United States

Our US and Geopolitical strategists delivered accurate calls on Trump’s tariff shock and Israel’s strike on Iran in 2025 but missed the China equity rally and overestimated near-term prospects for a Ukraine ceasefire. Their 2025 outlook correctly anticipated…

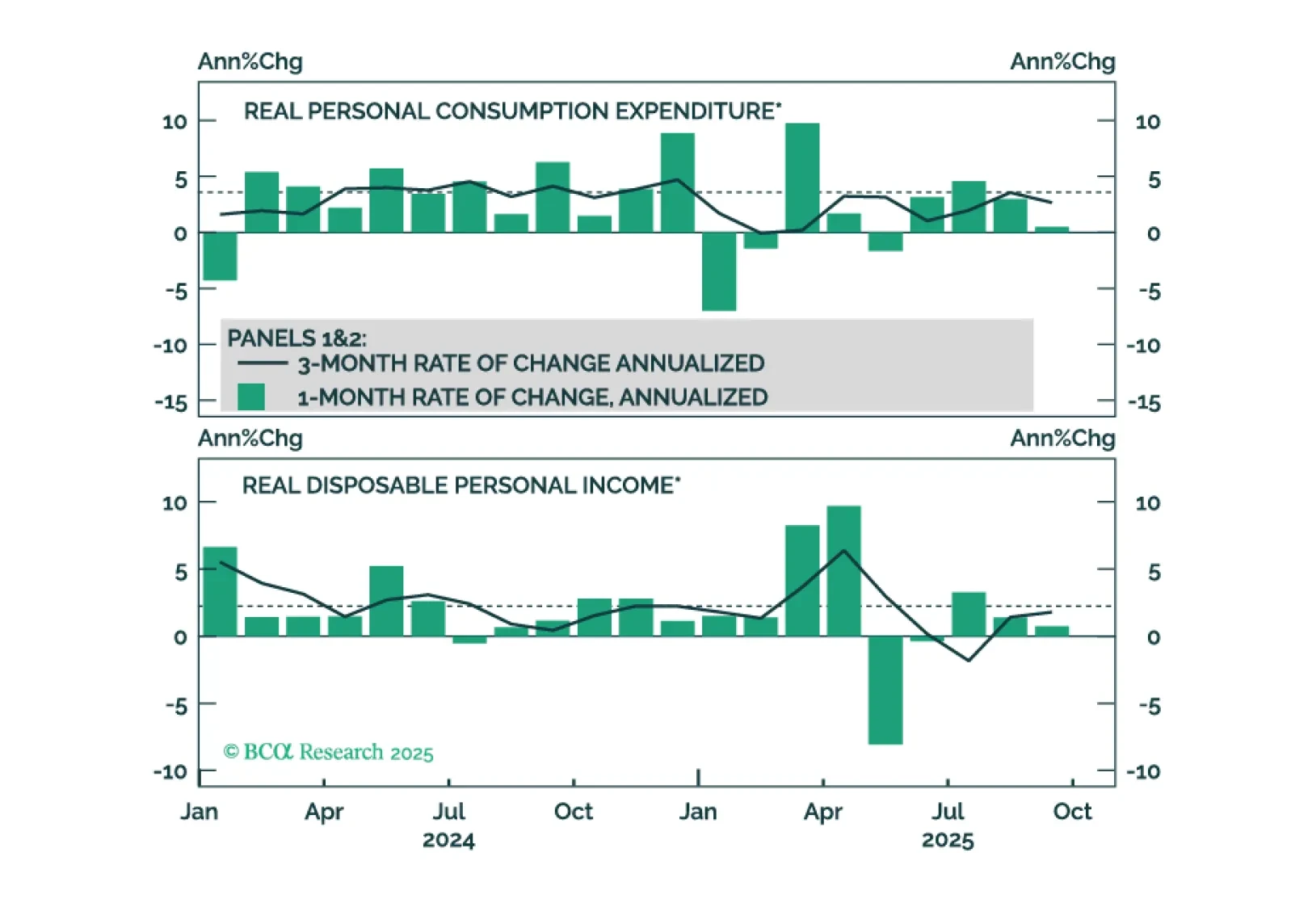

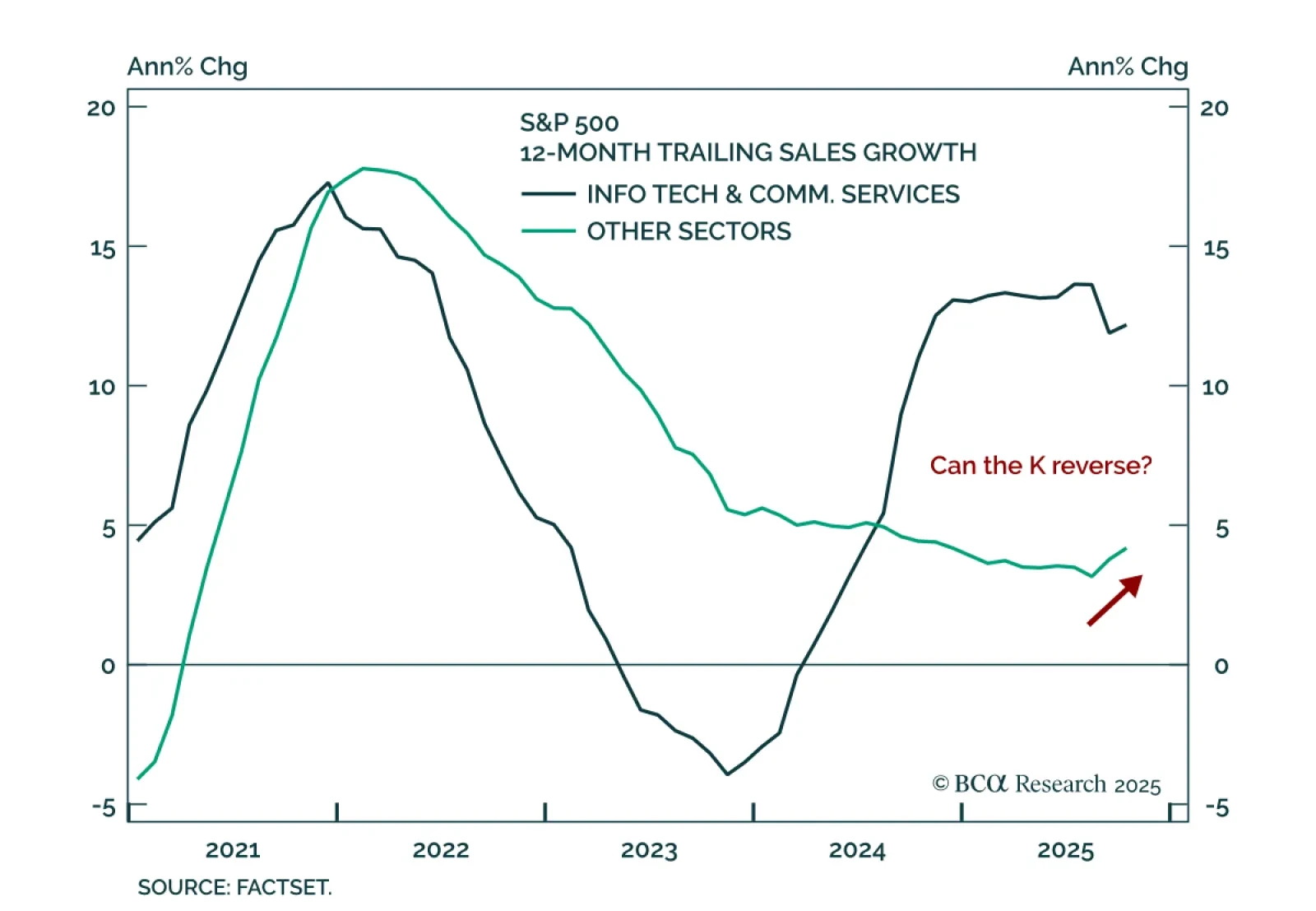

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

Our Portfolio Allocation Summary for December 2025.

