United States

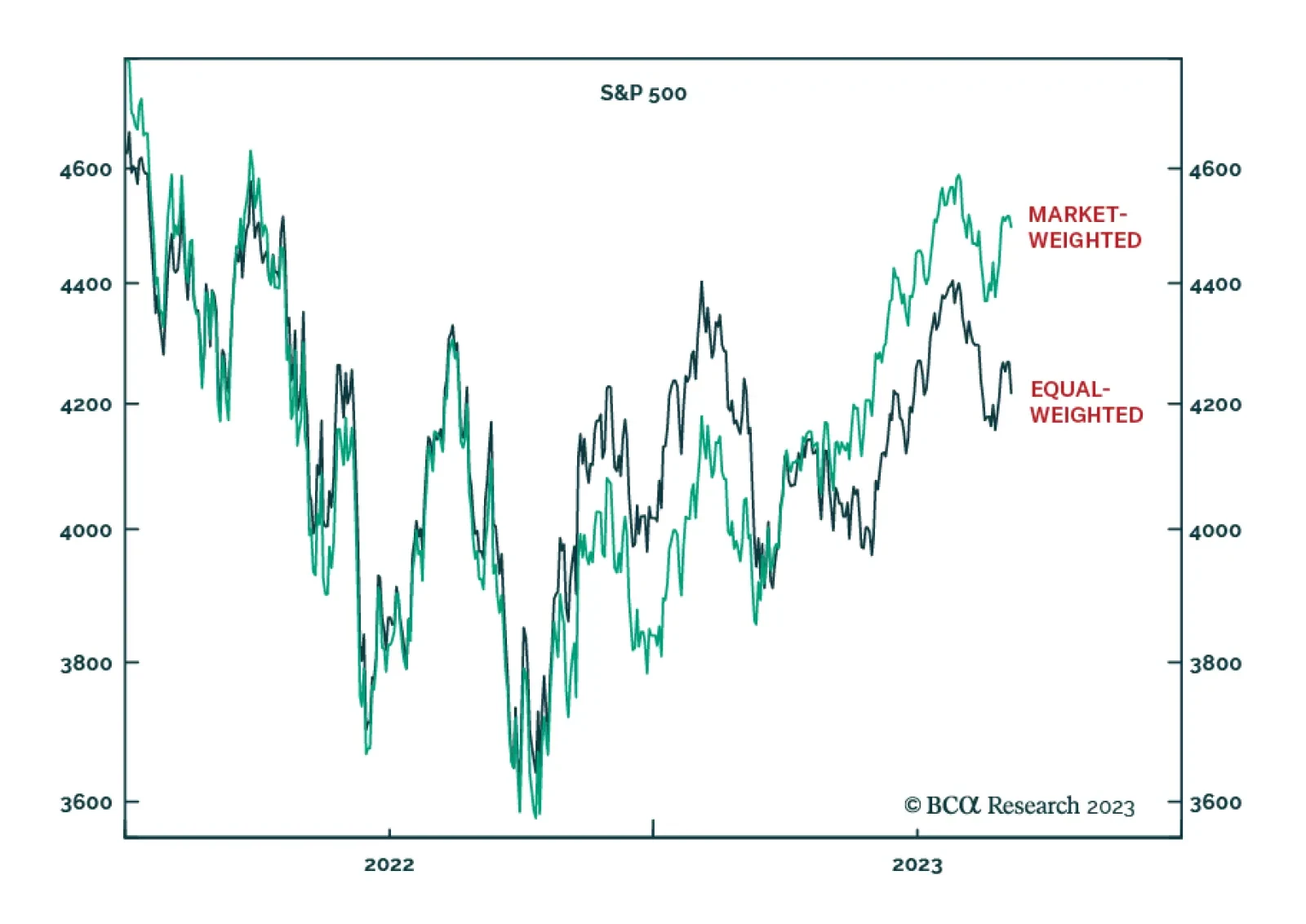

The broader rally that started in June is premised on a Goldilocks narrative that will prove to be a fairy tale. Either by stubborn inflation. Or, by higher unemployment that shows that the war on inflation is far from costless. Or, by both. We discuss the implications for stocks and bonds. And we reveal our new top long dollar cross.

