United States

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

Our Portfolio Allocation Summary for August 2023.

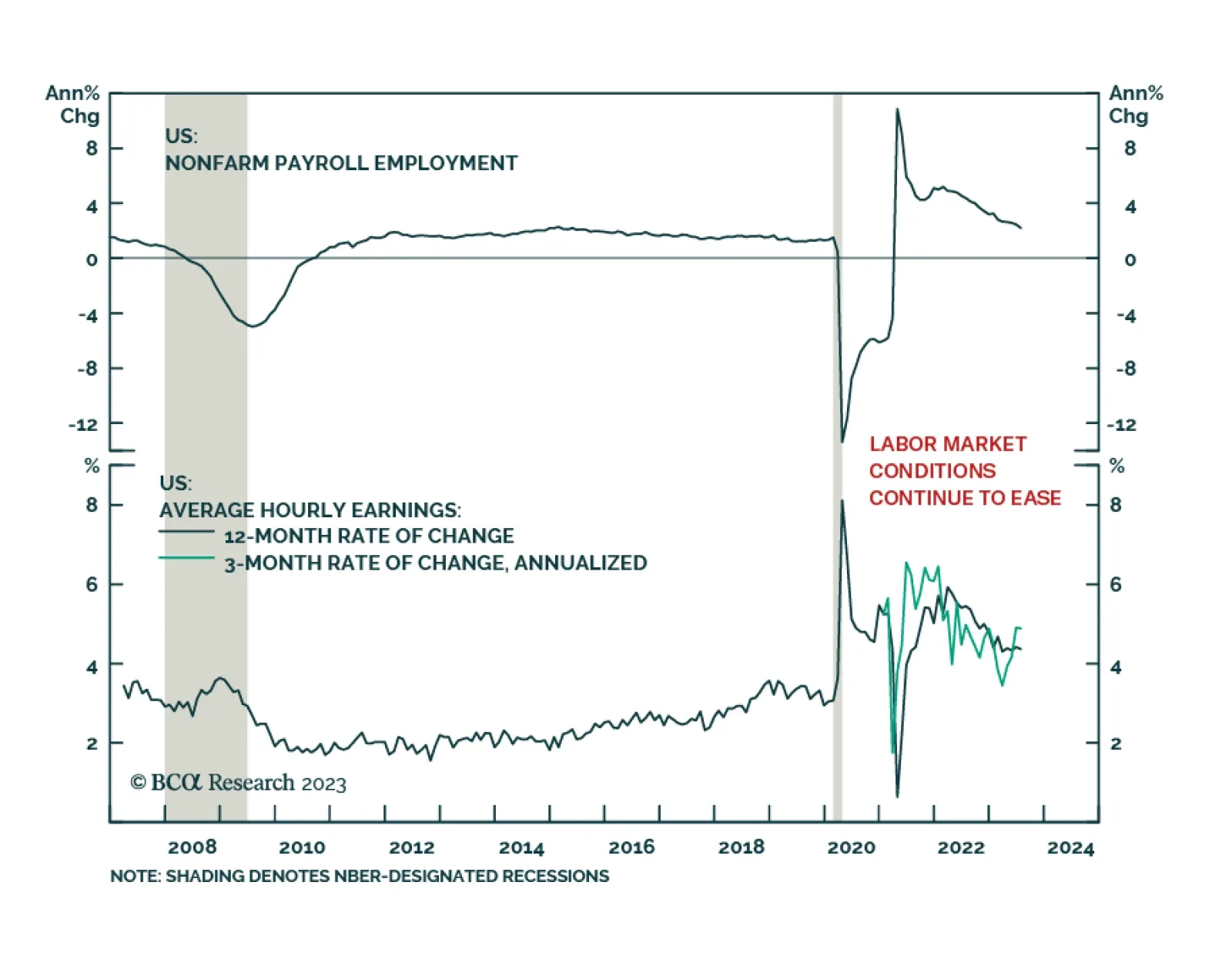

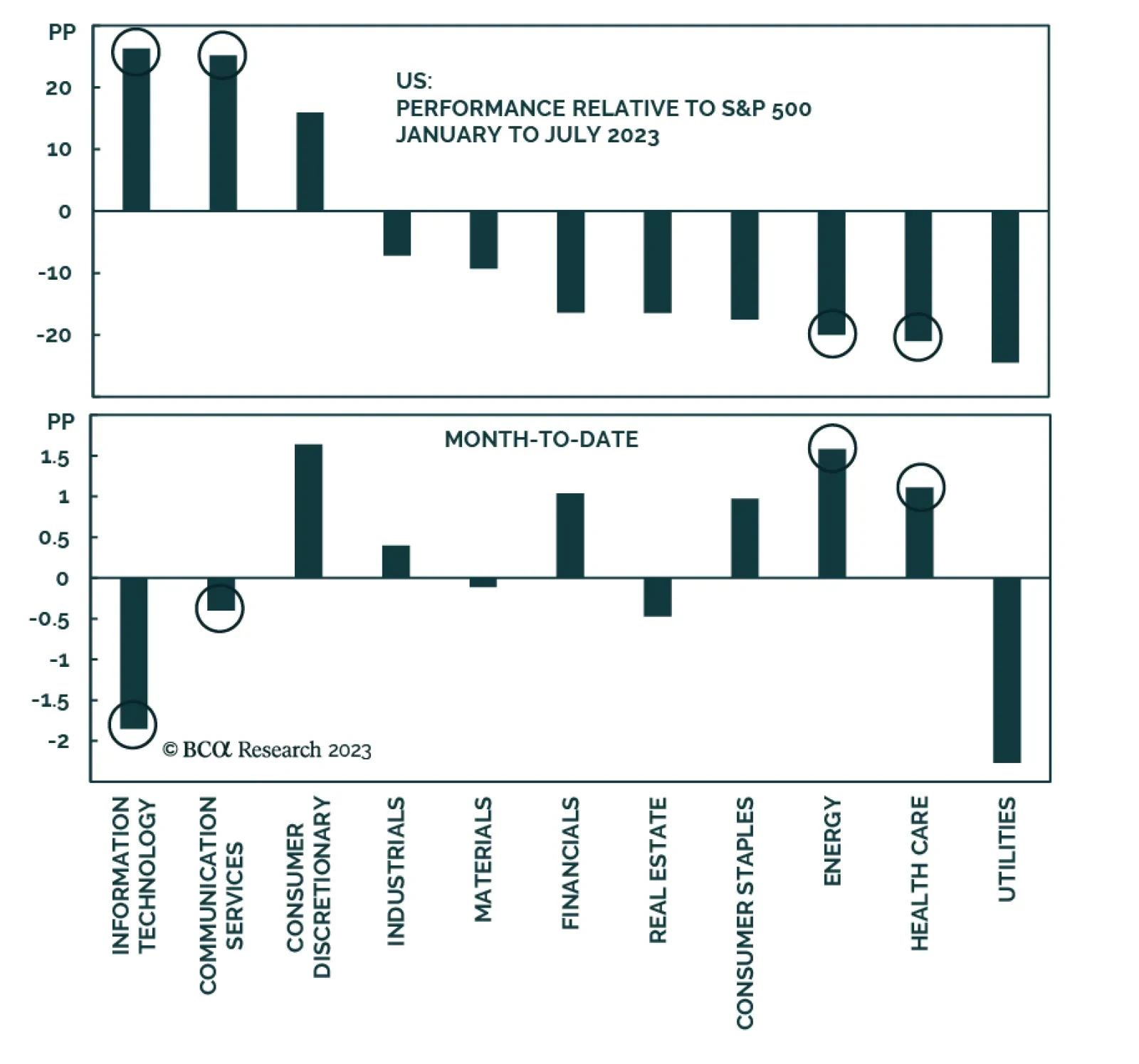

The S&P 500 rally broadened in July, lifting this year’s laggards. Surging long yields are altering the macroeconomic backdrop, as the market absorbs that monetary policy will stay restrictive for a long time. Yet, a move down in yields is more likely than a move up over a tactical horizon. Q2 earnings were better than expected but investors were unimpressed – the good news is already priced in. The market is overvalued and is close to being overbought, which makes it vulnerable to disappointment.