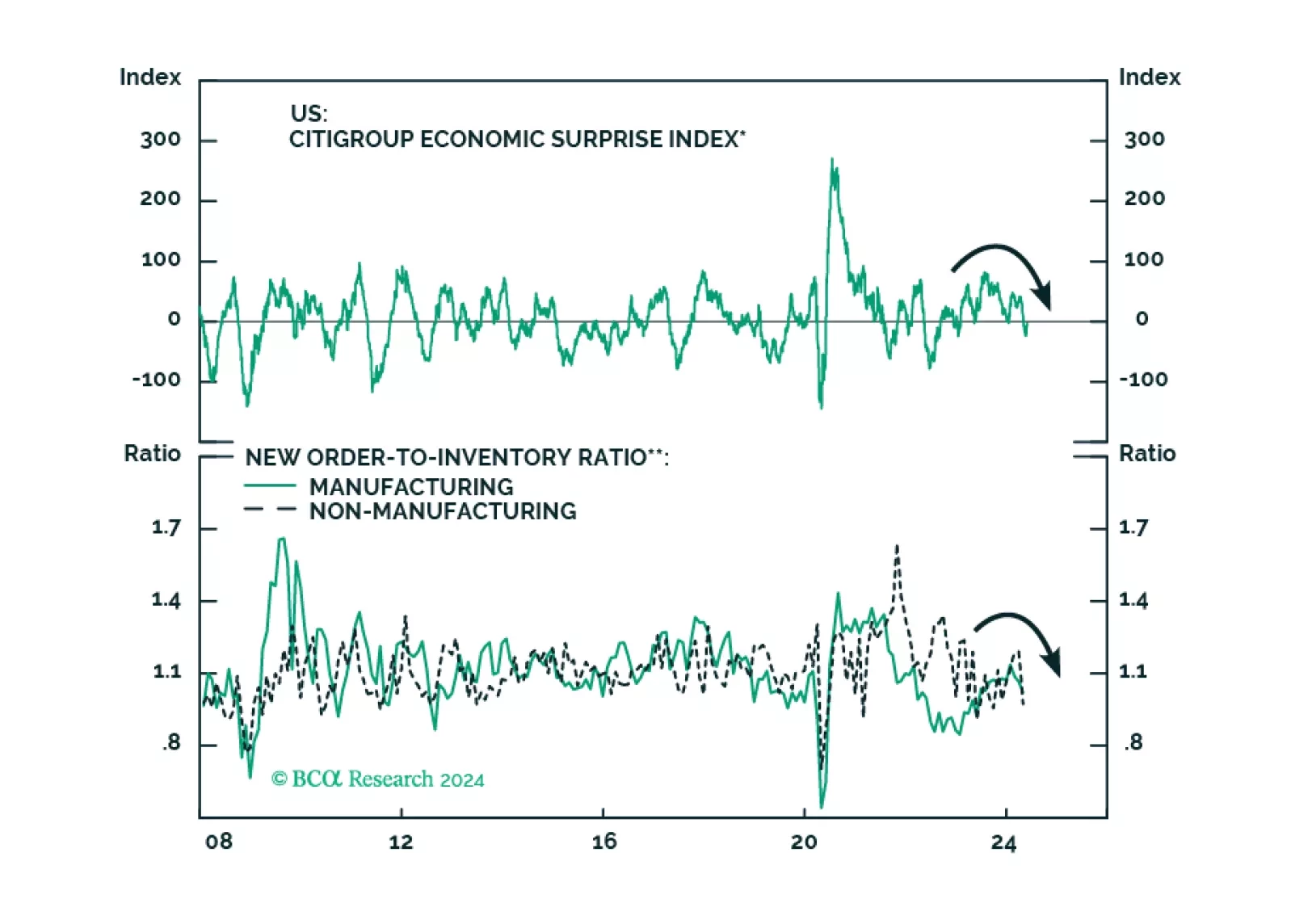

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

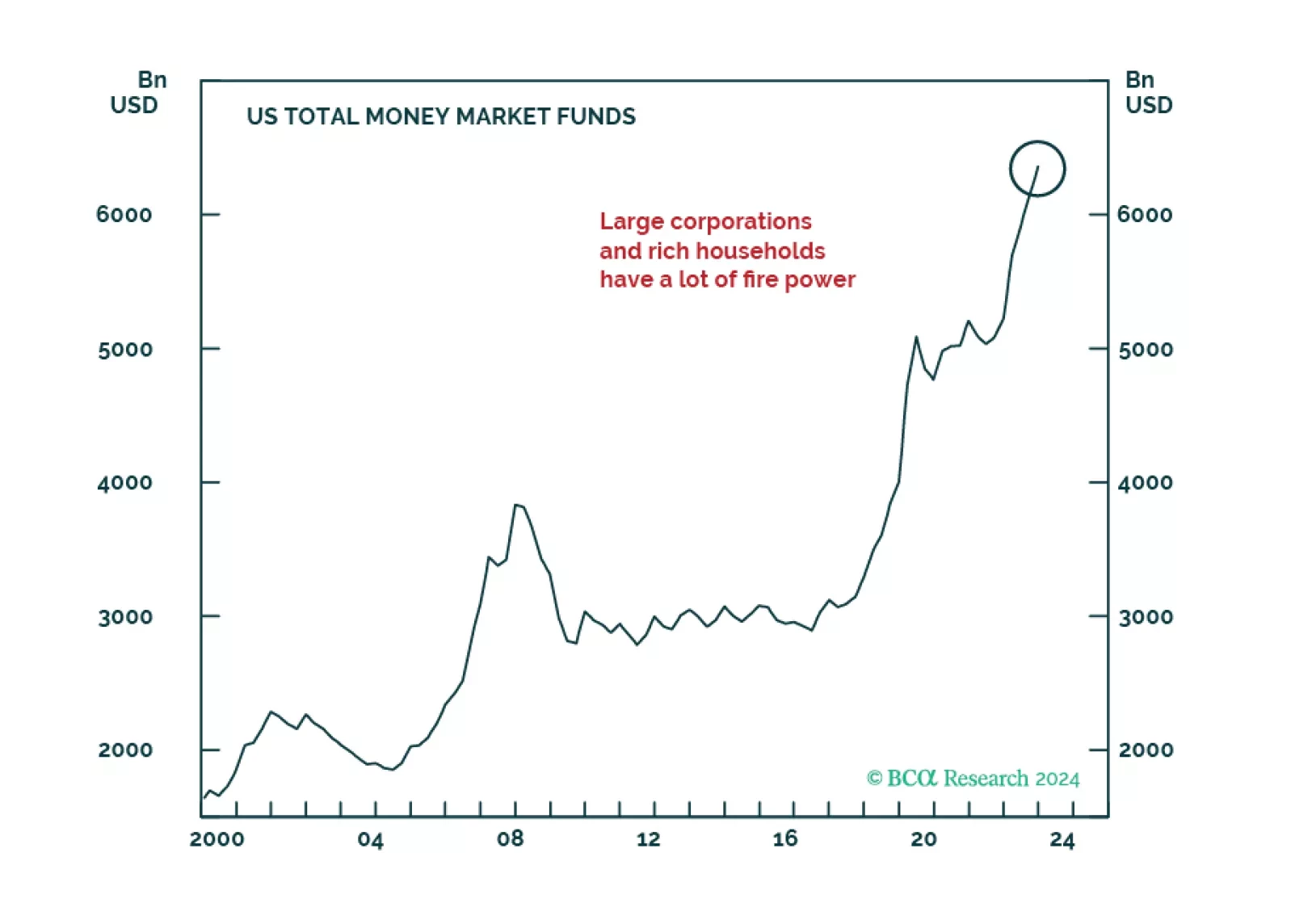

Generative AI-related rally resumed in May. Much of the recent market gains are down to excess liquidity that was begotten by the massive pandemic stimulus, creating a dichotomy between multiple economic challenges and exuberant markets. The Fed is unlikely to step in to prevent the bubble as it is currently more worried about the near-term downside for growth than financial stability.

