United States

Equity markets reacted negatively to the preliminary Q1 US GDP on Thursday, with the S&P 500 shedding 0.5%. Meanwhile, the 10-year Treasury yield rose 6 bps in response to the stronger-than-expected core PCE inflation print for Q1. Importantly,…

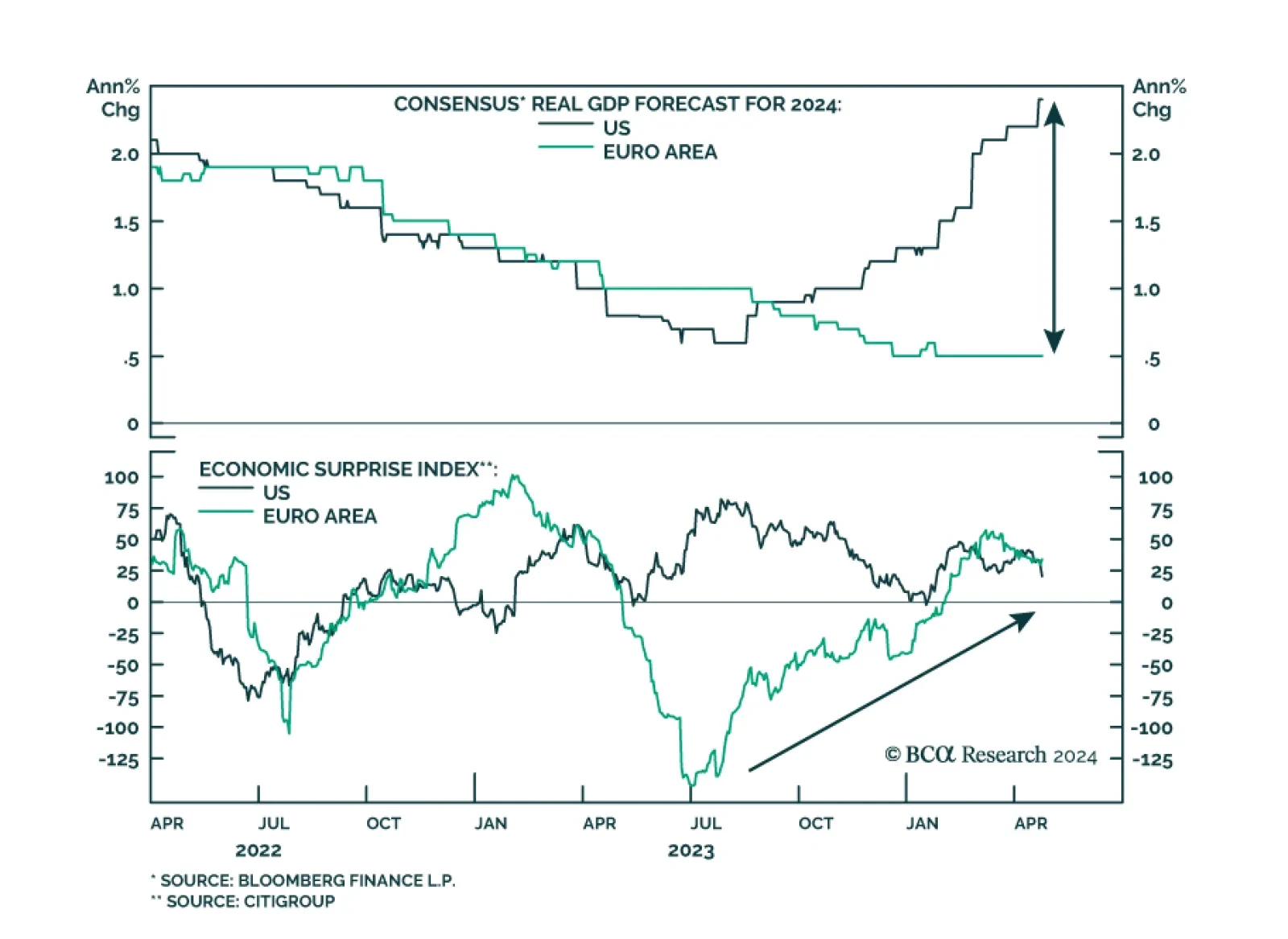

