United States

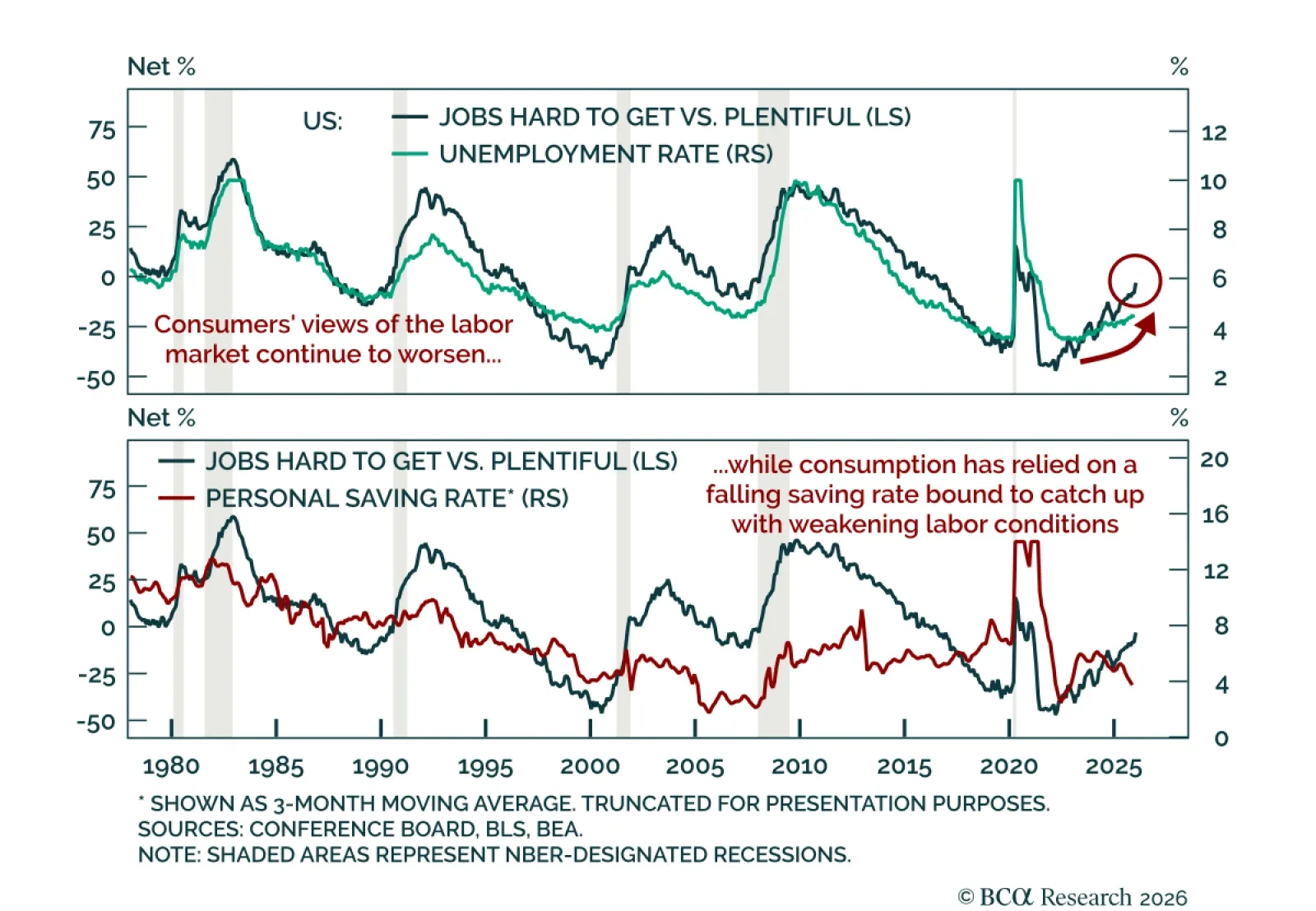

Stay long duration as weakening consumption and labor-market perceptions point to further Fed cuts. The January Conference Board survey missed estimates, with the headline index dropping to 84.5 from 94.2. The decline was driven by a weaker assessment of both…

