United States

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

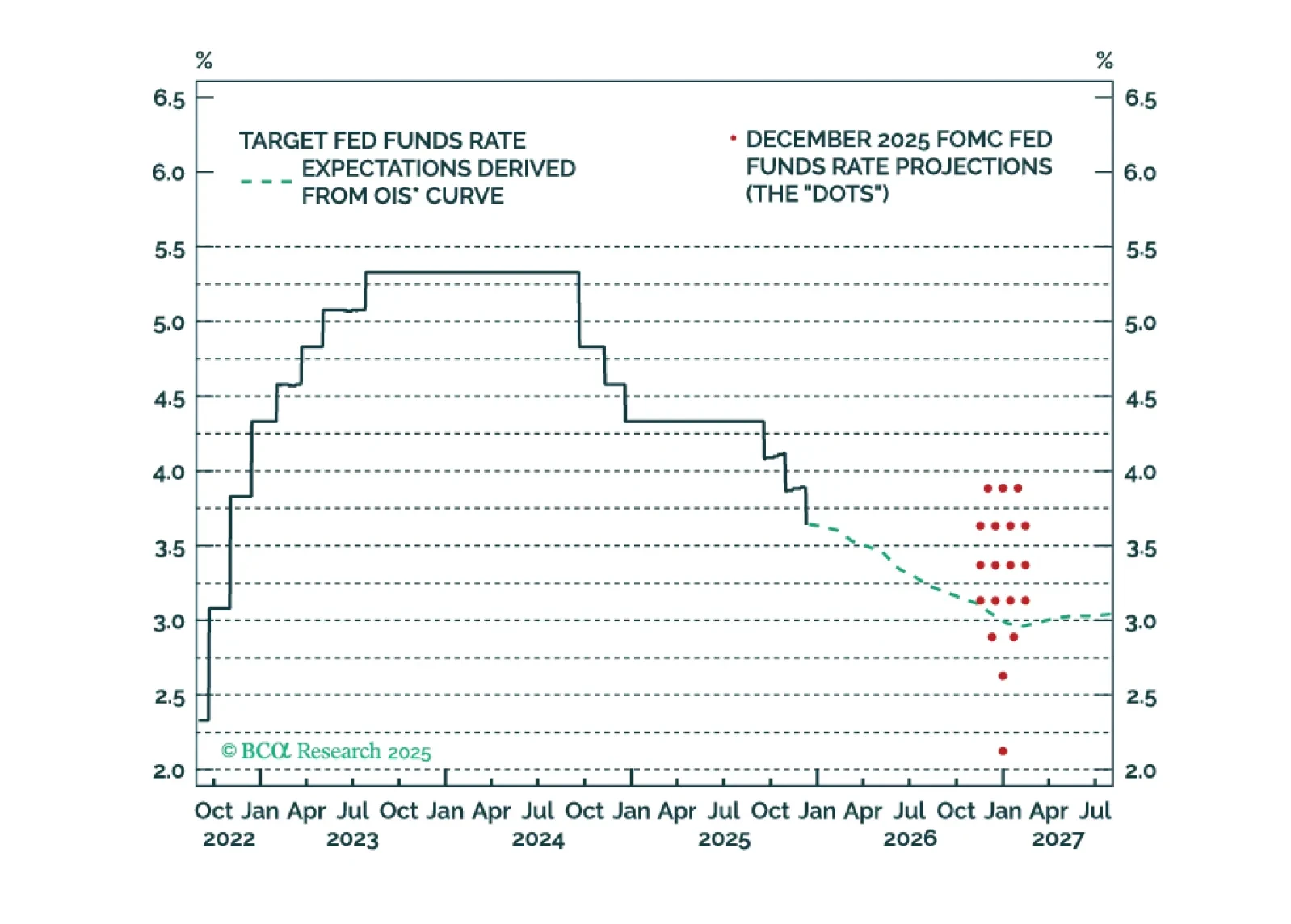

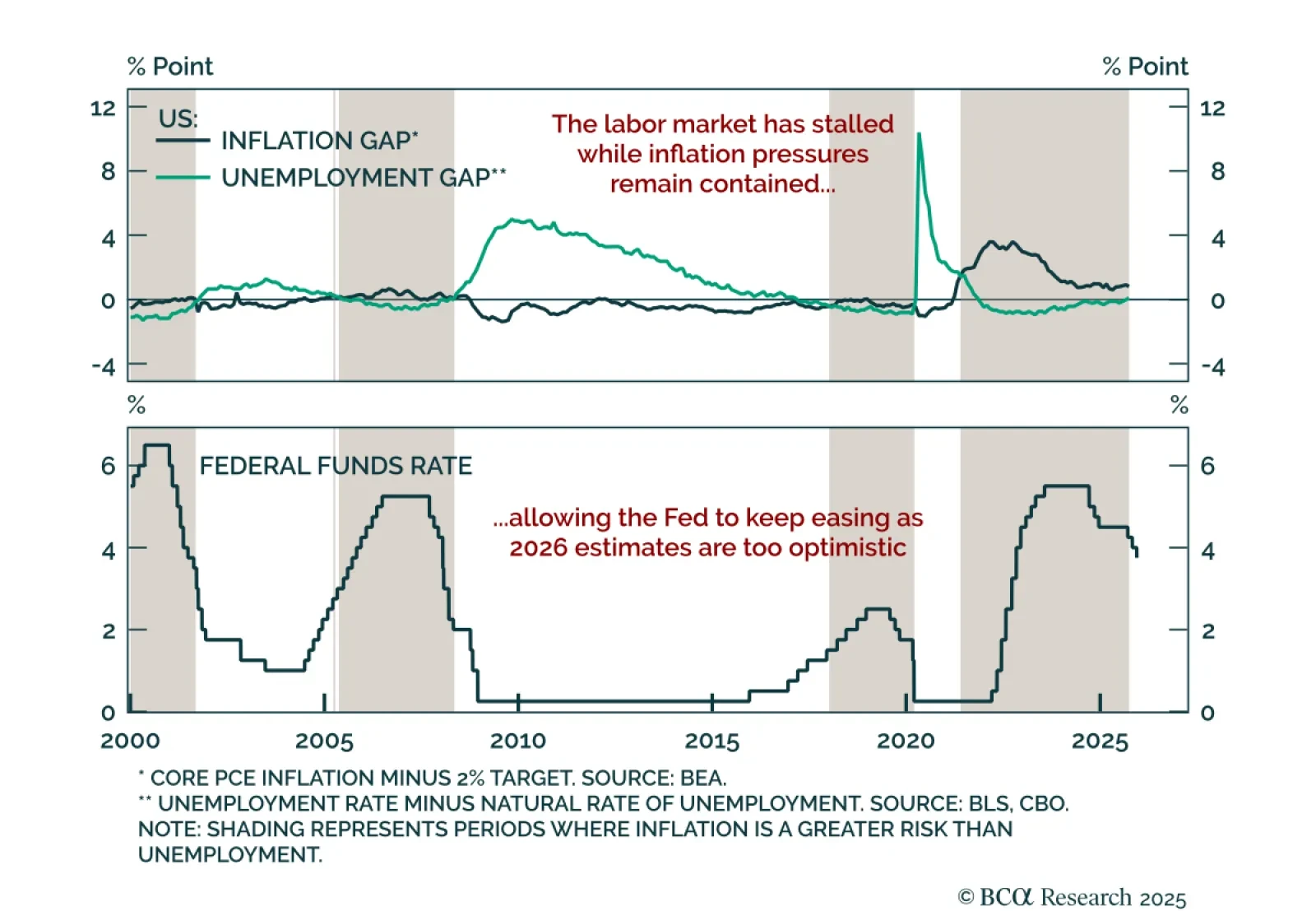

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