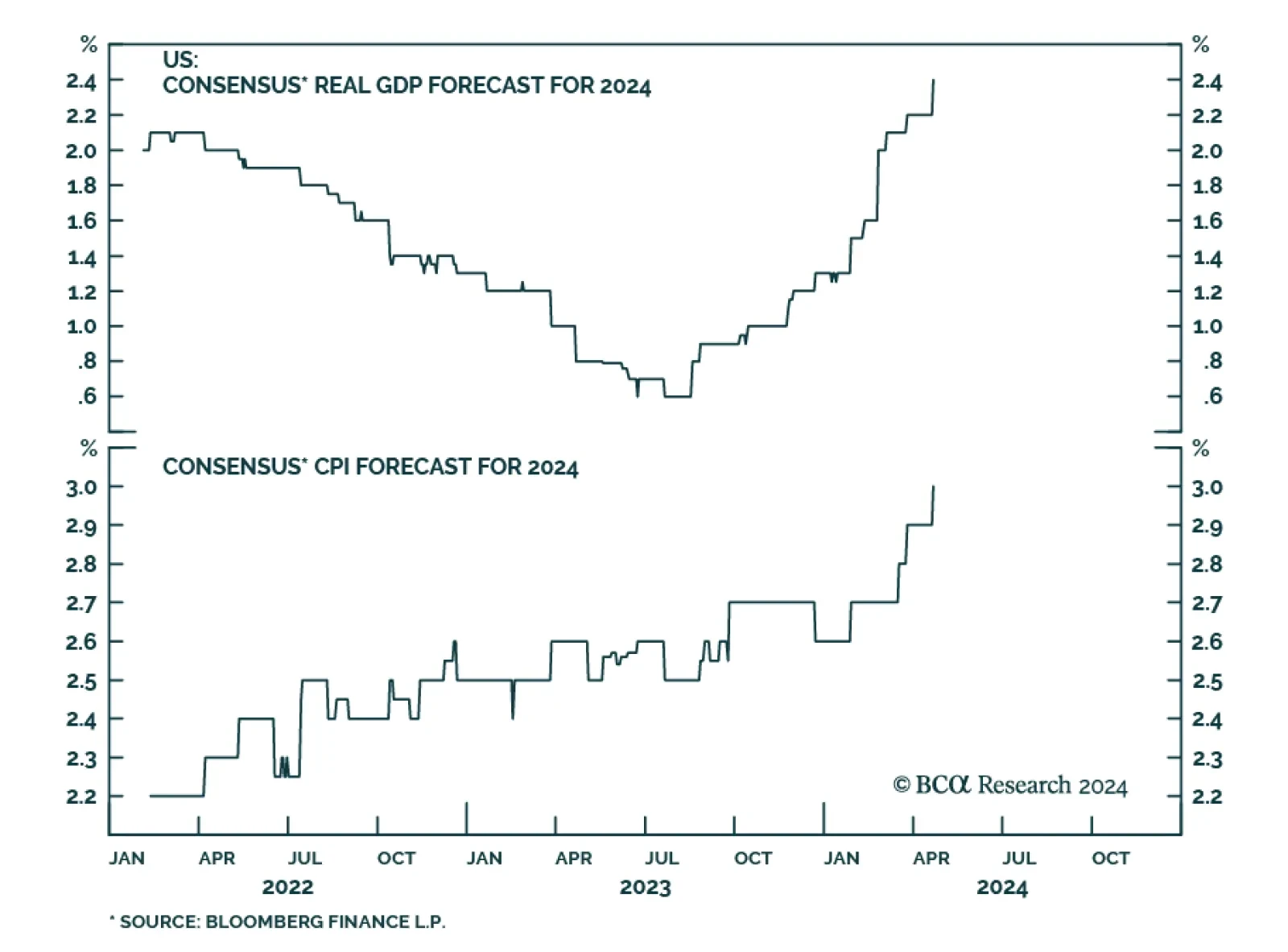

The resilience of the US economy has led economists to consistently revise up their consensus real GDP growth forecast for 2024, which now stands at 2.4%, up from 0.6% in July 2023. Conversely, the 2024 consensus Eurozone growth estimate has been trending…