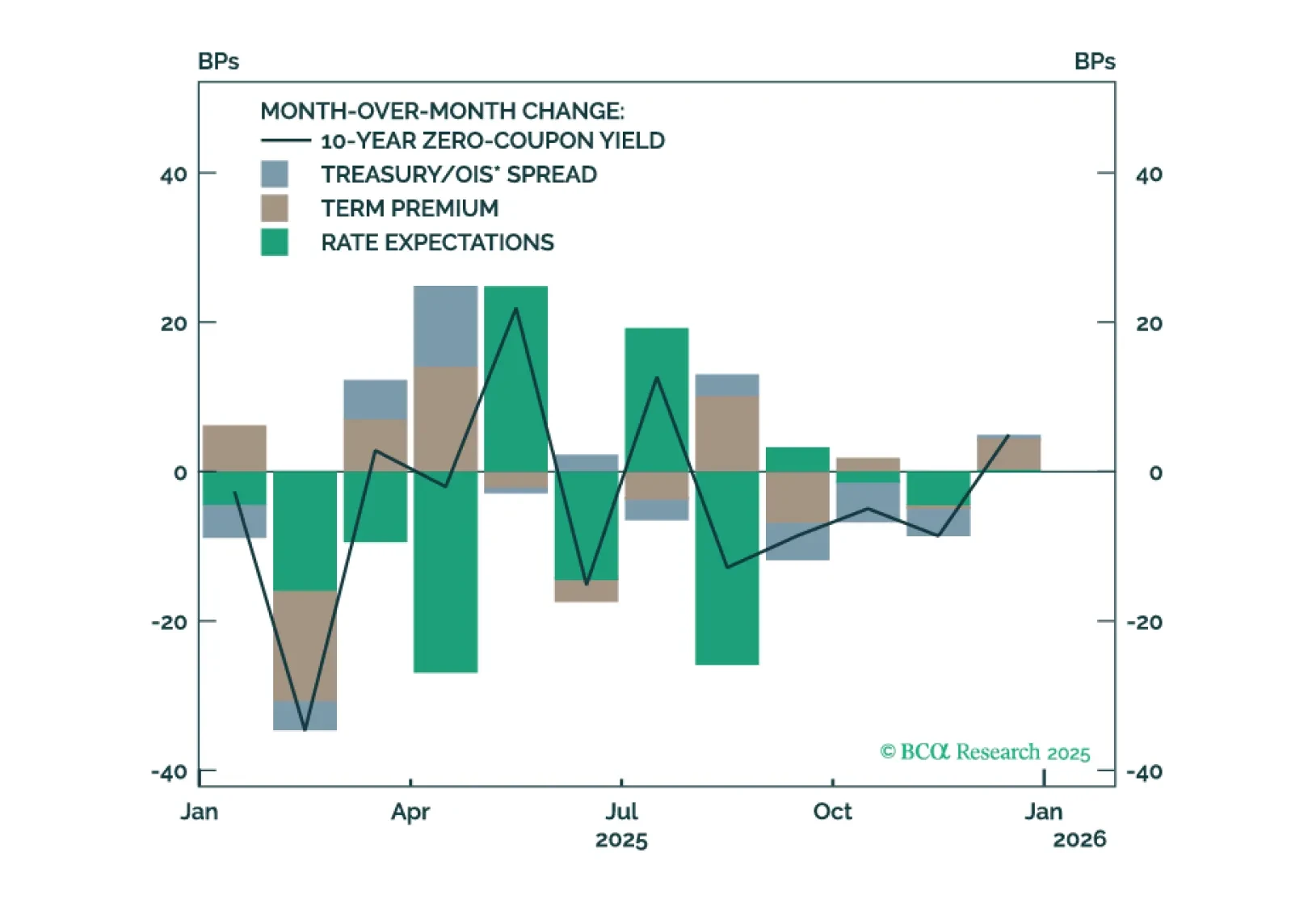

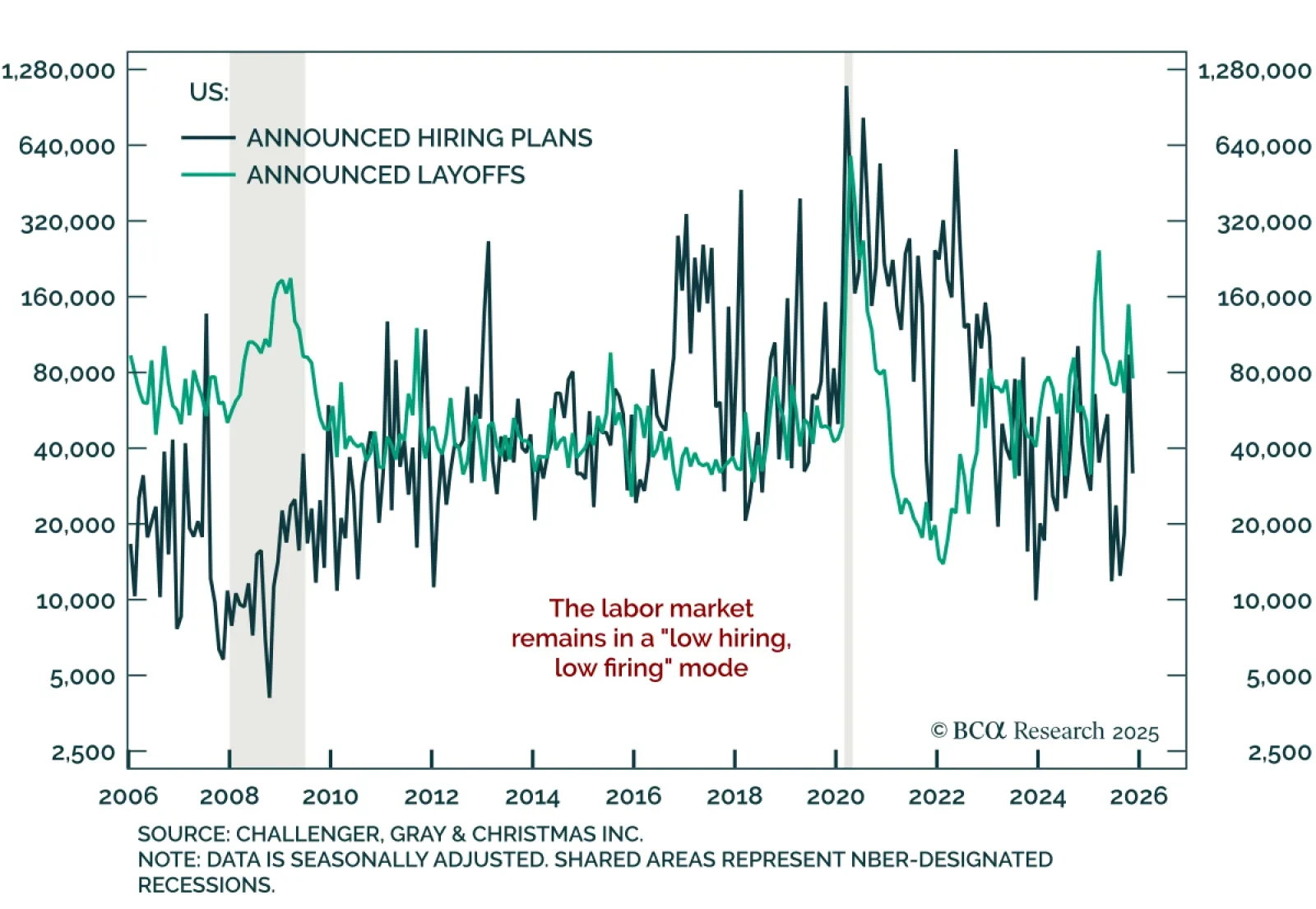

Stay overweight duration and favor curve steepeners as a stalled labor market and fading inflation pressures argue for more Fed easing than priced next year. The November Challenger report beat estimates, showing a 23.5% y/y rise in layoff announcements, down…

