United States

An adverse shock is not a recession prerequisite. The empirical record shows that the US economy regularly evolves its way into a contraction with little fanfare. If current cooling trends continue, we project a recession will begin in late 2024/early 2025. …

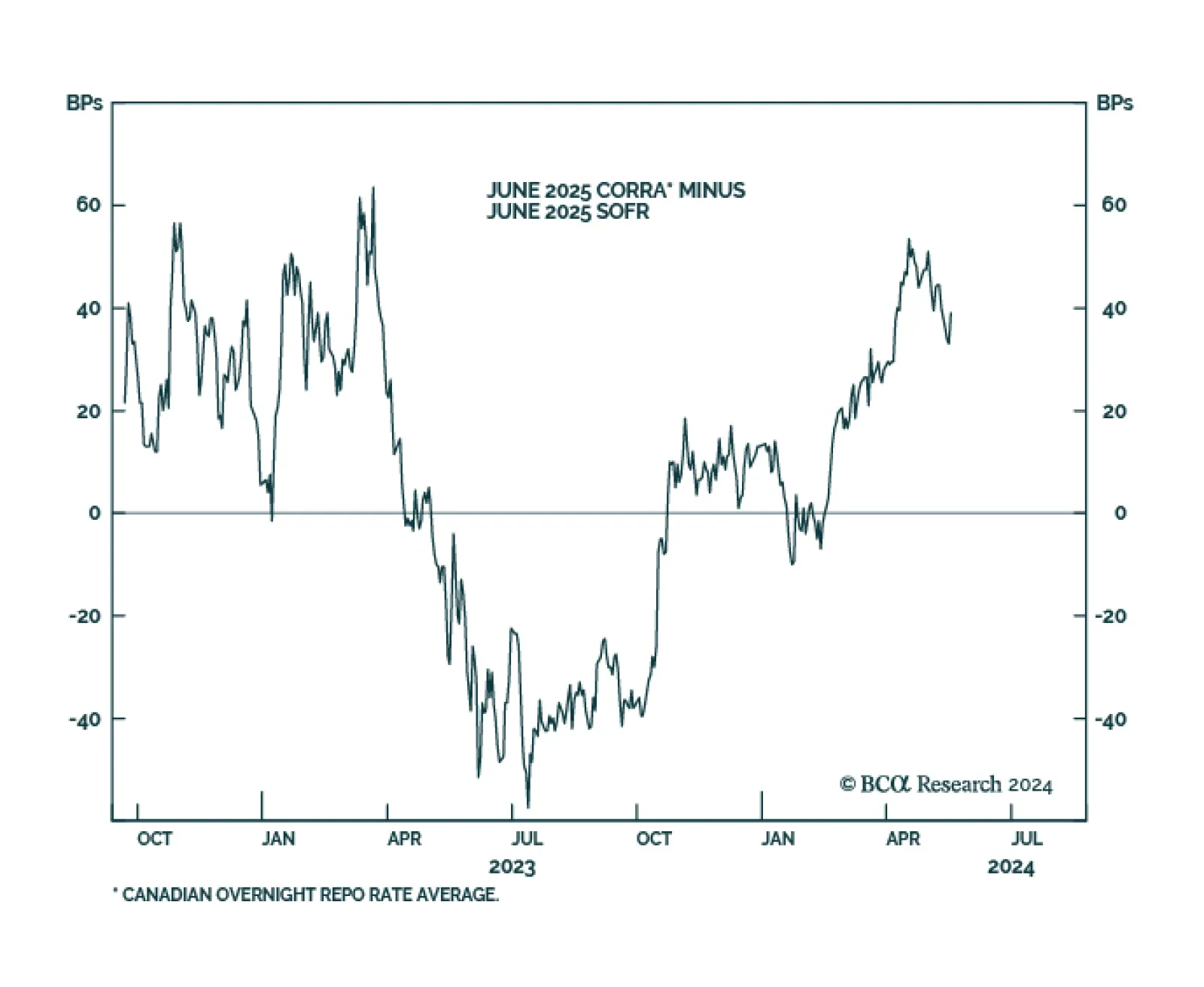

According to BCA Research’s Global Investment Strategy service, the BoC should have sufficient evidence of Canadian disinflation to cut rates this summer. The market is pricing in a similar amount of rate cuts for the BoC and the Fed over the next 12 months.…

