United States

Remain neutral on equities and underweight credit as the US economy enters 2026 at a pivotal but fragile point. A new year does not reset the business cycle, yet the US economy is entering 2026 at an important juncture. Recession fears have not materialized…

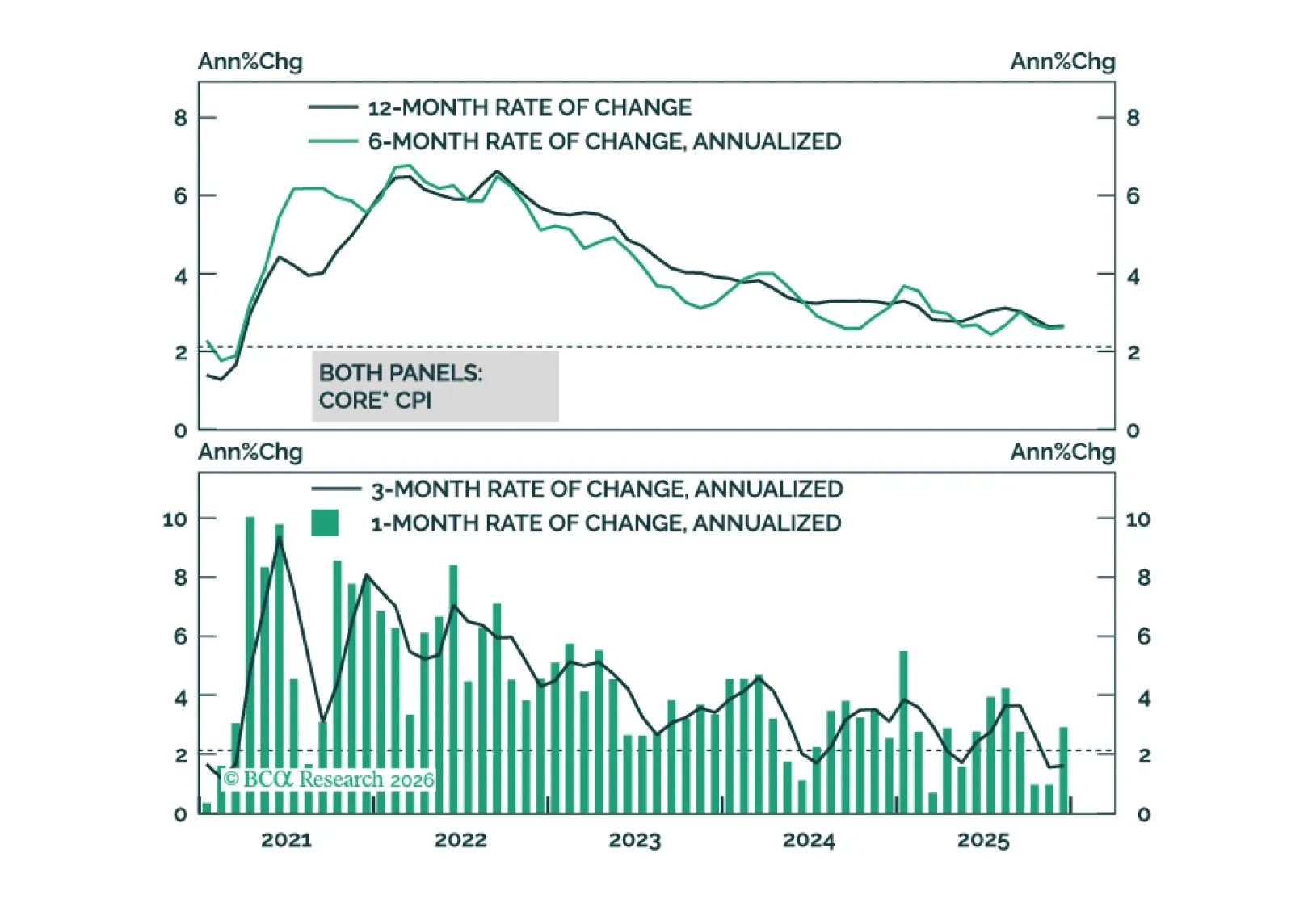

Maintain above-benchmark duration and 2-year/5-year Treasury steepeners as disinflation continues to support Fed cuts. US December CPI came in slightly cooler than expected, with headline inflation rising 0.3% m/m (2.7% y/y) and core inflation rising 0.2% m/m…

