United States

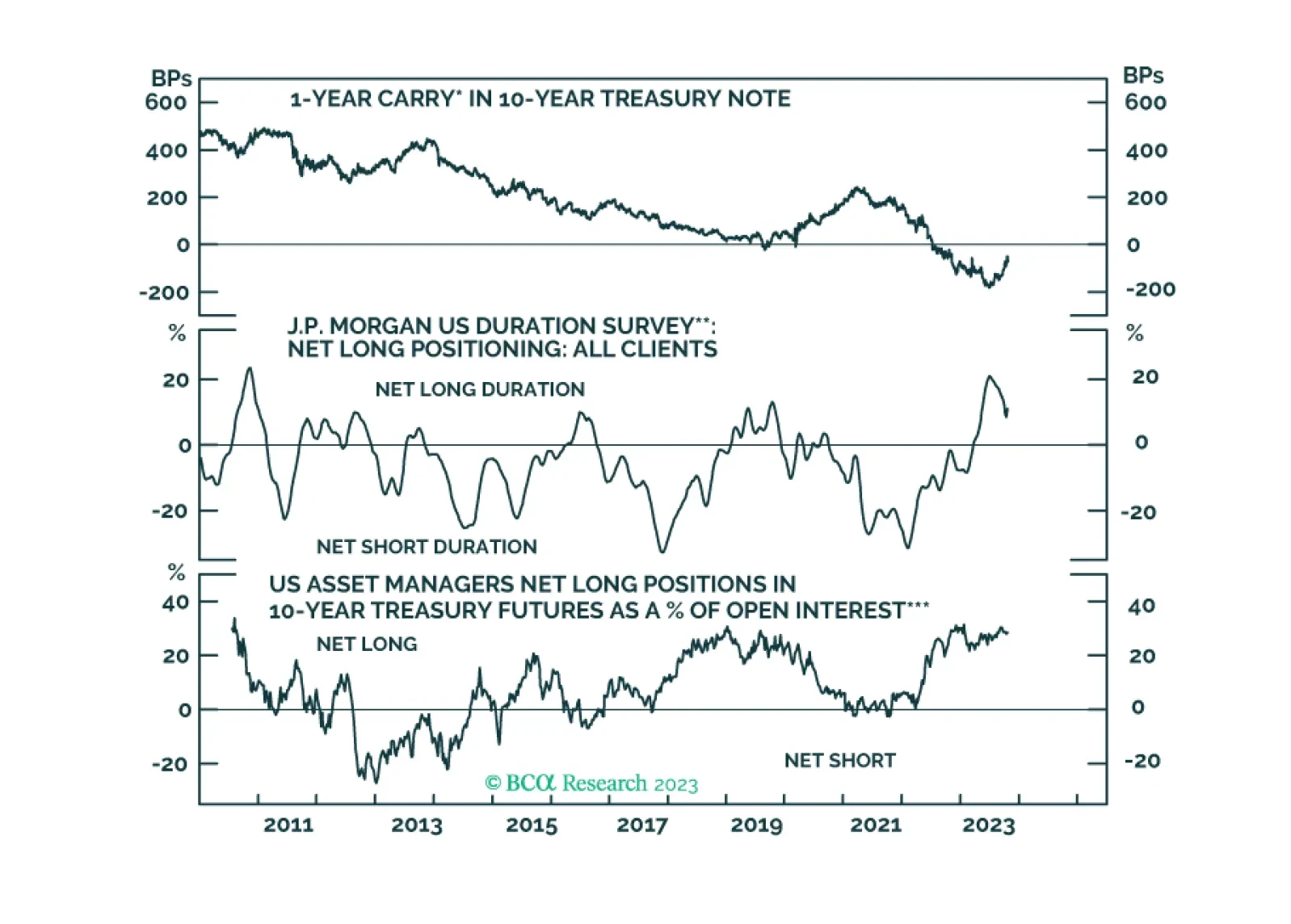

This week’s report contains an update on the Treasury curve’s recent bear-steepening trend and a look at different measures of long-maturity Treasury valuation.