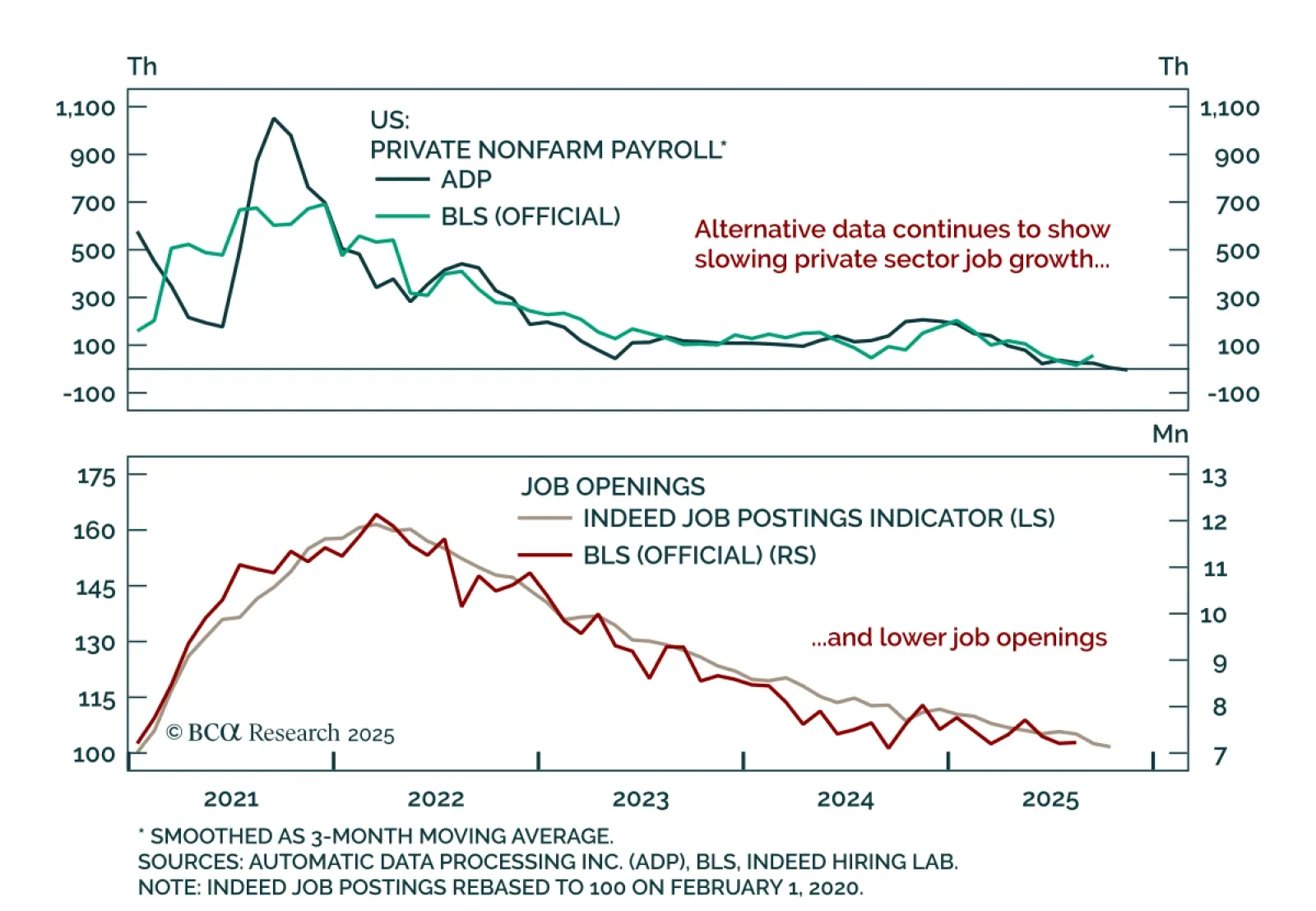

Stay long duration and favor curve steepeners as weakening ADP data reinforce rising labor-market risks and the case for further Fed cuts. The November ADP report missed estimates, showing a loss of 32k jobs after a 47k gain in October. Only 40% of industries…

