United States

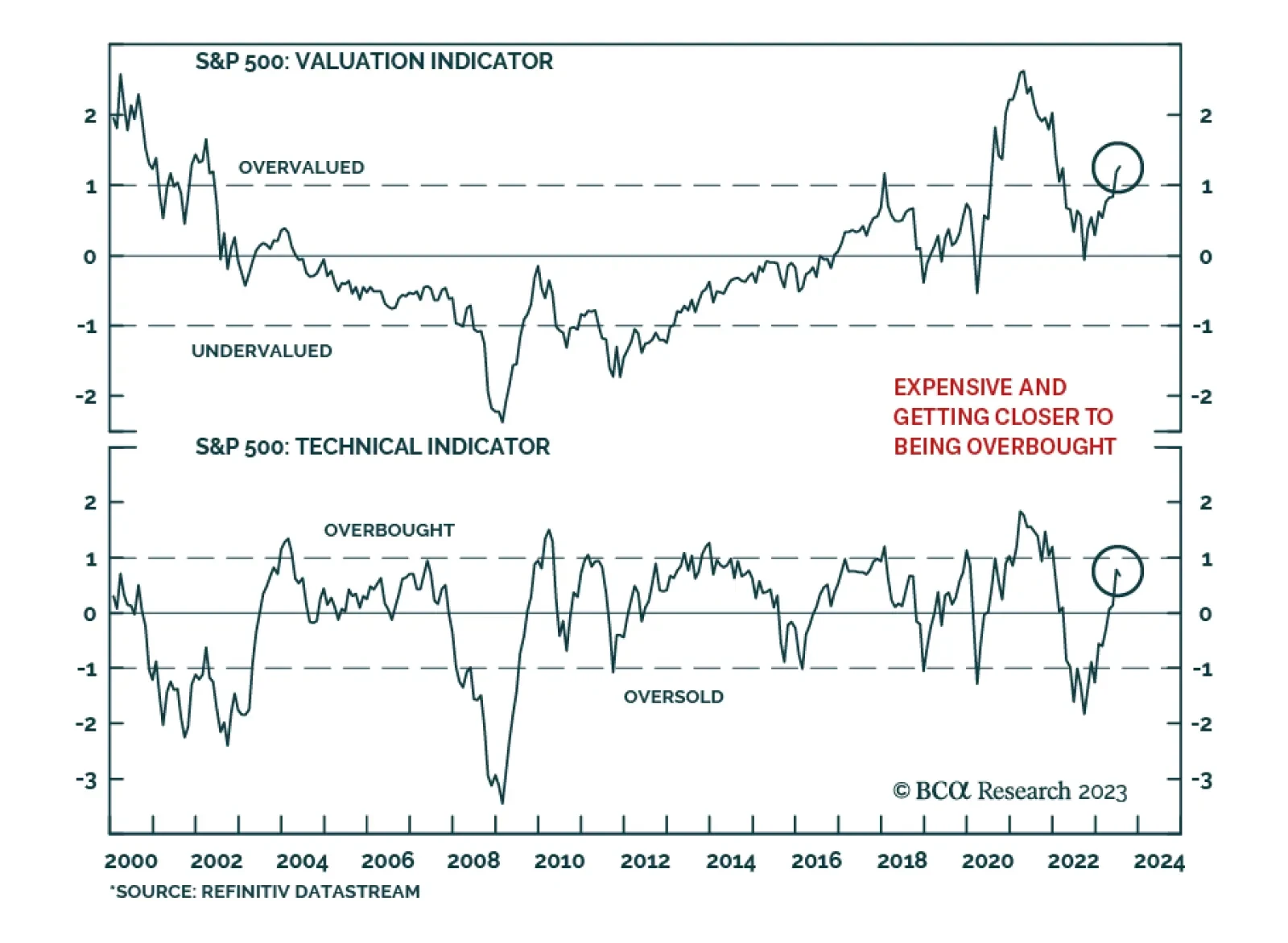

History suggests that a “soft landing” is highly unlikely after such an aggressive Fed tightening cycle. The rally could continue for a little longer but, on the 12-month horizon, market risks are very skewed to the downside.

Investors remain cautious about the US economy and still have significant cash that needs to be put to work which could extend the rally further. Earnings rebound later in the year will be supported by rising sales growth and surging earnings of the Magnificent Seven. A restocking cycle, and a pickup in freight activity support transports. Upgrade Transports to an overweight.

