United States

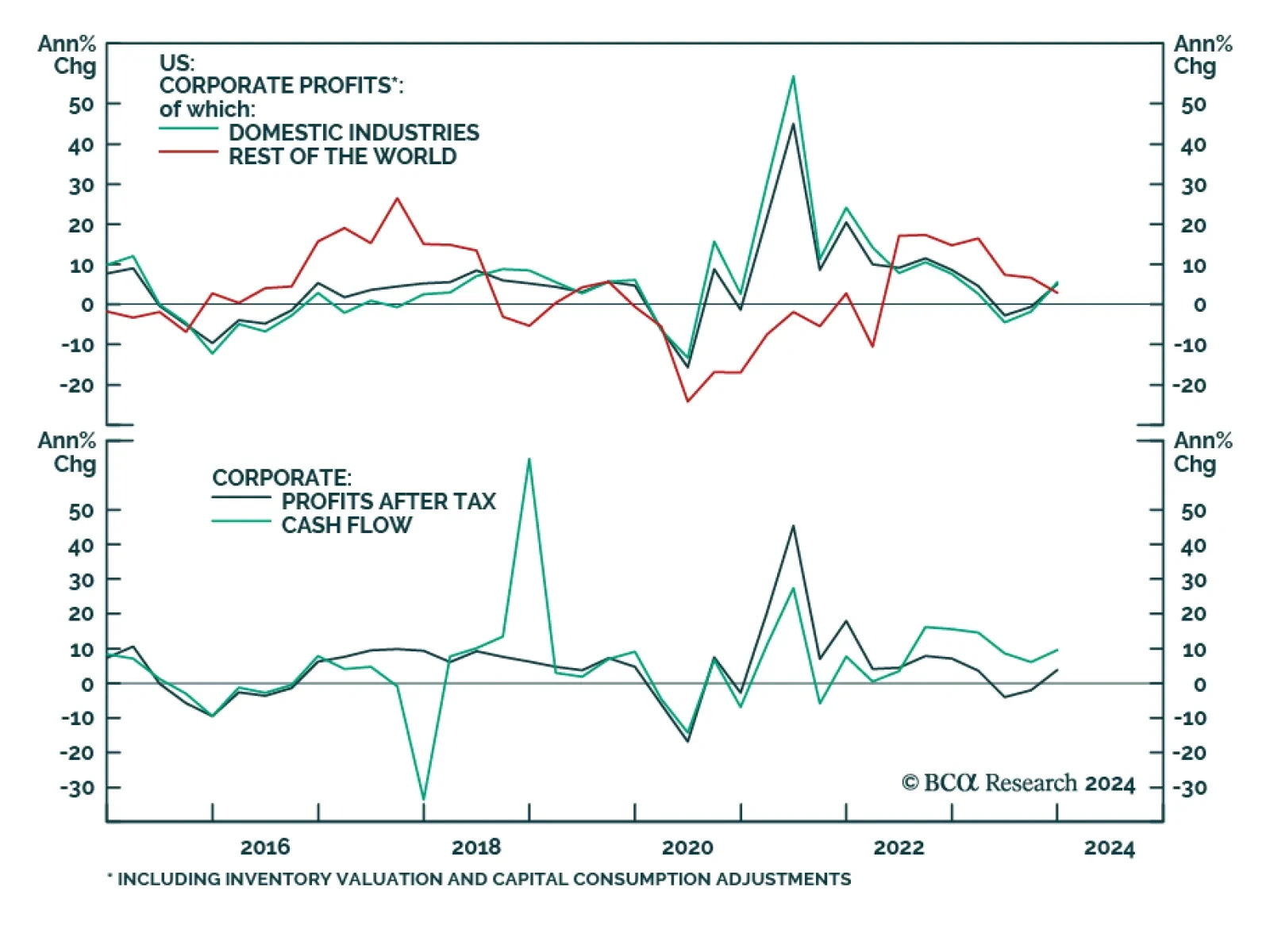

The US economy expanded at a faster pace than previously believed in 2023Q4. GDP grew at an annualized 3.4% q/q rate, thus annulling the second estimate’s downward revision. Notably, consumption growth was revised even higher to 3.3% q/q, from 3.0% q/q and…

