United States

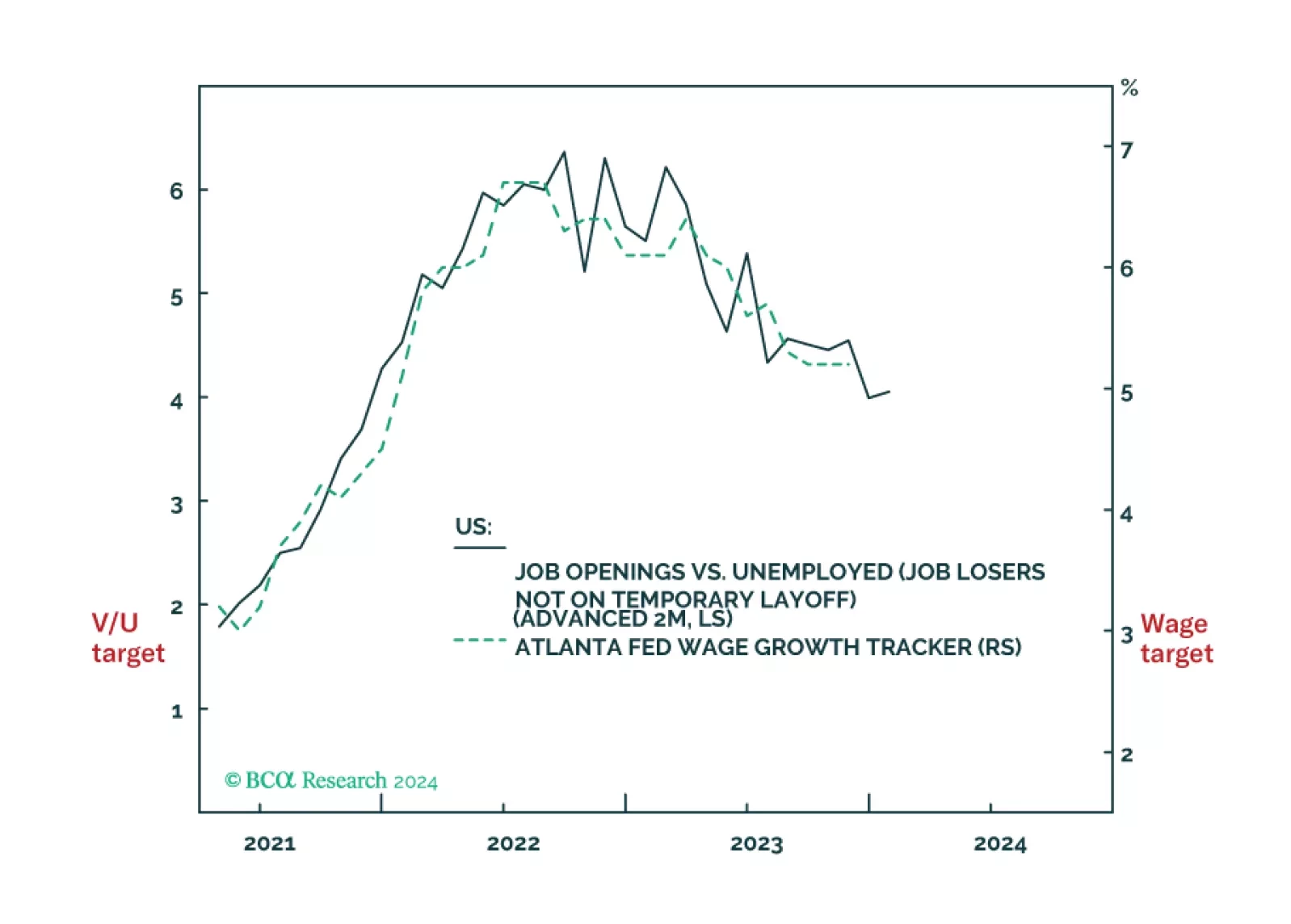

The Fed faces a dilemma. Cut rates early to avoid a recession, but at the risk of not slaying wage inflation. Or, not cut rates early to ensure that wage inflation is slayed, but at the risk of a downturn. Faced with such a dilemma, the lesser evil is to slay wage inflation even at the risk of a downturn. Meaning that the market has overpriced early rate cuts. We discuss some other investment implications, and identify two rebound candidates.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Our Portfolio Allocation Summary for January 2024.

