United States

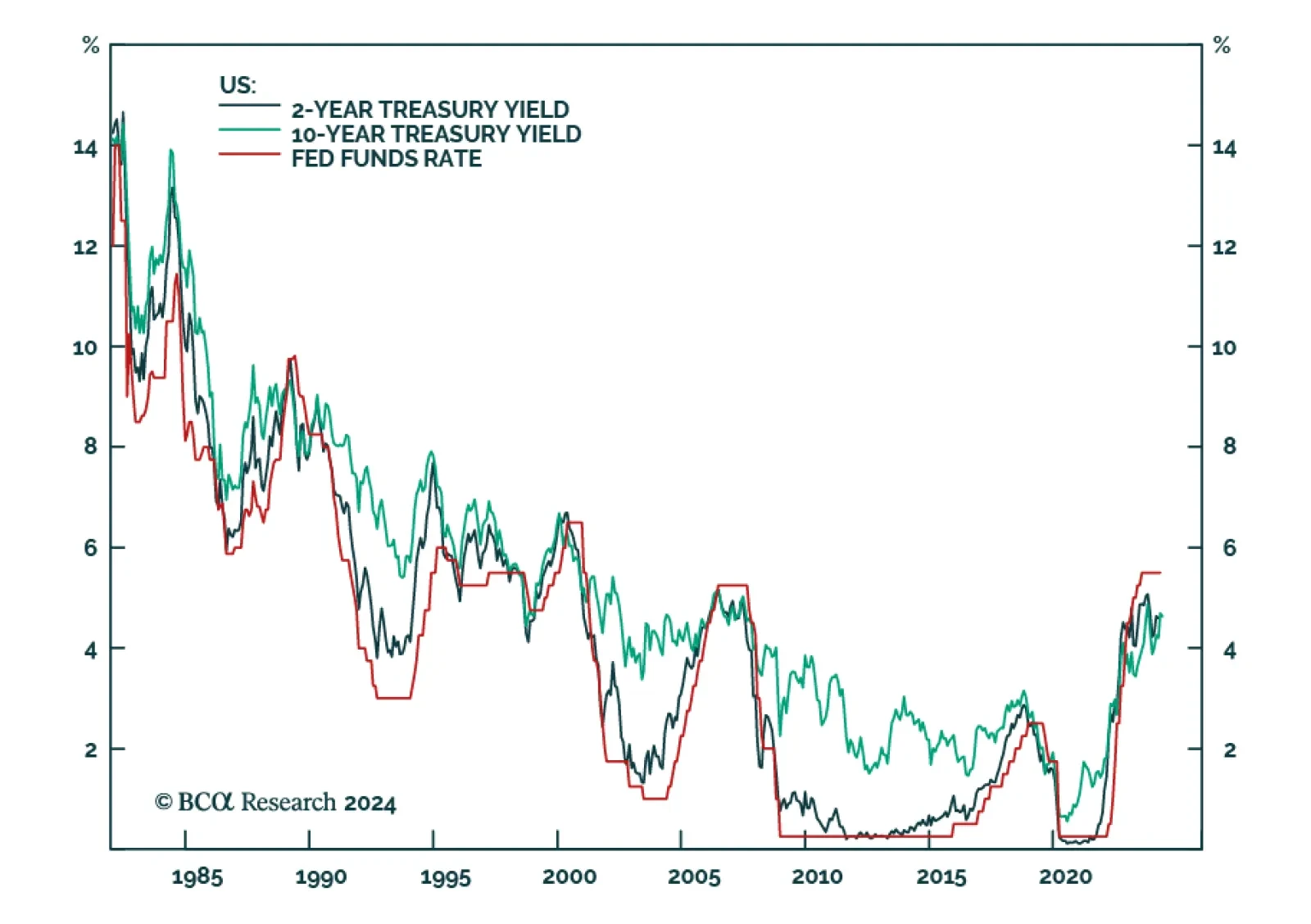

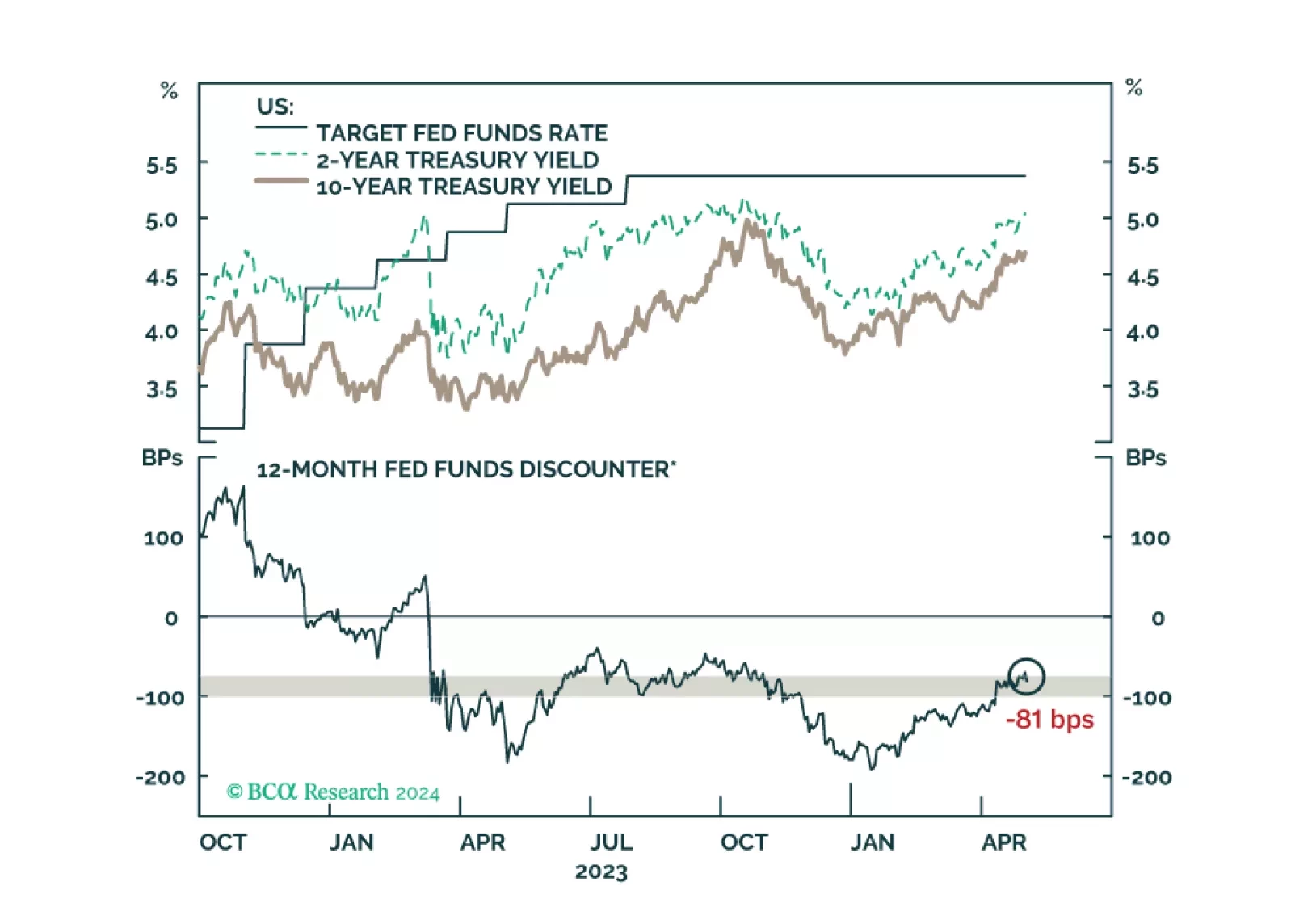

The Fed left the policy rate unchanged following its May FOMC meeting. It also announced it would slow the pace of quantitative tightening starting on June 1, from the current $60 billion per month to $25 billion per month for Treasuries redemptions, while…

Updated views on US Treasury yields and the dollar following today’s FOMC meeting.