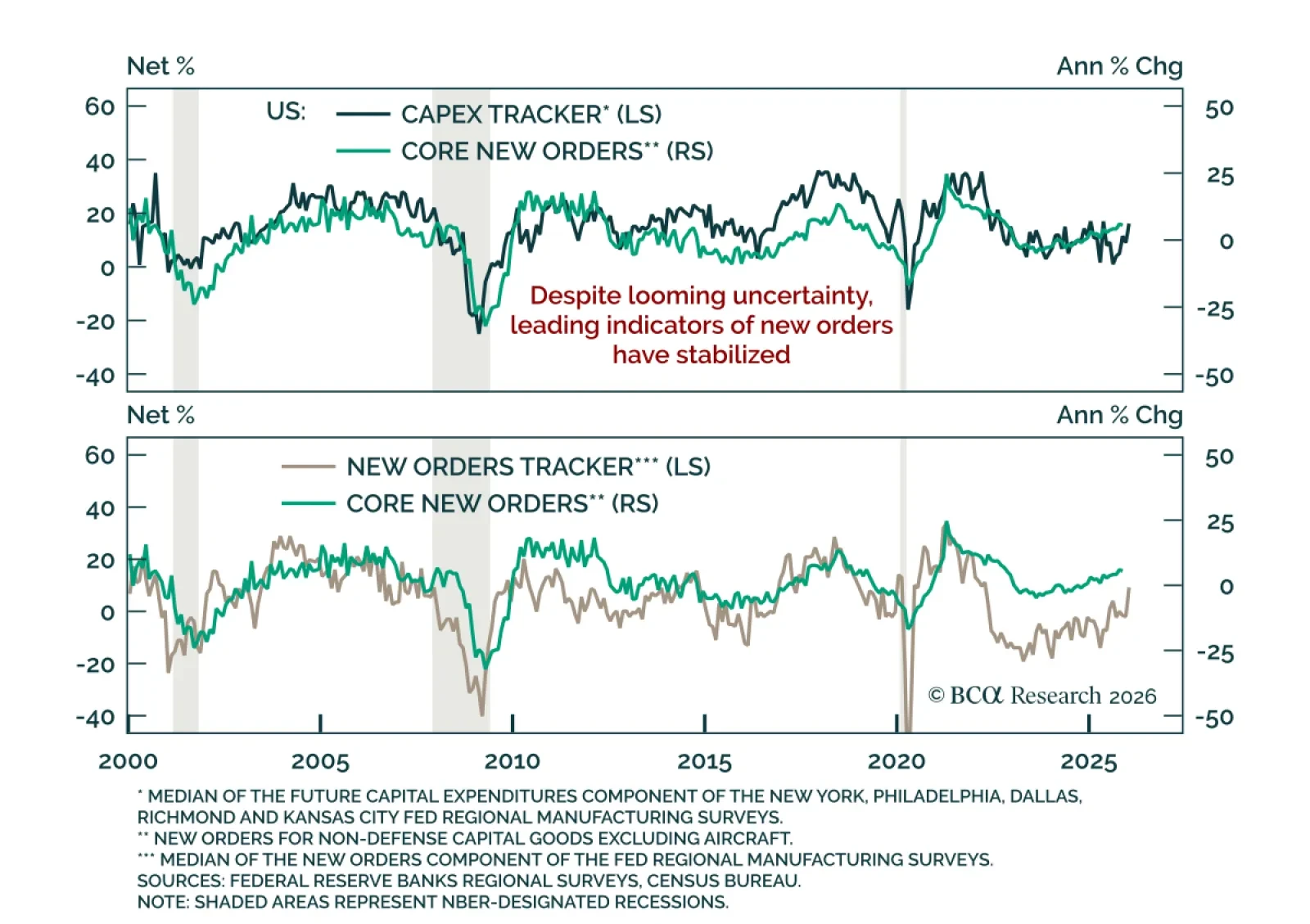

US manufacturing indicators point to stabilizing yet muted growth. US November manufacturing orders beat expectations. New orders for non-defense capital goods excluding aircraft rose 0.7% m/m, accelerating from a 0.3% increase in October, while shipments…