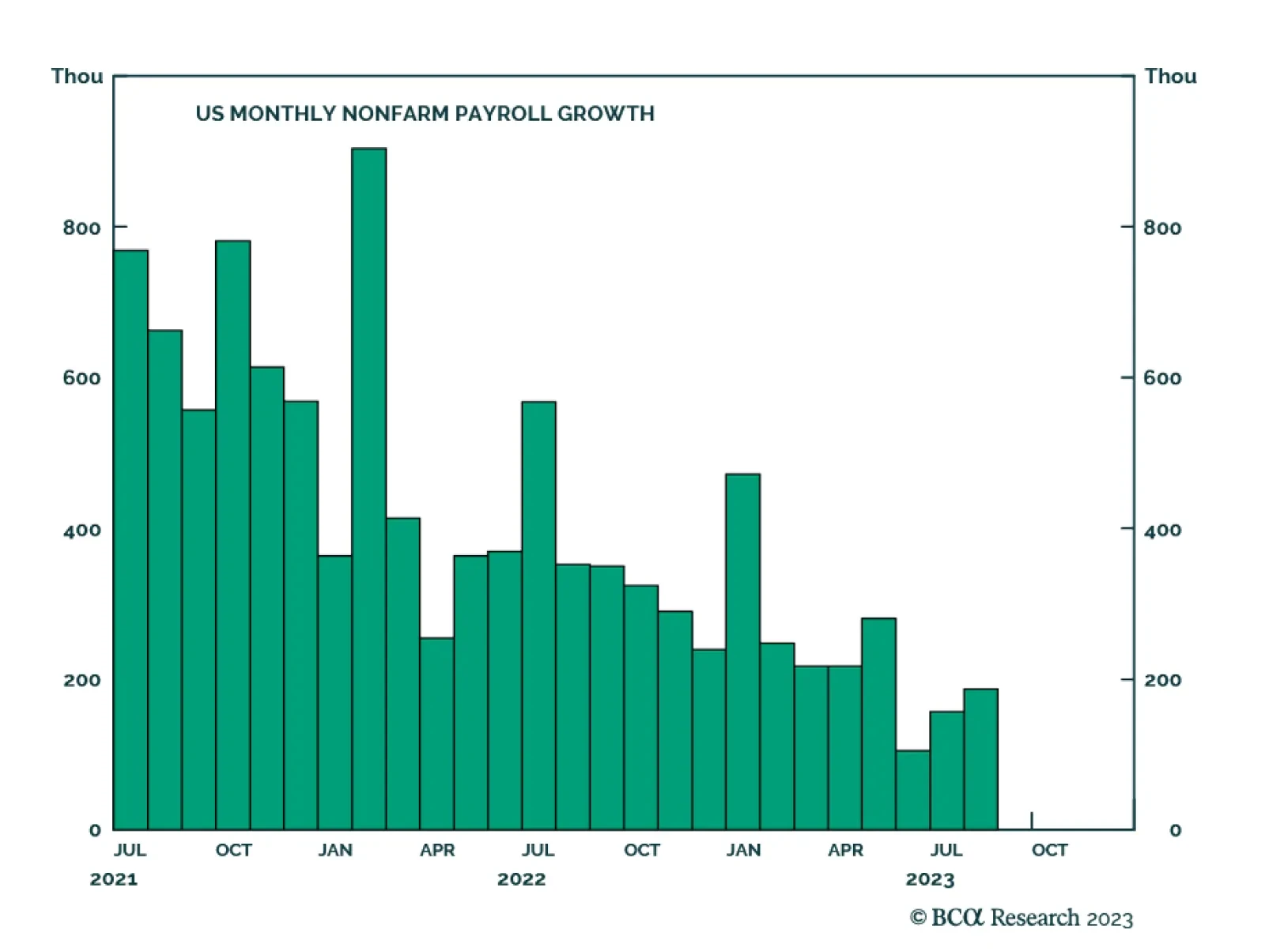

The resiliency of consumers through 2023 has surprised investors. However, consumer strength will fade into yearend as factors supporting growth in income and spending are waning. i.e., job gains are slowing, wage growth is decelerating, and excess savings are running out. Consumers are starting to feel the pressure from tighter monetary policy as financial obligations rise. Hence, as consumer spending decelerates, economic growth will slow into yearend. We confirm our underweight of the Consumer Discretionary sector.