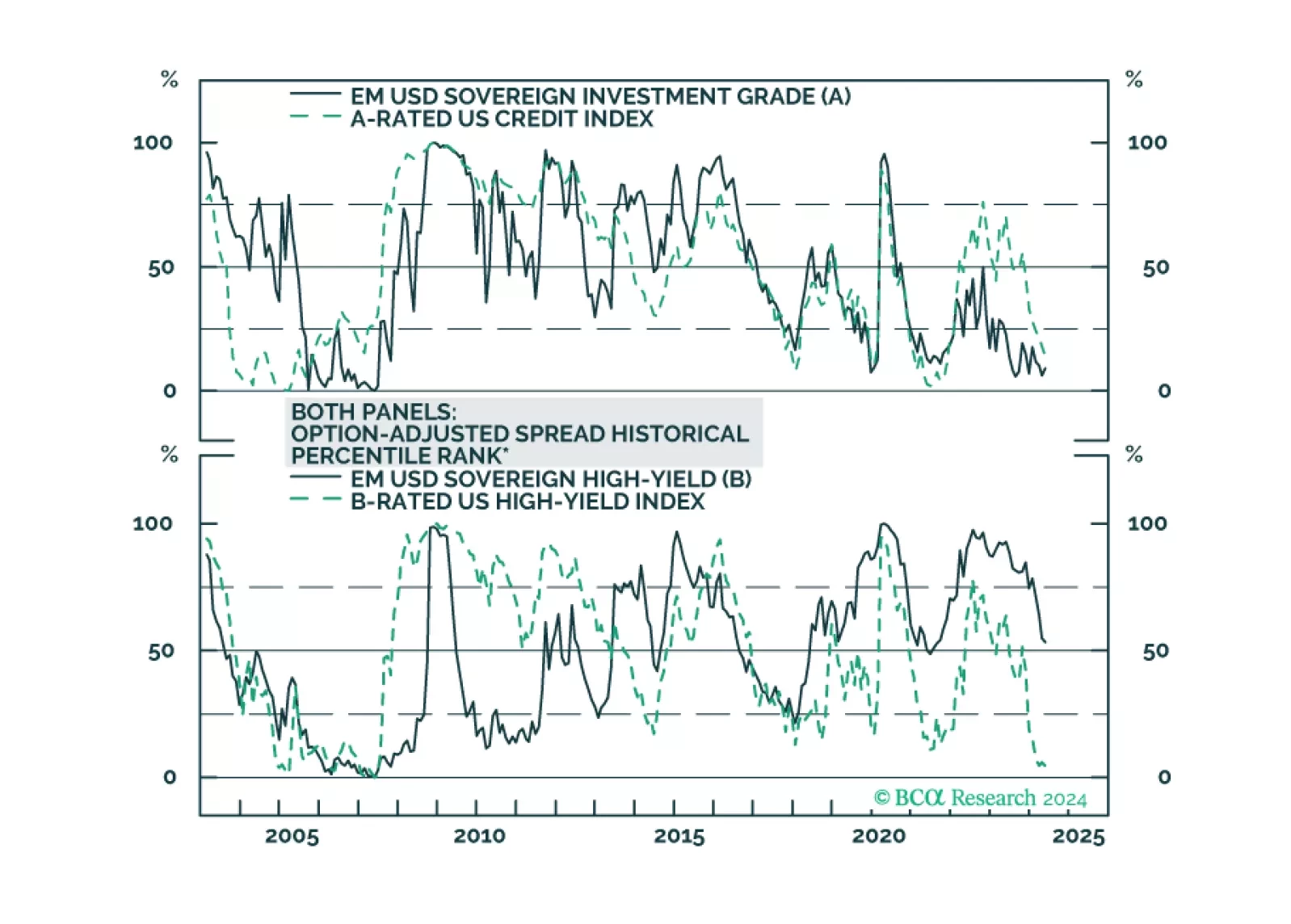

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

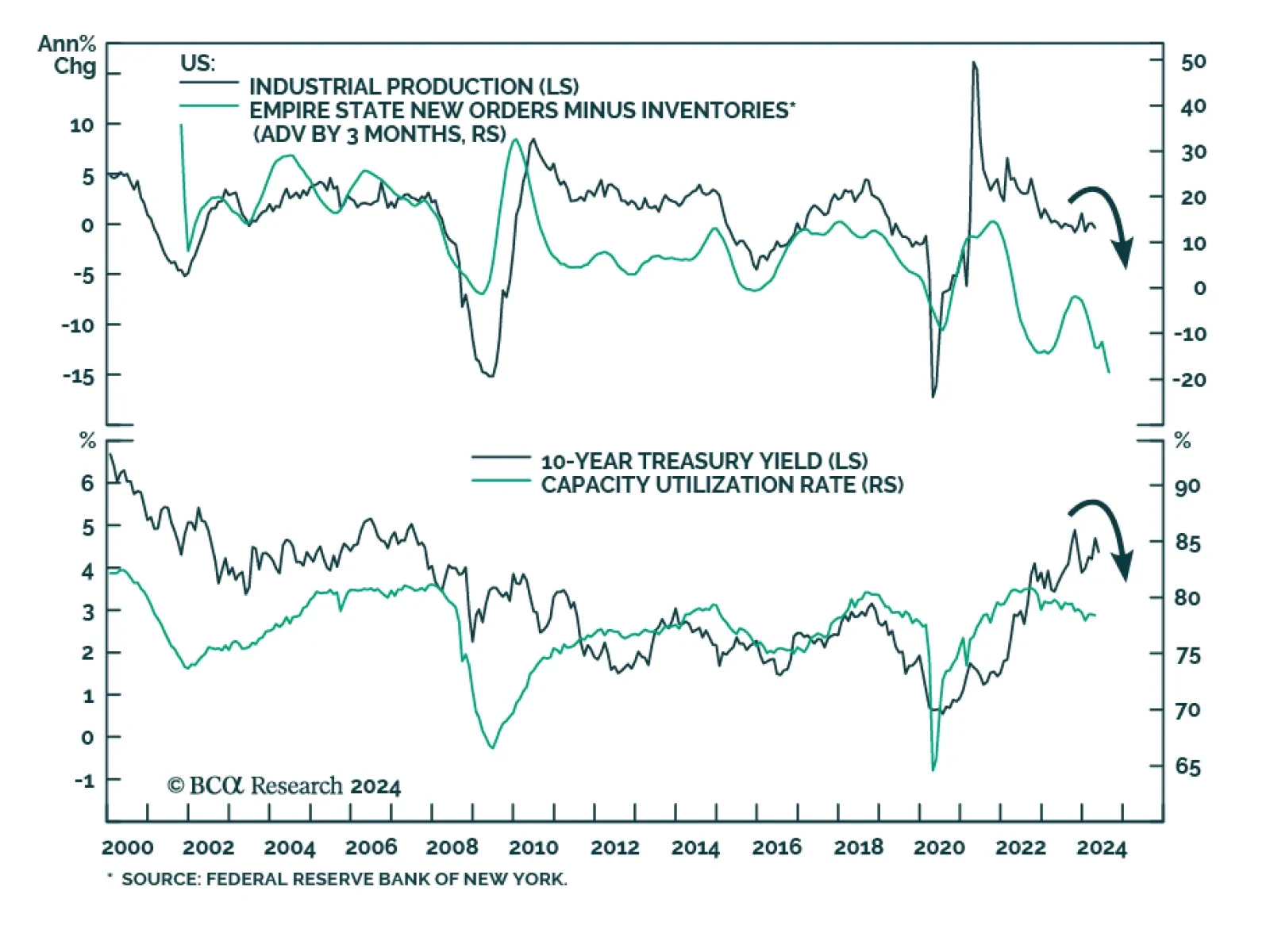

US industrial production stalled in April against expectations of a moderate pace of growth (0.1% m/m) and March’s growth rate was revised lower from 0.4% m/m to 0.1% m/m. Notably, pro-cyclical manufacturing production unexpectedly contracted 0.3% m/m from a…