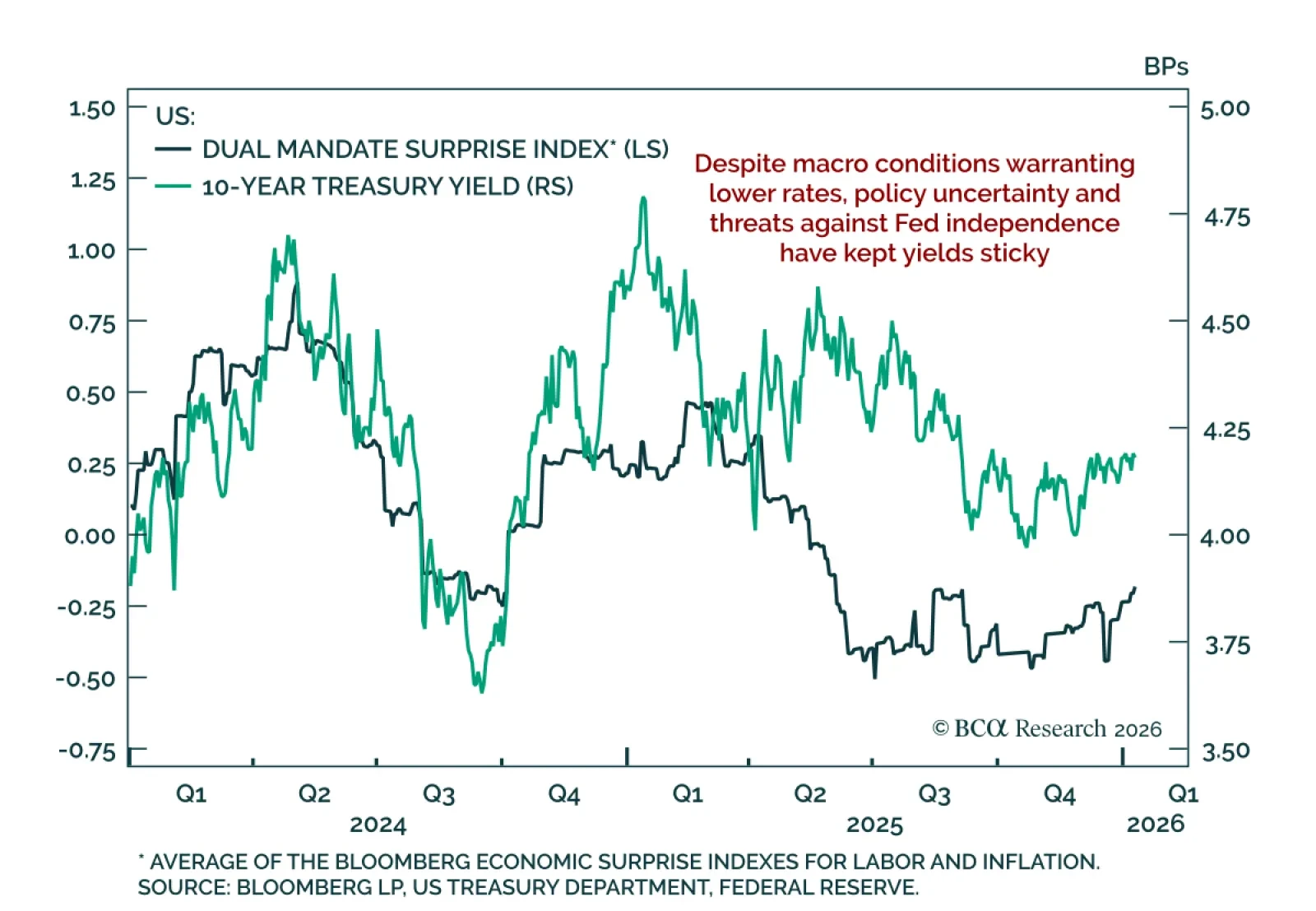

Our Global Fixed Income strategists maintain an above-benchmark duration stance as labor market risks continue to support downside yield potential, even as the global easing cycle winds down. With policy normalization largely complete, monetary policy is…

After 250 years, the USA is still the biggest thing happening in the world. But it faces huge challenges in the coming decades from socioeconomic imbalances and strategic competition.

