United States

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.

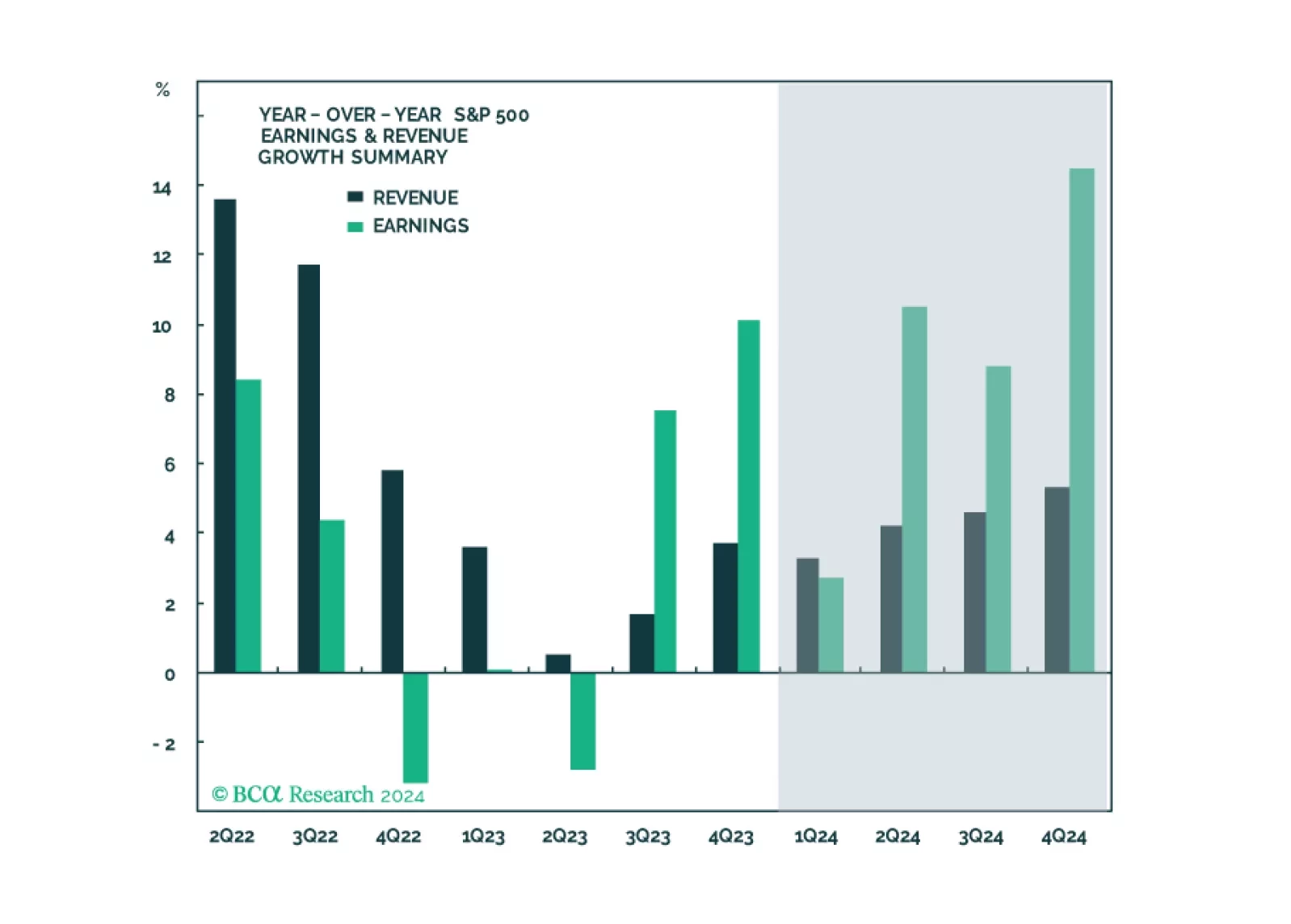

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.

