United States

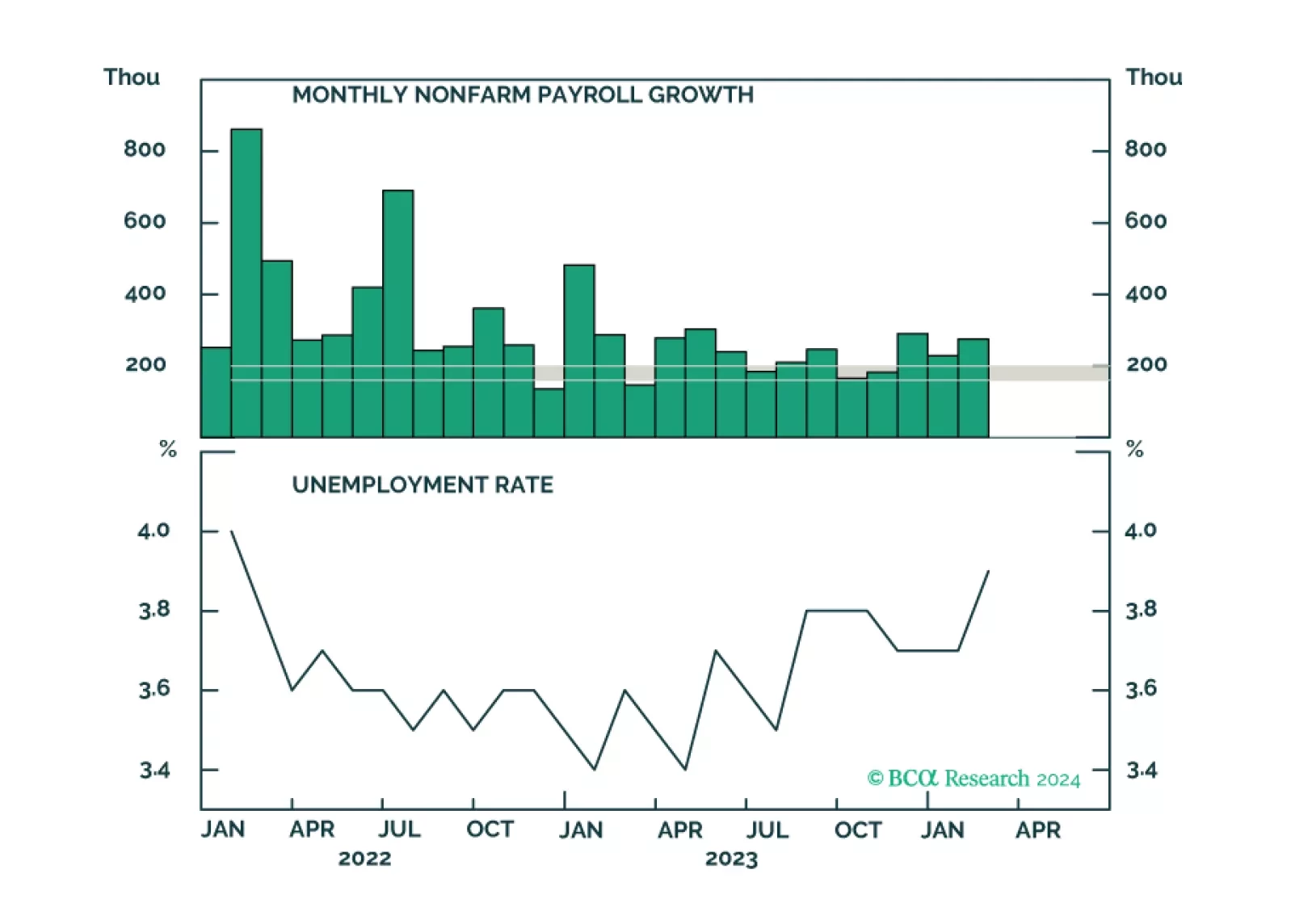

We update the indicators in our duration checklist following this morning’s employment report.