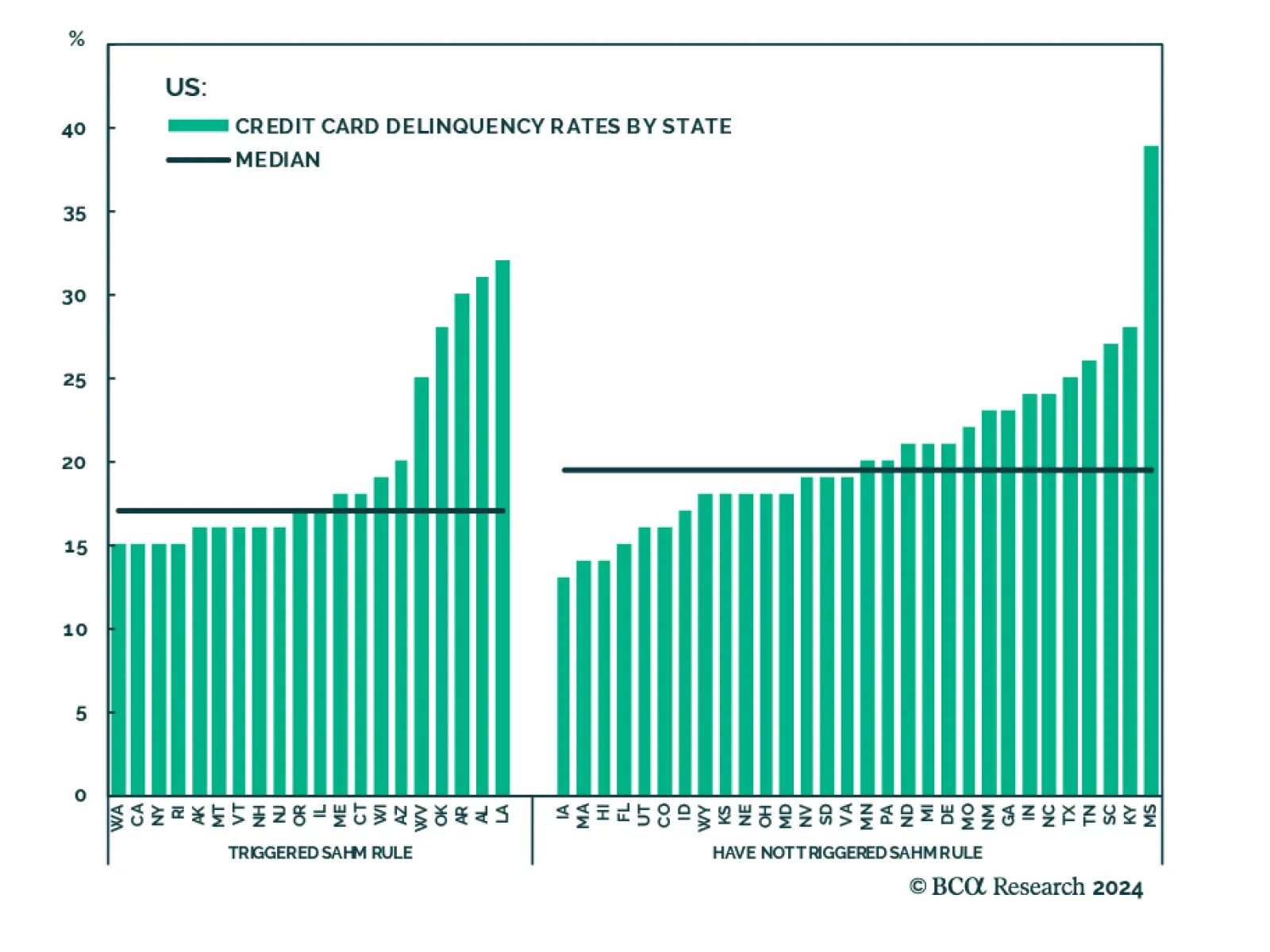

At 3.9% in February, the unemployment rate remains quite low in the US, corroborating the signal from GDP that current economic conditions are fine. Similarly, the Sahm Rule – which currently stands at 0.3 pp – has somewhat stabilized in recent months and has…