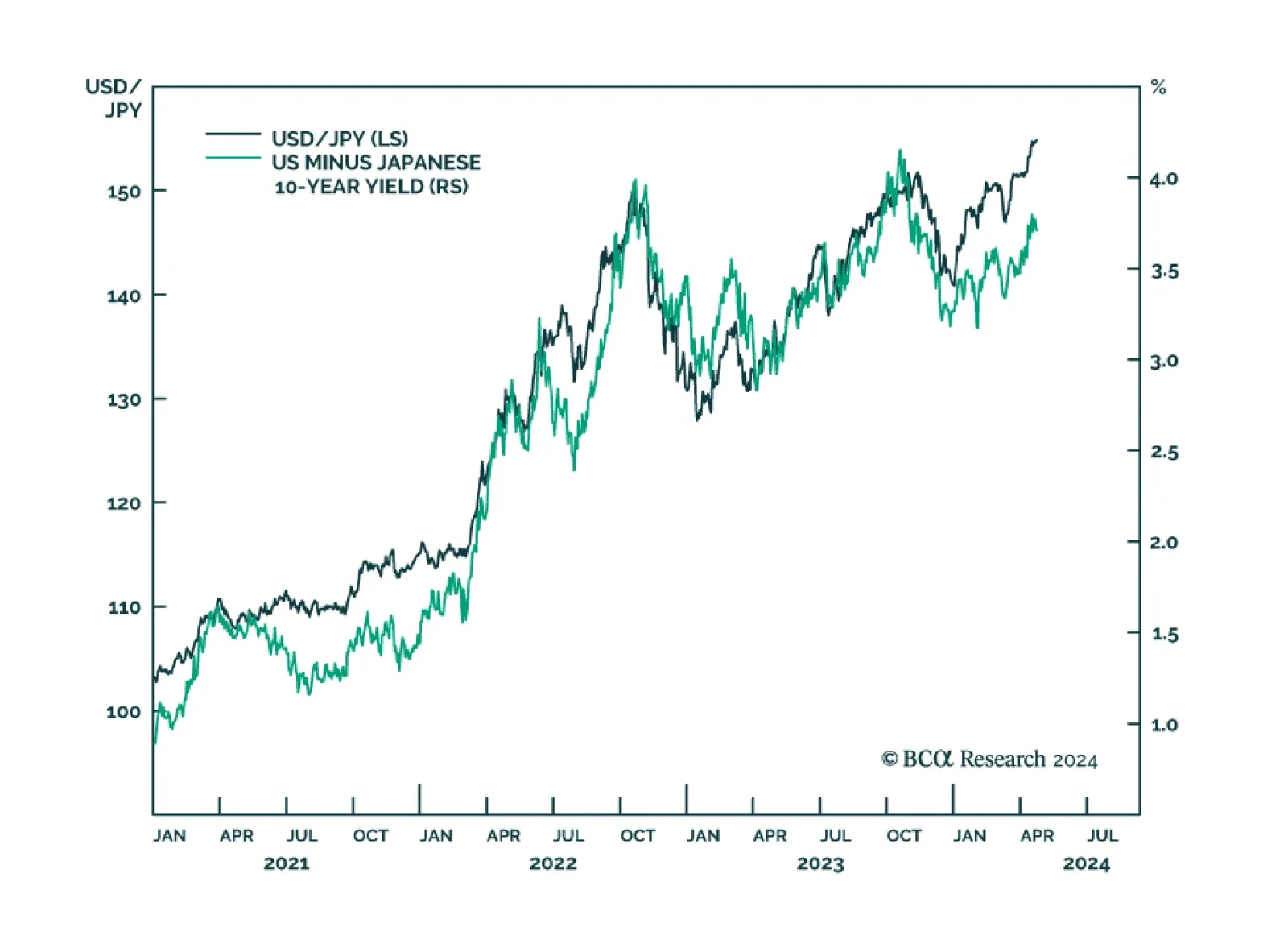

USD/JPY has appreciated by over 10% so far in 2024, making the yen the worst performing G10 currency year-to-date. This cross has also surpassed the 150 threshold which historically is the level at which the Bank of Japan begins to intervene. Today, it stands…