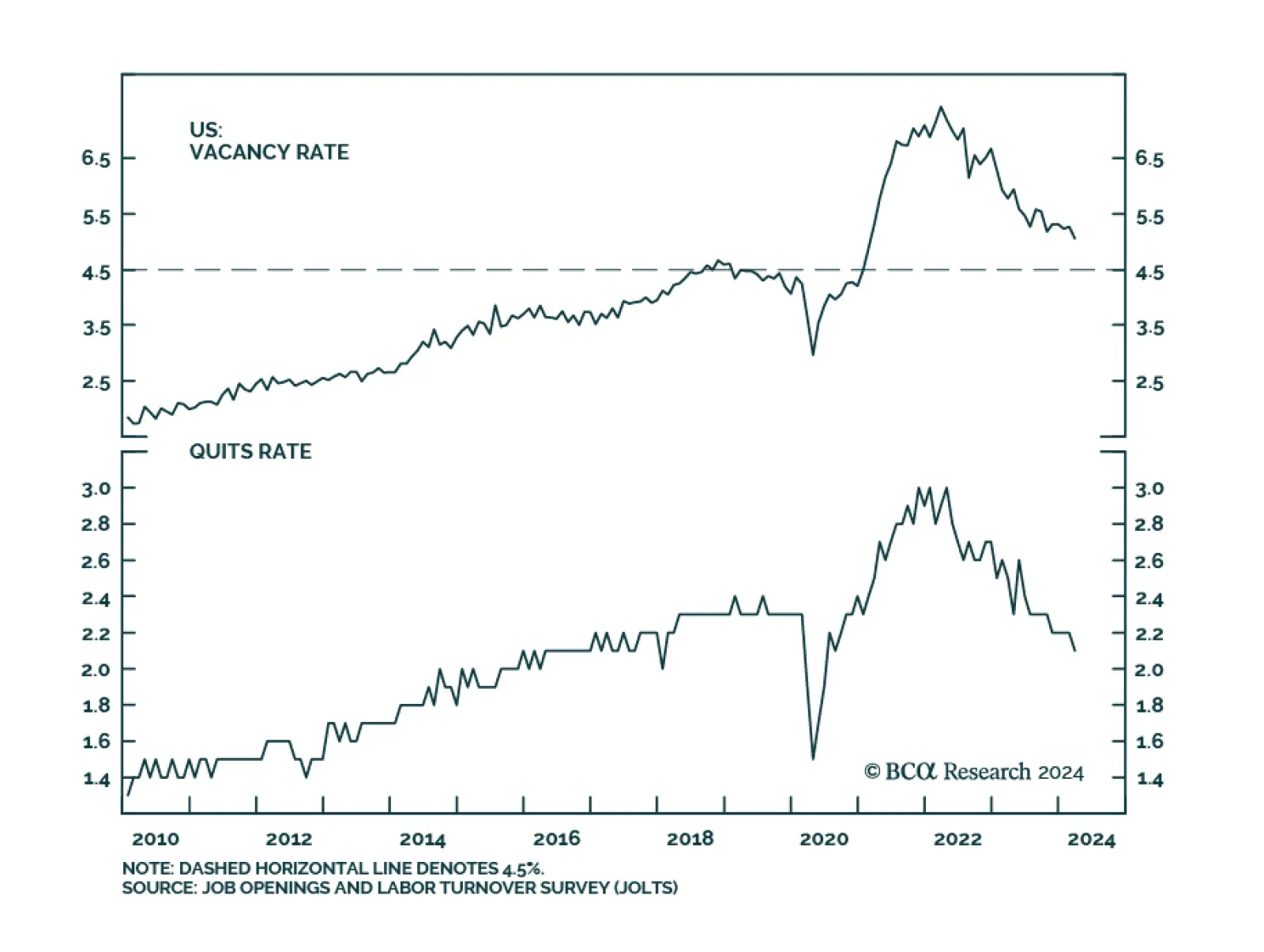

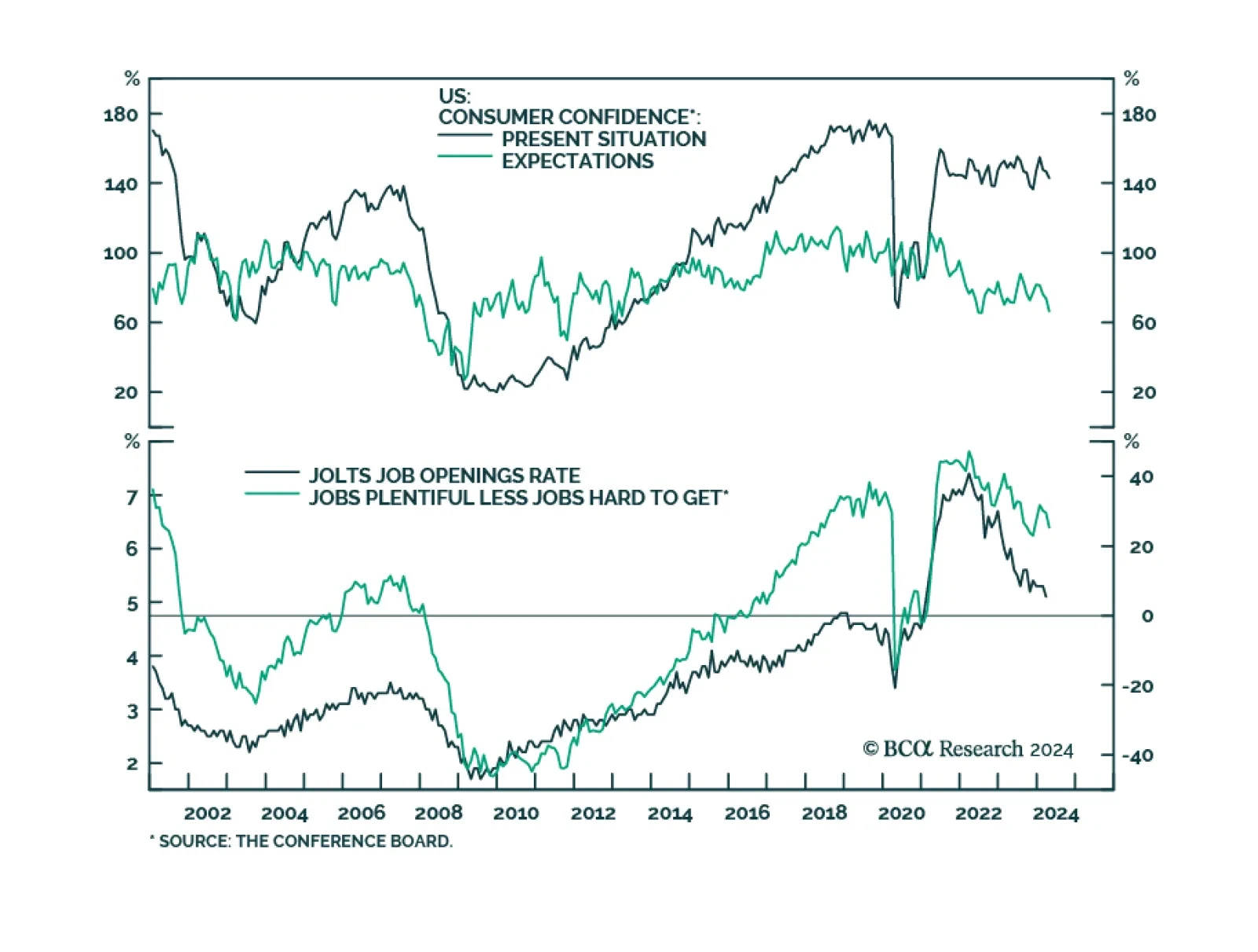

The details of the JOLTS report showed a labor market that continued to cool in March. The number of US job openings decreased to 8.488 million in March, from 8.813 million in February, and below expectations of 8.680 million. Workers seemed to be less…