Democrats remain slightly favored for the White House because they are the four-year incumbent presidential party and the economy is not in recession. But if the unemployment rate rises in the lead up to November, then Biden and Democrats will become disfavored regardless of Trump’s convictions.

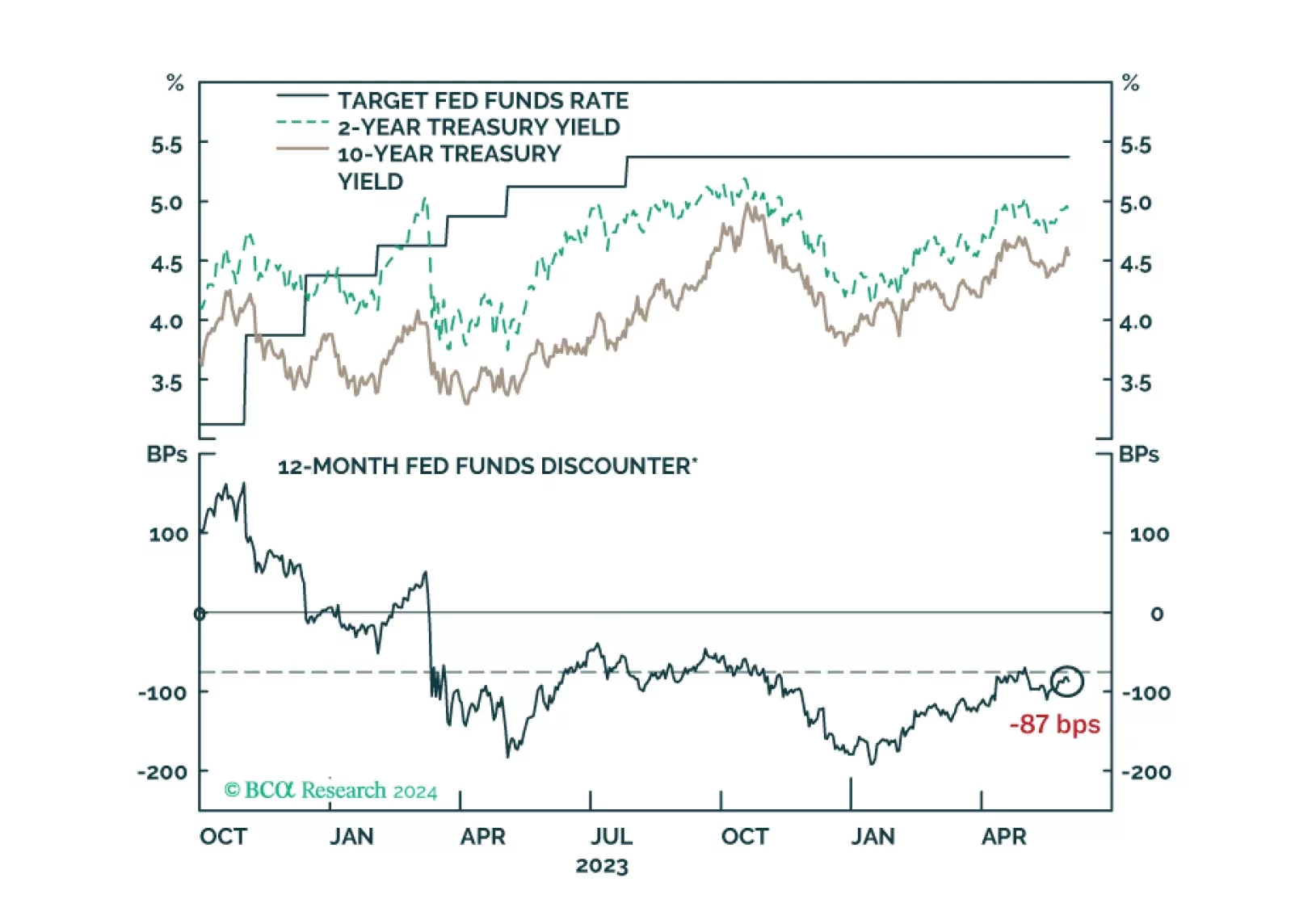

We comment on whether Treasury market valuation is sufficiently attractive to get long bonds and consider some of the common arguments for why yields may yet make new highs.