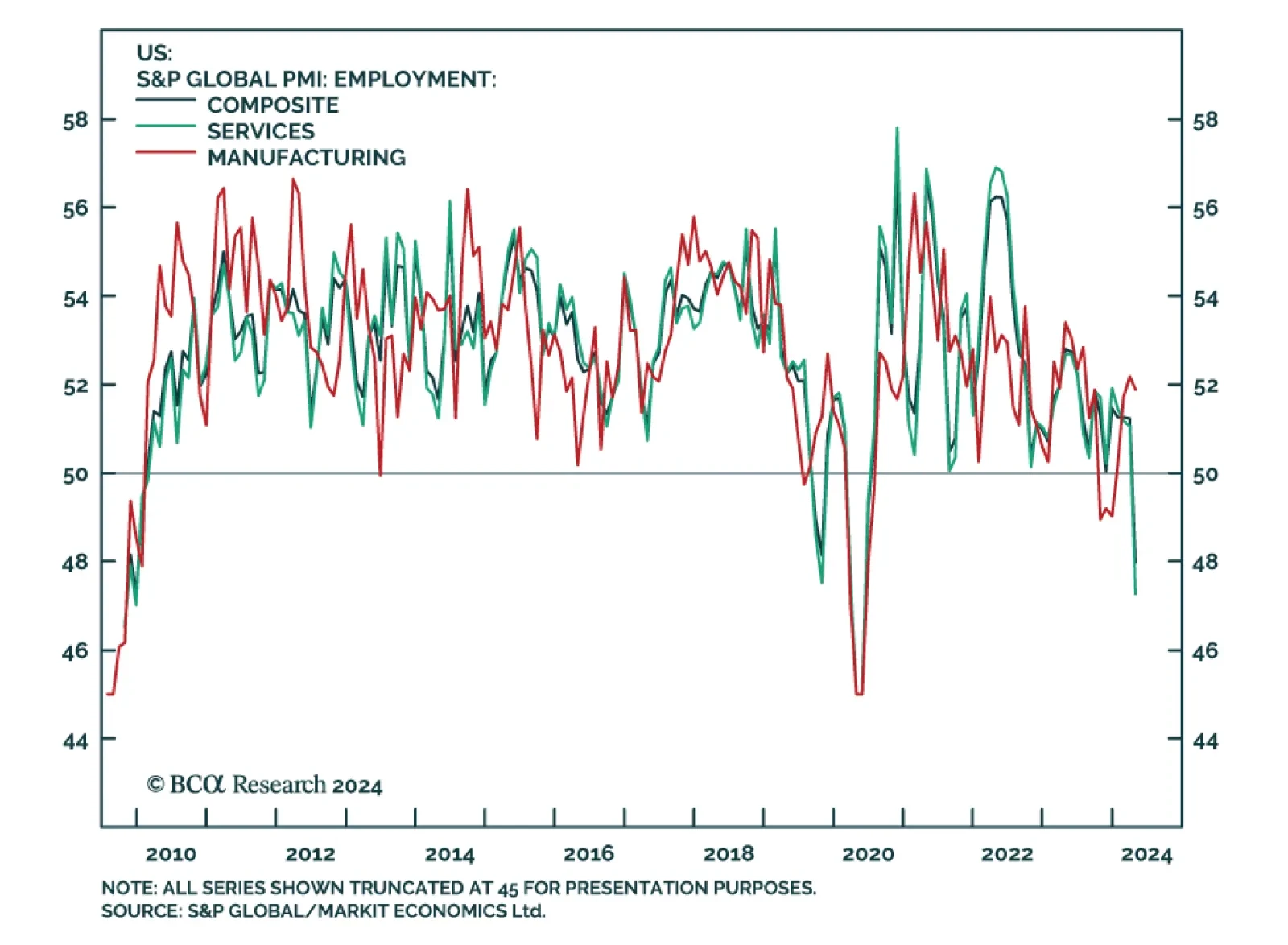

Preliminary S&P PMIs for the US showed the manufacturing index declined to contraction territory of 49.9 from 51.9, falling short of expectations of 52. The services PMI also disappointed coming in at 50.9, versus expectations it would improve from 51.7…