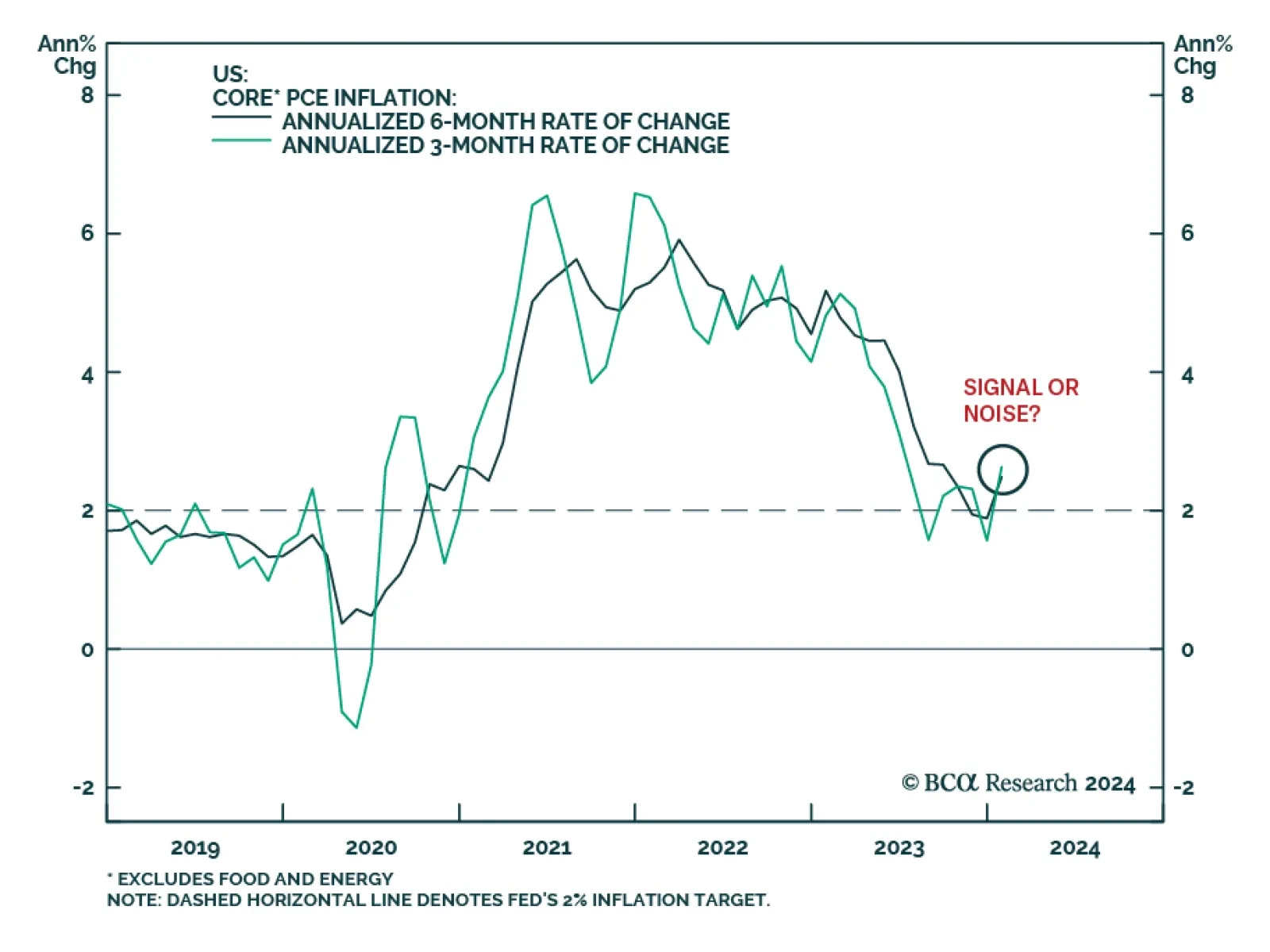

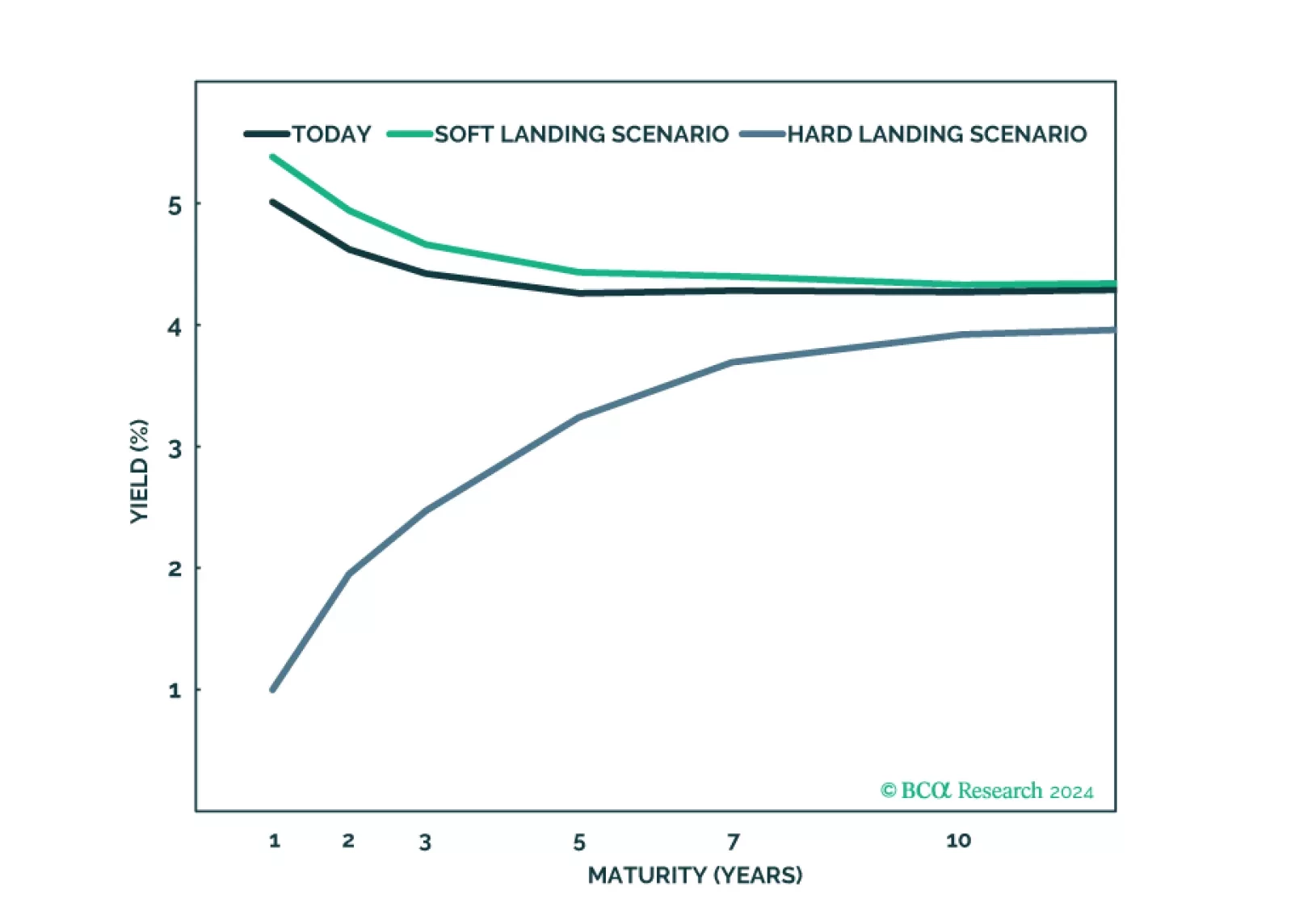

The message from Fed Governor Christopher Waller’s speech on Wednesday could not be clearer: there’s still no rush. While market participants as well as the FOMC are still pricing in three rate cuts this year, the recent hotter-than-anticipated inflation data…