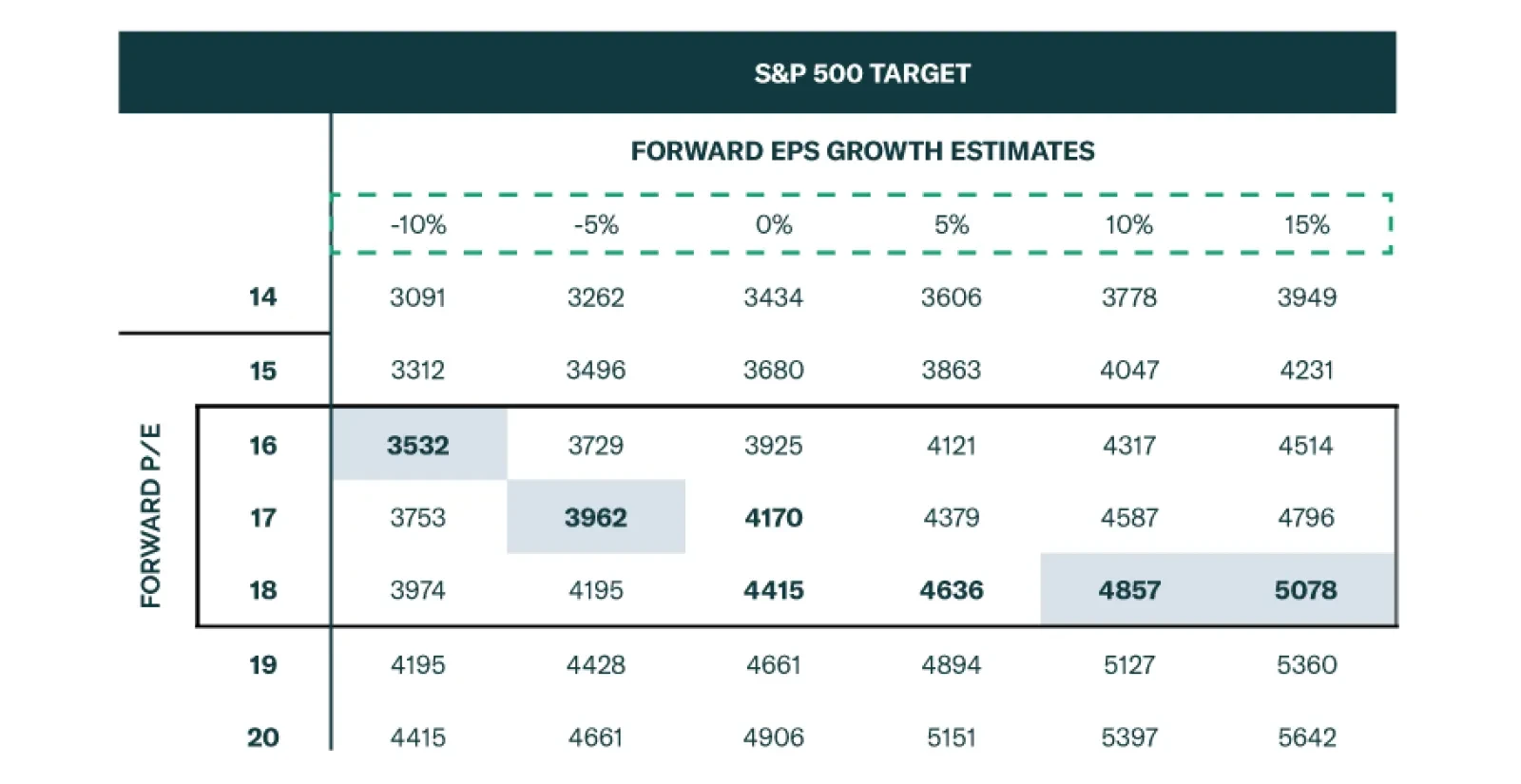

Despite the blah opening to the year, we do not think stocks have reached an inflection point. We expect that incoming data will continue to flatter the soft-landing narrative for another couple of months, helping the S&P 500 to establish a new all-time high before the rally runs out of steam.

