United States

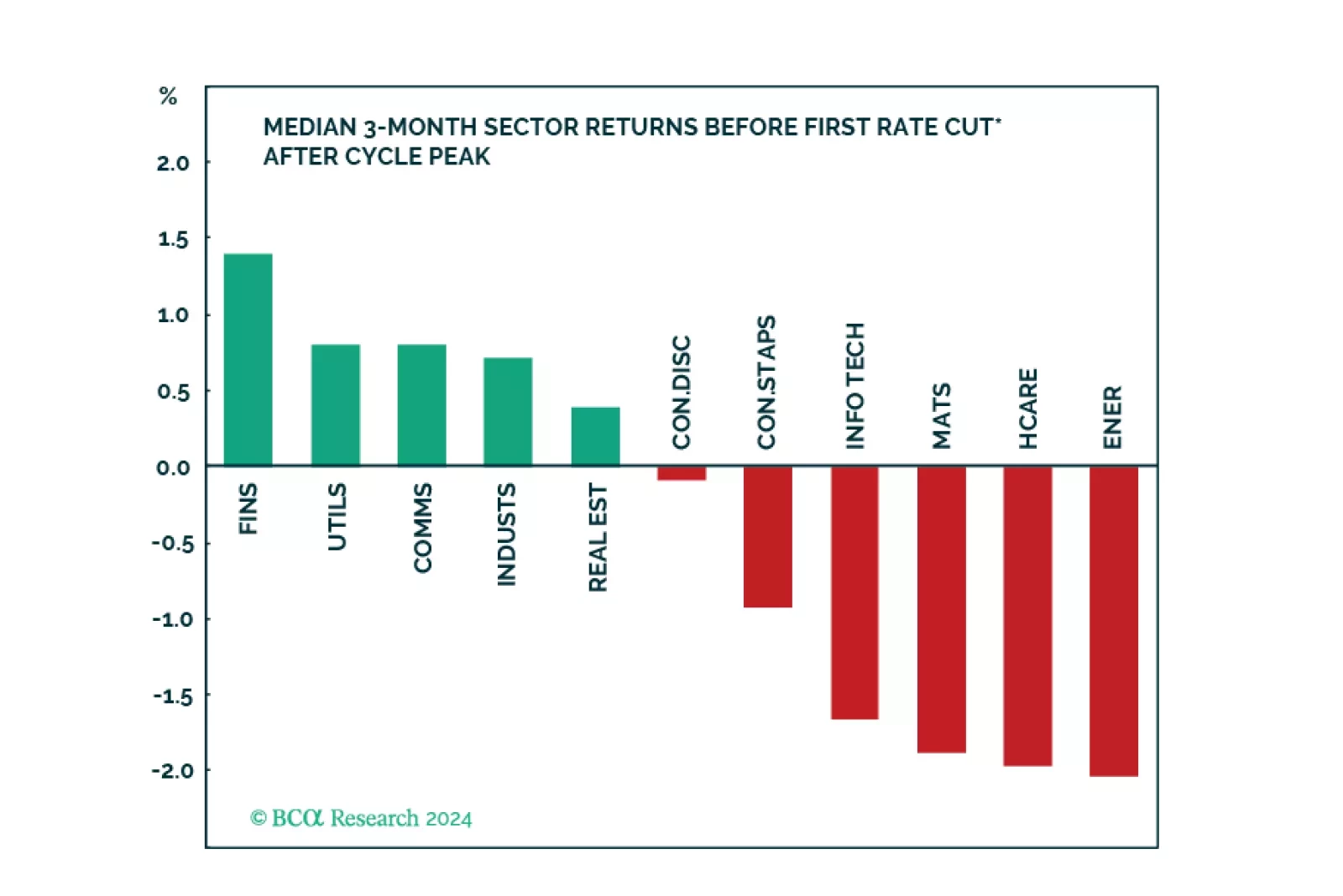

We created a sector selection scorecard based on performance of sectors under various macroeconomic regimes while taking into consideration revisions to expected earnings growth and valuations in a historical context. Our total sector selection scorecard suggests overweighting defensives such as Utilities, and Consumer Staples, and underweighting cyclicals such as Consumer Discretionary, Industrials, and Financials. Considering this analysis, we have adjusted our sector positioning accordingly.

