United States

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

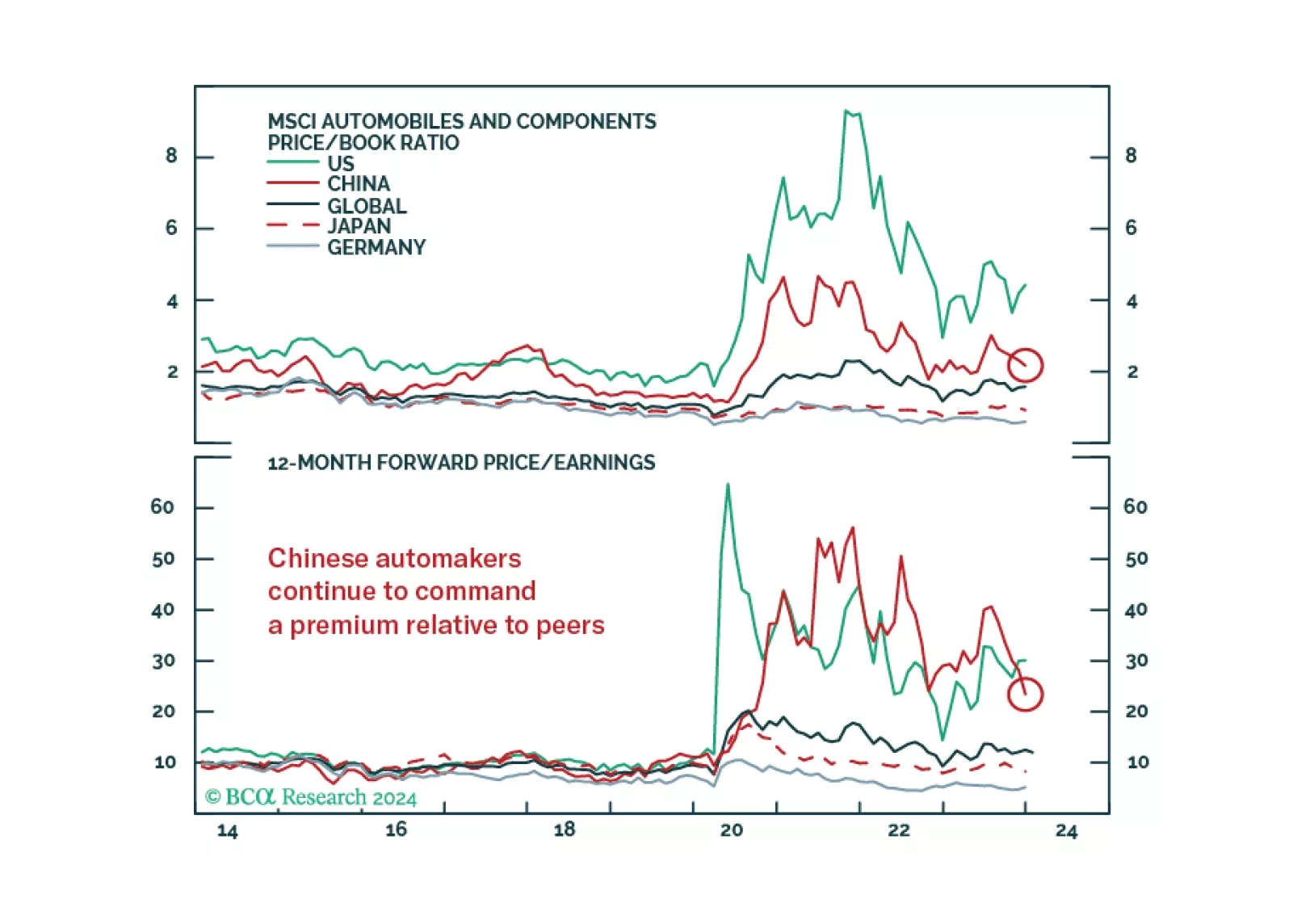

The expectation that China is best placed to win the global EV race presumes the persistence of the status quo. Reality, however, may differ as the sector looks set to be hit by a range of changes. If nonlinearity were to emerge in the global auto sector, as it often does, then the EV transition could end up spawning a very unexpected list of winners and losers.