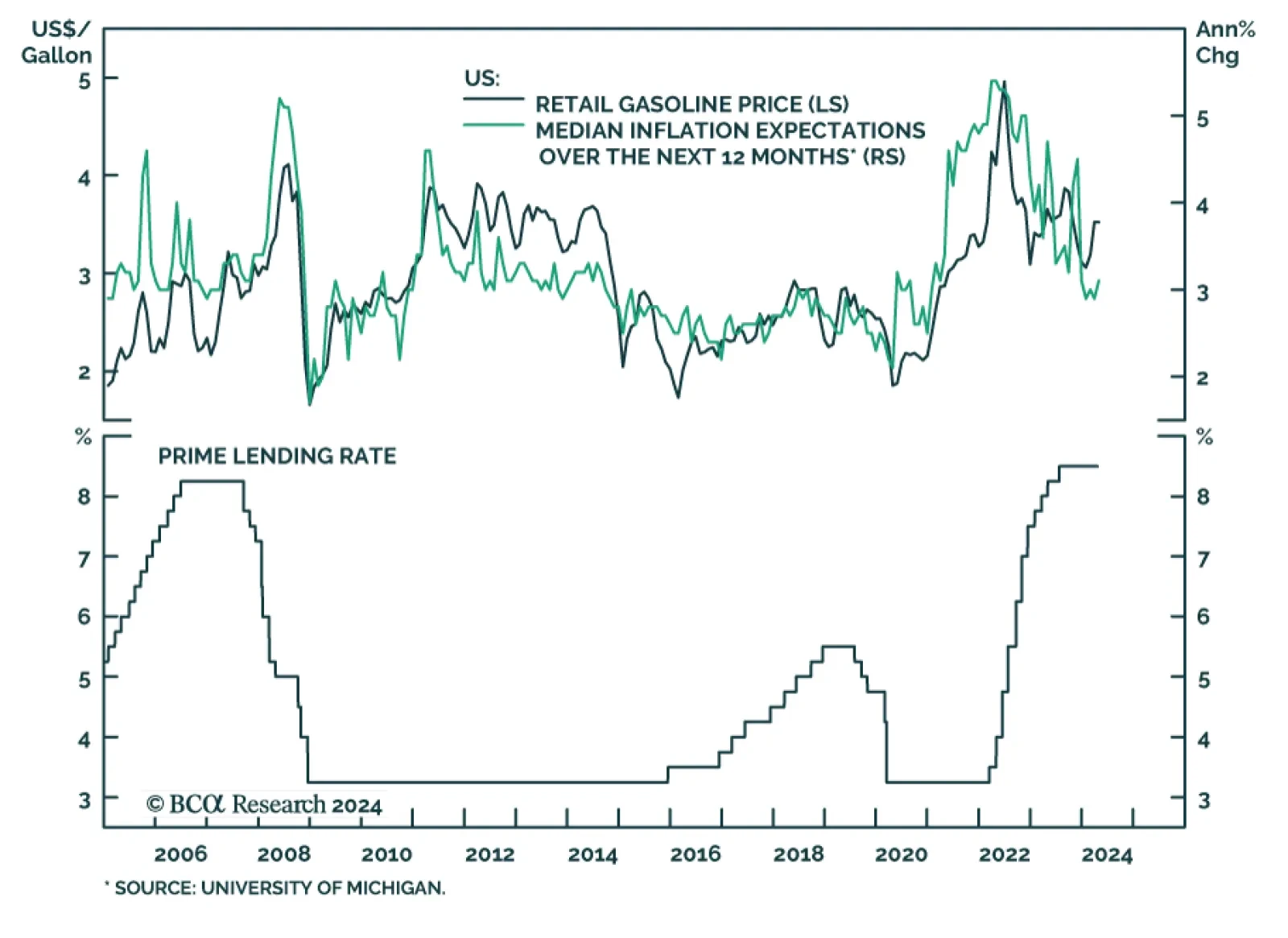

Retail gasoline prices have surged 13% since the beginning of the year, boosted by resilient global demand and geopolitical tensions. A key question for investors pertains to the ability of US consumption to sustain further gasoline price increases.…