The latest round of earnings calls from the systemically important banks suggested that the expansion is still intact. Households are still flush and still spending and consumer and business delinquencies remain remarkably low.

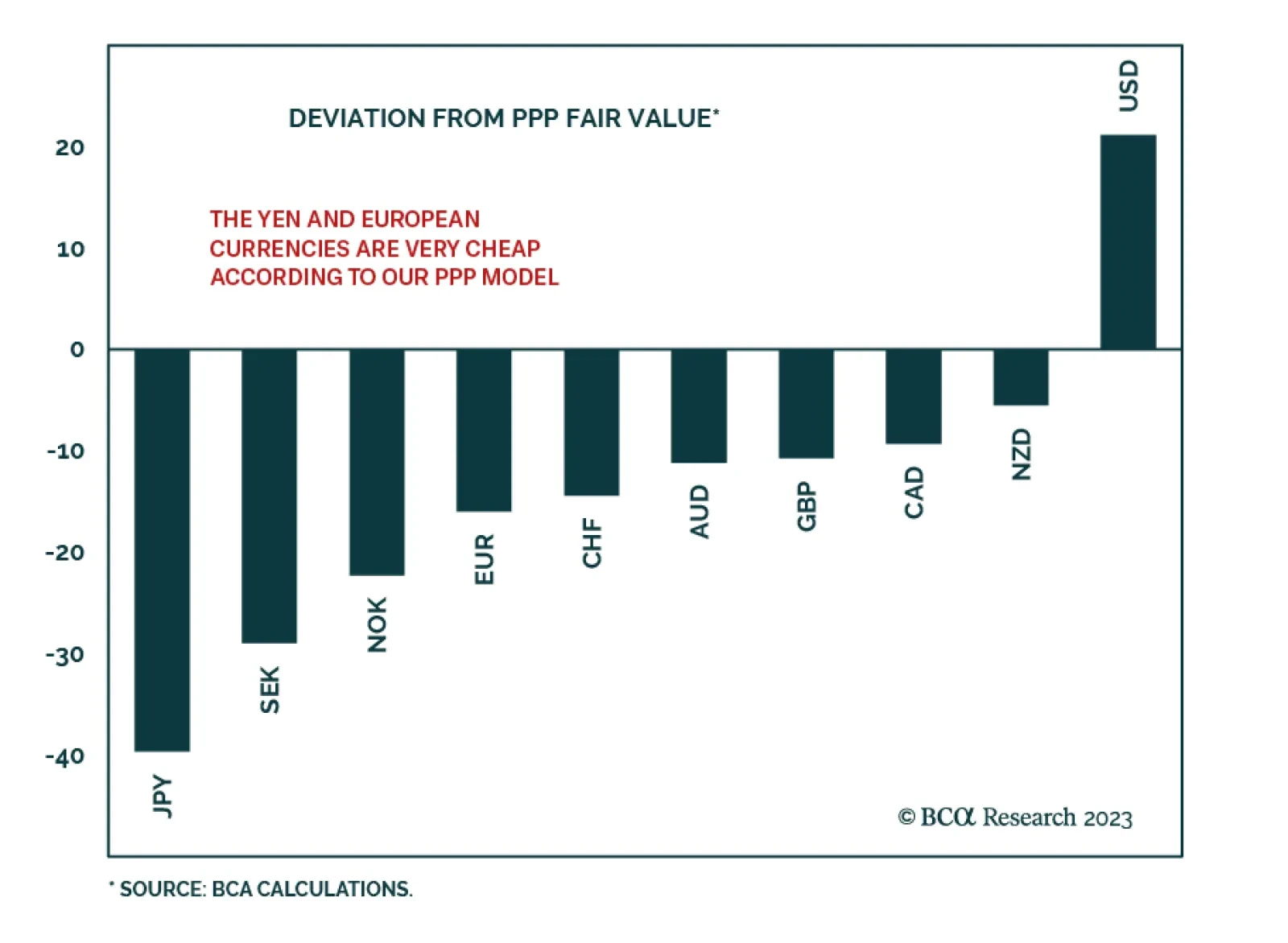

The DXY will continue to have near-term upside, as economic growth holds up in the US, while it deteriorates in other parts of the world. Remain constructive on the DXY at current levels, but pivot to a short position on evidence US growth is boosting the rest of the world.