United States

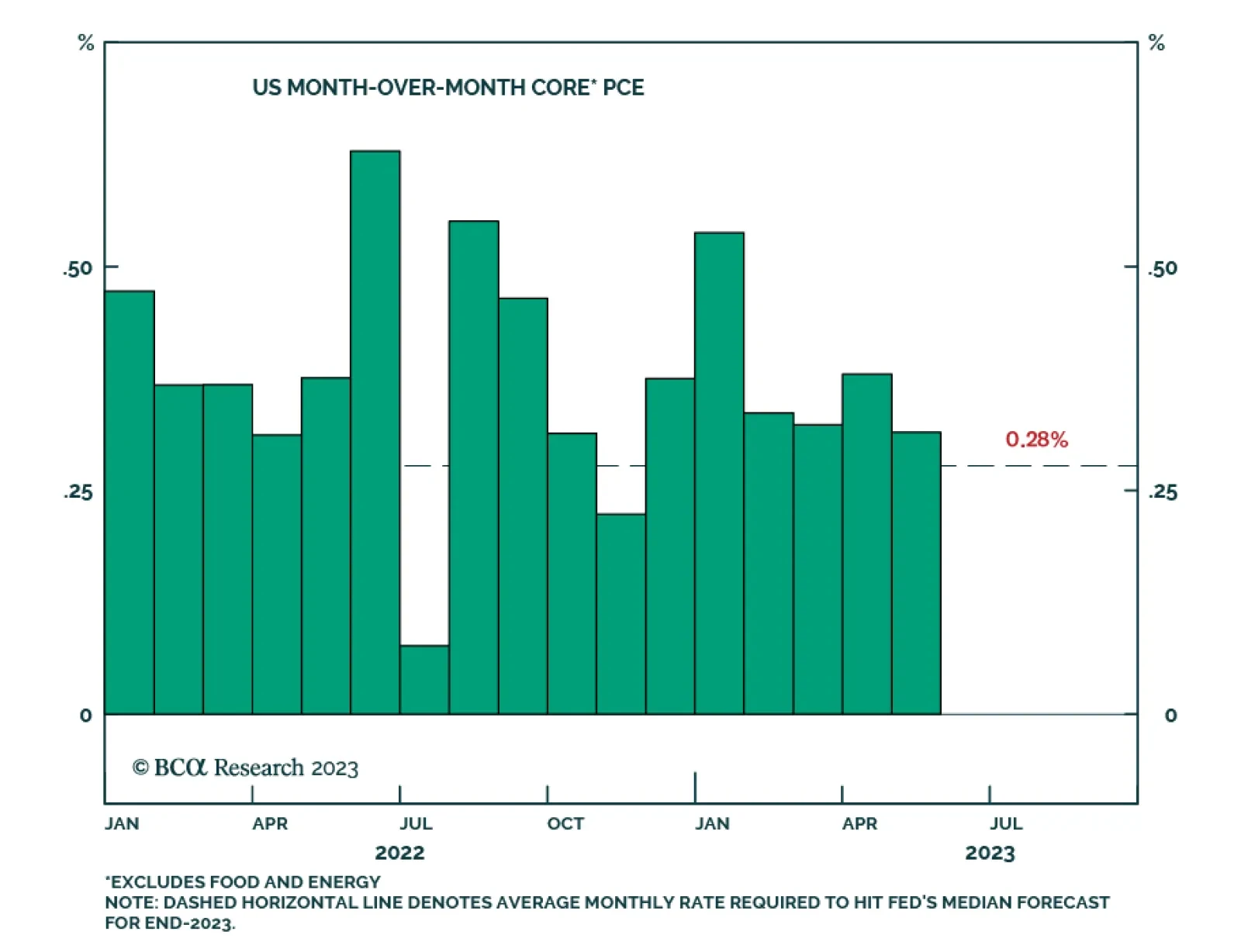

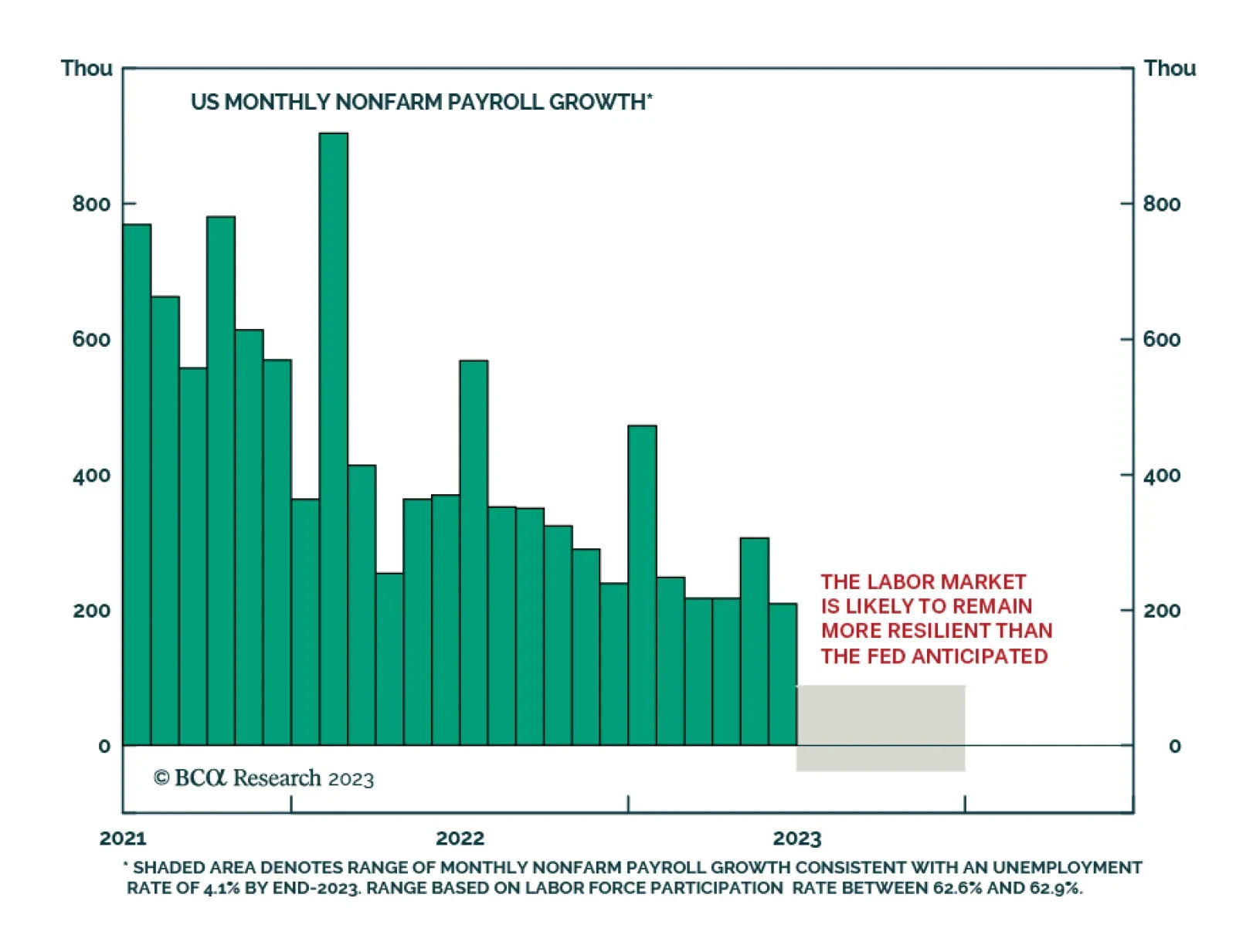

The US is not out of the woods when it comes to inflation, which means that it is too early to conclude that the Fed can stop raising rates. Any further increase in inflation risk would prompt us to turn more cautious on stocks.

A look at recent US data on economic growth and inflation, with an update on the implications for monetary policy and bond yields.