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

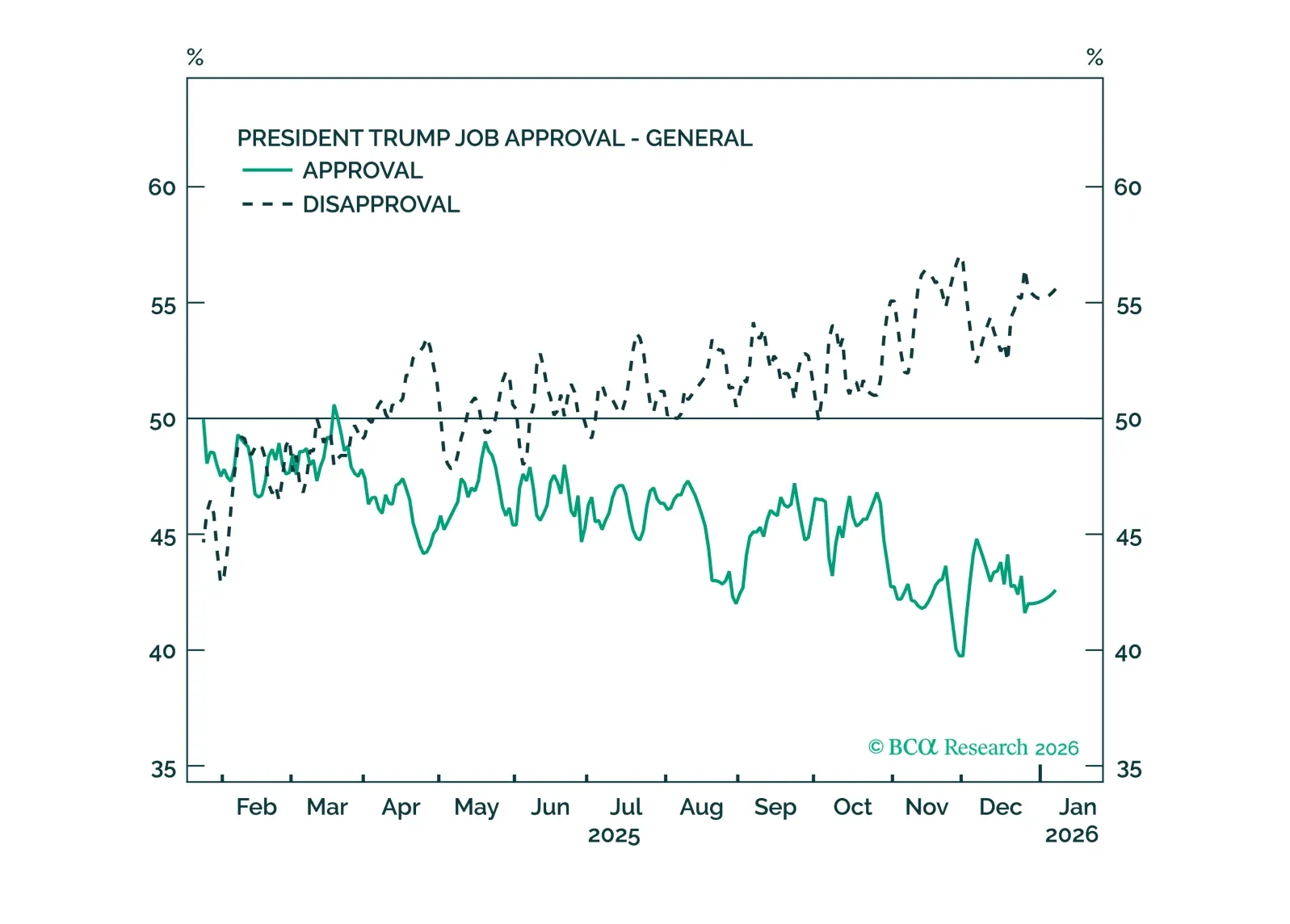

Congress will ultimately limit Trump from acting on his worst impulses, but his efforts to bypass those limits will cause market volatility.