US bond investment takeaways from this week’s PCE and employment releases.

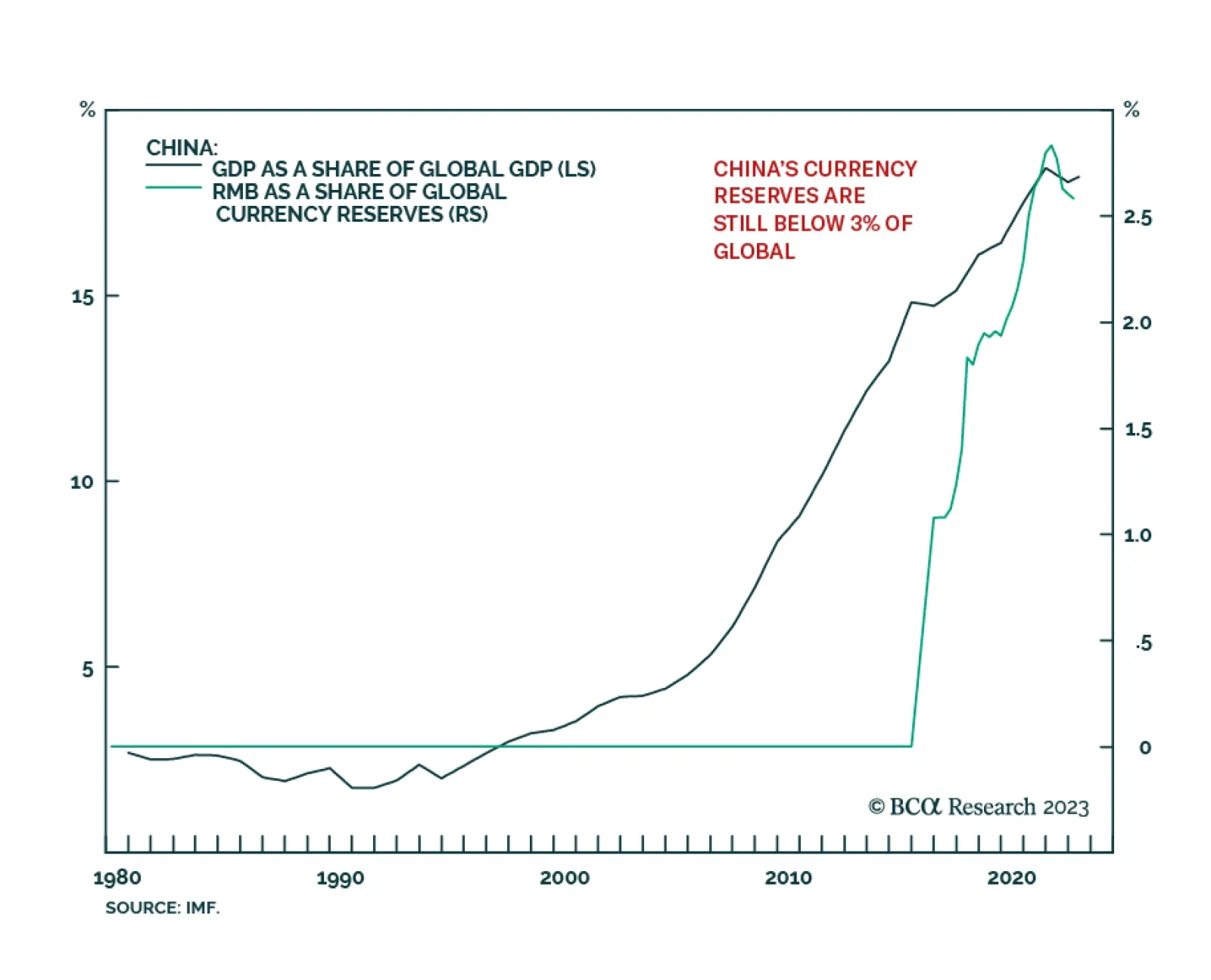

In this report, we explore what a new BRICS+ union means for the dollar over the next 6-to-9 months.