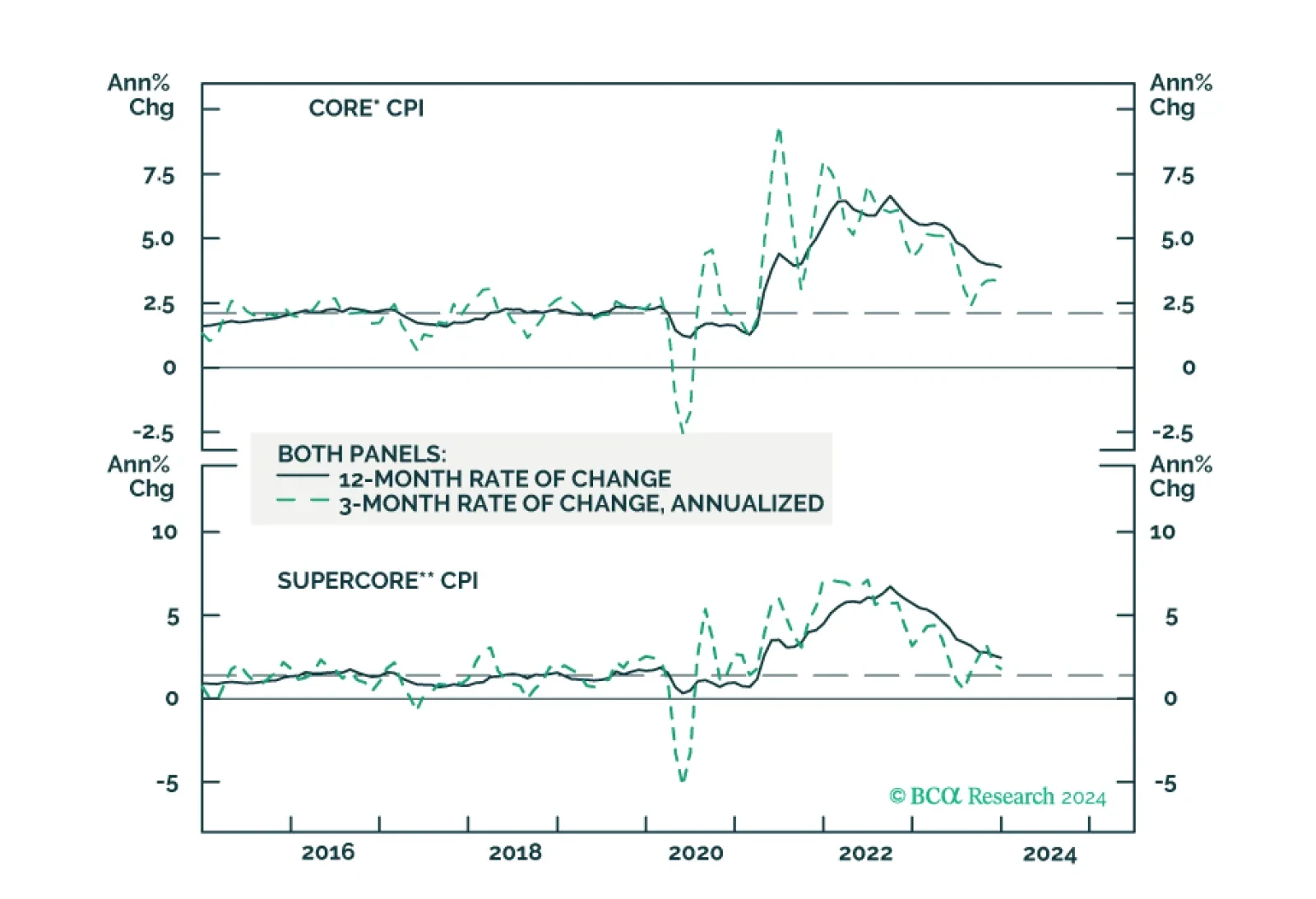

We update our inflation forecast following this morning’s CPI report.