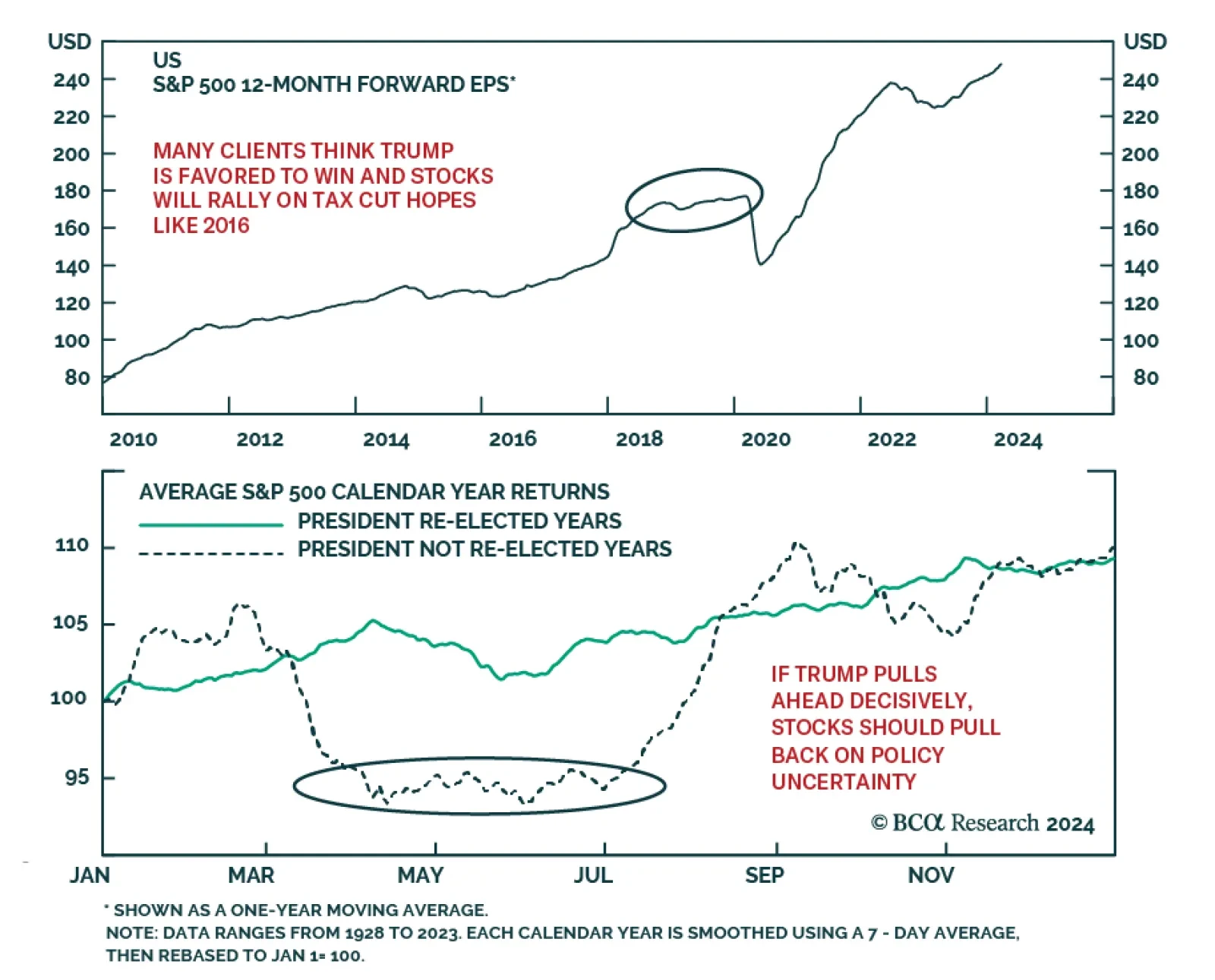

According to BCA Research’s Geopolitical Strategy service, Trump’s agenda is structurally inflationary and would eventually be needed to be discounted by markets, if he wins. Most retail investors – and many clients – seem to believe that Trump will win…

Investors around Europe and North America are concerned that the stock market is increasingly overbought and vulnerable to exogenous risks. We agree and have good reasons to fear that festering geopolitical risks and the US election season will deal negative surprises.

We expand our risk/reward analysis of US investment grade corporate bonds to focus on the 44 industry groups included in the Bloomberg index.

