United States

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

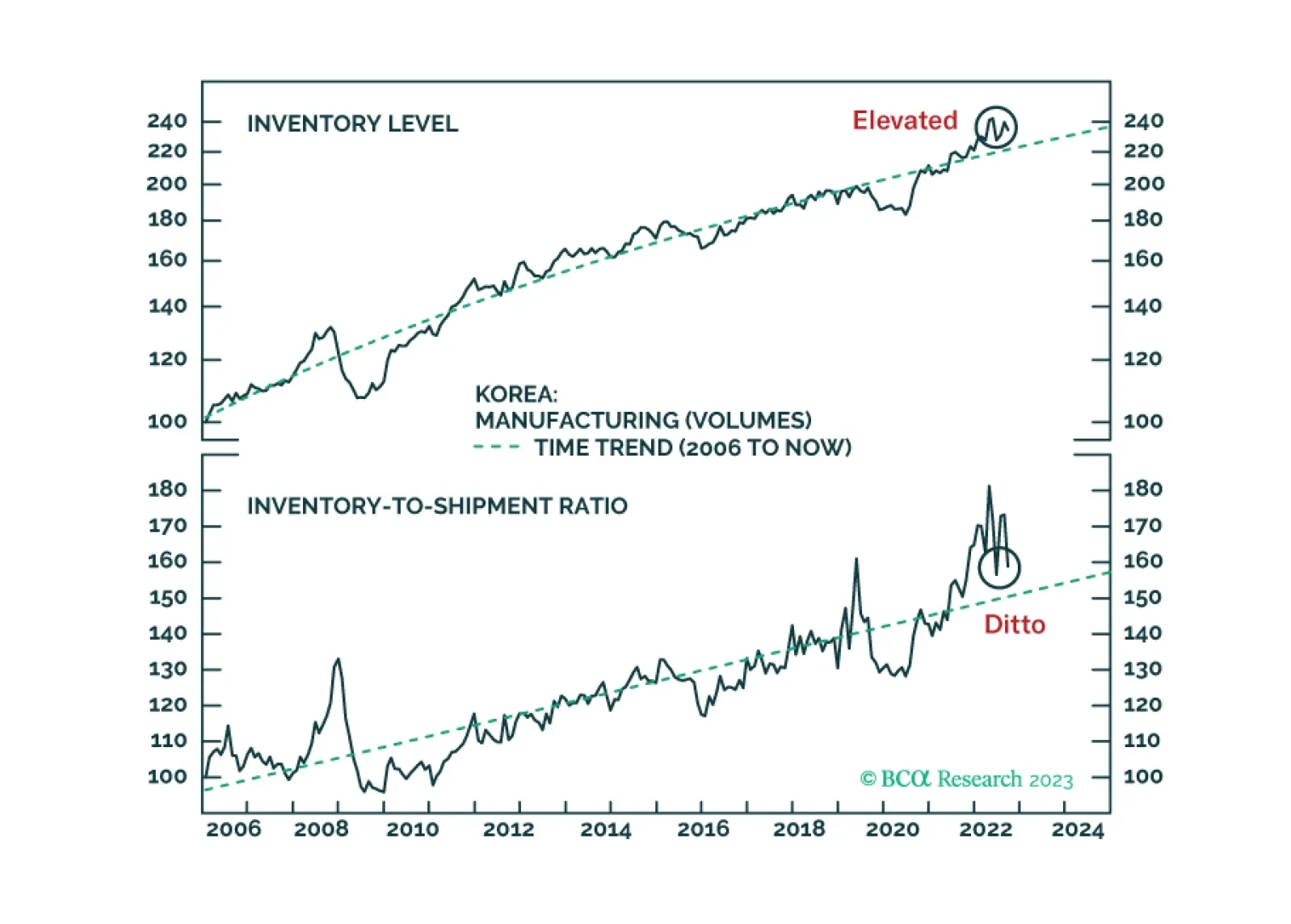