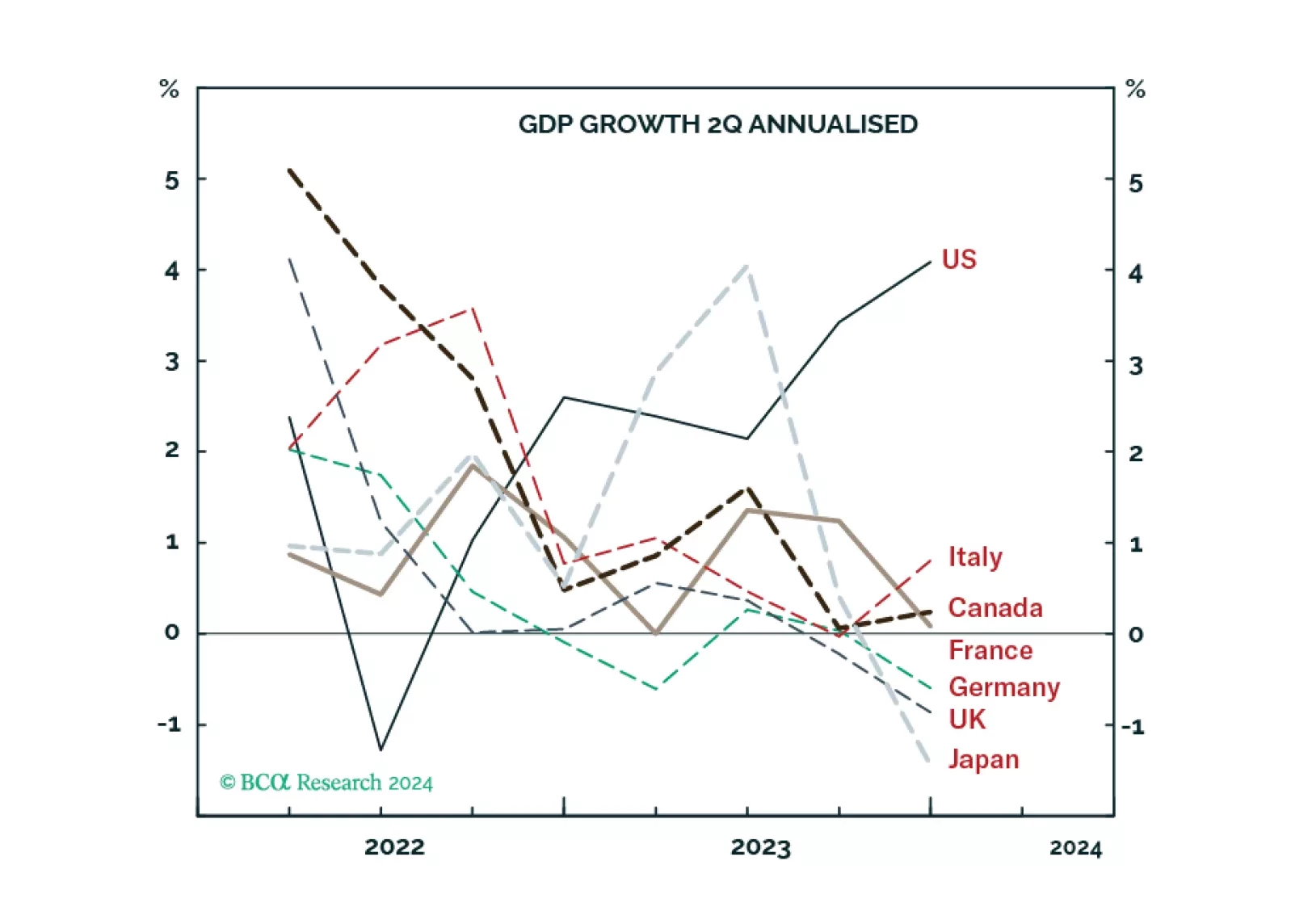

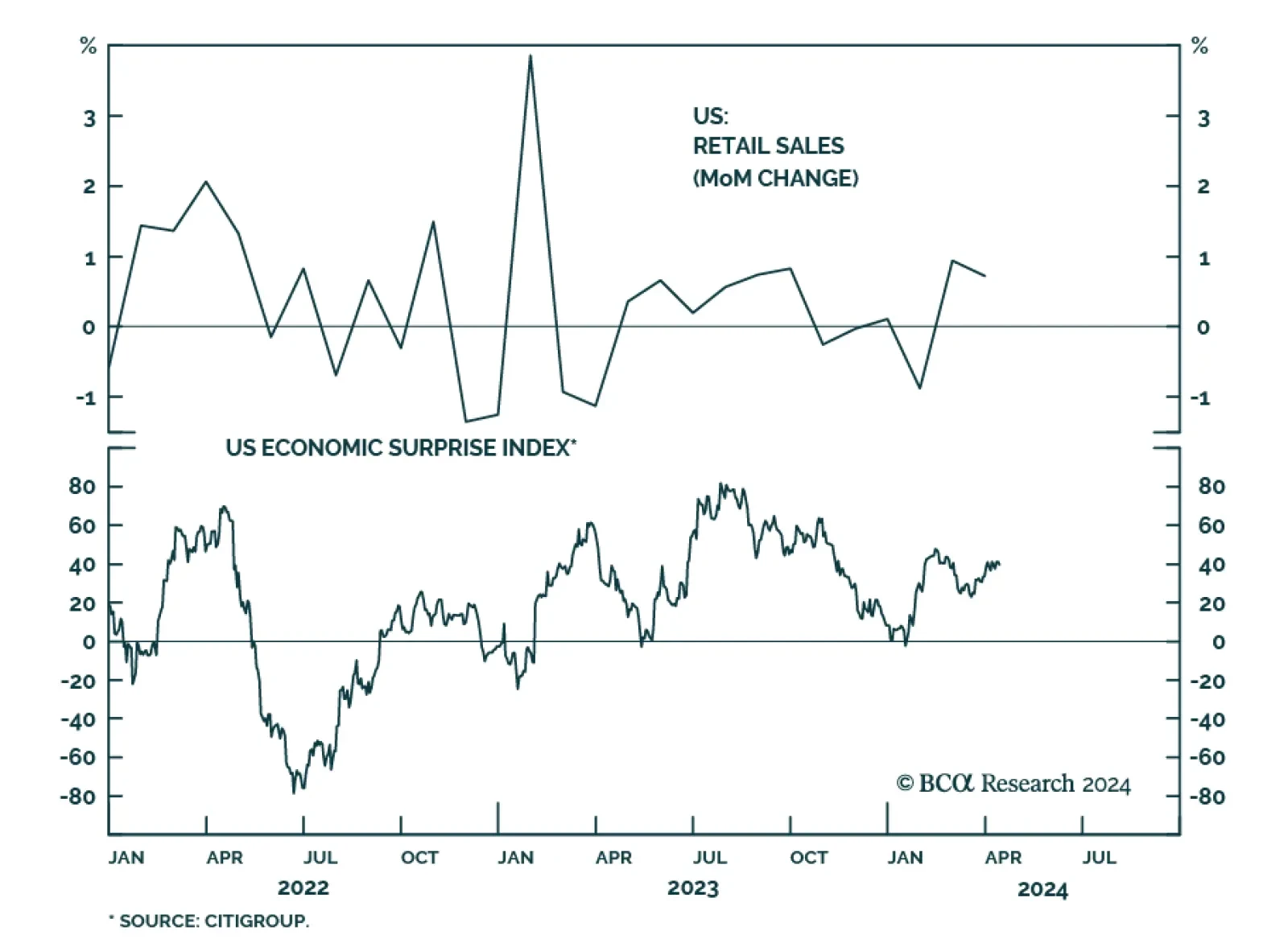

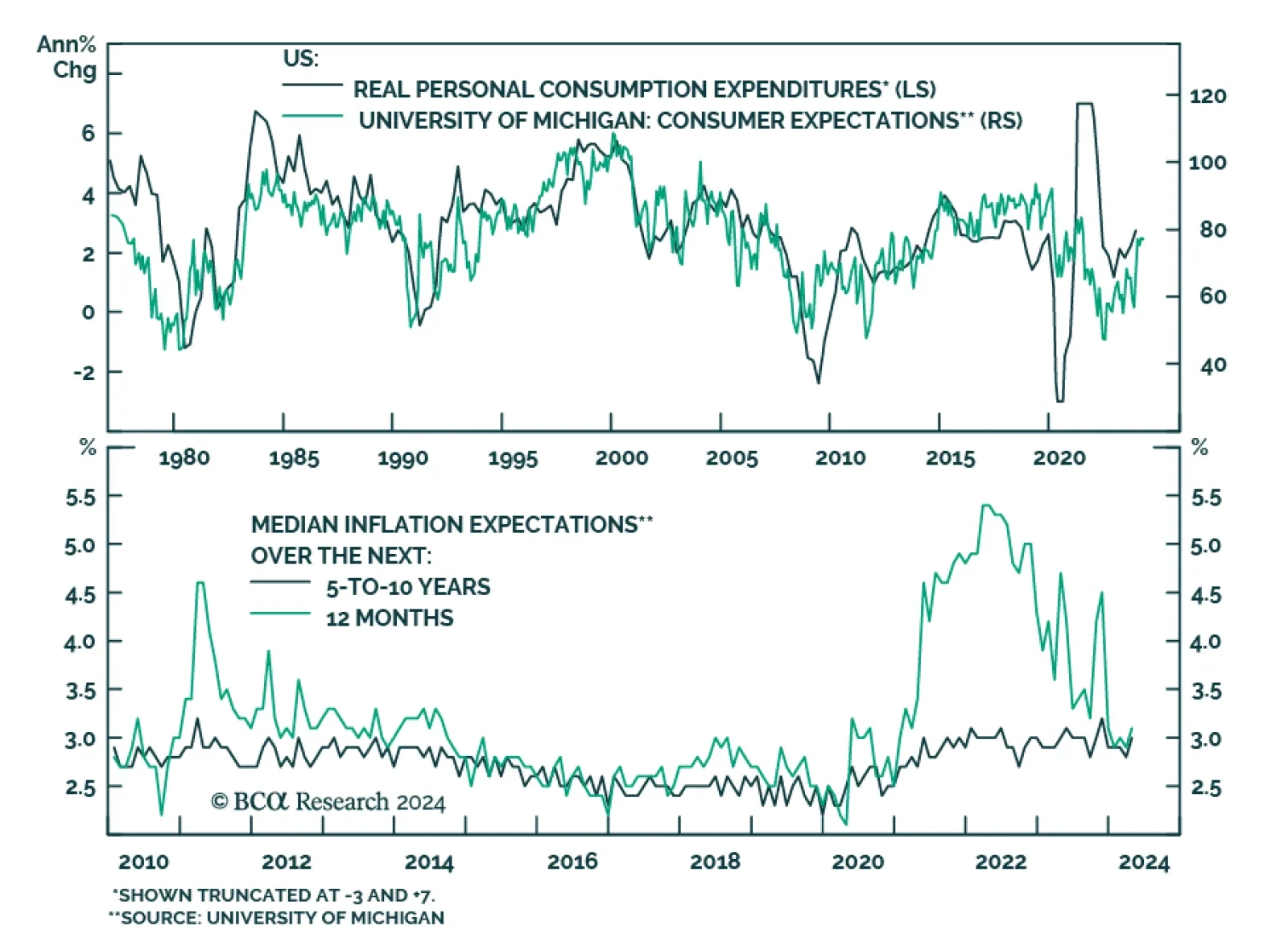