Expect limited near-term market impact but longer-run USD headwinds as challenges to Fed independence play out. The Federal Reserve was served grand jury subpoenas by the Department of Justice threatening a criminal indictment. Fed Chair Powell responded with…

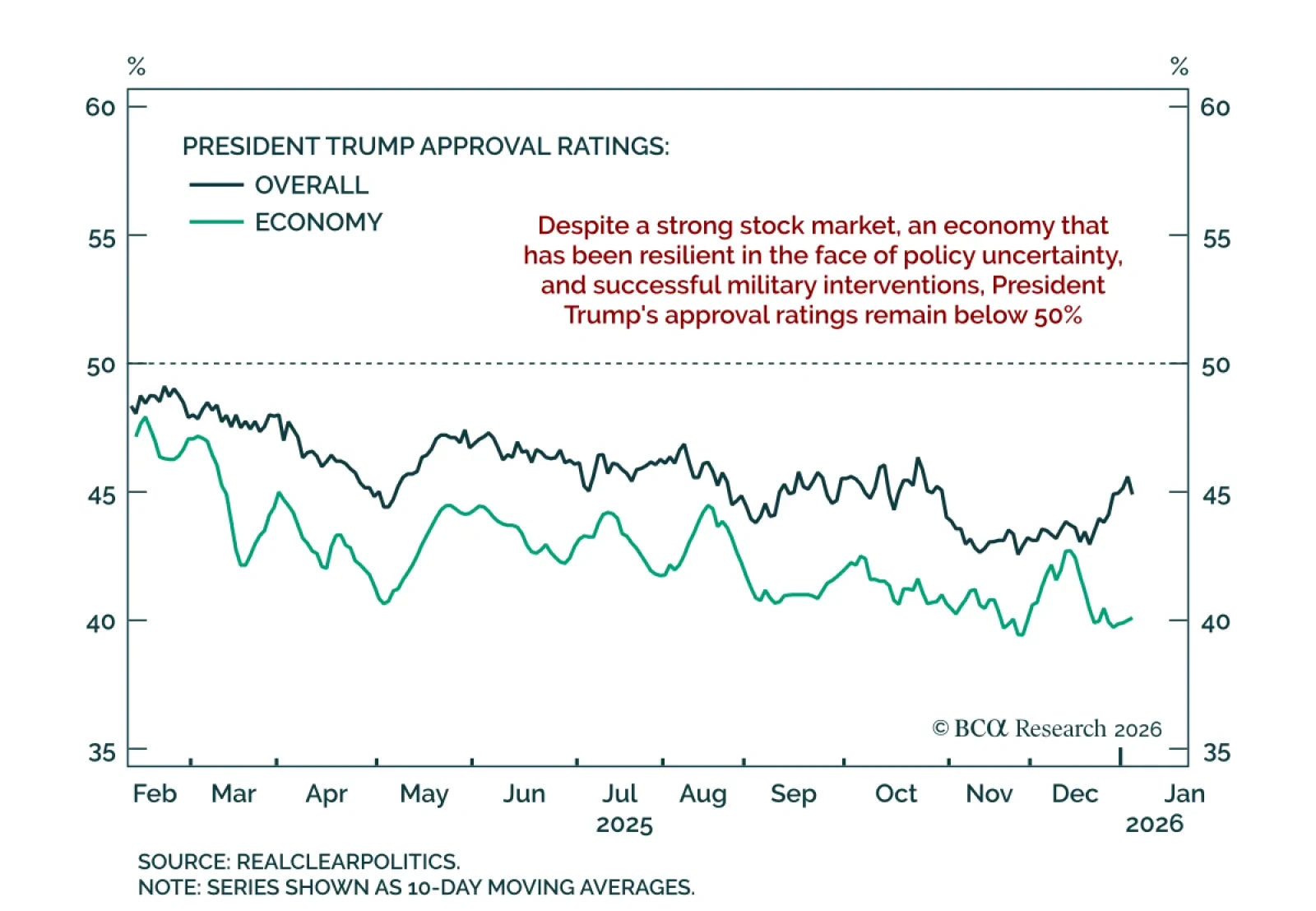

Maintain a moderately defensive stance as a bold but constrained Trump keeps policy risk elevated. President Trump’s second mandate has been quite different from his first. Trump remains a disruptive and unorthodox actor deliberately challenging norms and…