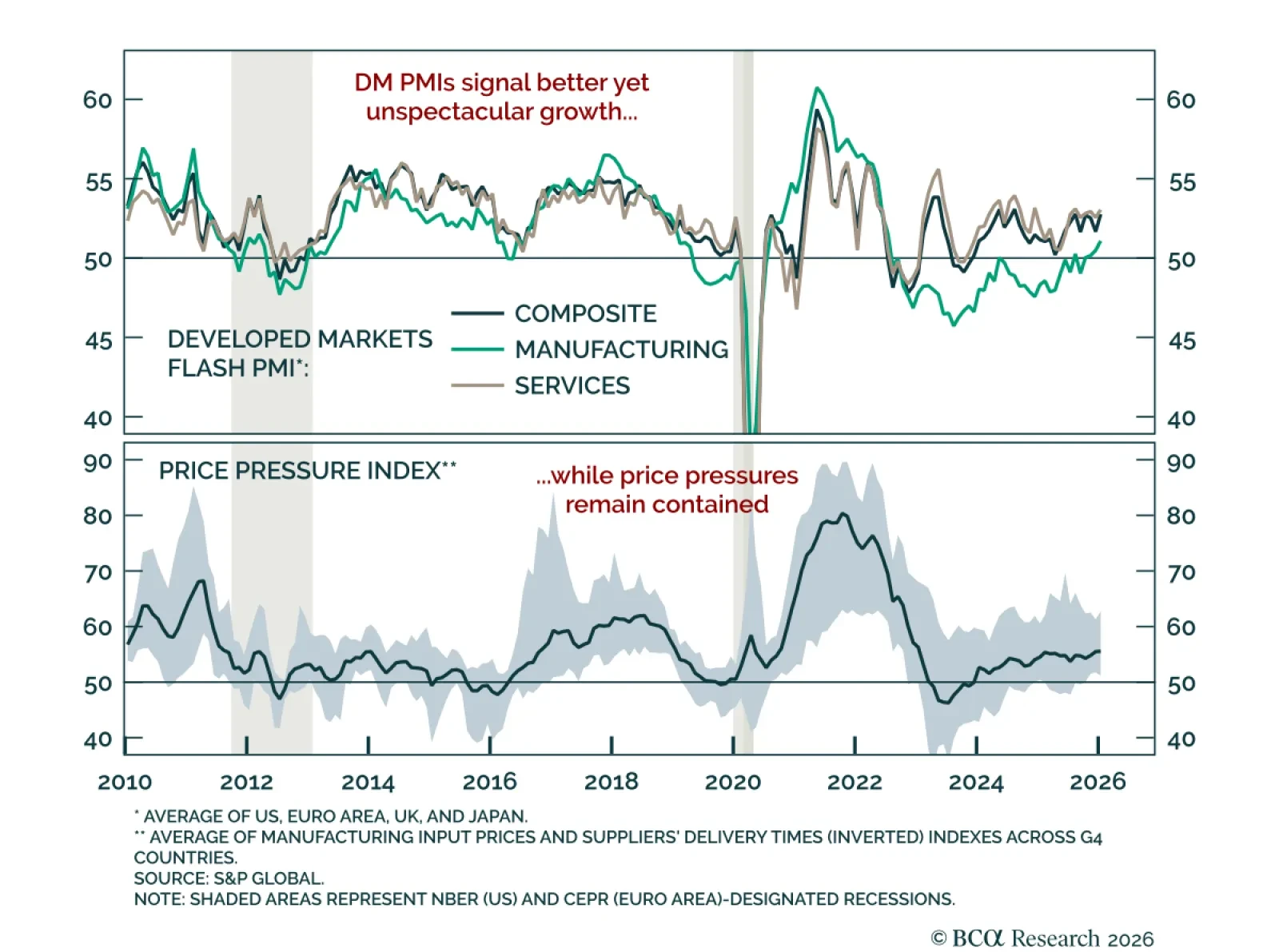

January flash PMIs point to better, though unspectacular, global growth momentum. Developed markets PMIs showed improvement in global growth momentum. PMIs have largely moved sideways through 2025, with manufacturing now recovering after trade uncertainty and…