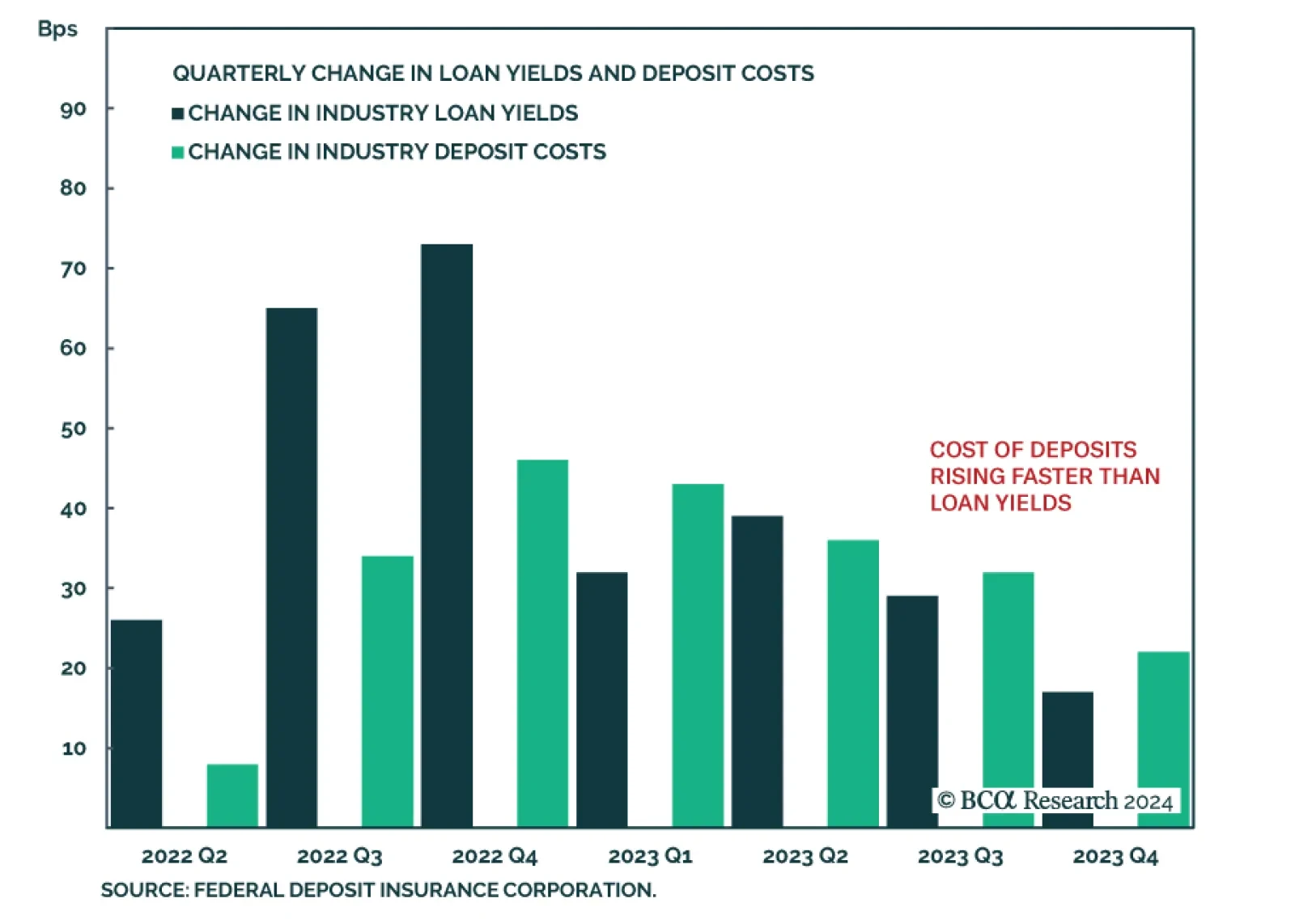

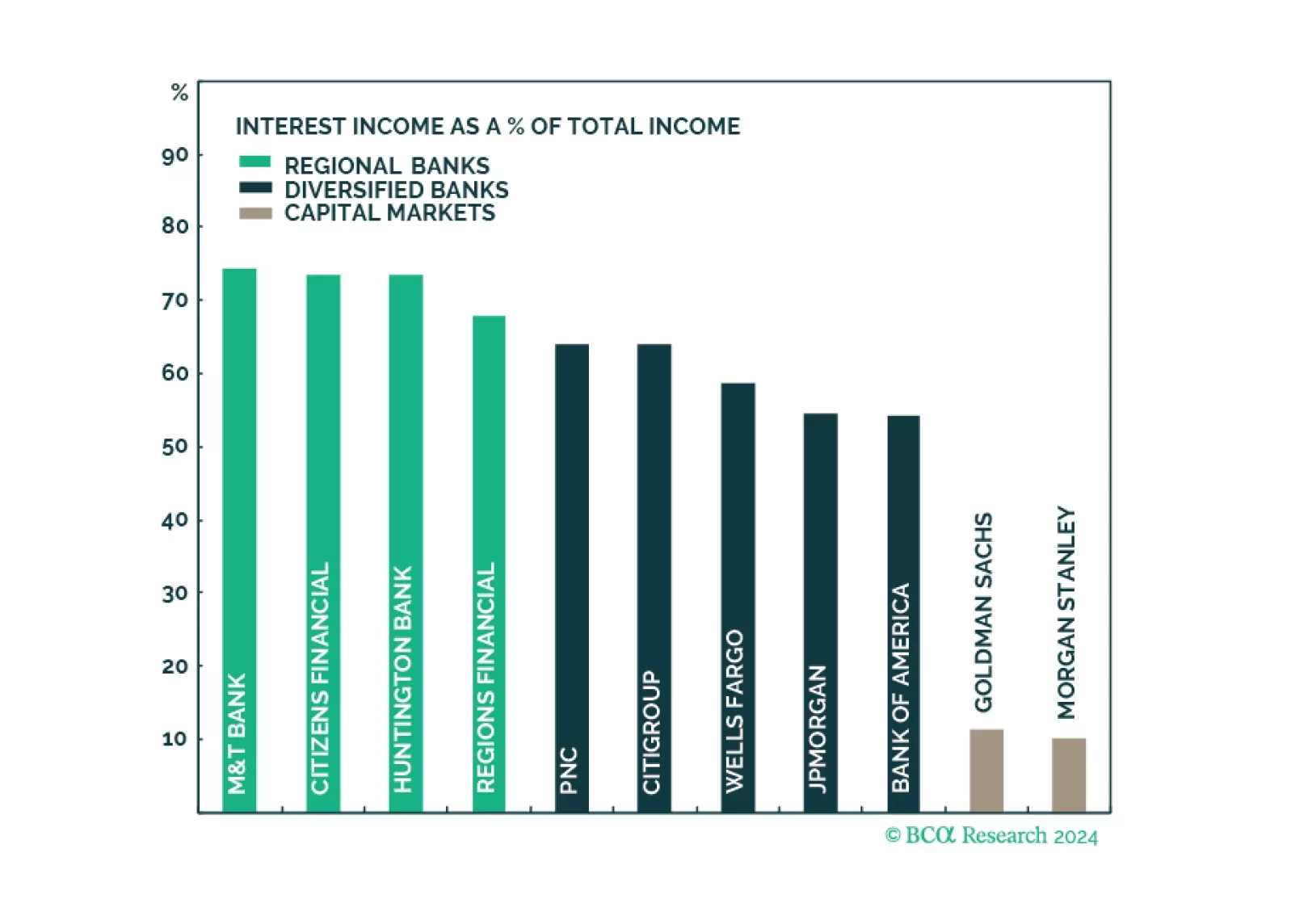

According to BCA Research’s US Equity Strategy service, Q1 earnings results signaled that net interest income (NII) growth is set to decline in US banks. For nearly two years, America’s largest banks enjoyed a surge in NII thanks to rising rates and the…

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.