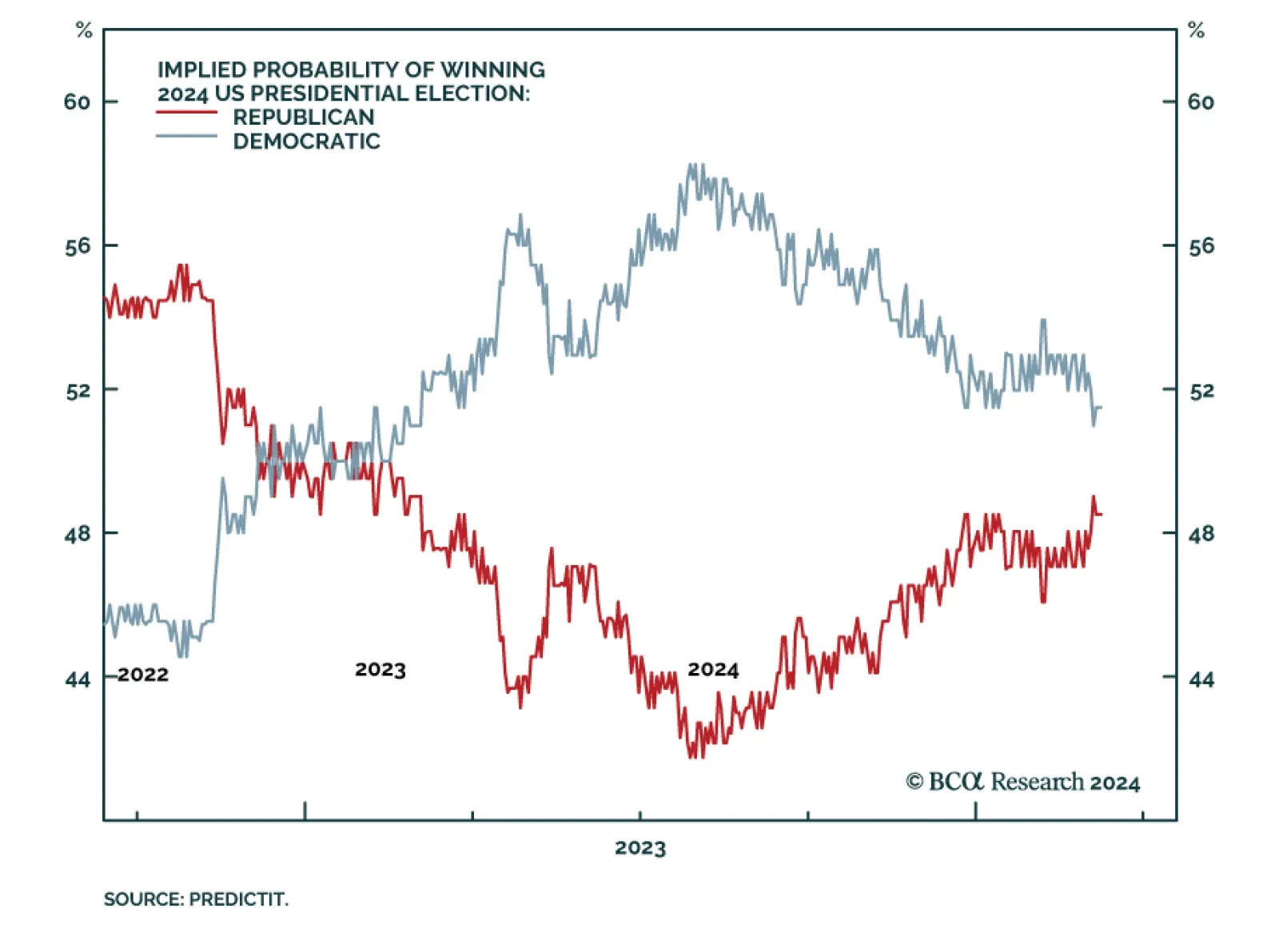

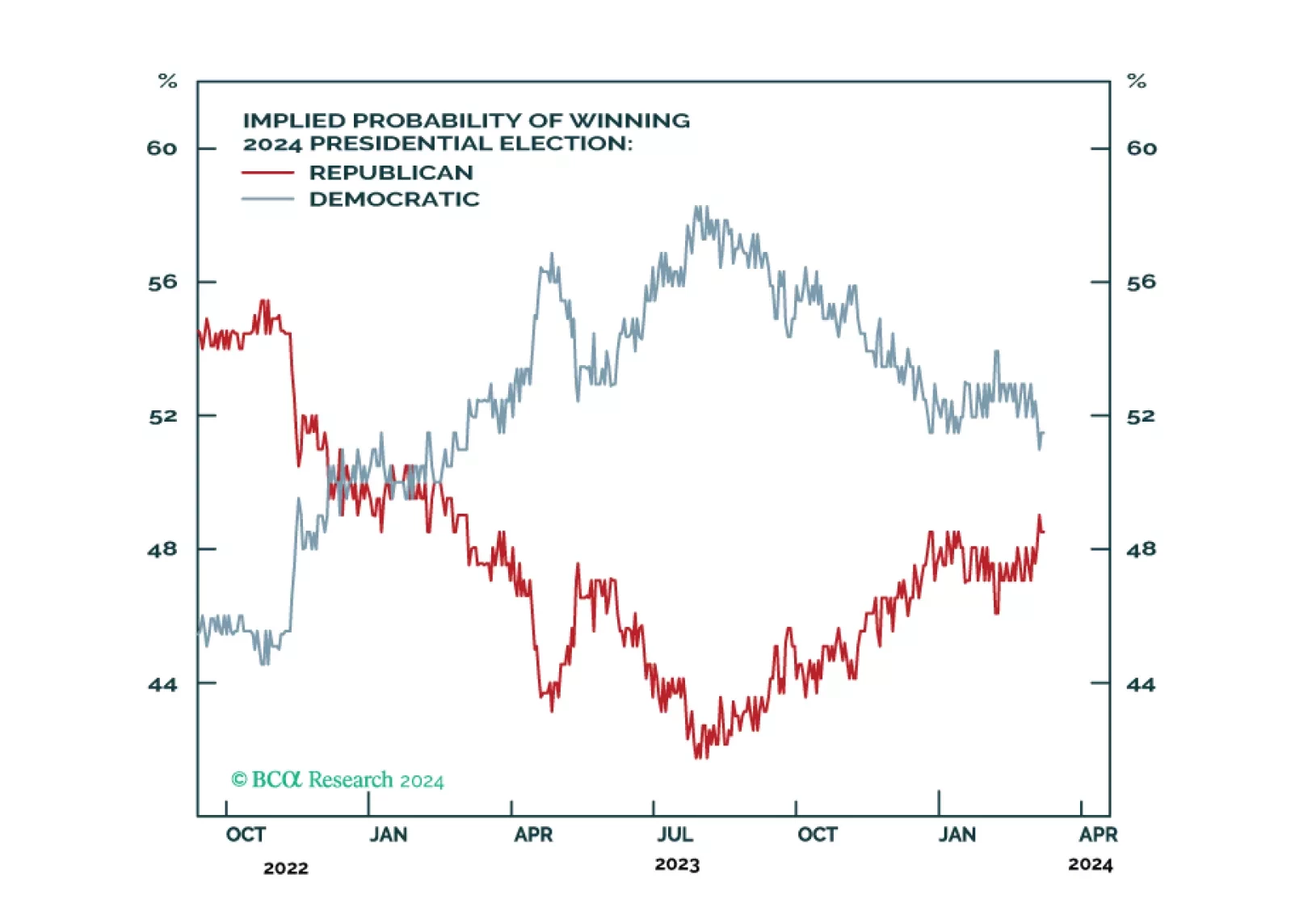

Democrats are still slightly favored for reelection as the incumbent party is presiding over a growing economy. However, Biden’s strong showing in the primary election is not lifting his popular approval yet, and that is a worrying sign. Policy uncertainty should rise sharply, which is marginally negative for the stock market.