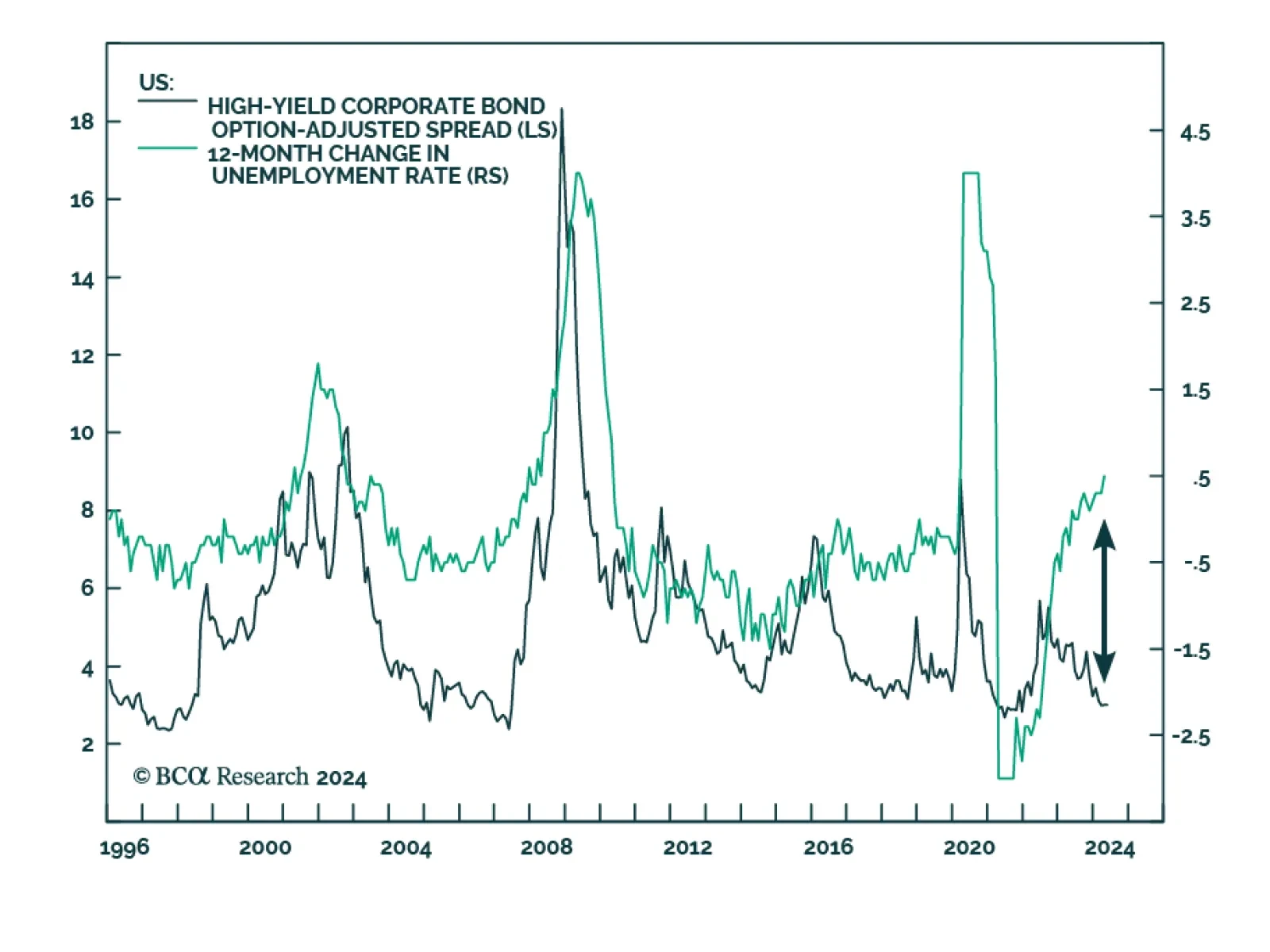

Credit spreads continue to price in a Goldilocks scenario. US investment grade and high-yield OAS have tightened 41 and 137 bps from their October peaks, resulting in handsome outperformance by both sectors relative to duration-equivalent Treasuries. …