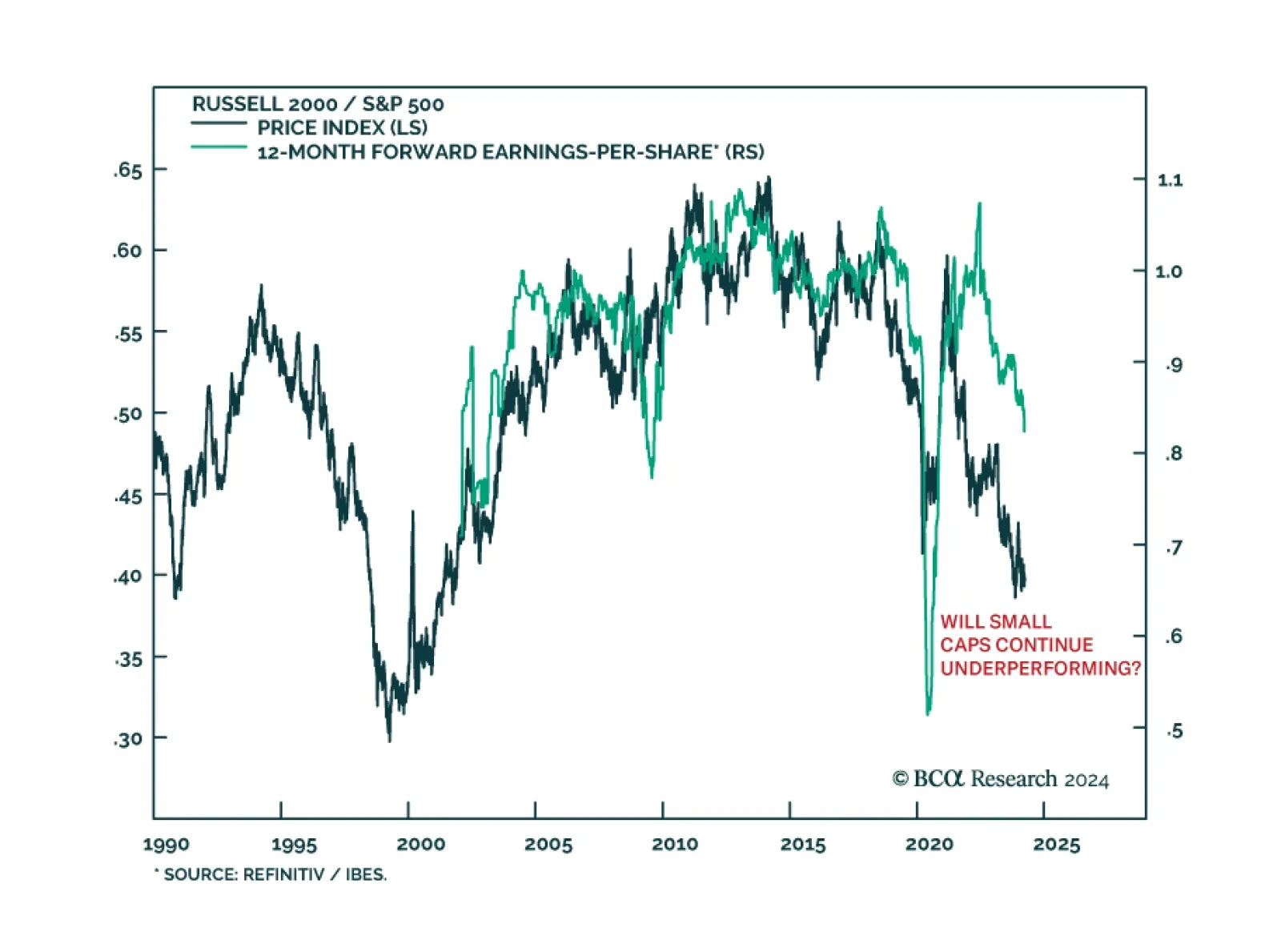

In an Insight we published yesterday, we highlighted that the S&P 500 rally has recently stopped narrowing with the gap between the market cap-weighted and equal-weighted indices stabilizing over the past month. This has also coincided with a…