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

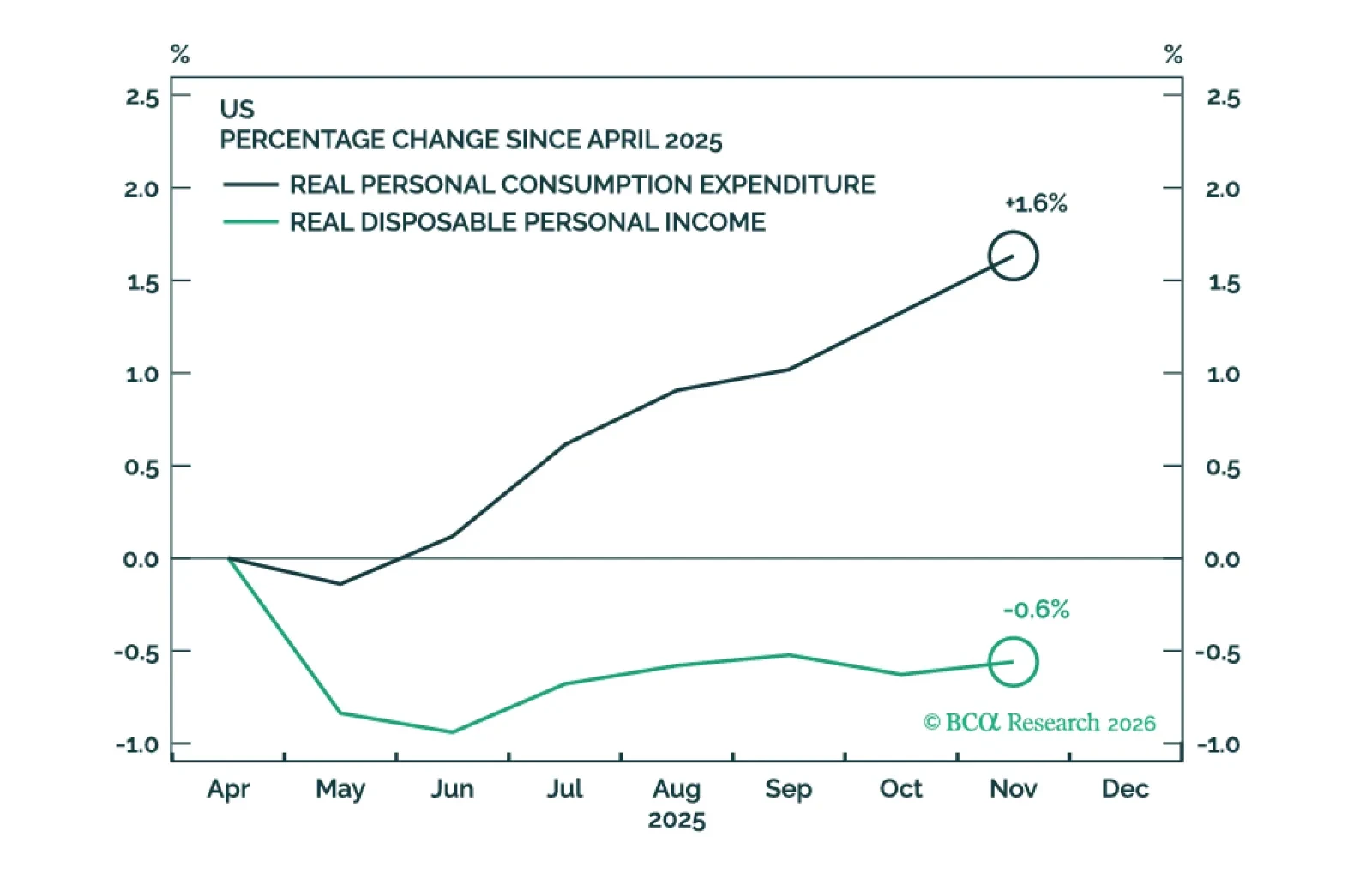

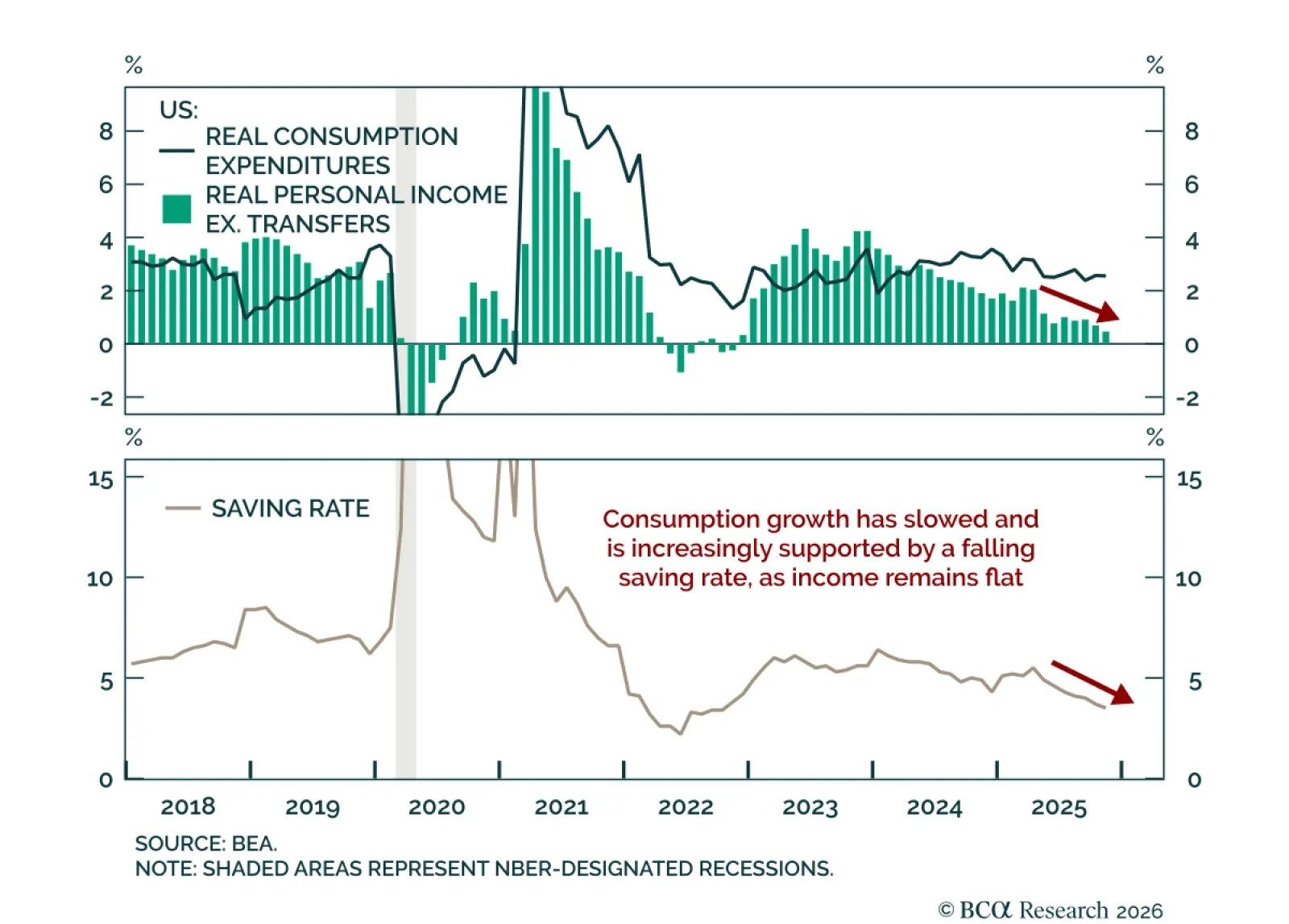

Maintain a modestly defensive stance as consumption fundamentals become increasingly fragile. US consumption in October and November was stronger than expected, but its support pillars have become more fragile. Real spending rose 0.3% m/m in both October and…