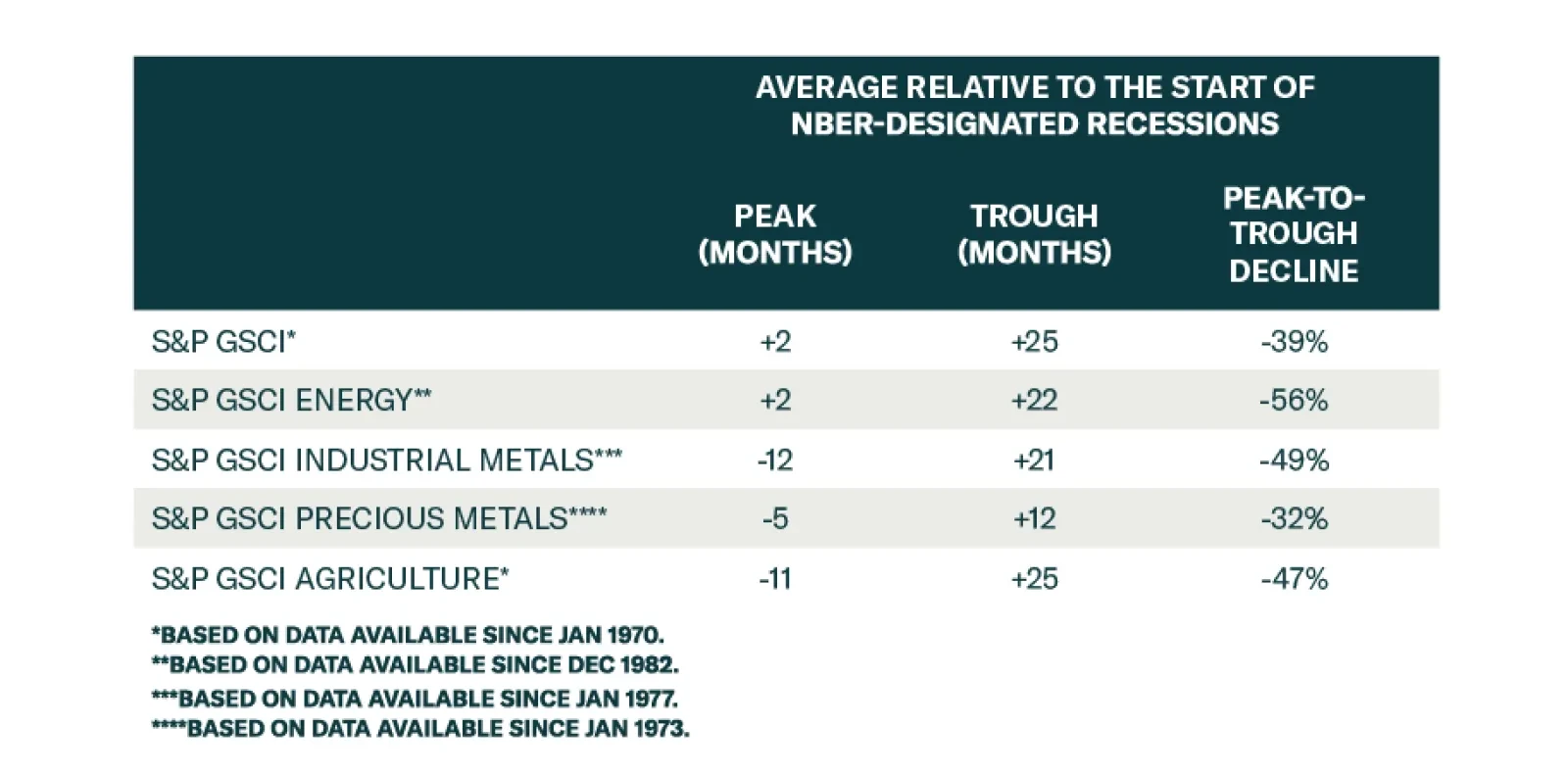

According to BCA Research’s Commodity & Energy Strategy service, among the commodity groups, industrial metals provide the most reliable leading signal that the US economy is heading toward recession. Industrial metals’ greater exposure to the very…