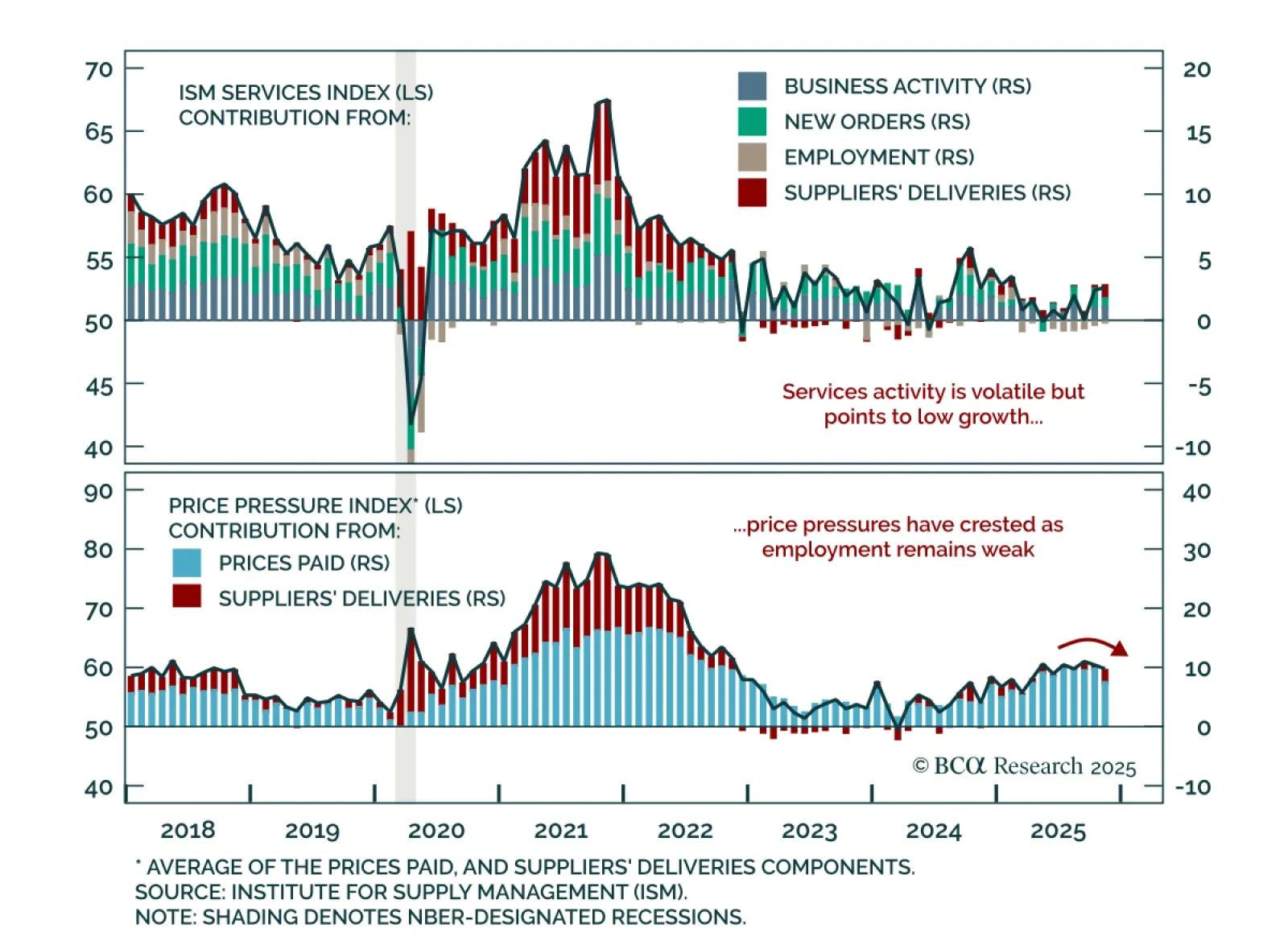

Maintain a neutral equity stance as cresting services inflation and weak employment temper right-tail risks. The November ISM Services PMI beat estimates at 52.6, up from 52.4, but the details were mixed. New orders fell to 52.9 from 56.2, but are still…