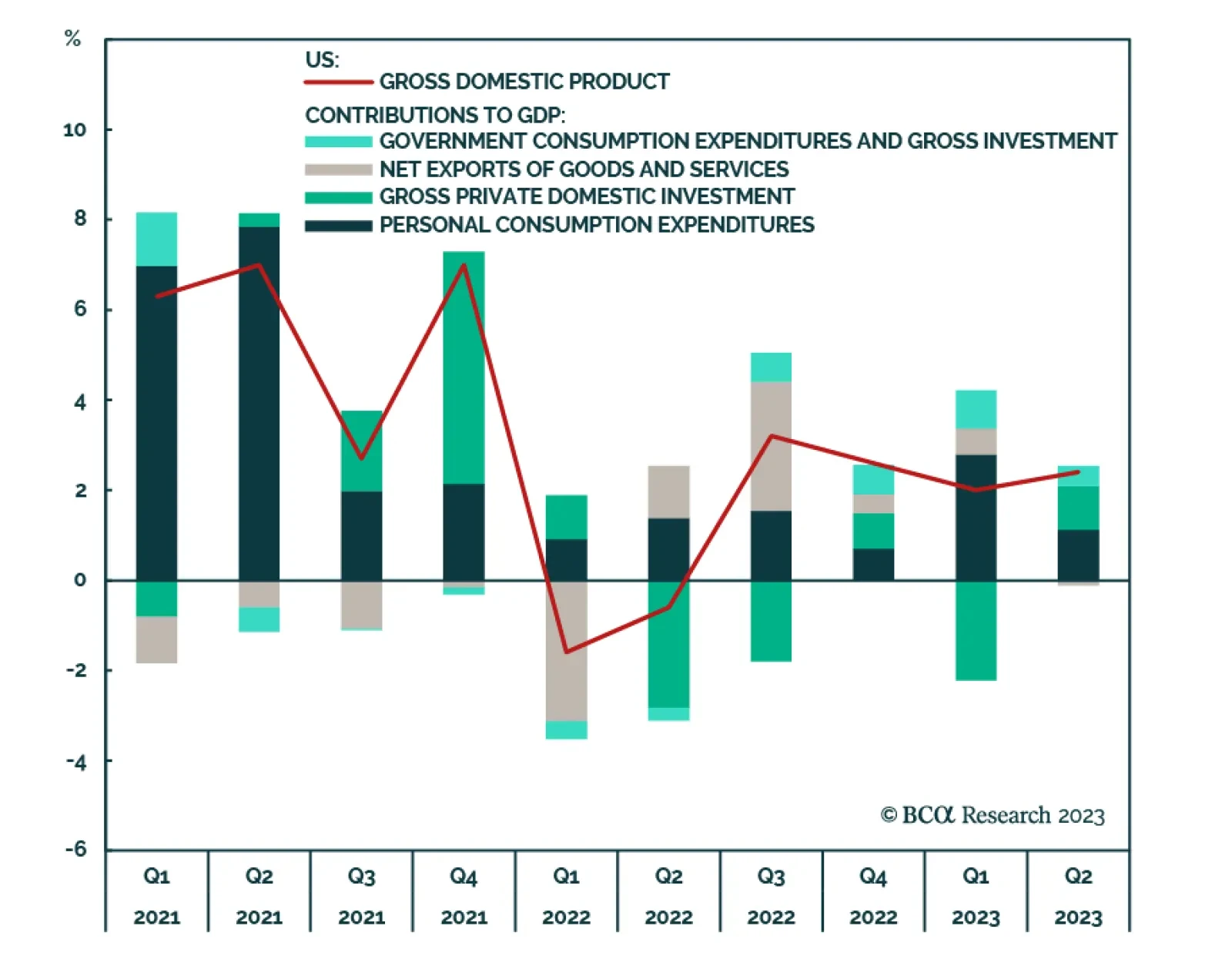

In Section I, we audit the market’s “soft landing” narrative in response to a meaningful challenge to our cautious stance from recent financial market developments. We acknowledge that US economic growth was stronger in the first half of the year than many investors expected, but we are unmoved by the recent uptick in “soft landing” hopes. A “soft landing” outcome very likely necessitates interest rate cuts before recessionary dynamics emerge, and it is far from clear that rate cuts or (especially) an easy monetary policy stance are likely to materialize over the coming year. As such, we continue to believe that conservative portfolio positioning is appropriate. In Section II, we discuss some simple approaches that we use when valuing the major asset classes that we cover. We conclude that global ex-US equities and ex-US developed market currencies are the main assets that can be considered “cheap” today.

Among the critical materials needed for the global energy transition, Li is expected to see the largest increase in demand from 2022 to 2050. Li supply is not constrained, but continued investment in mining and refining will be required to meet increasing demand. We expect strong Li-ion battery demand in the major economies of the world – the EU, US and China – will keep a bid under Li, and allow growing supply to find a home. At tonight’s close we are getting long the LIT ETF, consistent with our view.