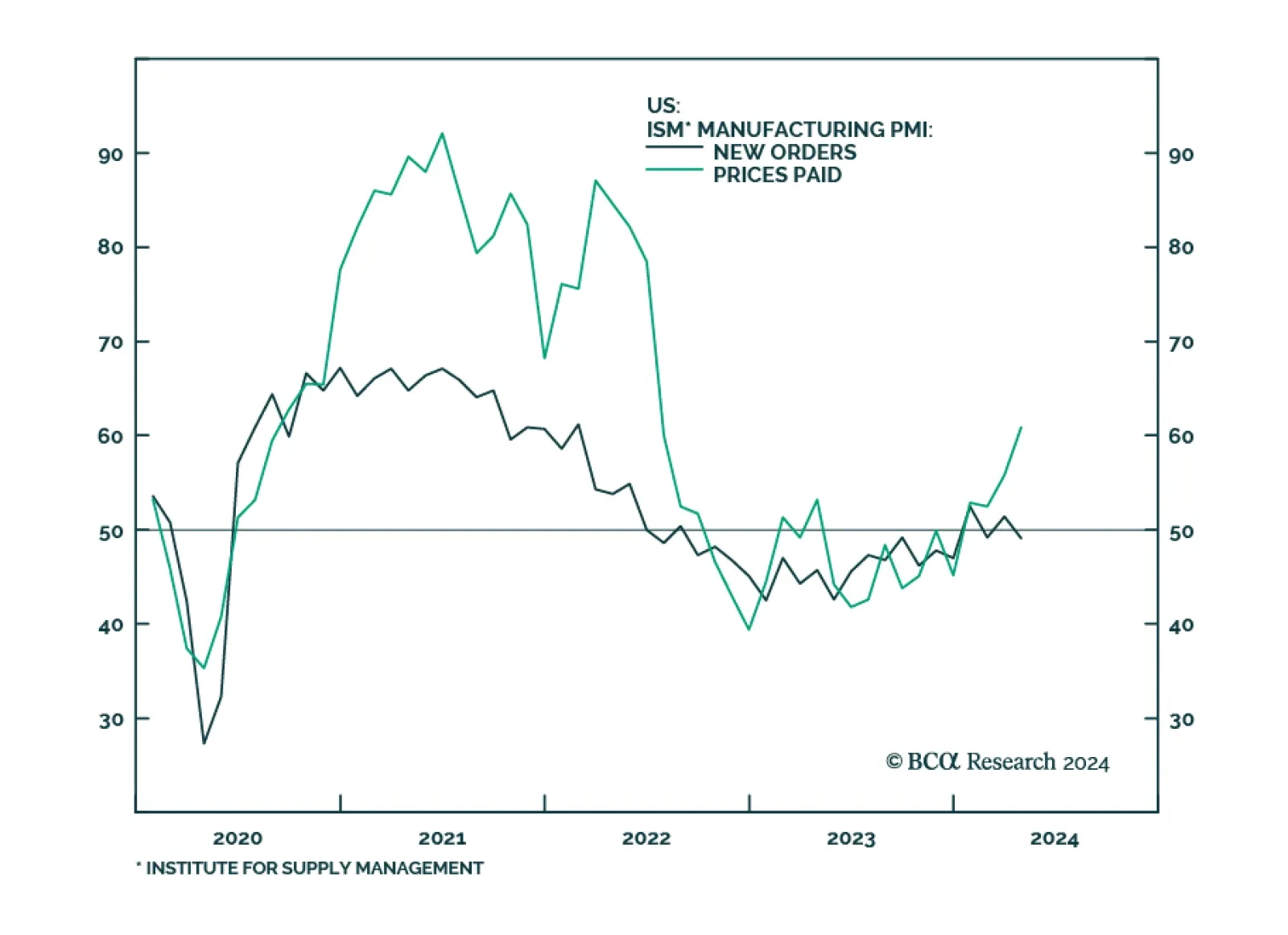

After briefly breaking a 16-month contraction streak, the ISM Manufacturing PMI dipped back below the 50.0 boom-bust line in April. It decreased from 50.3 to 49.2, disappointing expectations of 50.0. Notably, measures of domestic and foreign demand both…

