United States

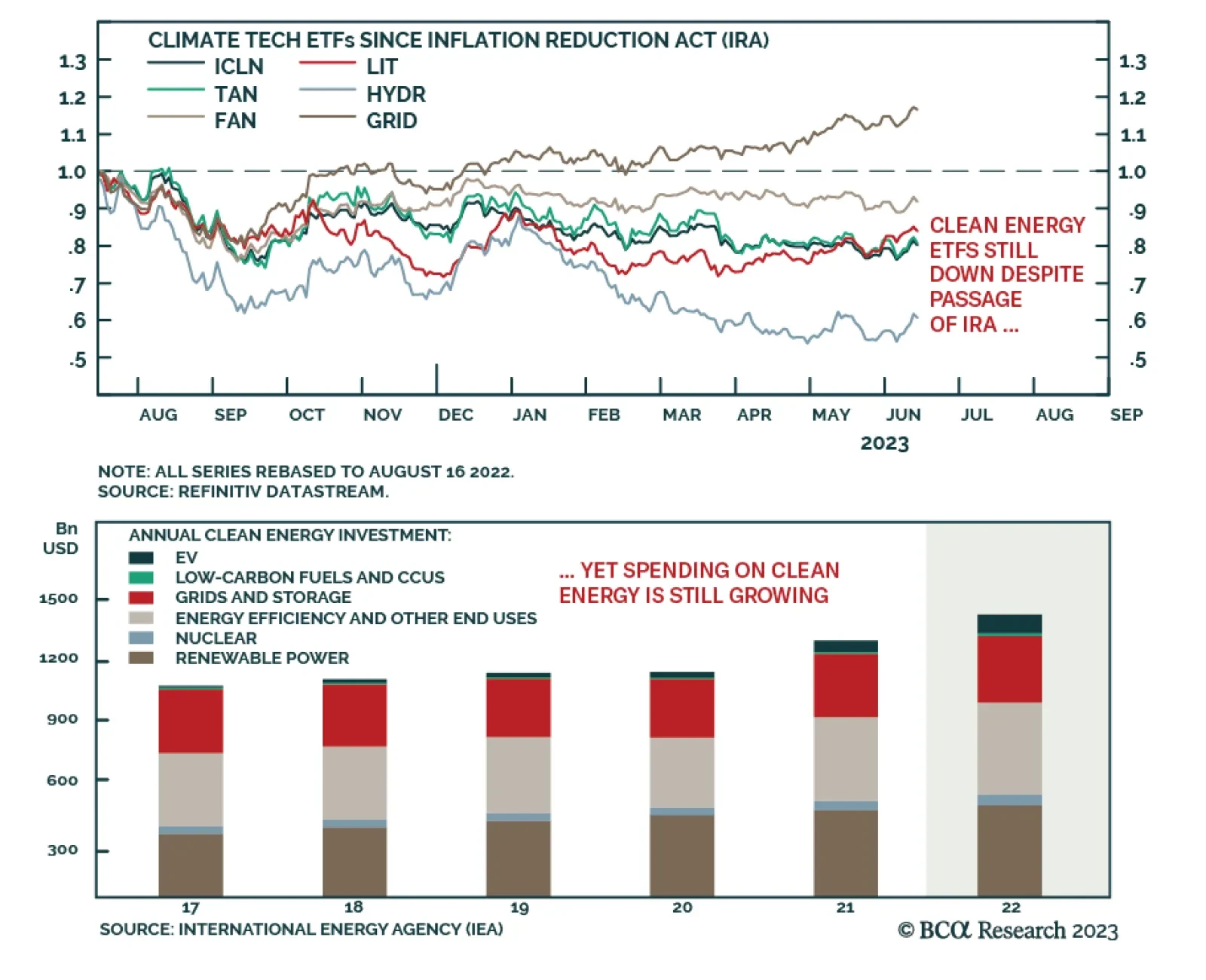

Both EV and Green Energy themes still hold strategic promise for investors, posing large upside, despite prevailing macro headwinds. While both themes have yet to claw back their pandemic peaks, a broadening of the rally supports a run for both, even in the face of high valuations.

In recent months, the European and US economies have greatly diverged, with the Euro Area massively disappointing while the US has surprised to the upside. Can this dichotomy continue or is it Europe’s turn to shine?

The S&P 500 reached our 4,500 mid-year target last week, but the bears have yet to capitulate and stocks could melt up so we are placing a trailing stop on our tactical overweight instead of downgrading equities outright.

Stocks fare best when there is plenty of slack in the economy and growth is strong and getting stronger. The good news is that the economic growth score for the US in our MacroQuant model is above its historic average. The bad news is that US economy is operating with little slack and sentiment is getting complacent. We recommend that investors maintain a modest overweight to equities for the time being but look to get more defensive later this year or in early 2024.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.