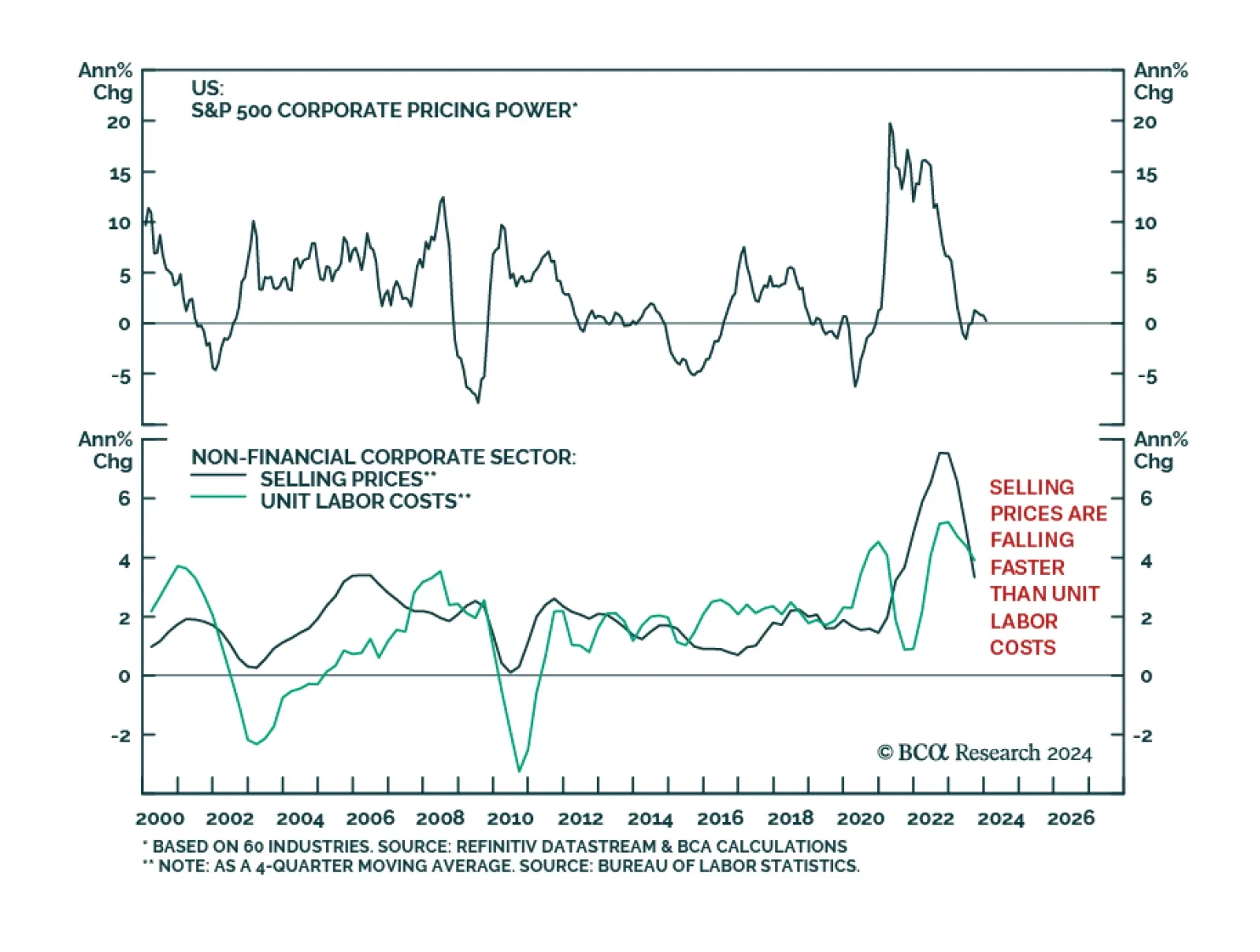

Presently, our four high-conviction themes are: (1) the US dollar will rally as US growth continues to outpace the rest of the world; (2) US equities will continue to outperform EM and European stocks until a major sell-off occurs; (3) a US profit margin squeeze is imminent; (4) EM domestic bonds and sovereign USD bonds are due for a setback.