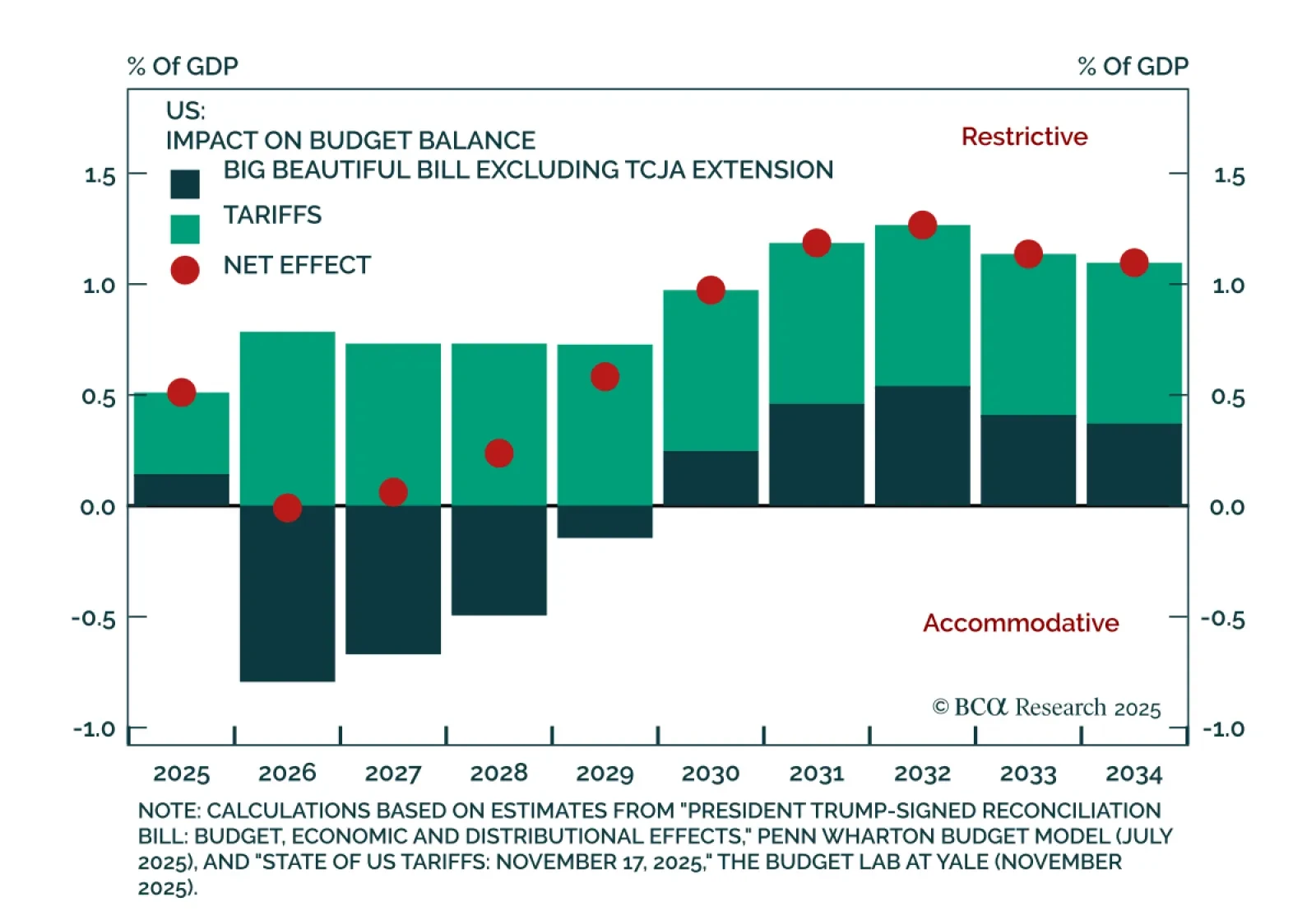

Fiscal policy is unlikely to drive the 2026 macro outlook, reinforcing a market dominated by AI sentiment rather than government spending. A key question for 2026 is how supportive fiscal policy will be for US growth. The combined effect of tariffs and tax…

Our Global Asset Allocation strategists expect the K-shaped economy to reverse in 2026, favoring cyclical areas and broadening market leadership. They upgrade Financials and Materials from neutral to overweight and downgrade Communication Services and…