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

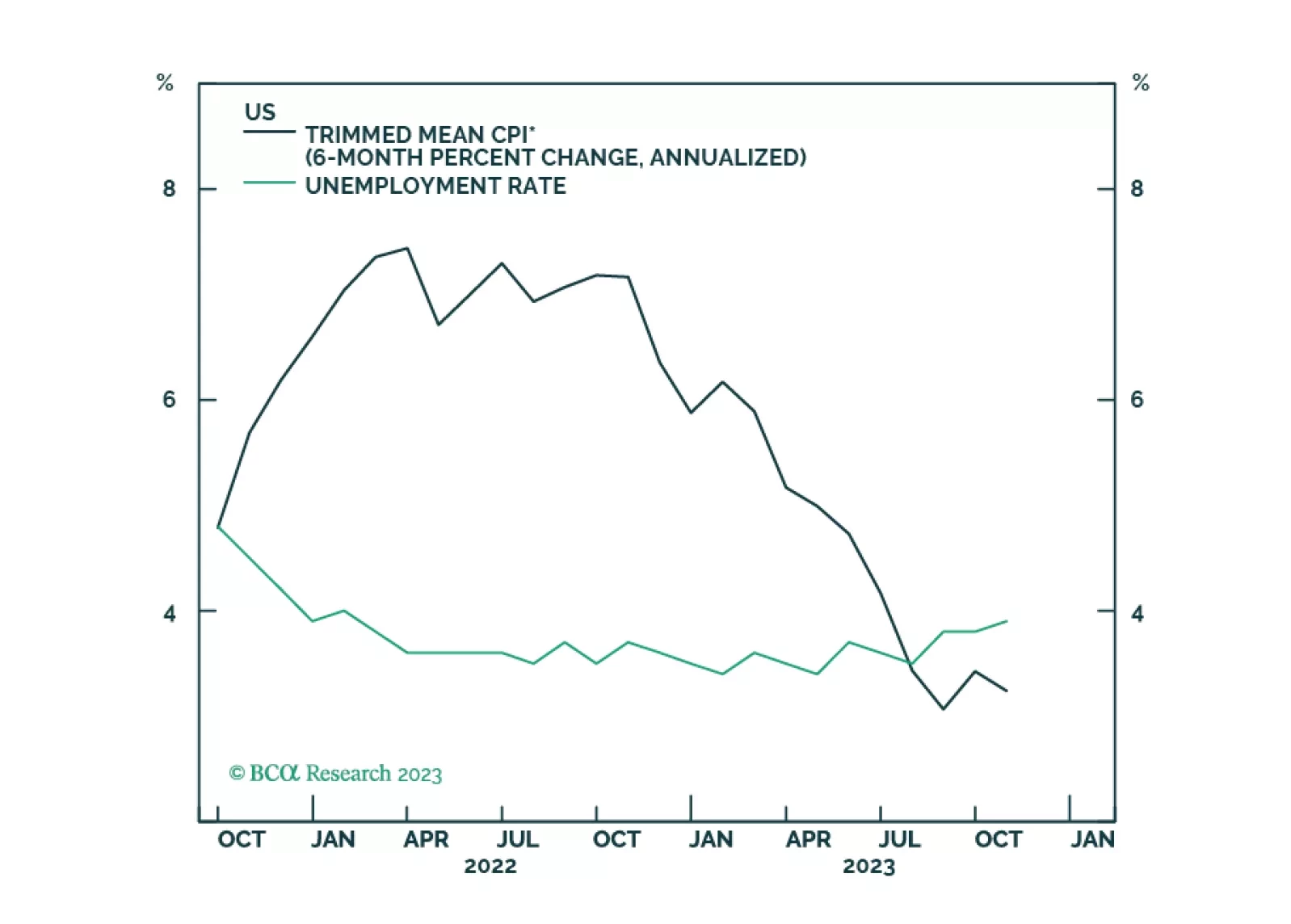

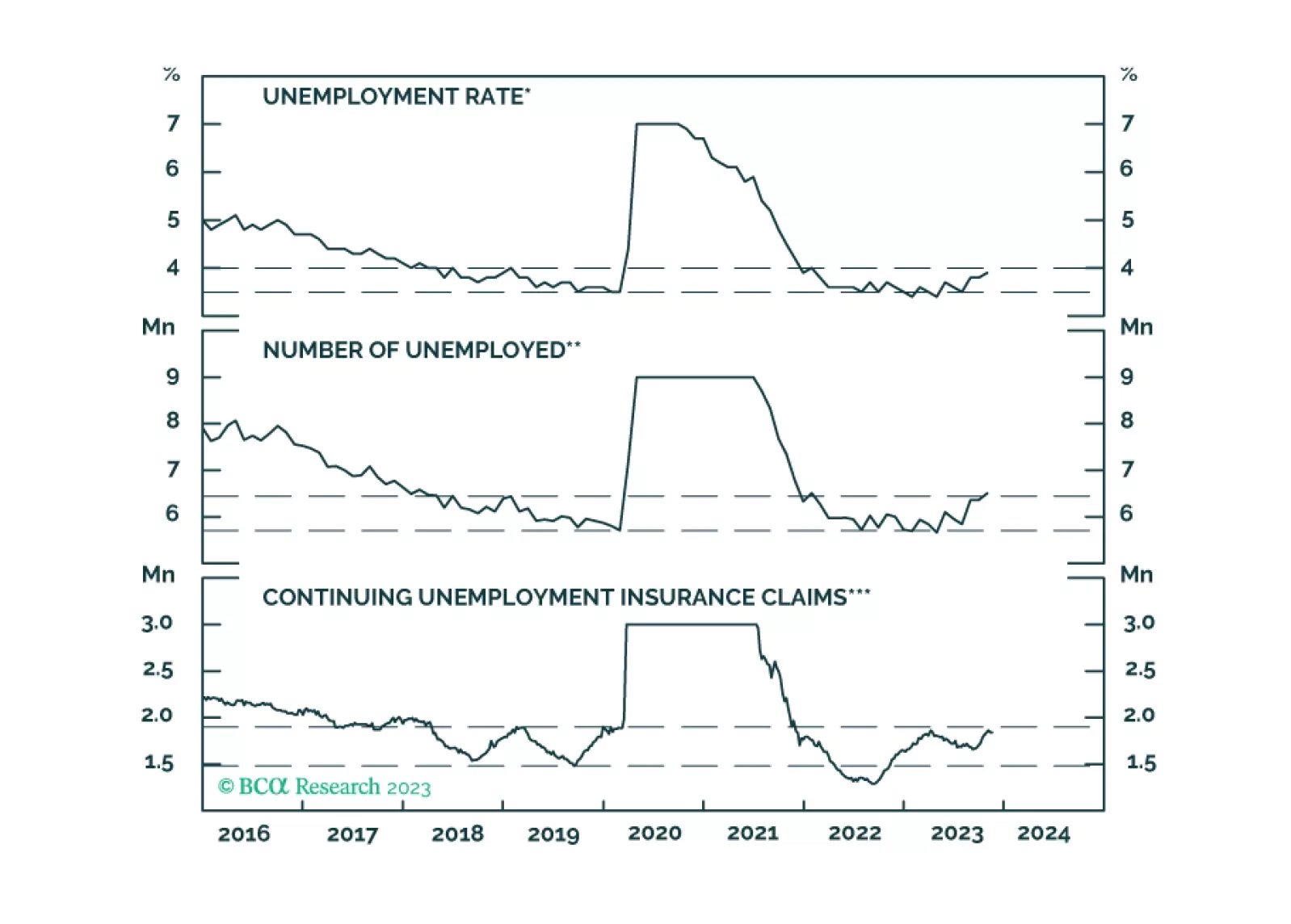

We investigate the recent increase in unemployment with the goal of determining whether it is flagging an imminent US recession.