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

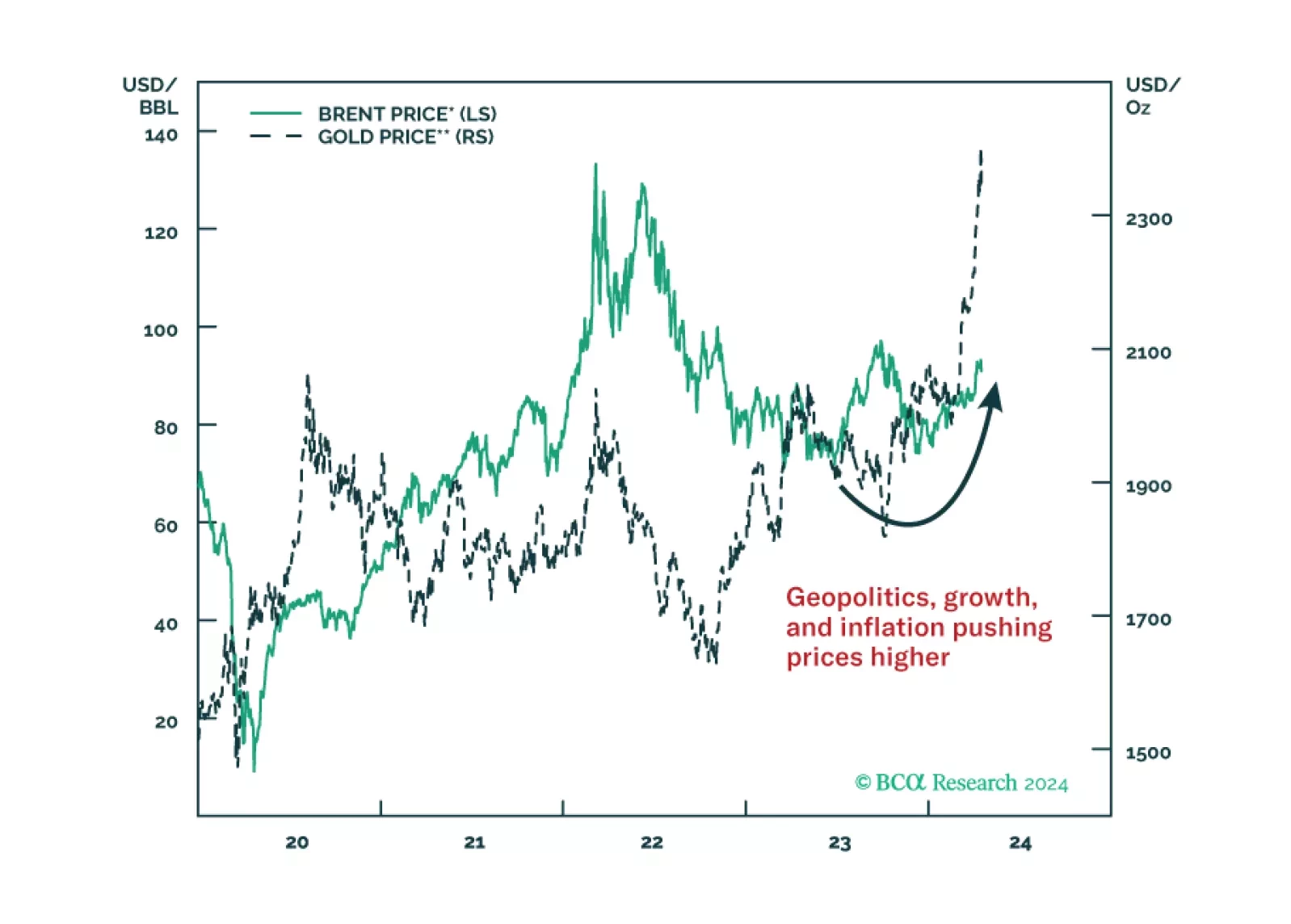

In the near term, favor oil and oil producers outside the Gulf Arab states. Over a 12-month horizon, favor US and North American equities, defensive sectors over cyclicals, and safe-assets. Within cyclicals, stick to energy and defense.