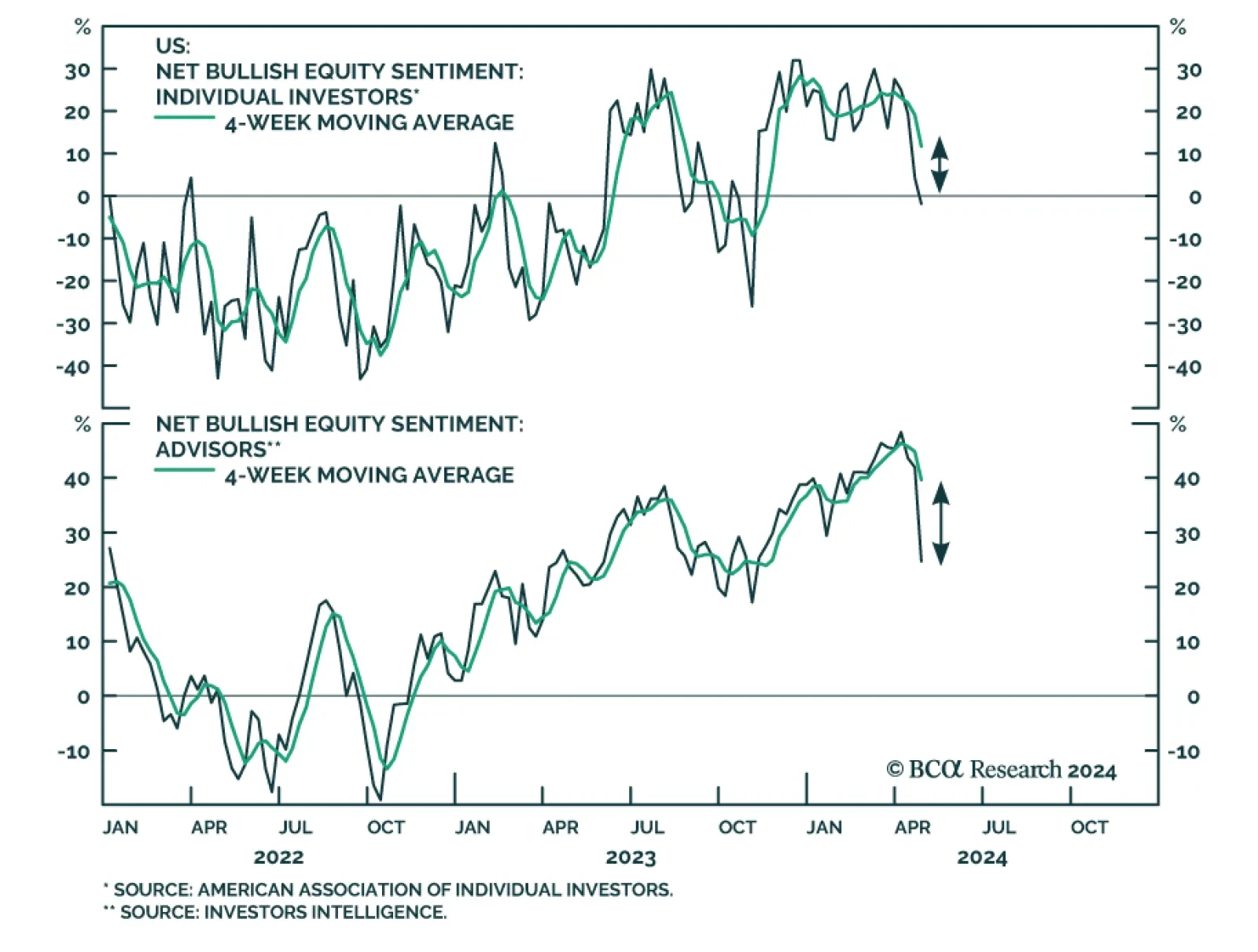

By the end of 2023, the “soft landing” scenario became the dominant narrative in financial markets. Following the regional banking scare in March of last year, market participants slowly came around to the view that the economy was entering a goldilocks…