The Conference Board’s gauge of consumer confidence largely disappointed in April. 3.9- and 7.6-point decreases in the Present Situation and Expectations subcomponents, respectively, drove the overall index to a 22-month low of 97.0 in April. This third…

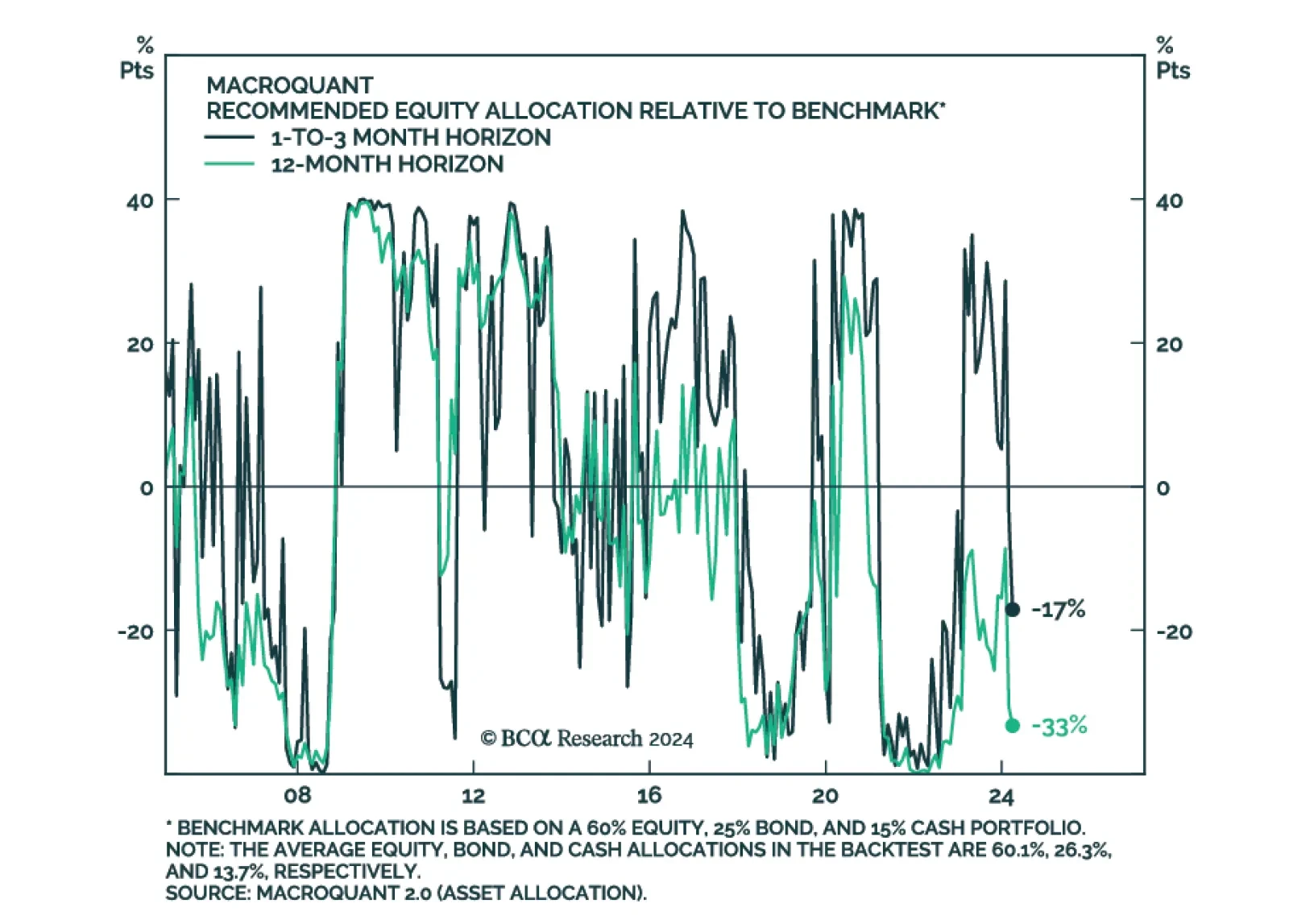