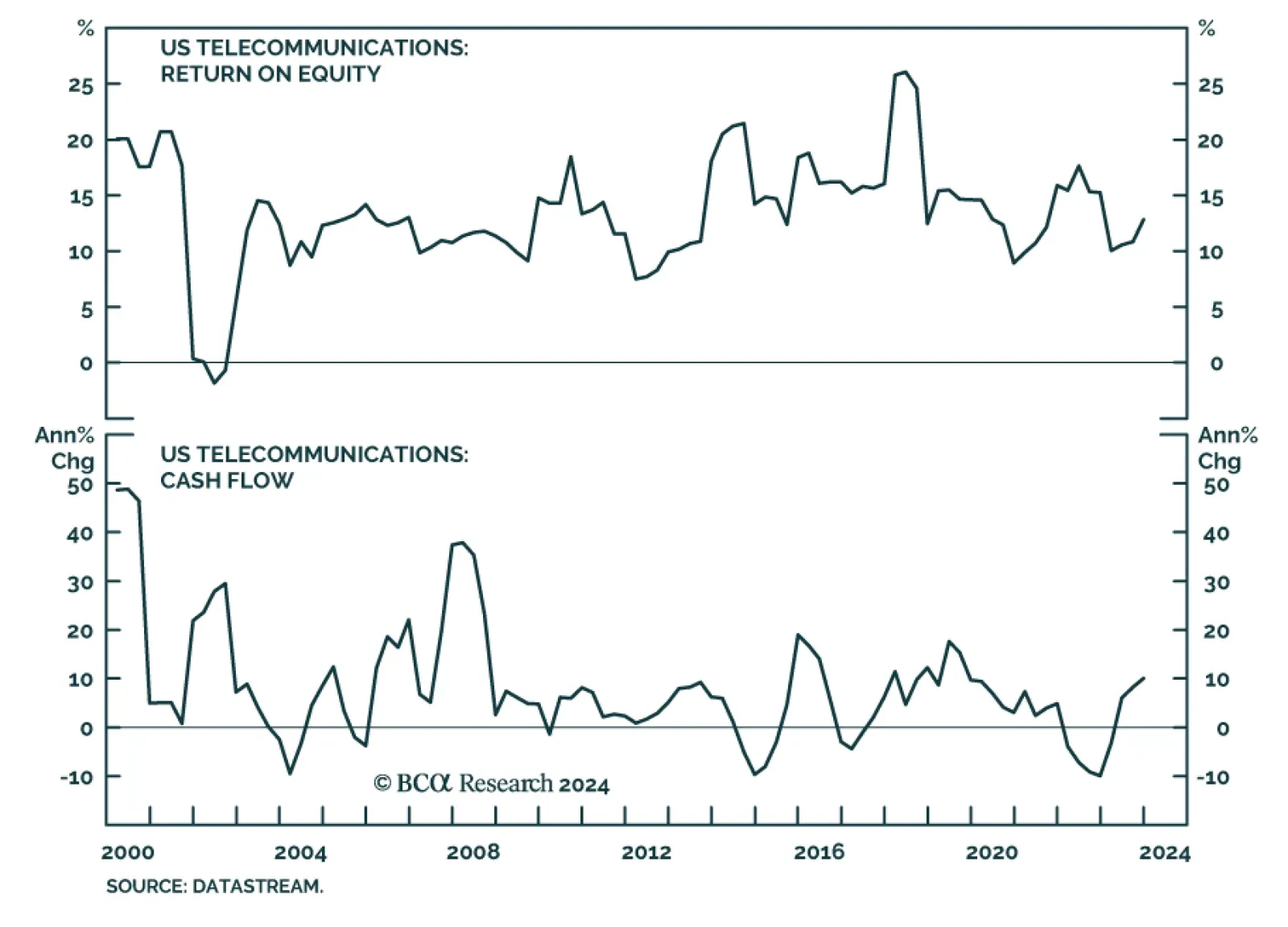

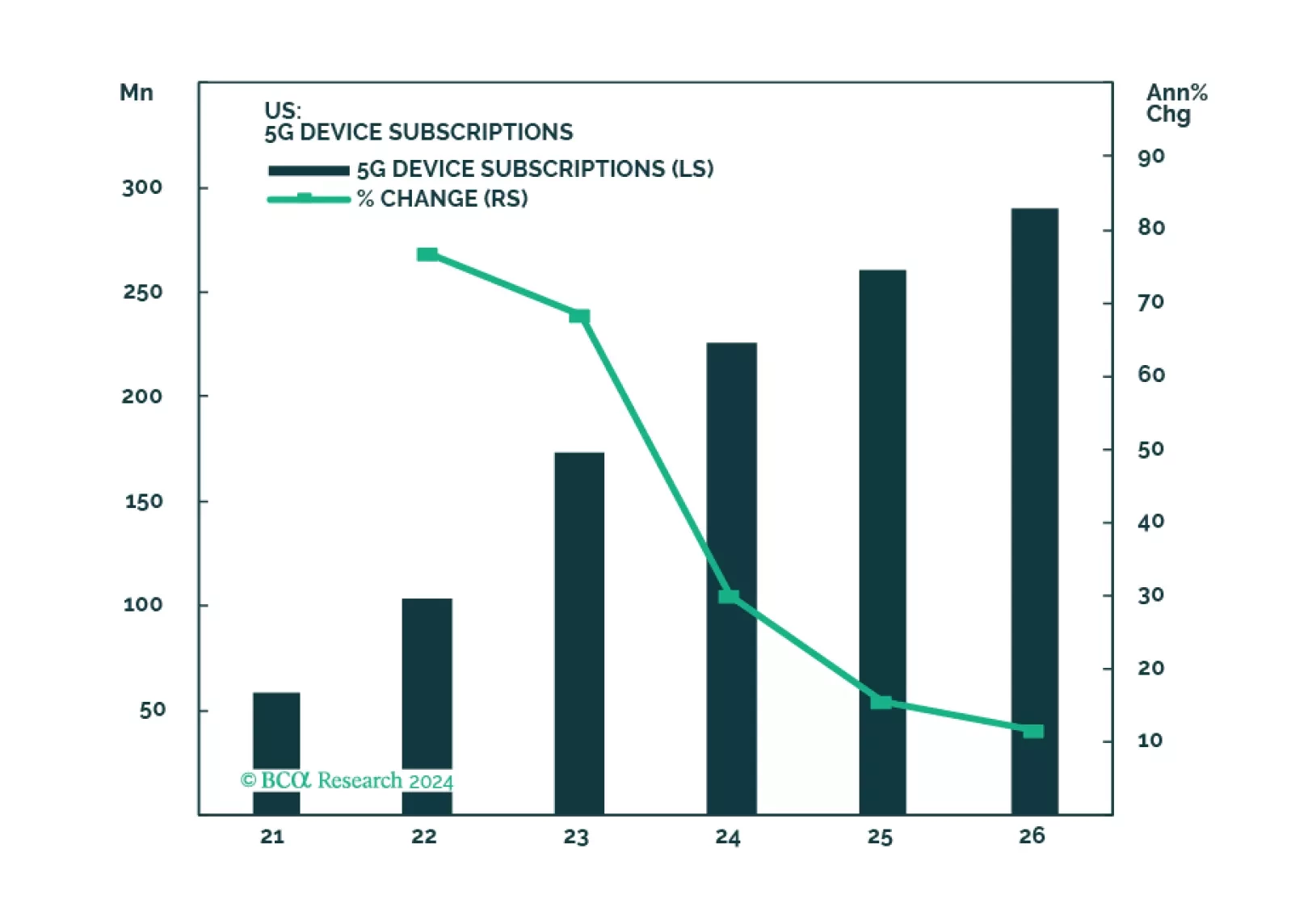

The Telecoms industry is highly concentrated, and carriers compete on price and quality of service in a slow growing market. Demand for capex is relentless. The roll out of 5G has disappointed. Recently, capex outlays have slowed, and operating cash flow has rebounded. Further, Telecoms is a quintessential defensive industry that will outperform during a market pullback.

In the short run, global risk assets are vulnerable due to rising oil prices and bond yields. Cyclically, a global economic downturn will weigh on global risk assets.