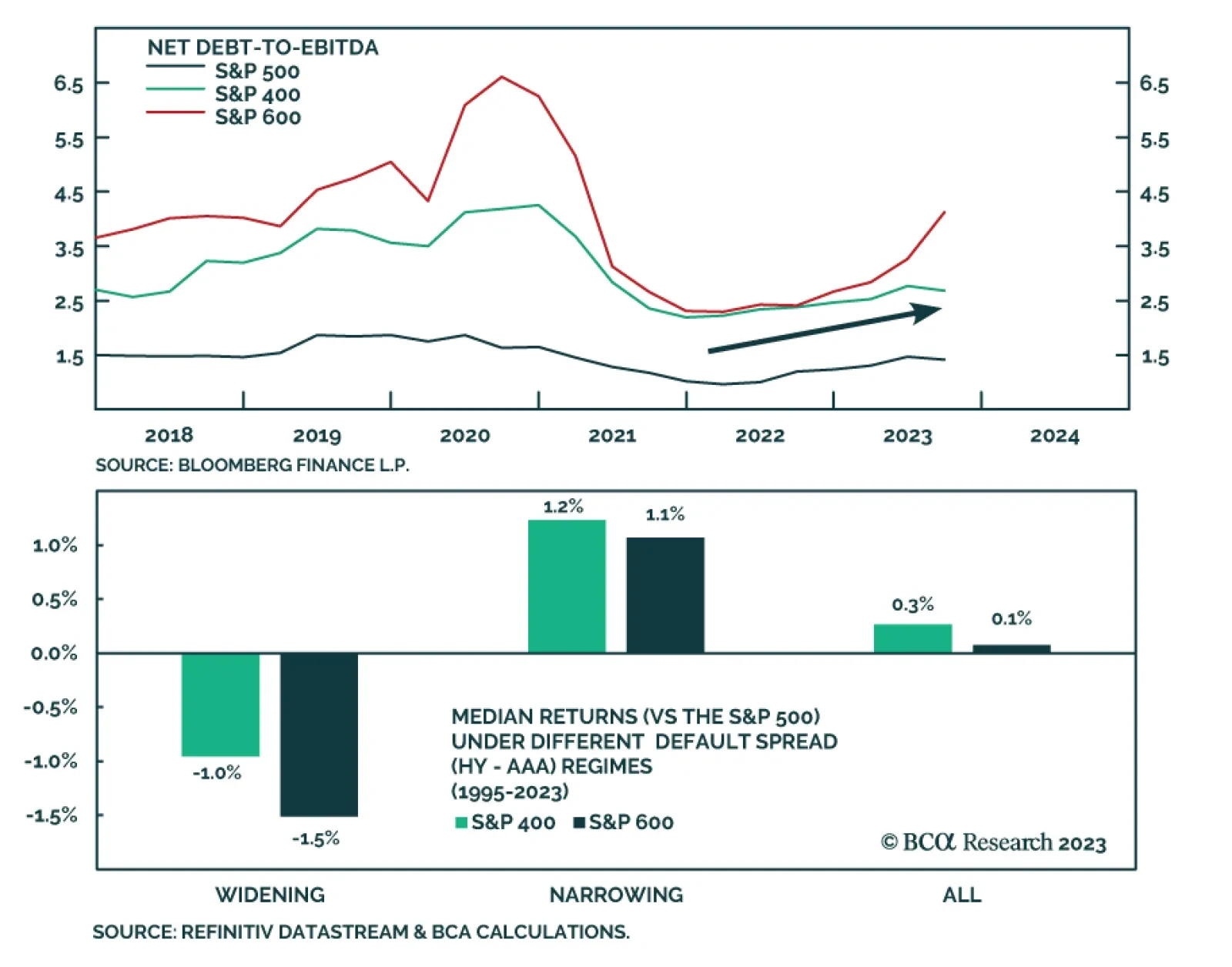

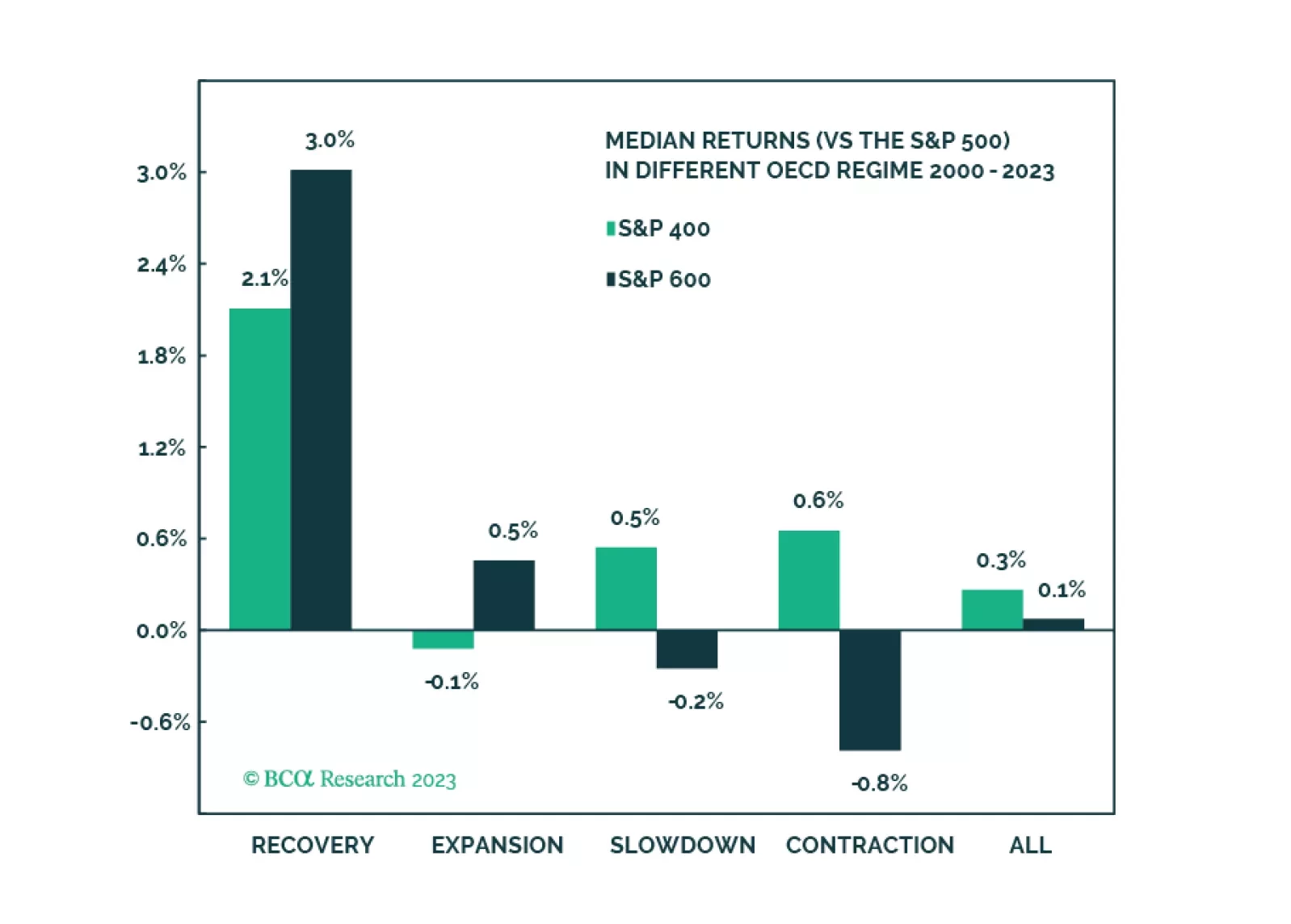