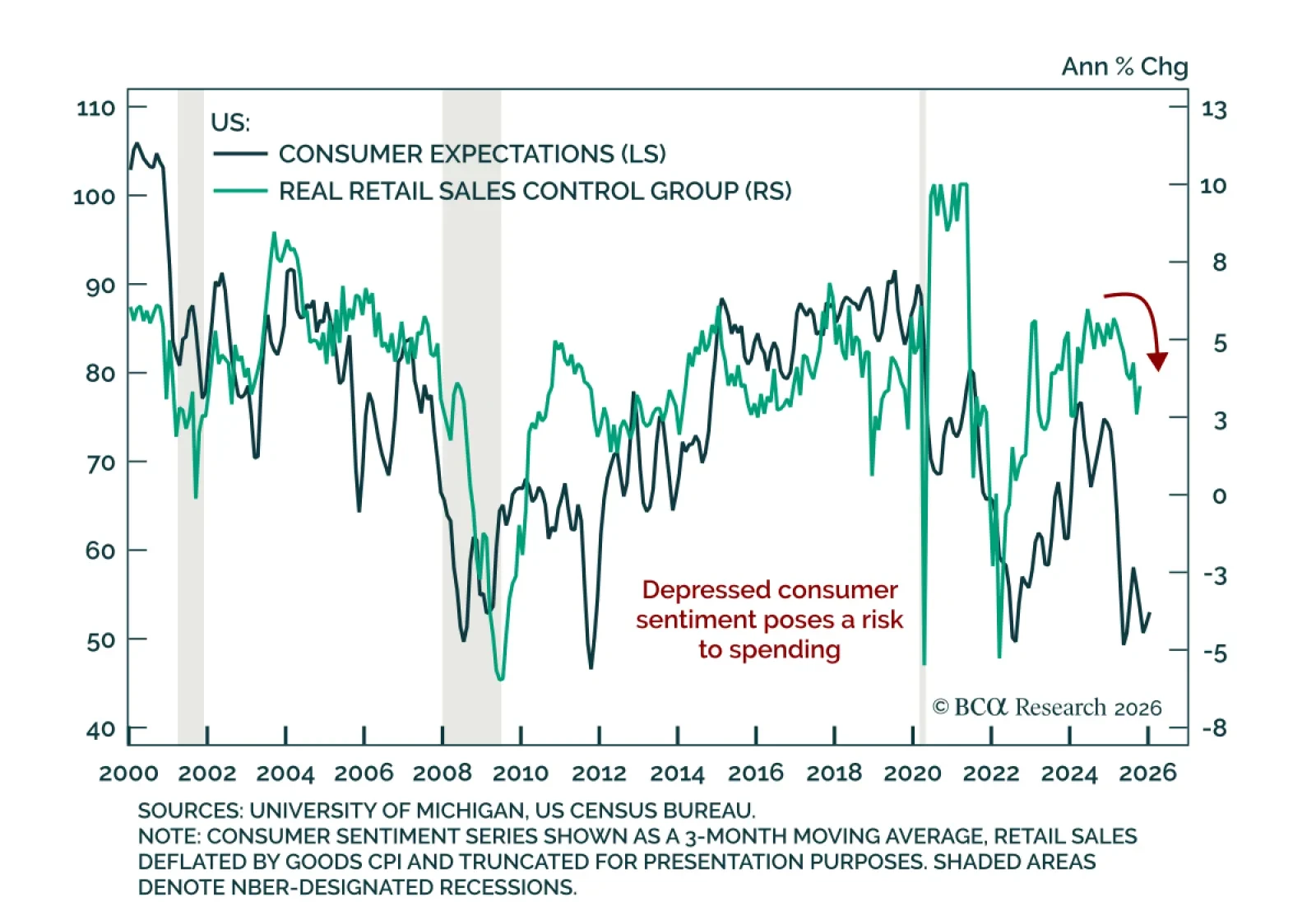

Maintain a conservative tactical stance as subdued sentiment and slowing labor dynamics pose risks to consumption. The preliminary January University of Michigan Consumer Sentiment Index slightly beat expectations, rising to 54.0 from 52.9, reflecting an…

Our Global Asset Allocation strategists remain constructive on risk assets and continue to overweight cyclical sectors while recommending staying overweight tail risk protection as markets brace for tariff-related uncertainty. A forthcoming decision on US…