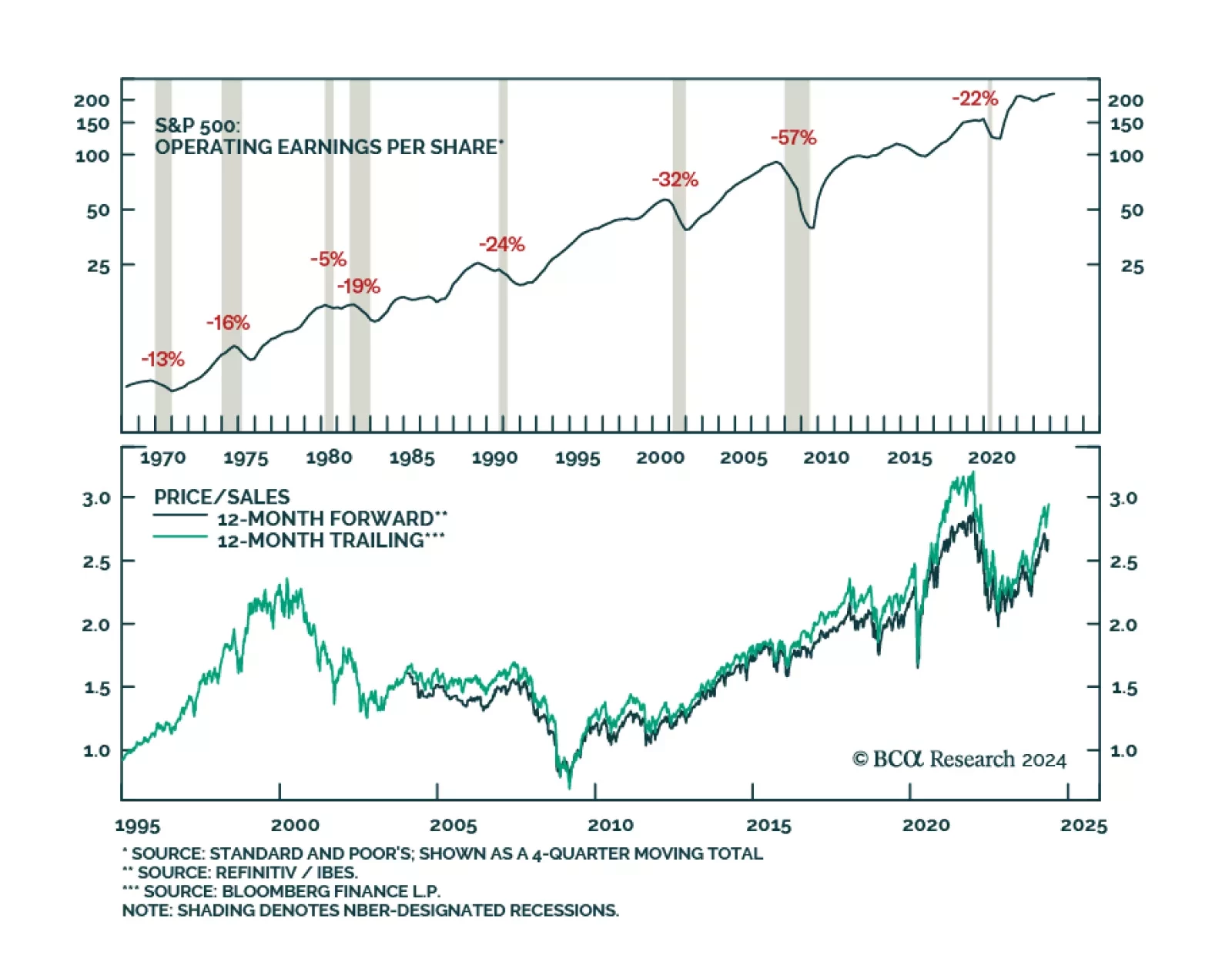

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

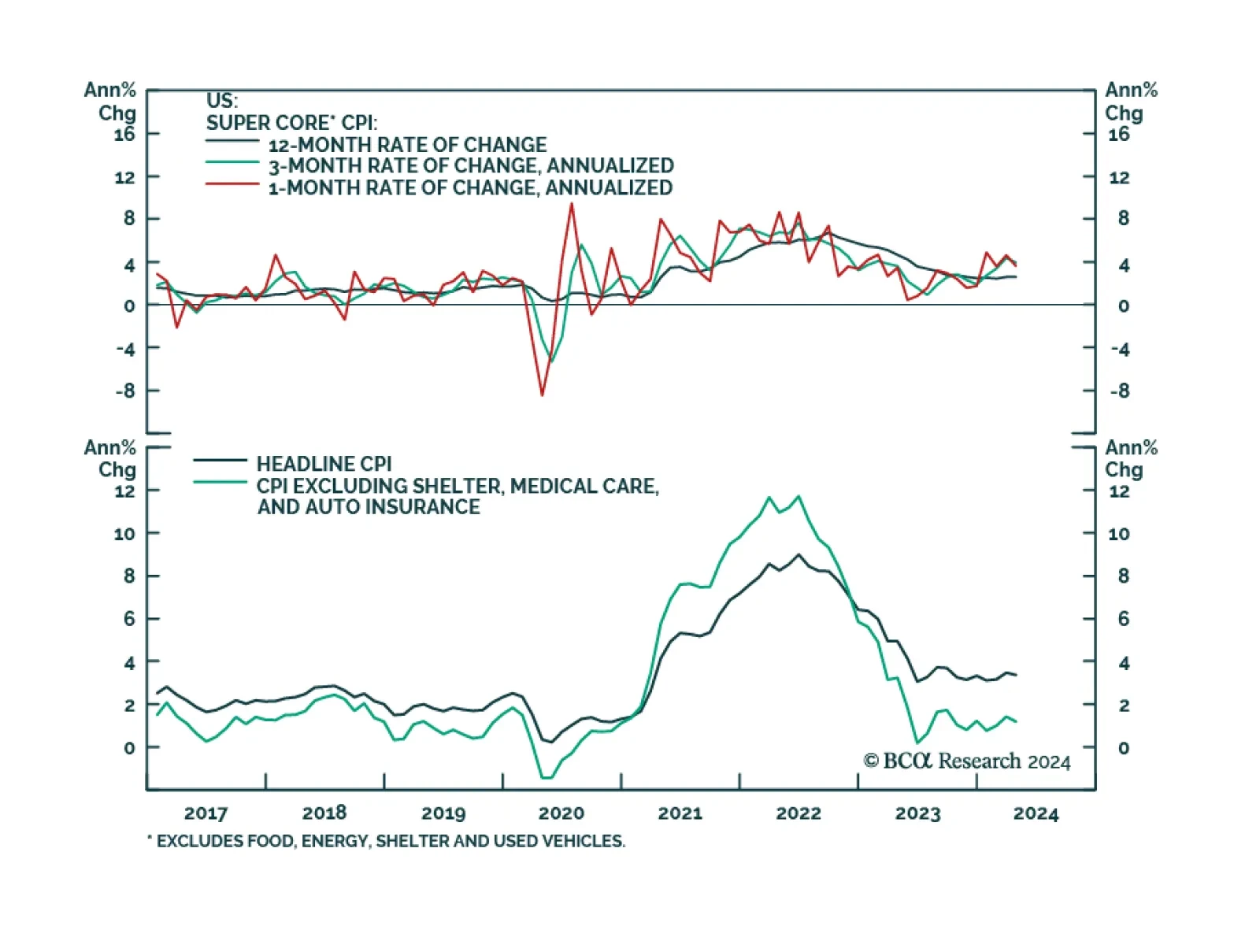

US headline CPI inflation decelerated to a softer-than-expected 0.3% m/m (3.4% y/y) in April, from 0.4% m/m (3.5% y/y). Core CPI eased from 0.4% m/m (3.5% y/y) to 0.3% m/m (3.4% y/y). Declines in new (-0.4% m/m) and used vehicles (-1.4% m/m) prices largely…