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

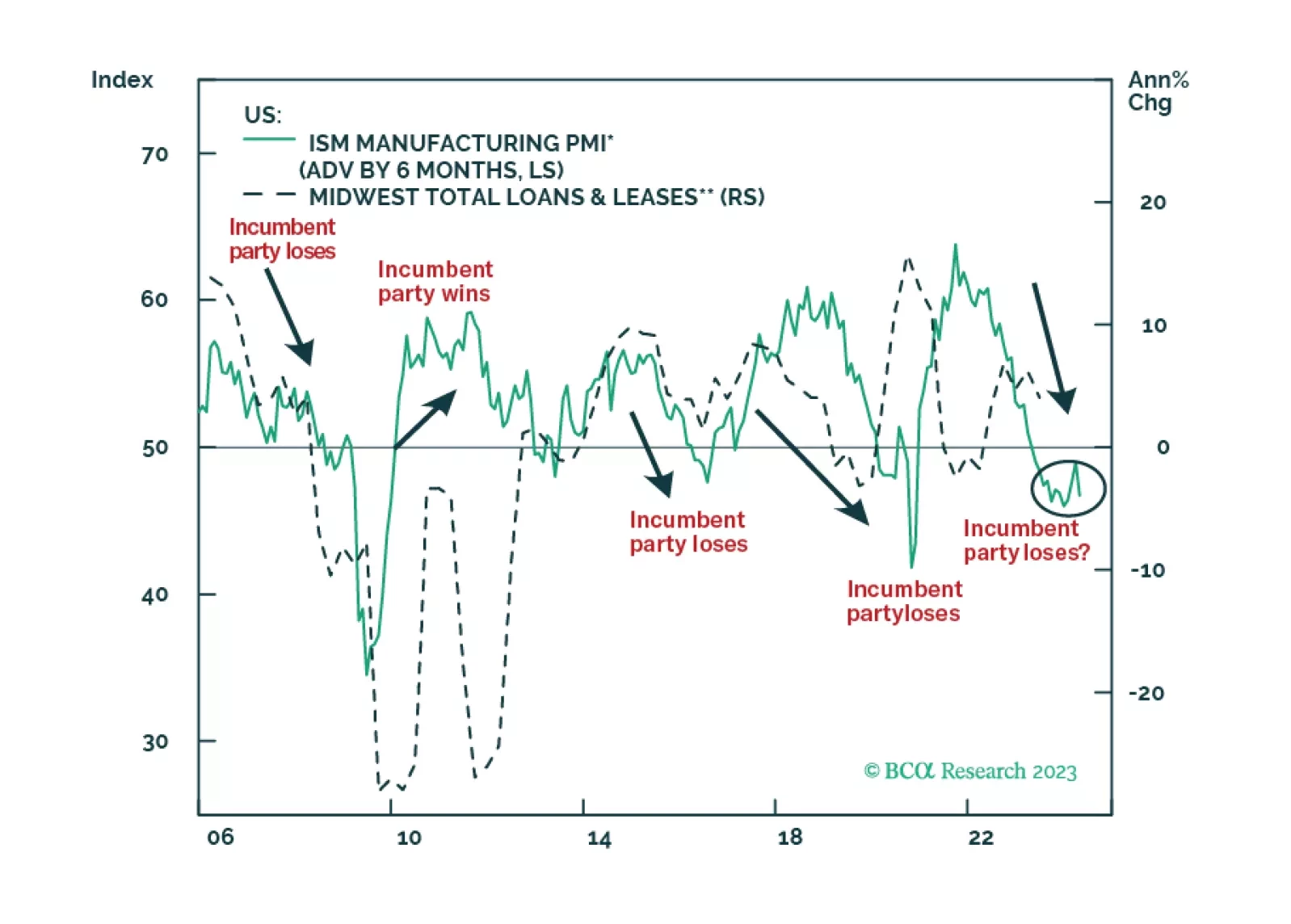

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.