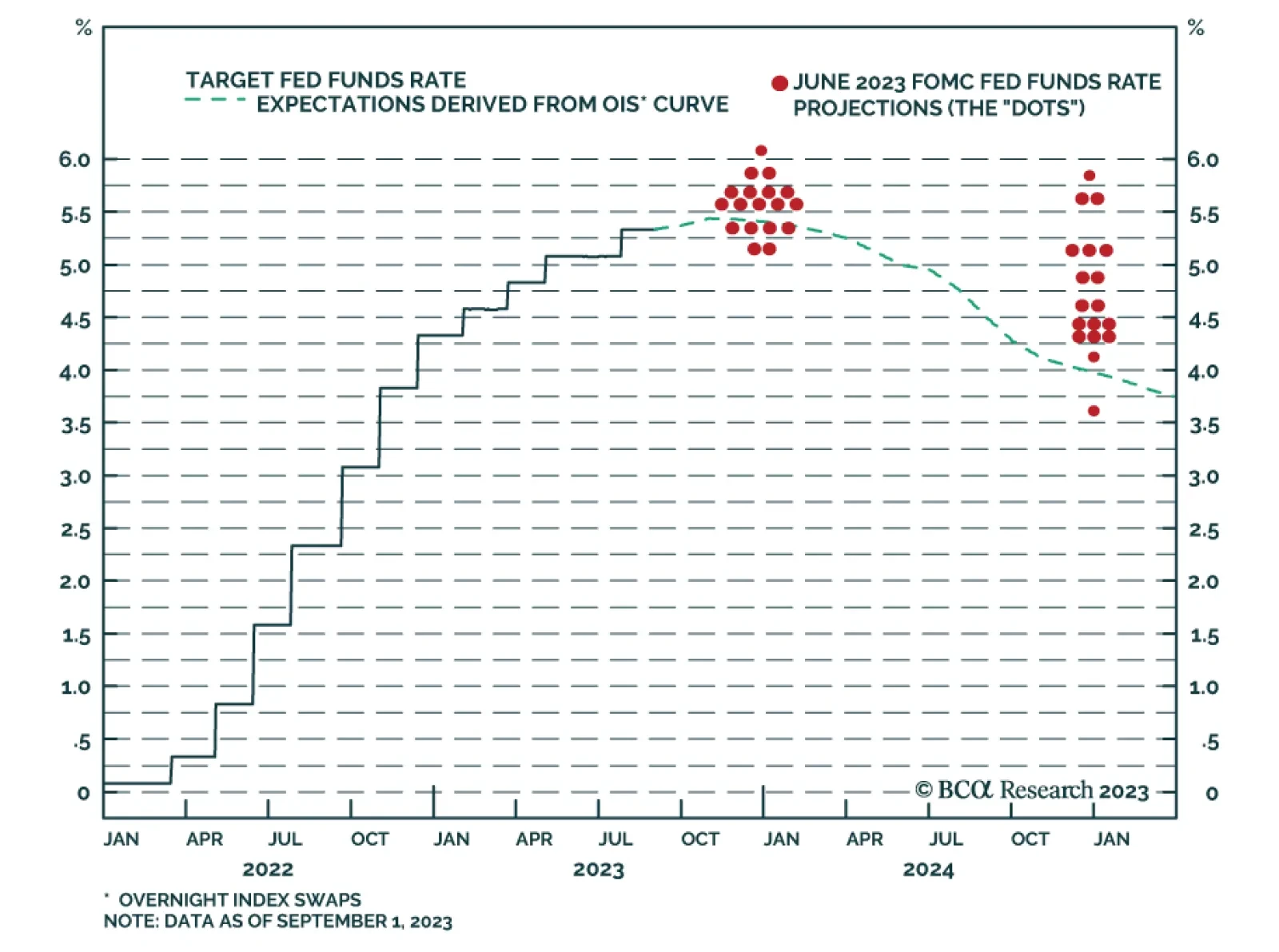

A global recession continues to be likely over the next 12 months. The impact of tighter monetary policy is slowly being felt. Government bonds look increasingly attractive as a safe haven.