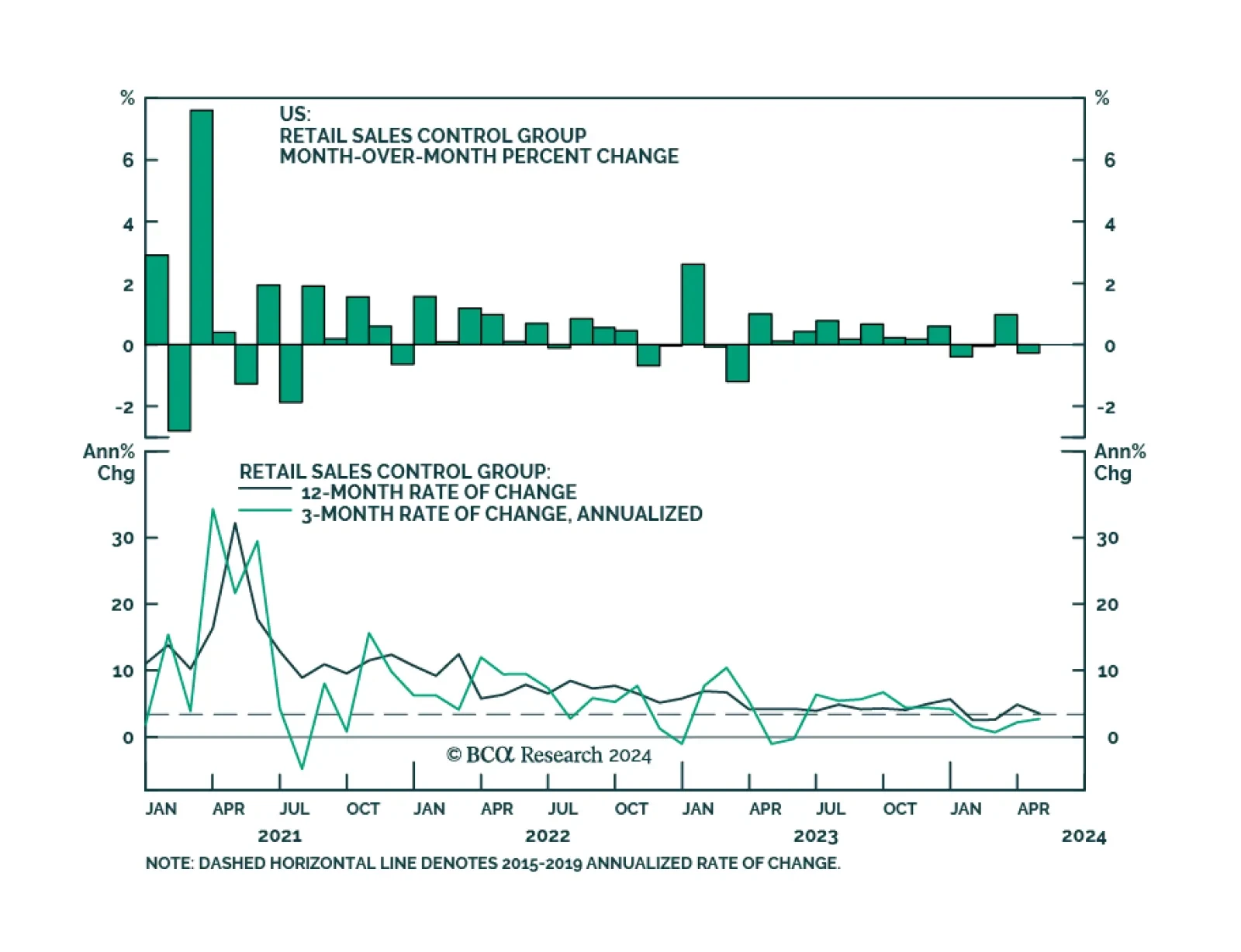

US retail sales remained unchanged in April, a downside surprise from expectations of 0.4% m/m growth. Notably, the retail sales control group (an input to GDP) declined by 0.3% m/m despite expectations of mild growth and all of the March figures were revised…