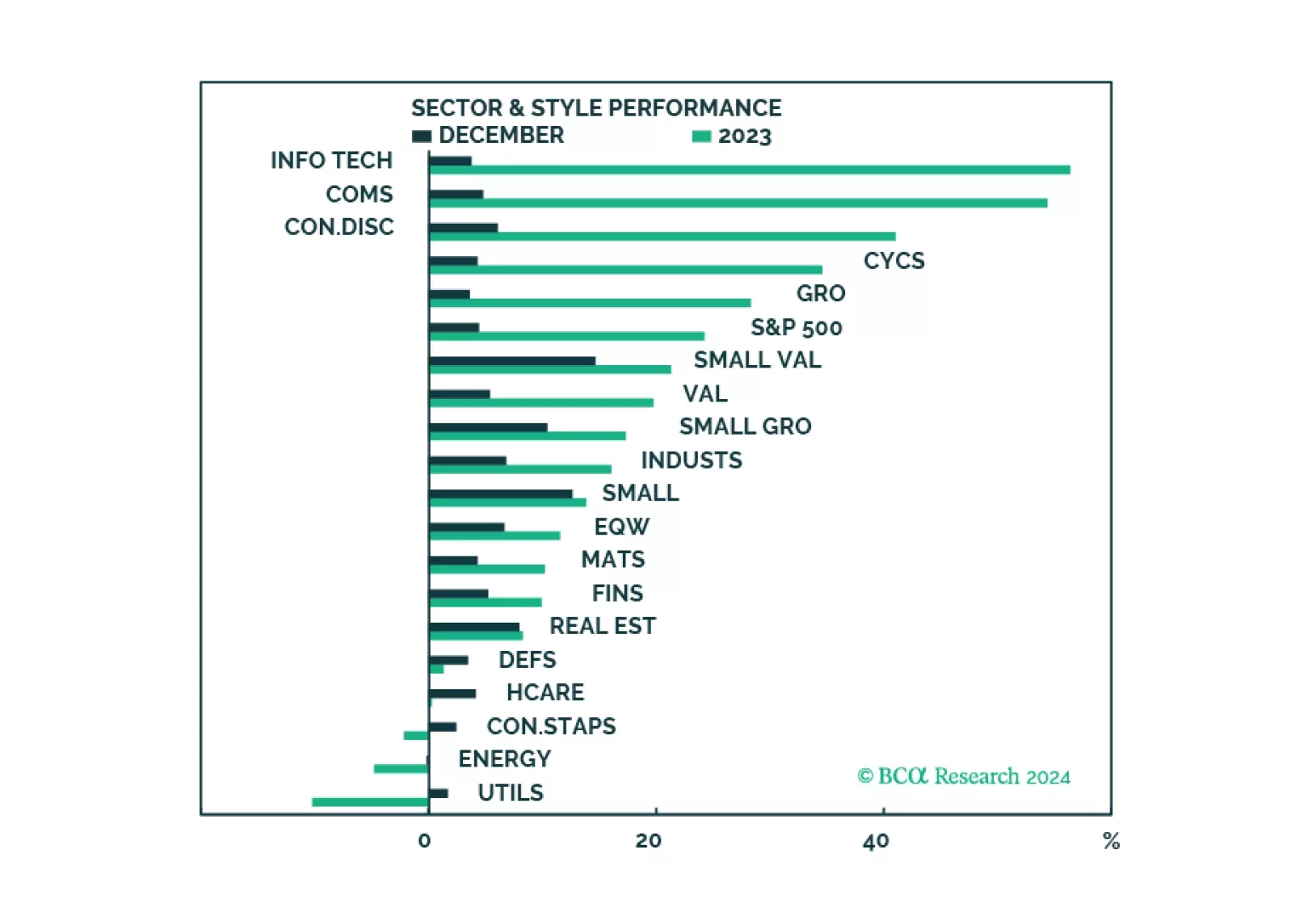

The Santa Claus rally has been fueled by investors optimism about a soft landing which is the least likely macro outcome in 2024. A pullback in the market is imminent as the probability of "too hot" or "too cold" will get priced in. We are downgrading Software and Services on a tactical basis to take profits but maintaining a strategic overweight in the same trade.