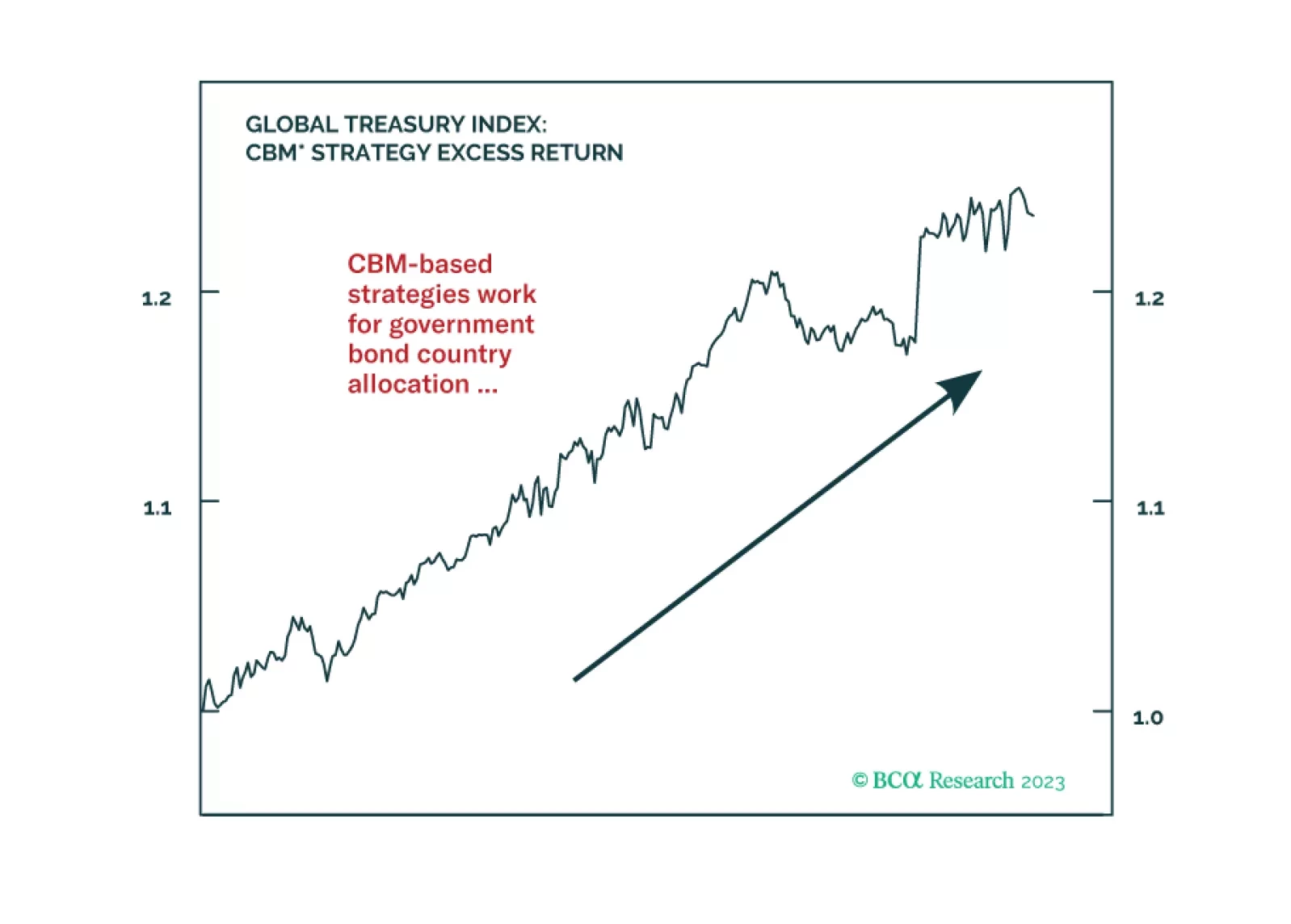

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

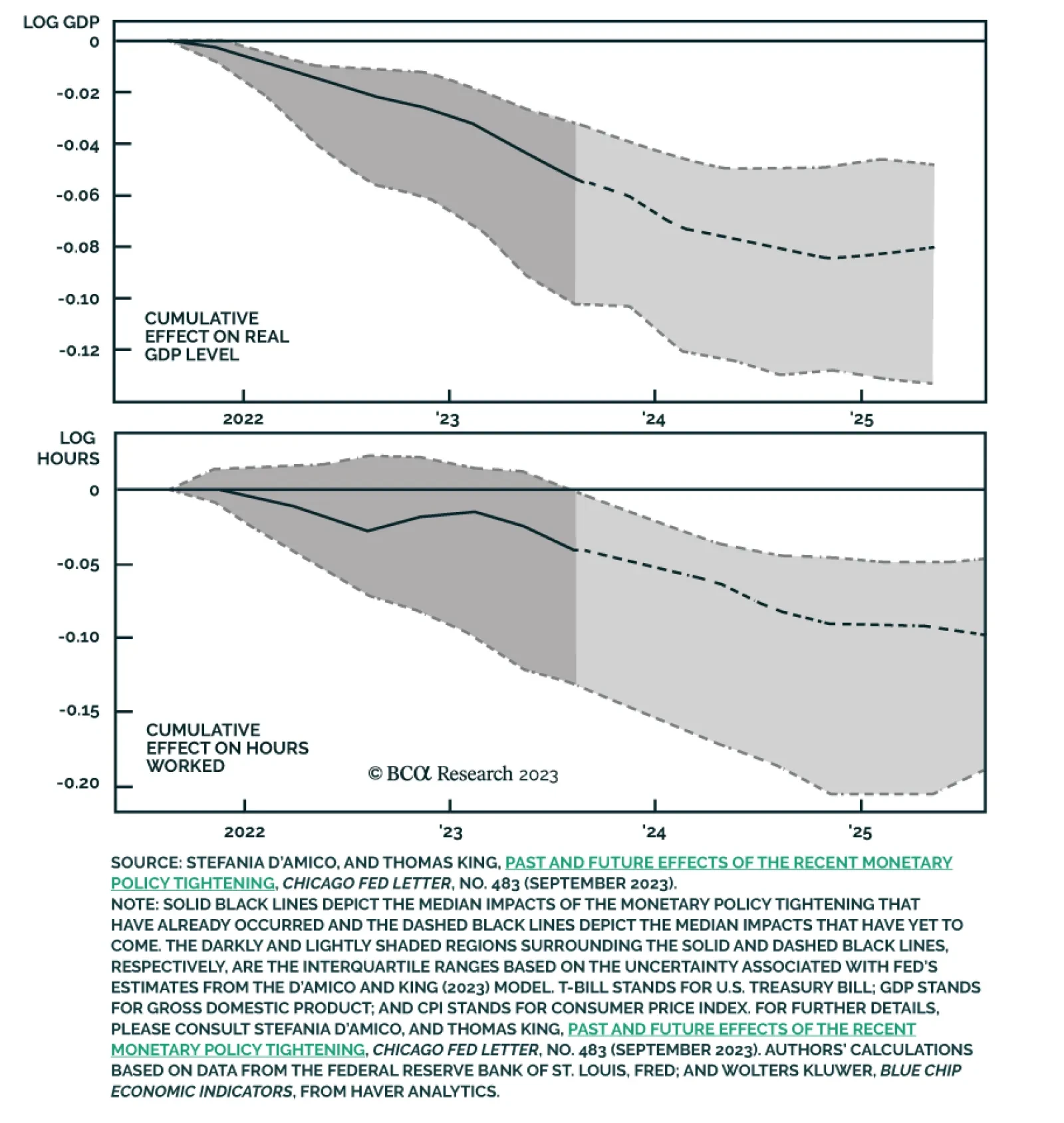

The biggest banks report that consumer credit card delinquencies still have yet to get back to pre-COVID levels and other credit performance indicators, leading and lagging, remain solid. There is still a great deal of cash sloshing around the banking system, though consumption has clearly slowed. We reiterate our view that a recession is coming, but not before the year is out.