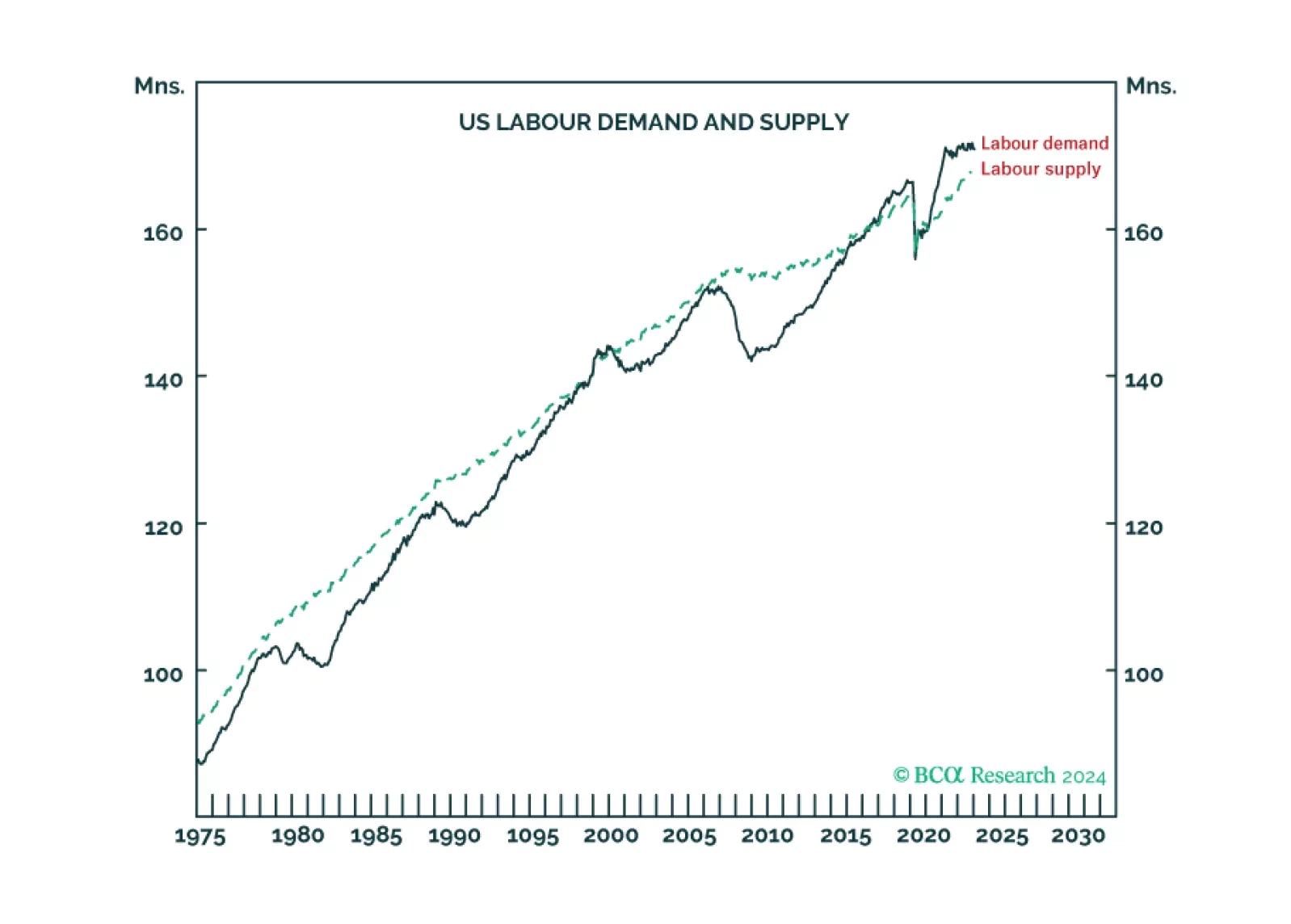

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and asset allocation. Plus: NVDA is at a consolidation point.