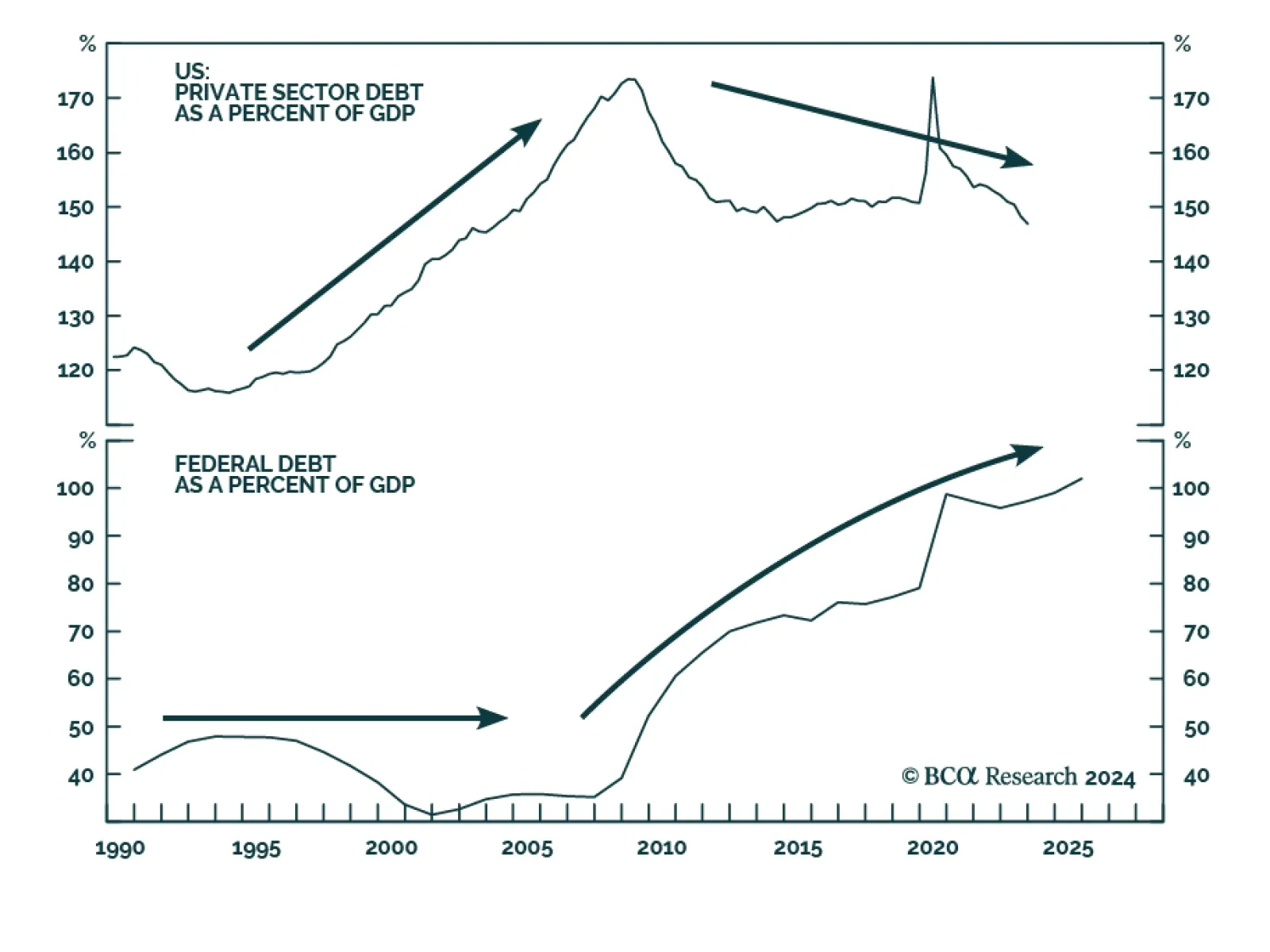

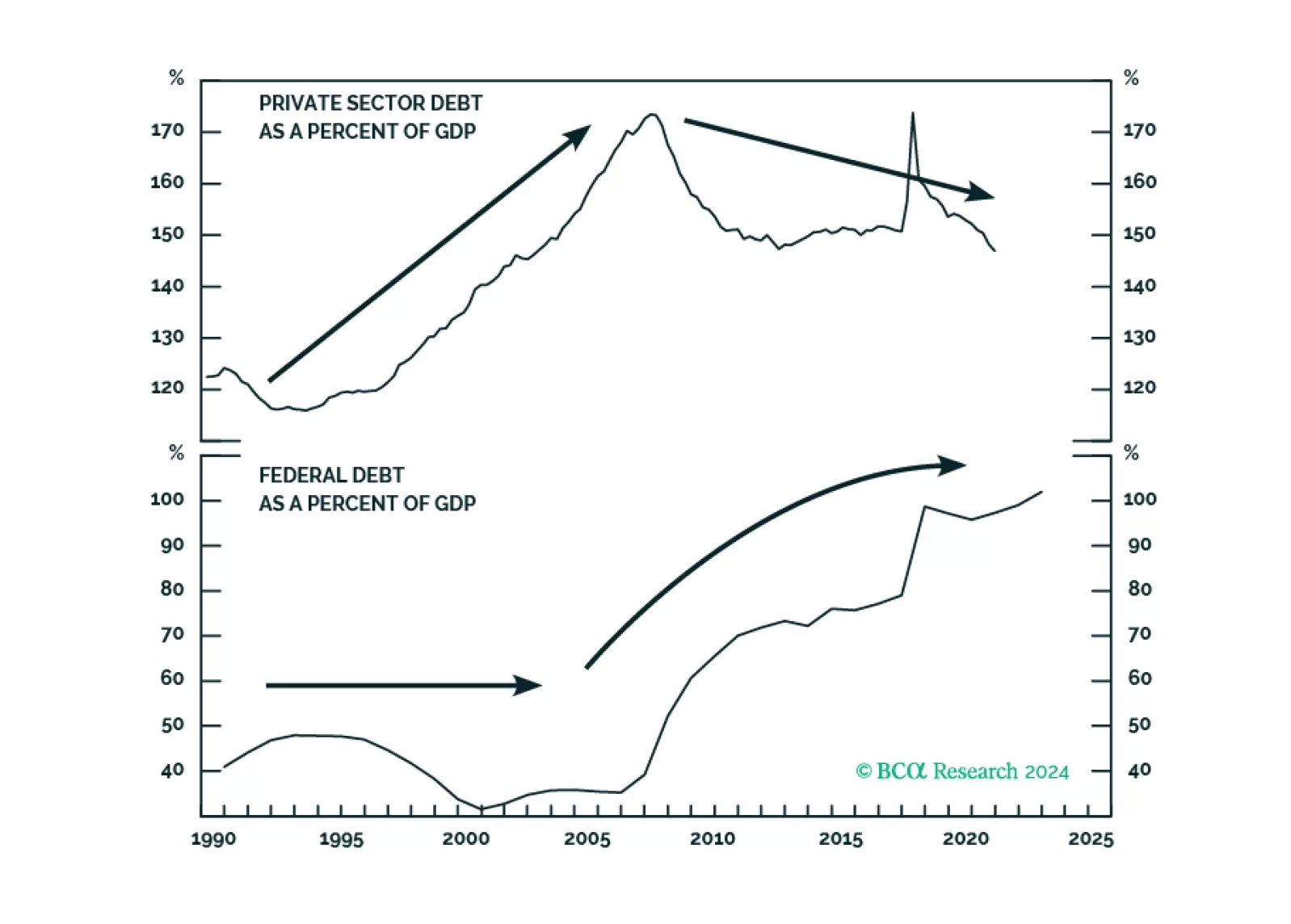

In a guest research report, Martin Barnes, BCA’s former Chief Economist, revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.