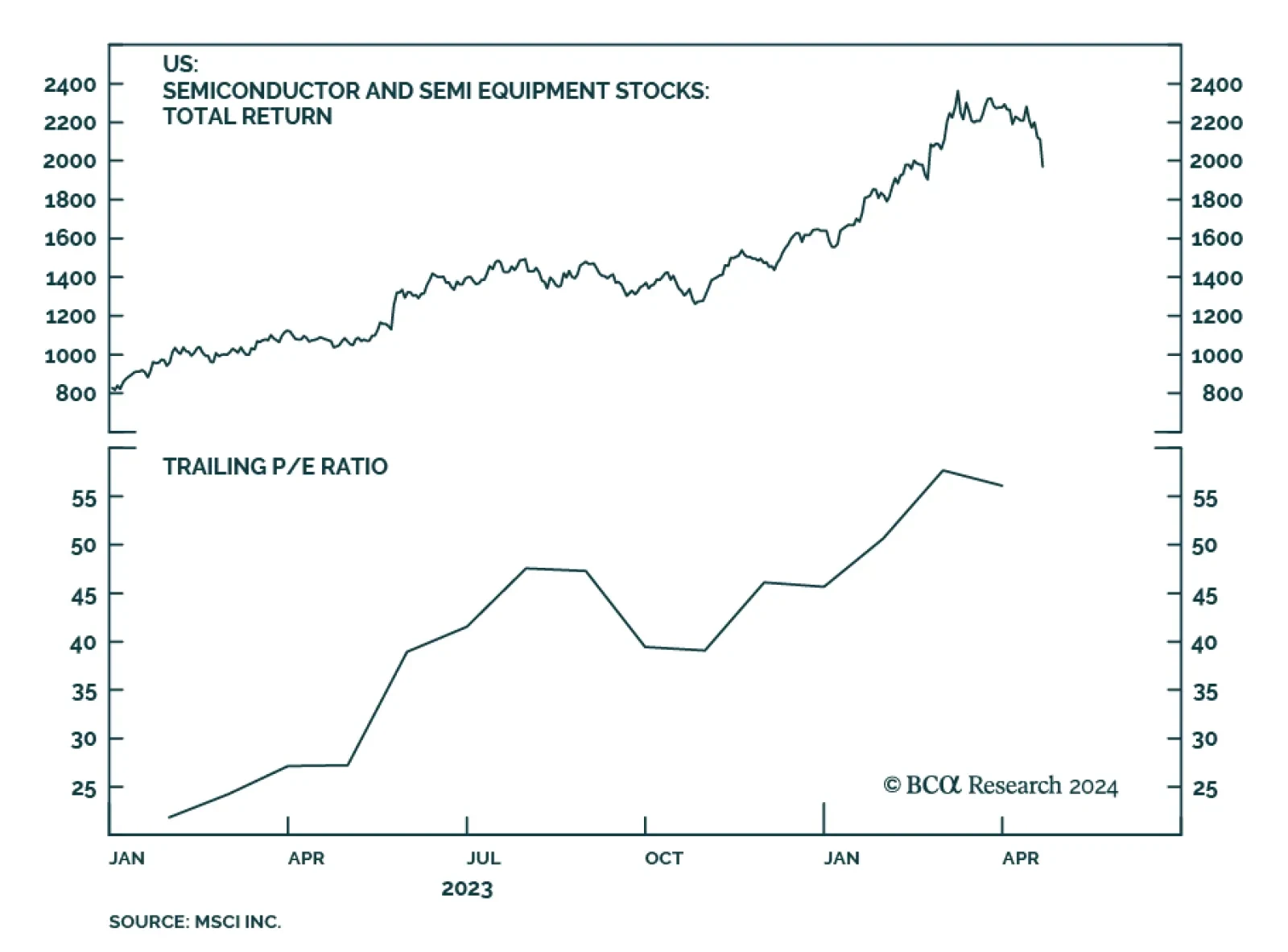

Over the last weeks, US semiconductor stocks have plunged by over 17%. In a way, this correction should be expected. Semiconductor stocks had skyrocketed this year. Even after the recent pullback, semi stocks are still up over 20%…

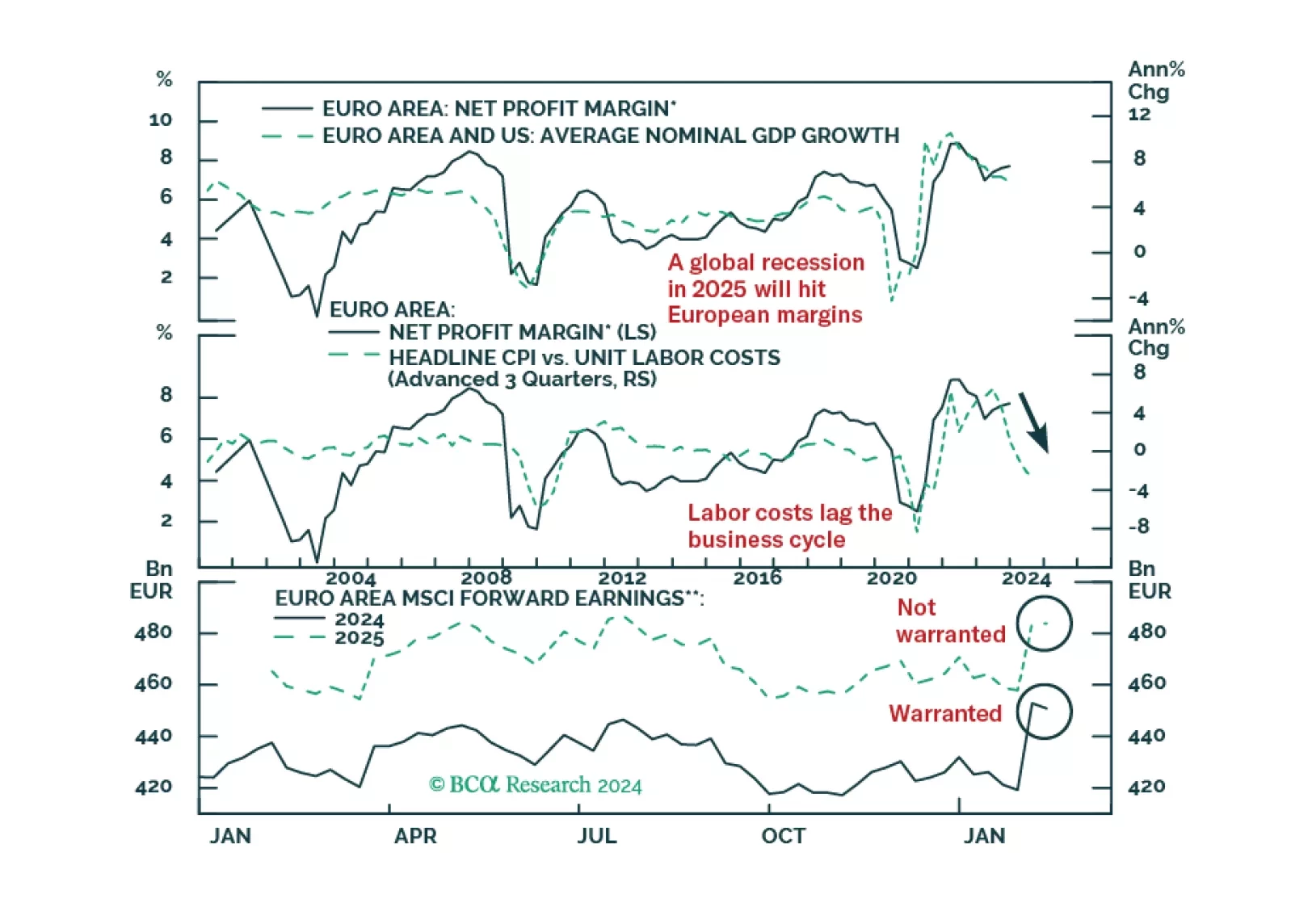

European profits margins are elevated. Will a mild recession be enough to bring them down?