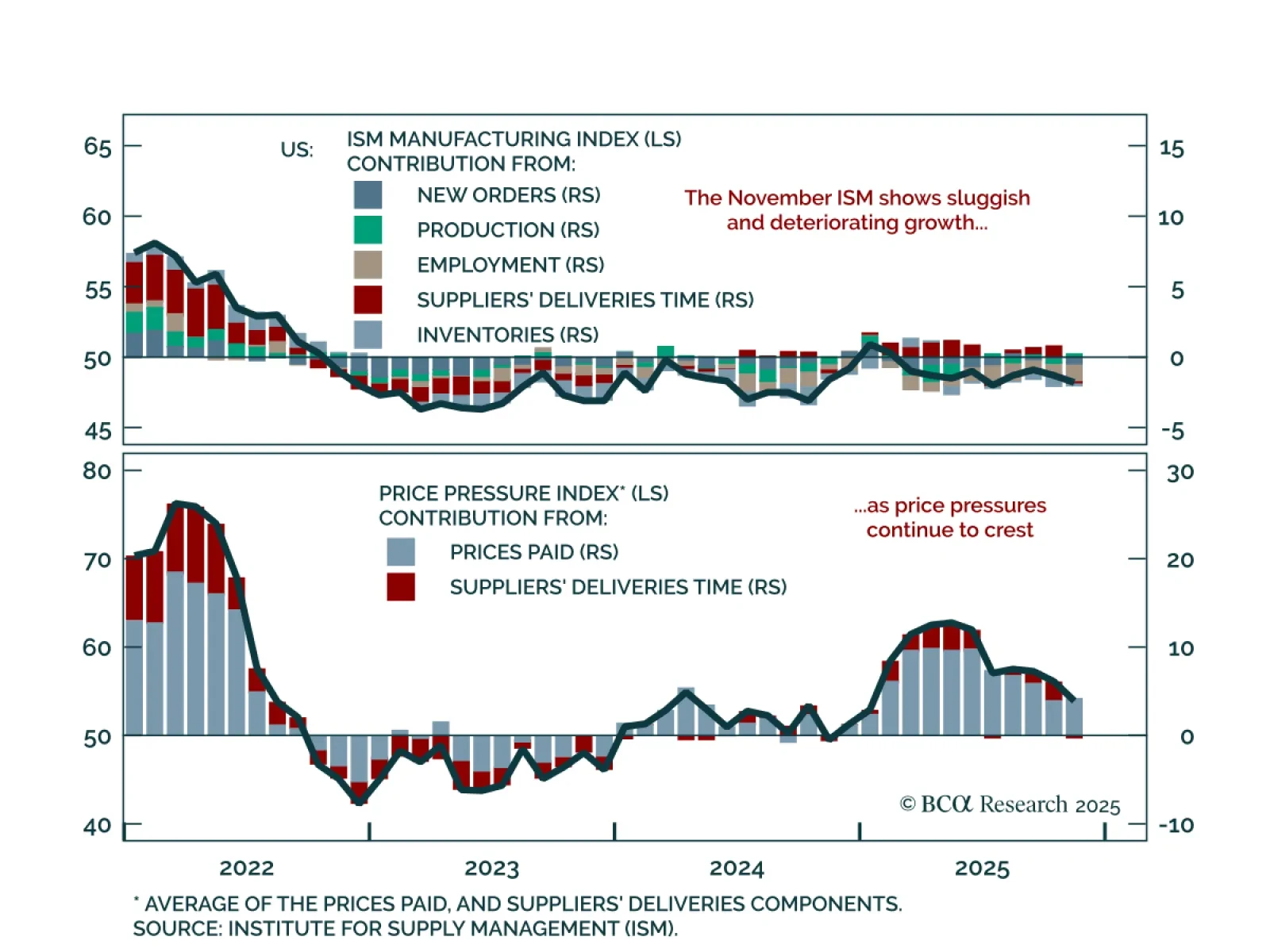

Stay overweight duration as weakening growth data and cresting goods inflation reinforce the Fed’s easing path. The November ISM Manufacturing PMI missed expectations, falling to 48.2 from 48.7 and marking a ninth straight month of contraction, driven by…

The outperformance of the S&P 500 relative to the S&P 500 EW index is likely to continue over the next year, supported by stronger earnings growth. However, extreme levels of market concentration will ultimately halt the outperformance of the mega-caps.