A brief recap of the July FOMC meeting and its investment implications.

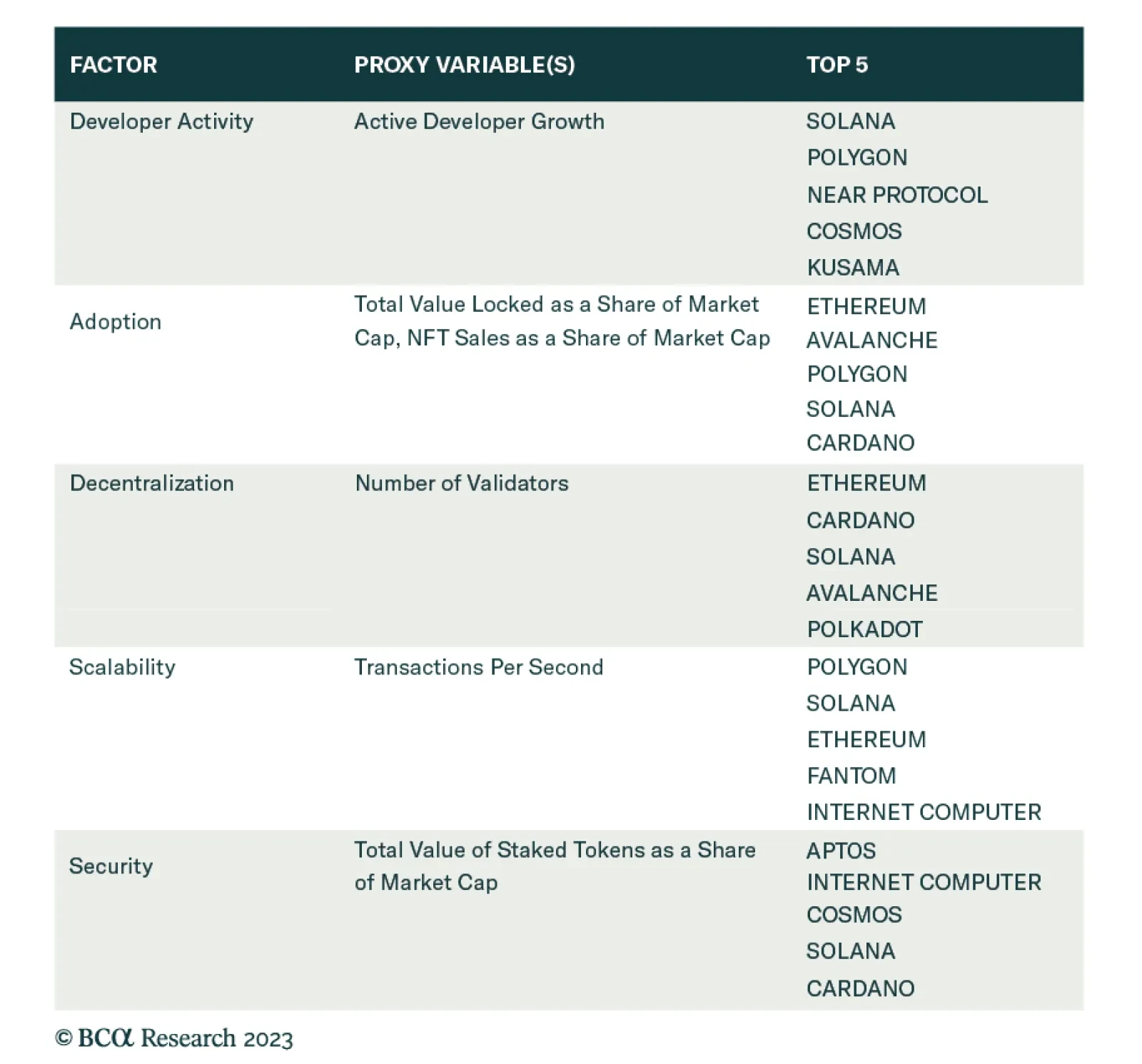

We recommend a small structural exposure to cryptocurrencies and blockchain tokens, given their incipient real-world uses as well as their proven hedging qualities against the debasement of fiat money and in banking crises. In this Special Report, we rank the major blockchains on five factors – developer activity, adoption, decentralization, scalability, and security – from which we arrive at our top five blockchains.