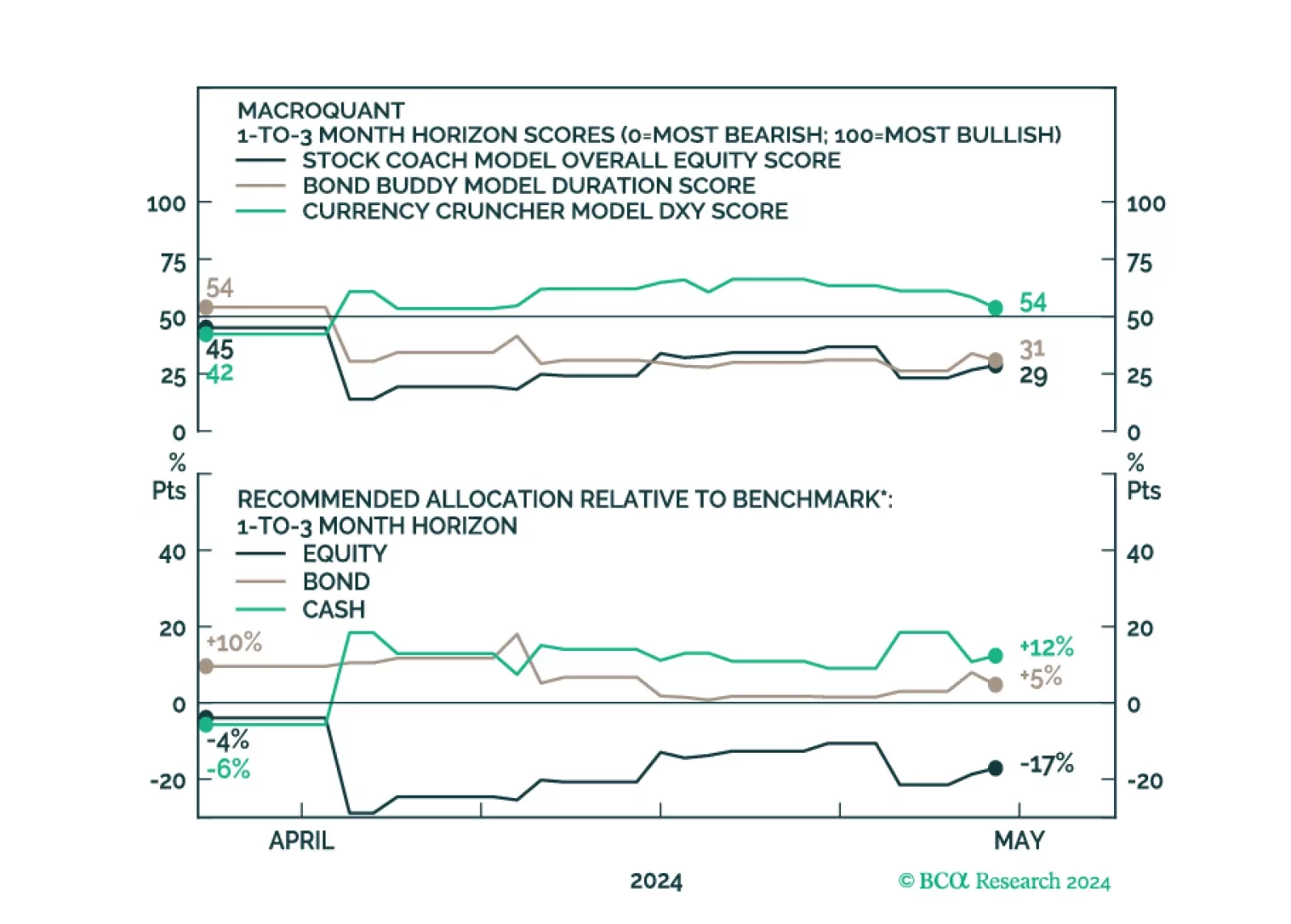

In its latest report, BCA Research’s Global Investment Strategy service provides an update on its MacroQuant model. The overall equity score declined in April, finishing the month at the 29th percentile, which is enough to prompt the model to assign US…