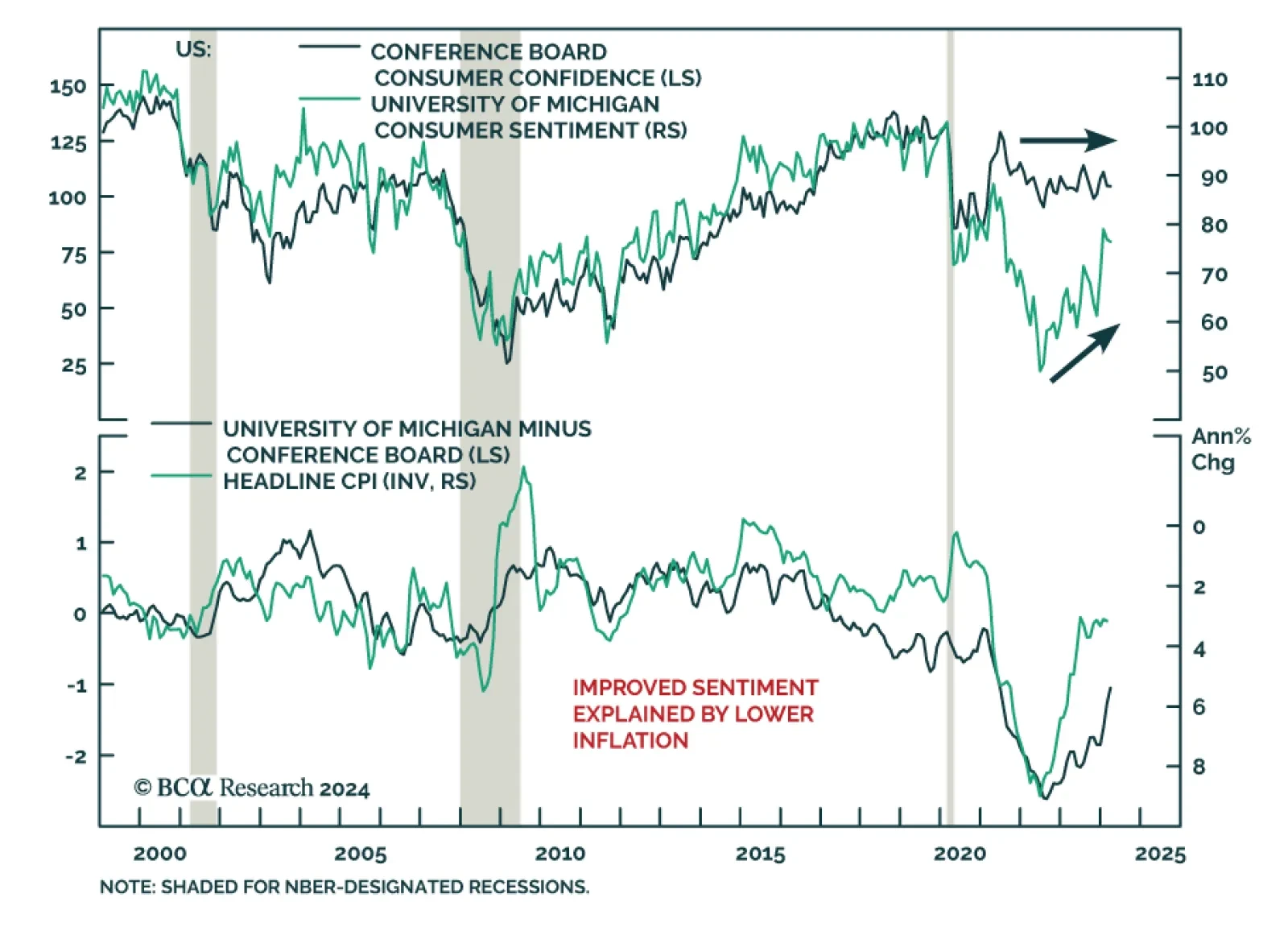

The Conference Board’s gauge of US consumer confidence came in at 104.7 in March – broadly unchanged from a downwardly revised 104.8 in February and below expectations of an improvement to 107. The Expectations Index deteriorated from 76.3 to 73.8, while…

The US equity rally has recently stopped narrowing with the gap between the market cap-weighted and equal-weighted indices for the S&P 500 stabilizing over the past month. Indeed, this has coincided with a shift in market leadership. Energy, Materials,…