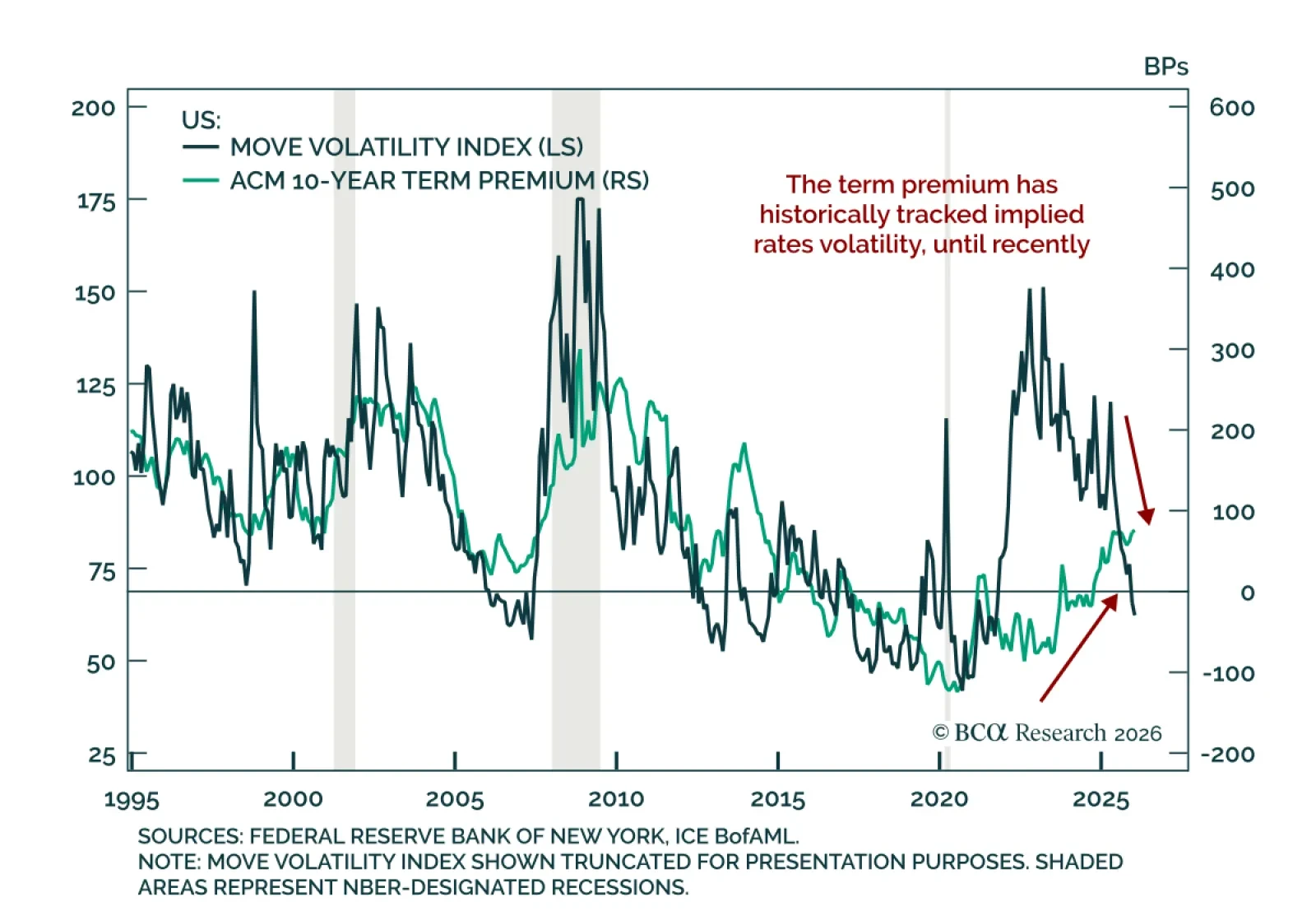

Our US Bond strategists expect long duration positions to outperform long credit risk in 2026. The Treasury term premium remains high despite declining rates volatility and tight credit spreads. The divergence between the term premium and interest rate…