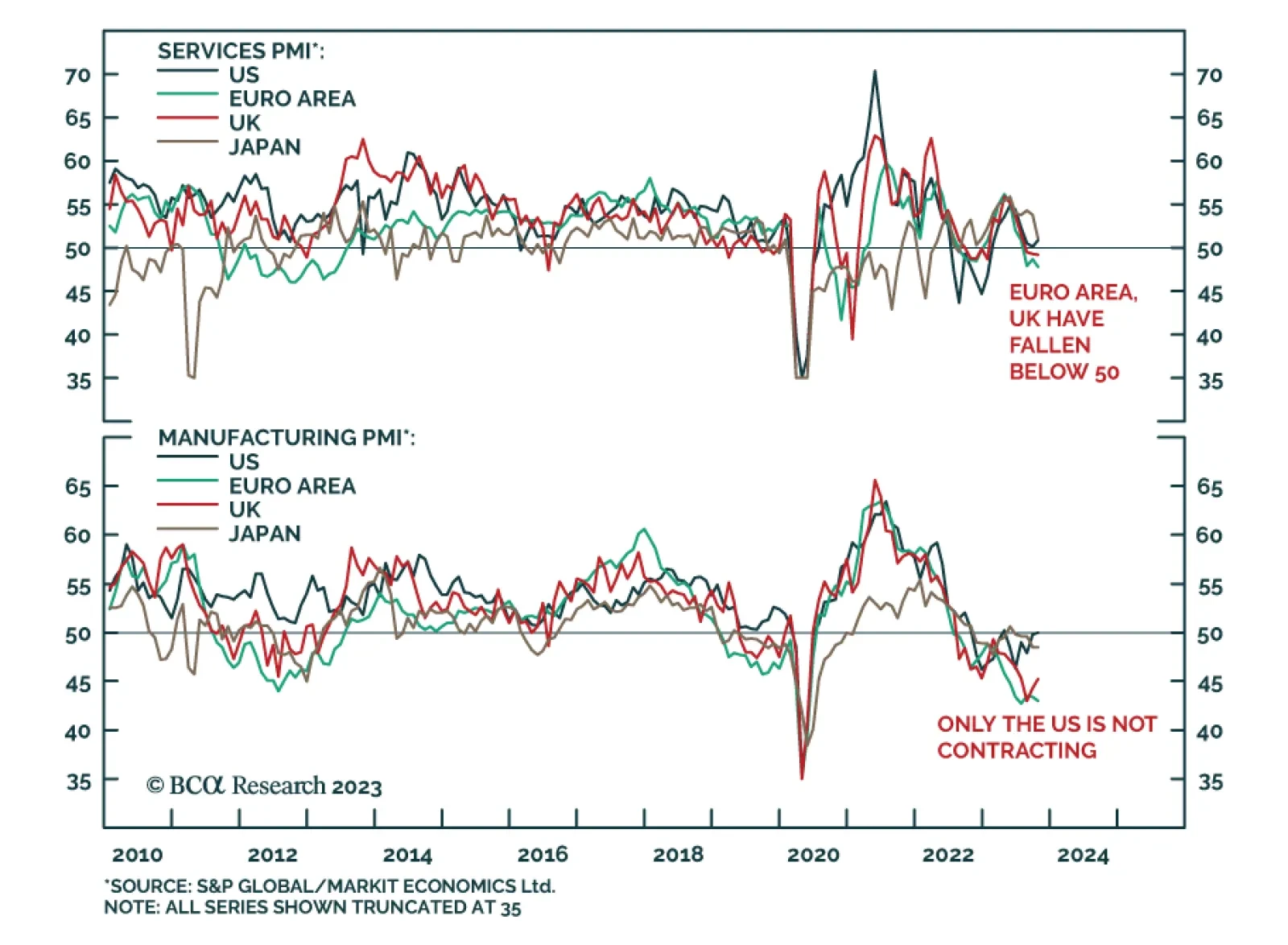

Europe’s weak patch is not about the ECB’s policy tightening, at least not yet. 2024 is another story, and the ECB’s policy will prompt a Eurozone’s recession around the summer.