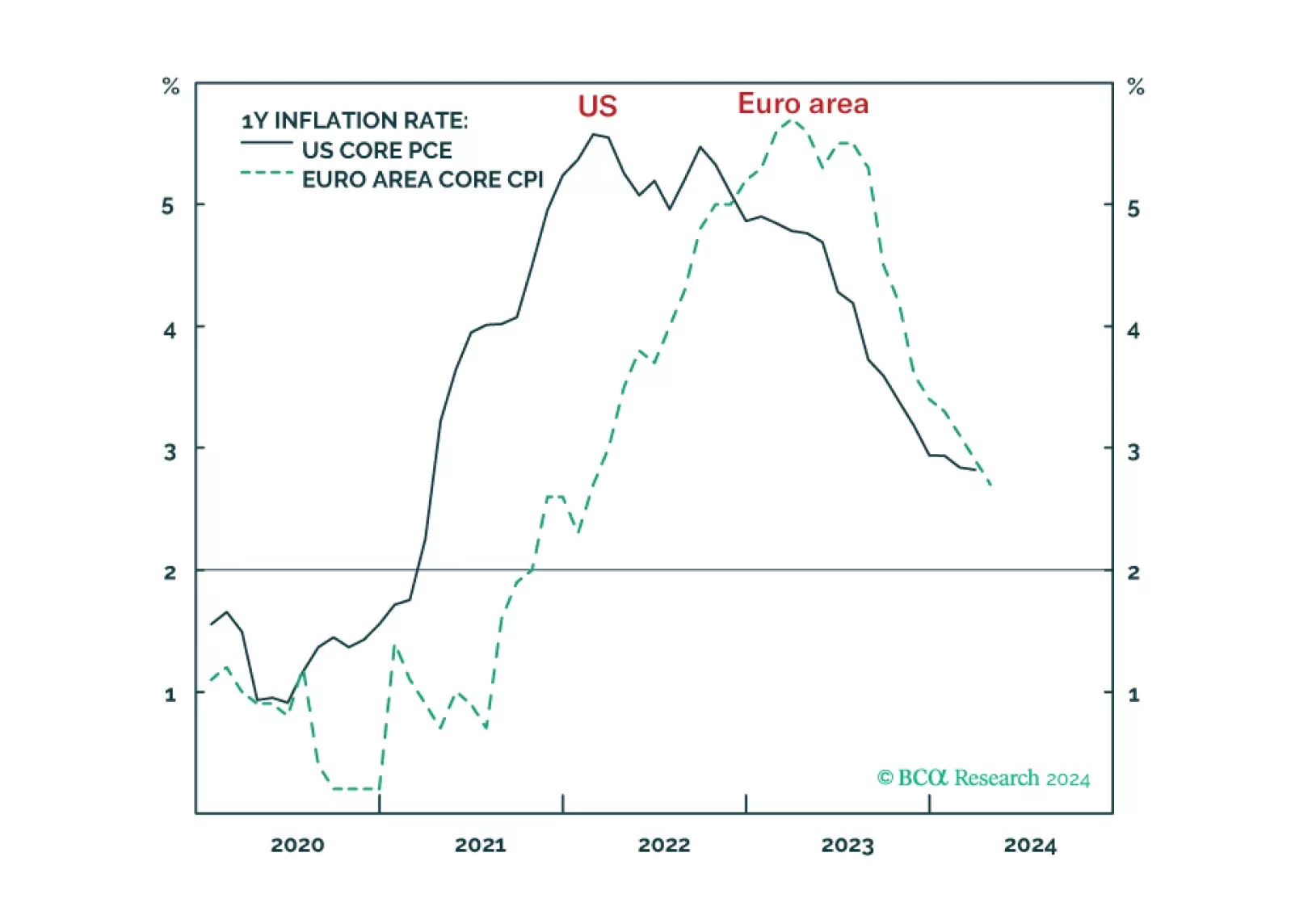

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

MacroQuant downgraded equities from neutral to underweight on a 1-to-3 month horizon. The model suggests increasing exposure to cash.