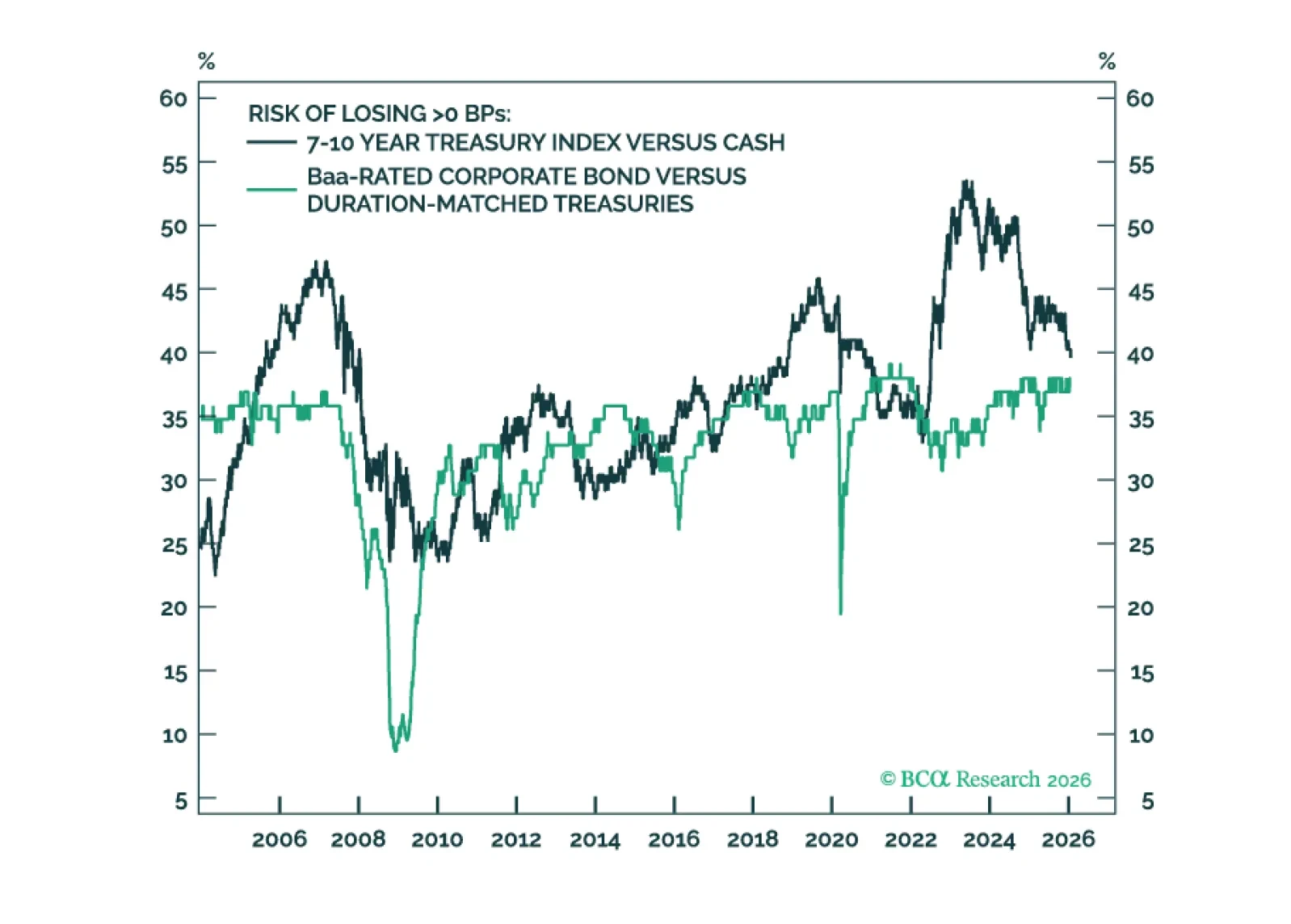

The 10-year Treasury term premium is now competitive with Baa- and Ba-rated credit spreads. Even without term premium compression, duration carry trades could outperform credit carry trades in a low rate vol environment.

Do not add tactical risk yet, and monitor rates volatility for a potential re-entry point. A key factor supporting the S&P 500 beyond the AI narrative in 2025 has been declining rates volatility. Despite occasional wobbles, the MOVE index trended lower…