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

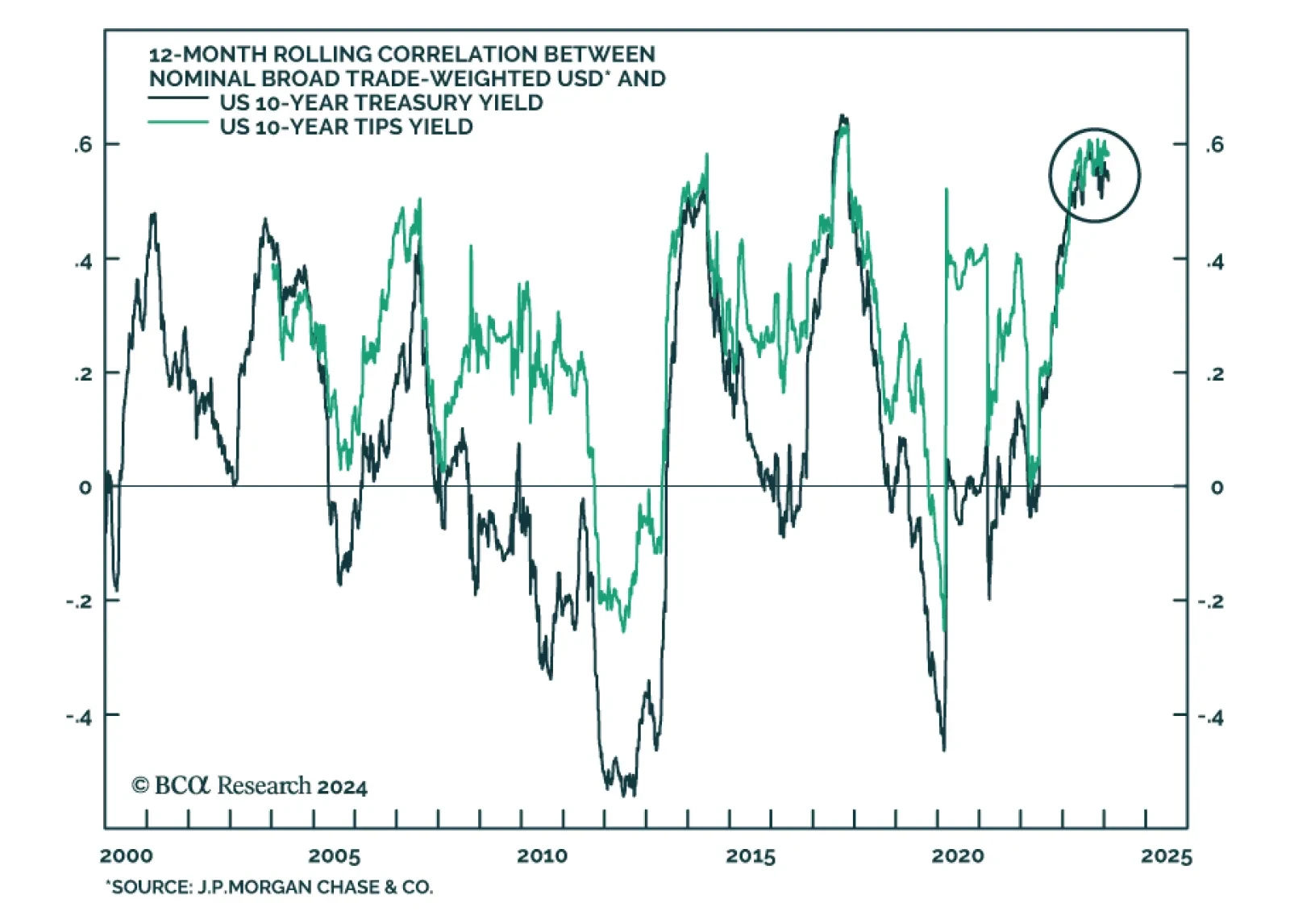

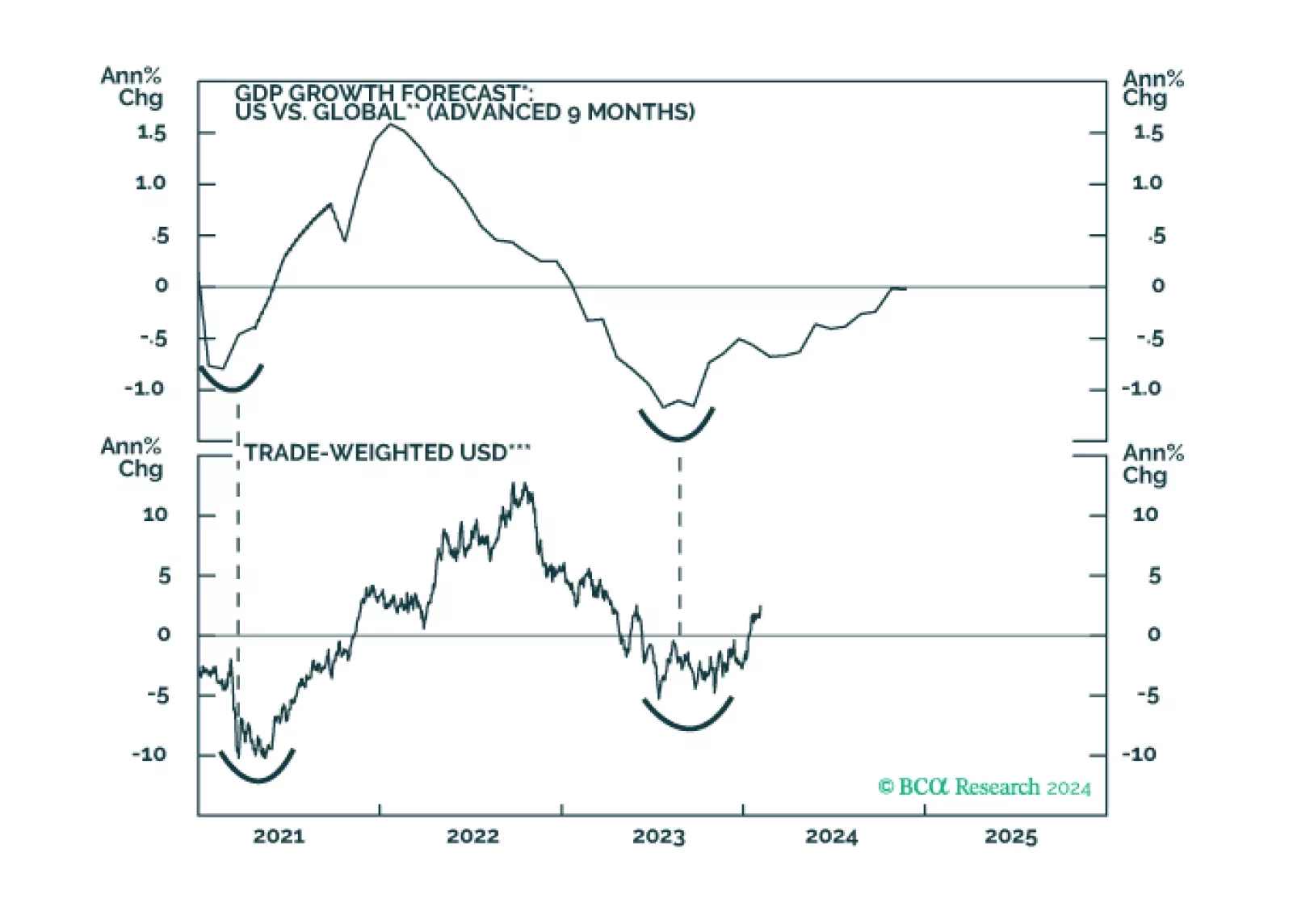

This week’s report explores factors behind the recent rise in the dollar, and whether this could continue in the next month.