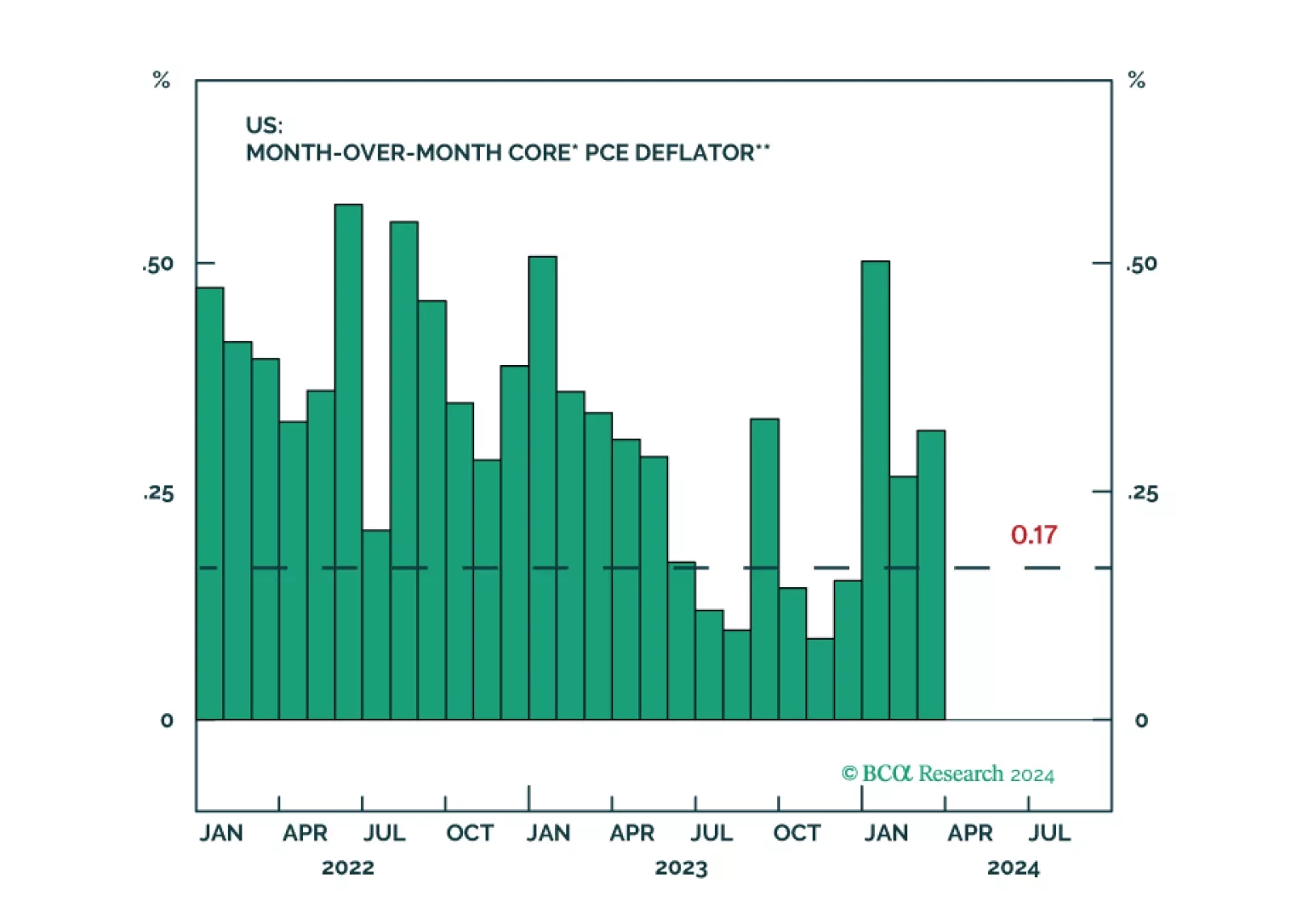

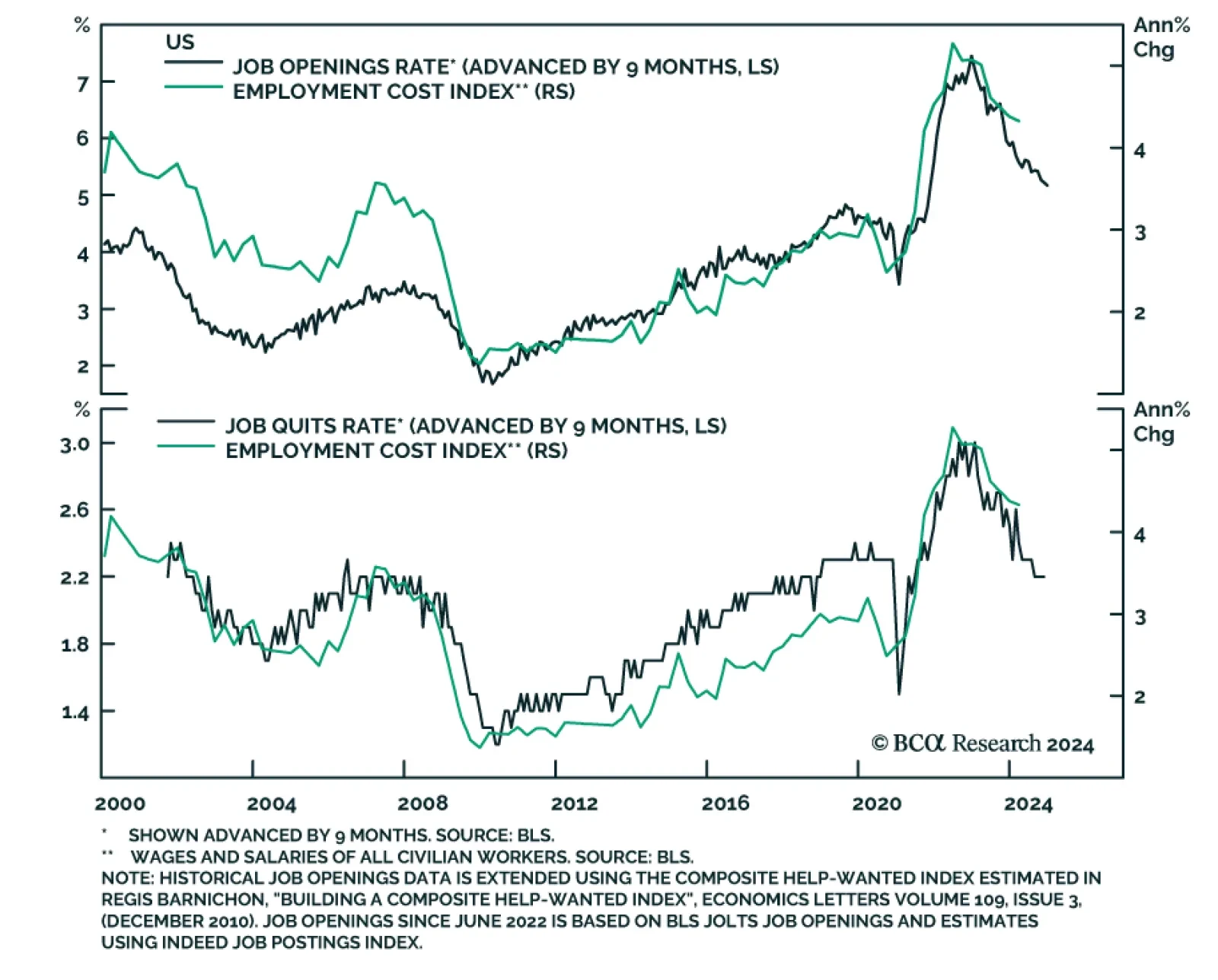

The Q1 US Employment Cost Index (ECI) accelerated at a faster-than-expected 1.2% q/q rate, from 0.9% q/q in Q4. On a year-on-year basis, it rose by 4.2% in Q1 and follows a similar annual increase in the previous quarter. The Fed is not expected to cut…