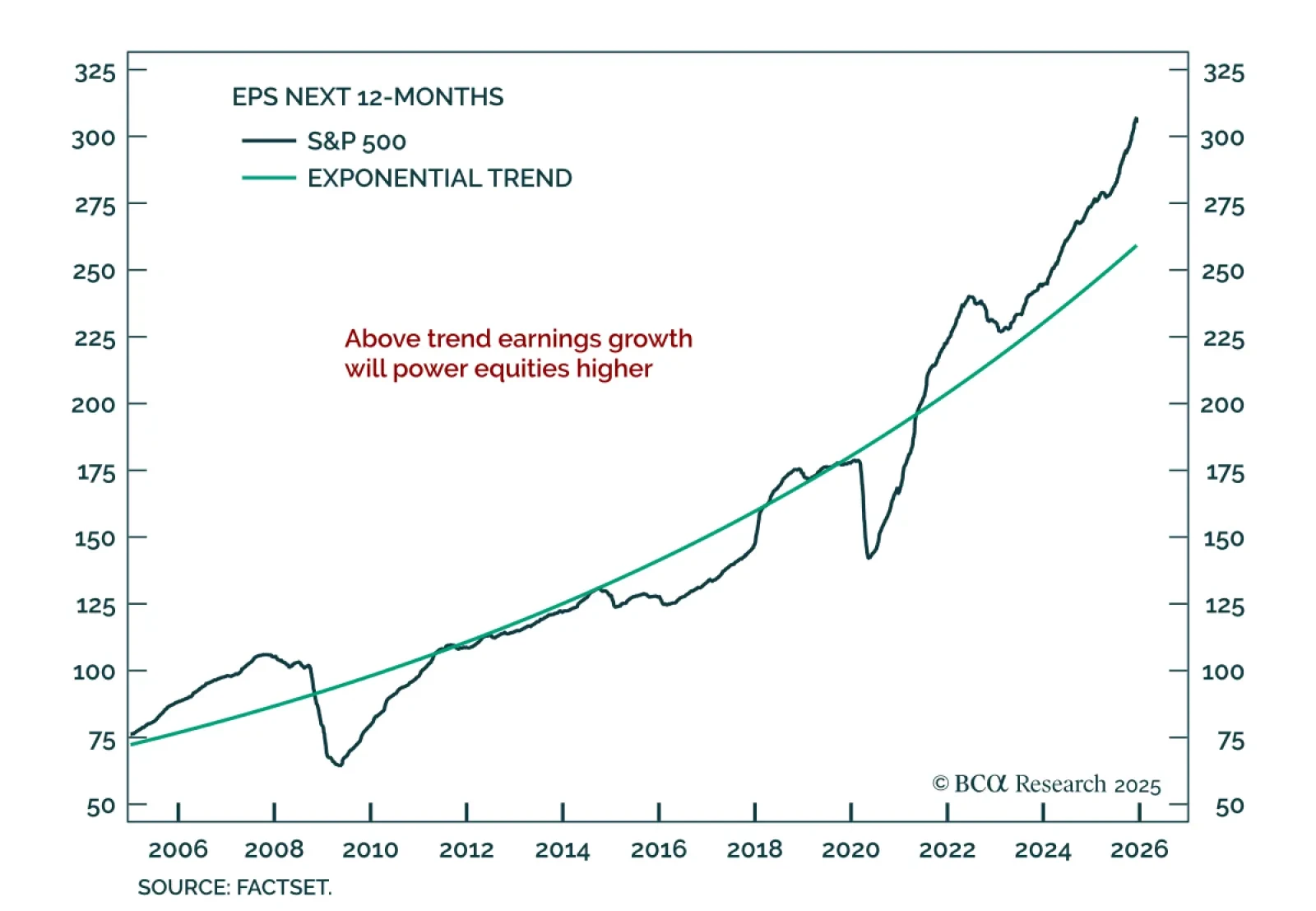

We are constructive on equities in 2026, as monetary easing, fiscal support, GenAI-related capex, and strong earnings growth are unequivocally positive for the asset class. Valuations are extended, but concerns about a bubble are overstated. Despite the favorable backdrop, we expect the S&P 500 to return only 5–10%, ending 2026 between 7,200 and 7,500.