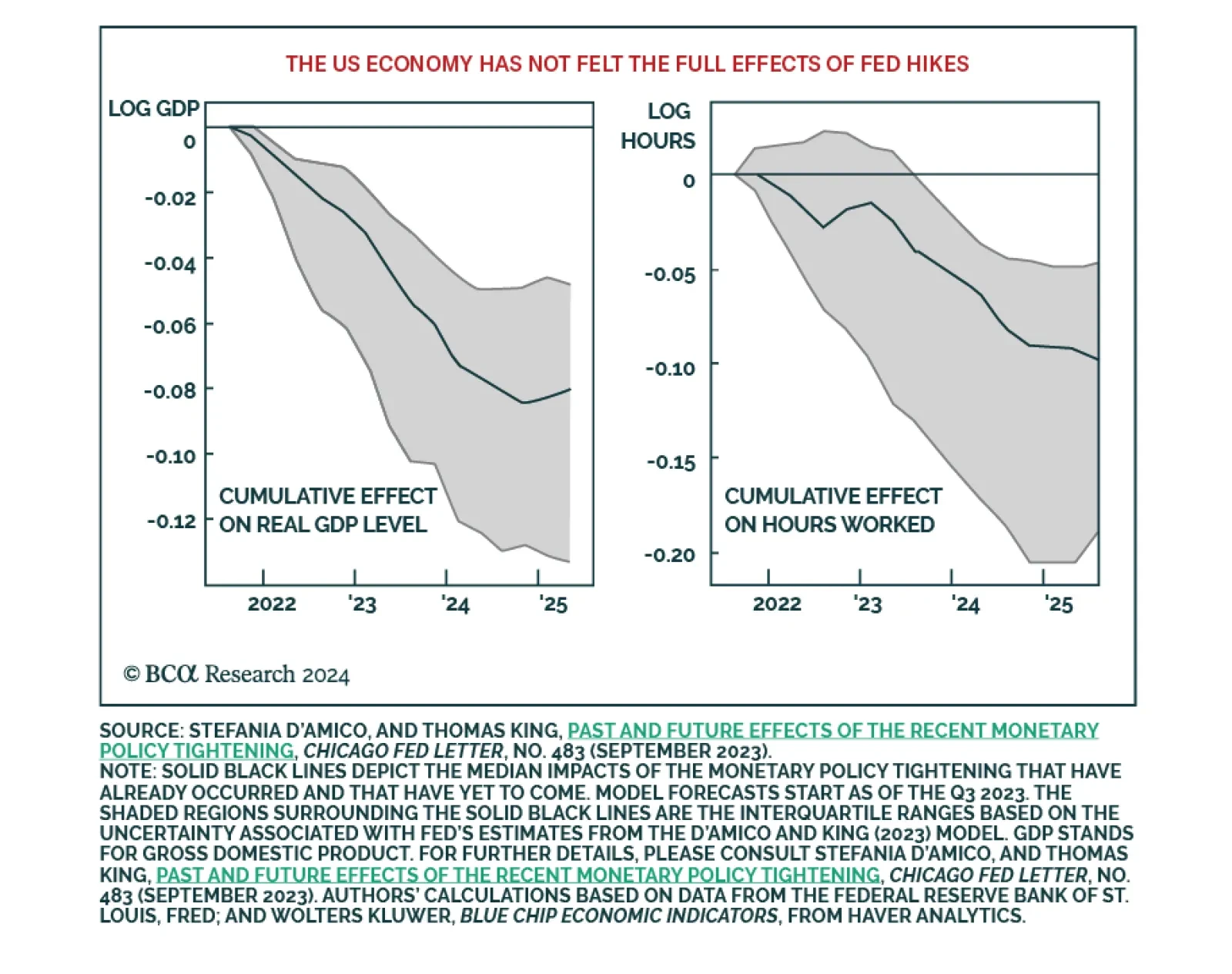

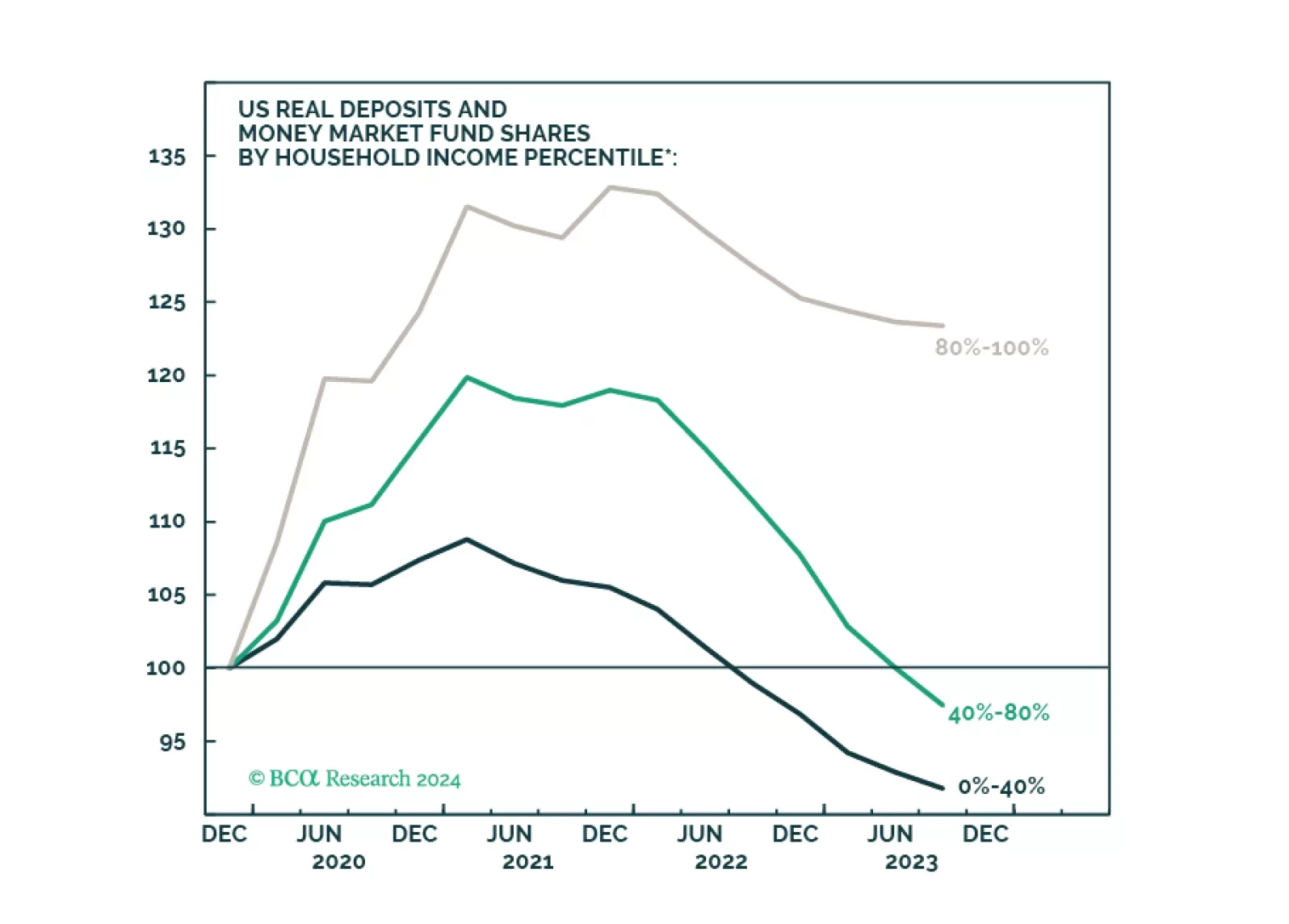

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.