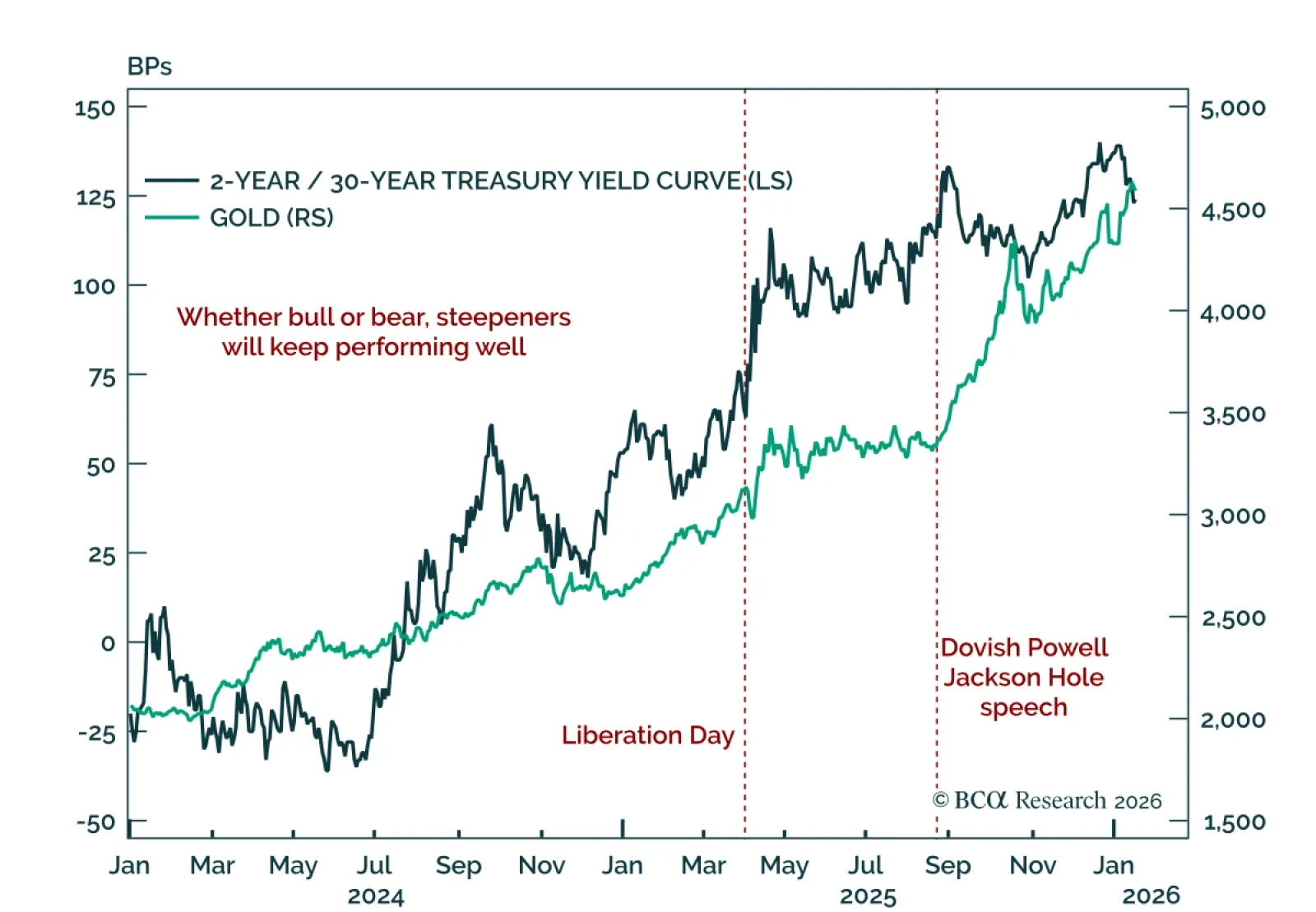

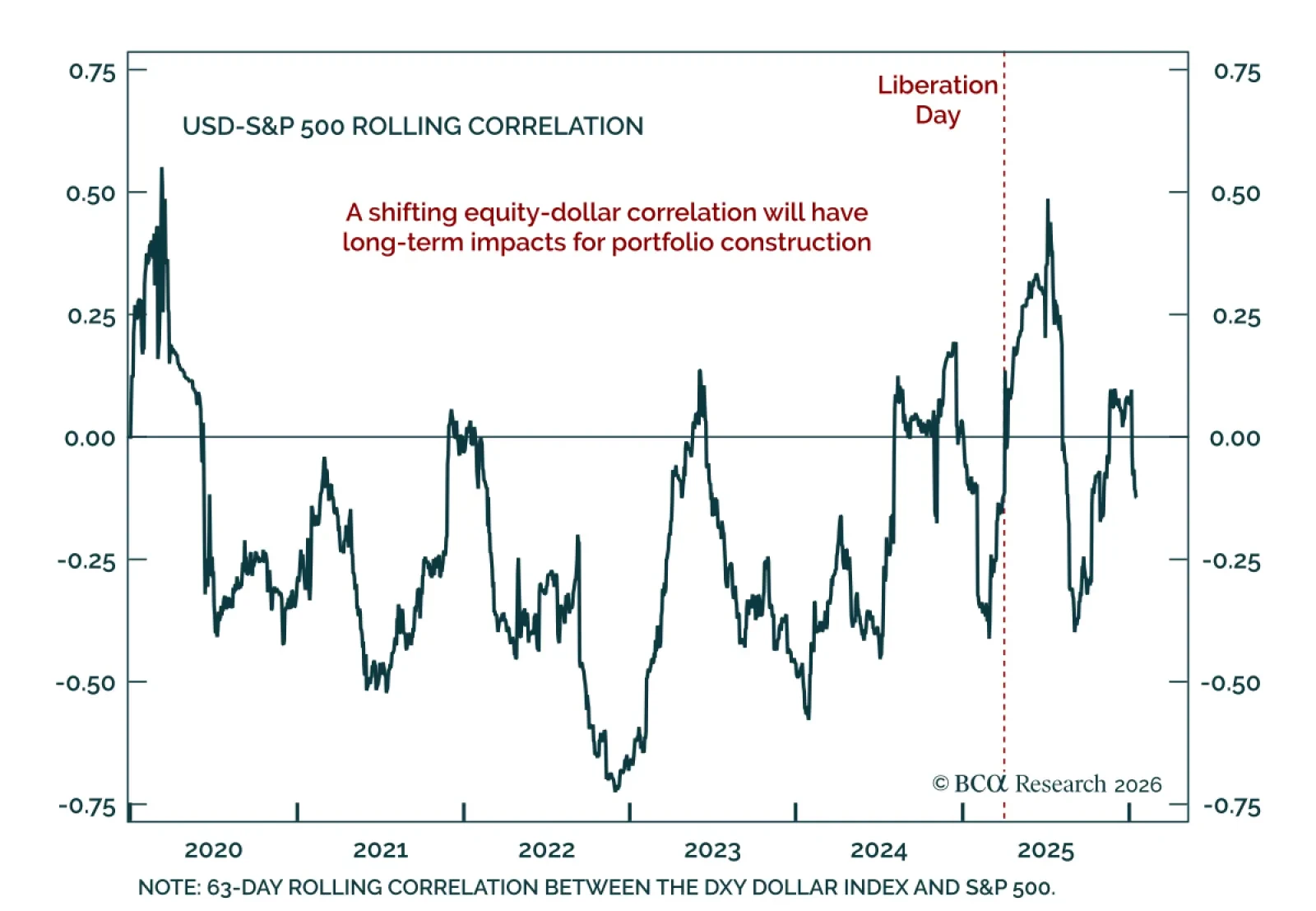

Favor curve steepeners and gold as recent price action highlights rising term premia and diversification away from US assets. With markets closed on Monday for the MLK holiday, Tuesday’s session saw price action reminiscent of last year’s “Sell America” trade…

Remain cautious on US equities and the dollar. Our monthly BCA Views meeting concluded that the outlook has become slightly more constructive. Recession risk over the next 6-12 months remains elevated but has diminished as growth and labor market conditions…