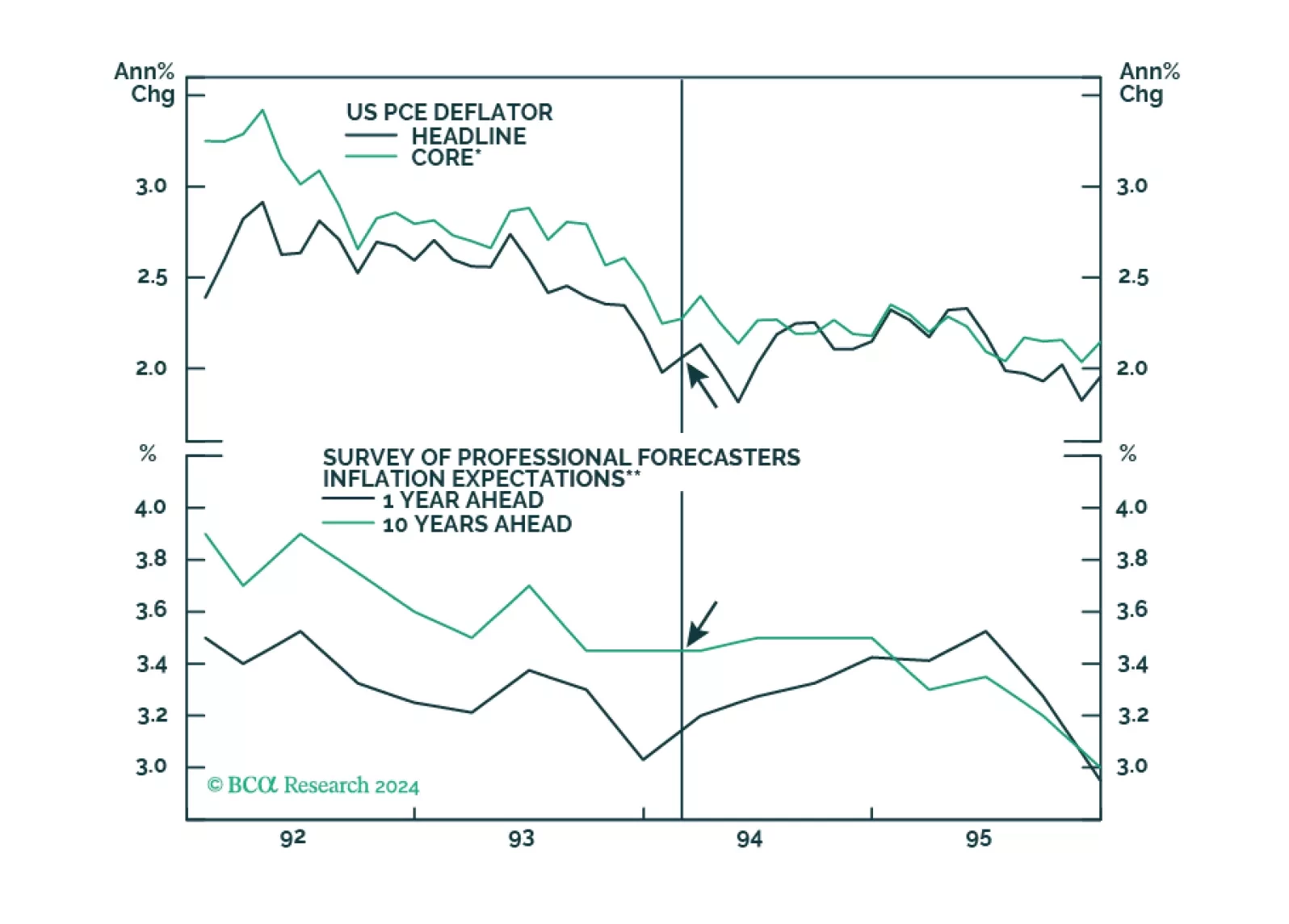

Many investors have cited the 1994 tightening cycle as an example of how the Fed managed to raise rates without triggering a recession. However, the unemployment rate was 6.5% in early 1994, which meant that inflation was less of a risk than it is today. Productivity growth also accelerated starting in the mid-1990s. While something similar may happen again thanks to AI, so far this is not visible in the aggregate productivity data.