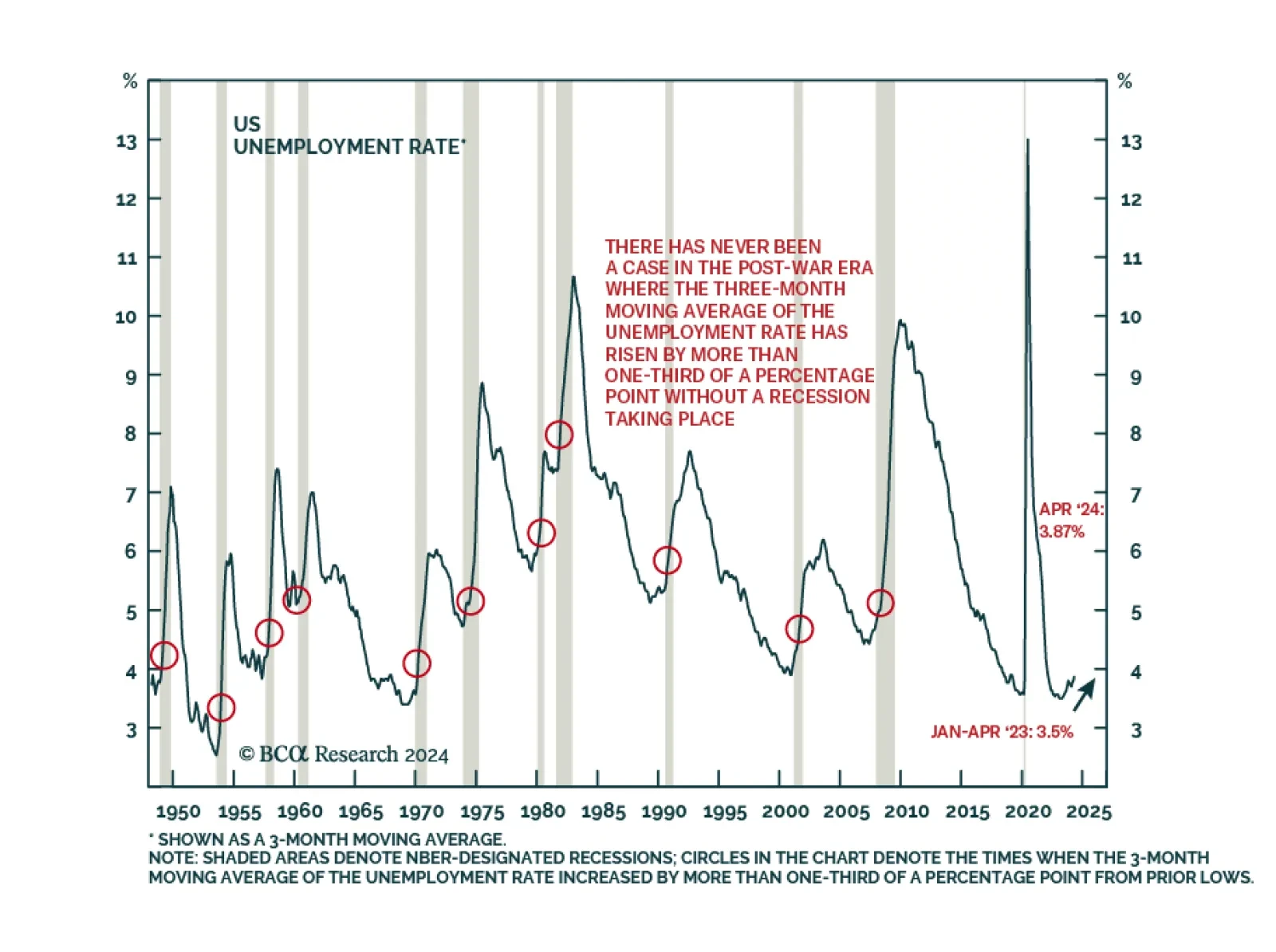

The 3-month moving average of the unemployment rate has been a reliable US recession indicator. Indeed, there has never been a case in the post-war era when it has increased by more than a third of a percentage point from its cycle low without a recession…