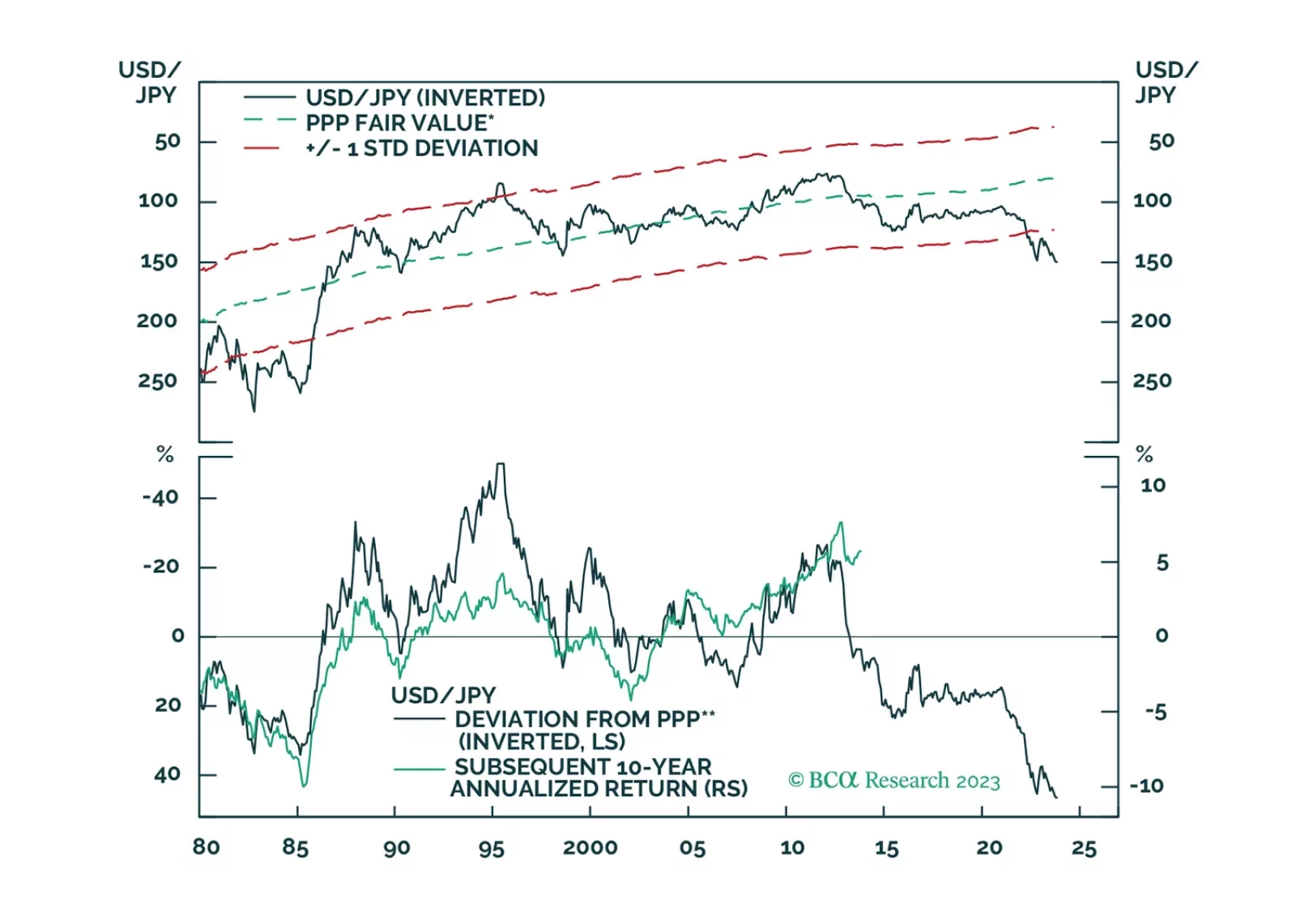

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.