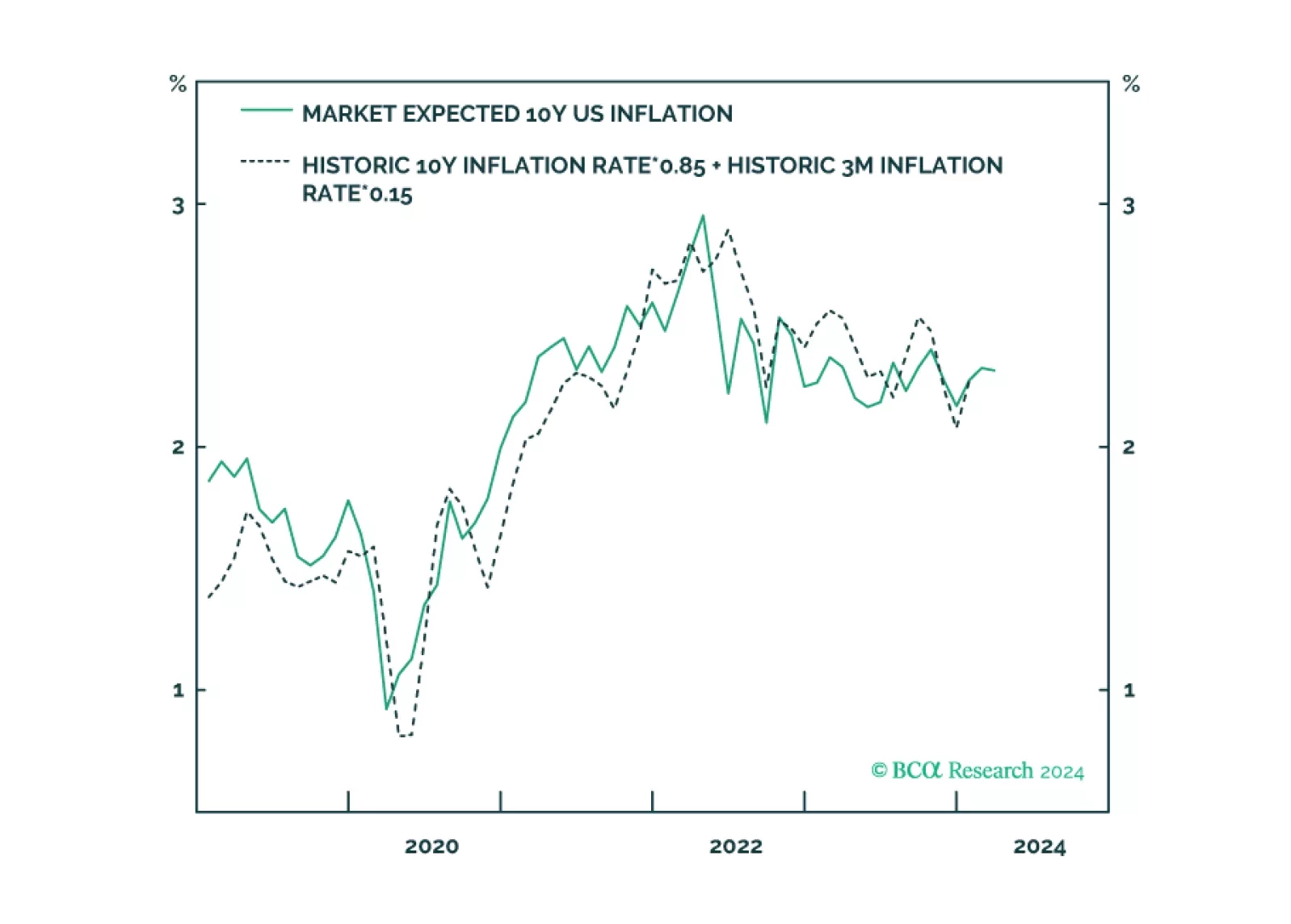

Expected inflation has surged to its highest level in a year. This has surprised many people, but expected inflation is behaving just as expected. Expected inflation is not a prophecy, it is just a mathematical function of delivered inflation. We discuss what this means for central banks in the US, UK, euro area, and Japan. Plus: bitcoin’s structural uptrend to $100,000+ is still intact.