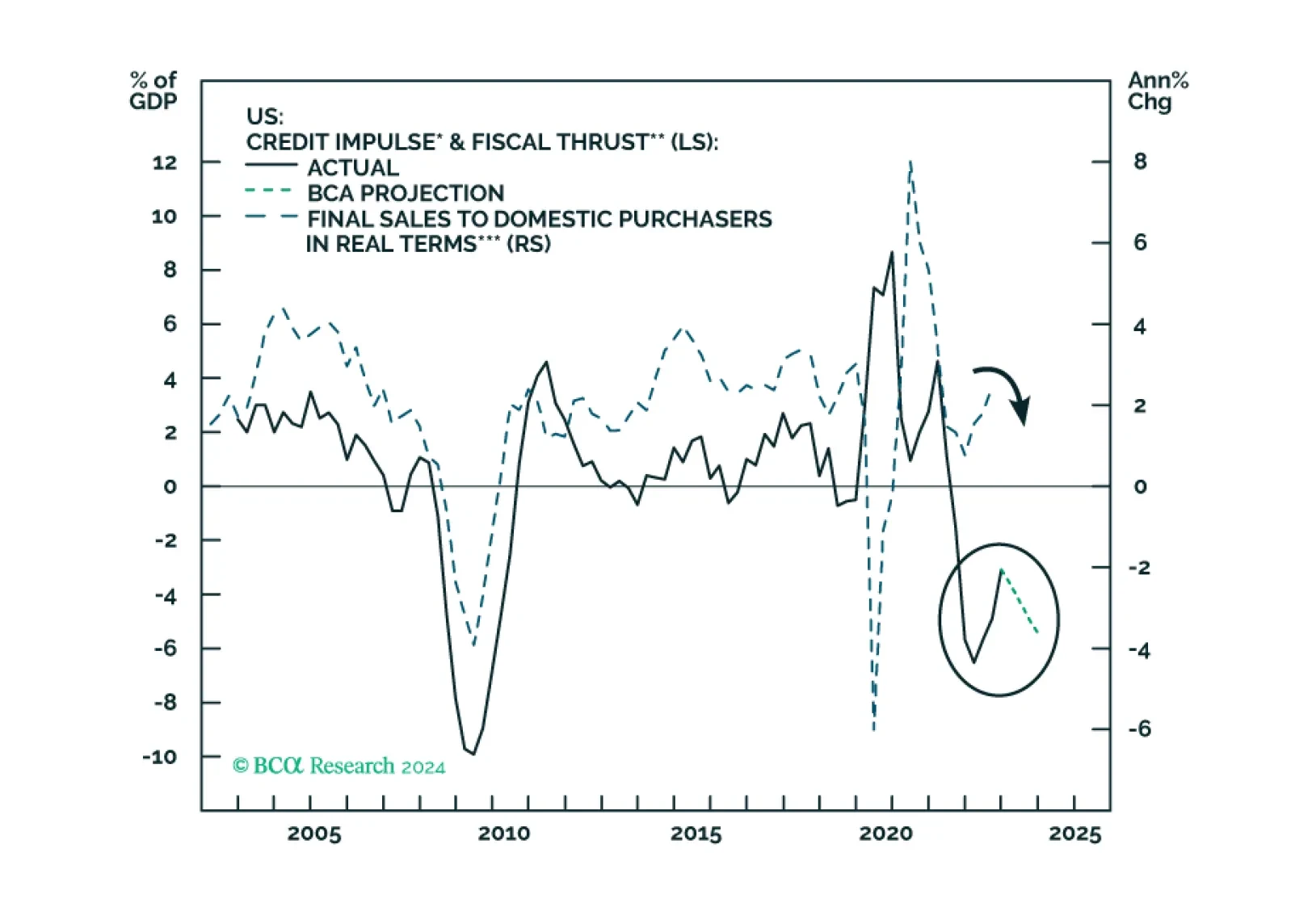

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.