United States

The world economy is likely already in recession, defined as world growth dipping to sub-2 percent. So far, the world recession has been China-led, but in the coming months it will change to being developed economy-led. Hence, while metals and industrial commodities may get some brief respite, high yield credit and stocks will underperform government bonds. New tactical recommendations are to overweight French luxury goods versus US tech, and to overweight USD/COP.

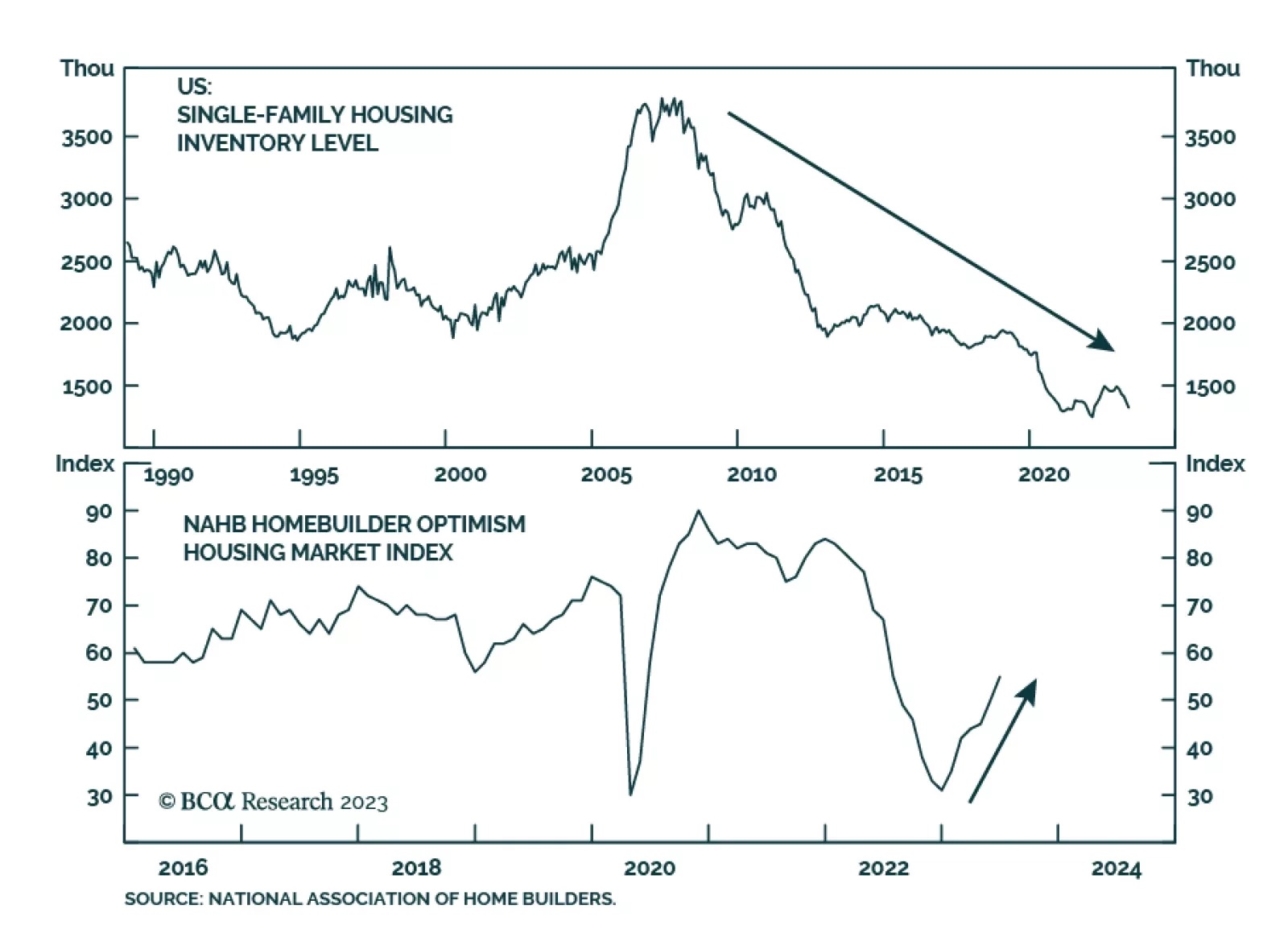

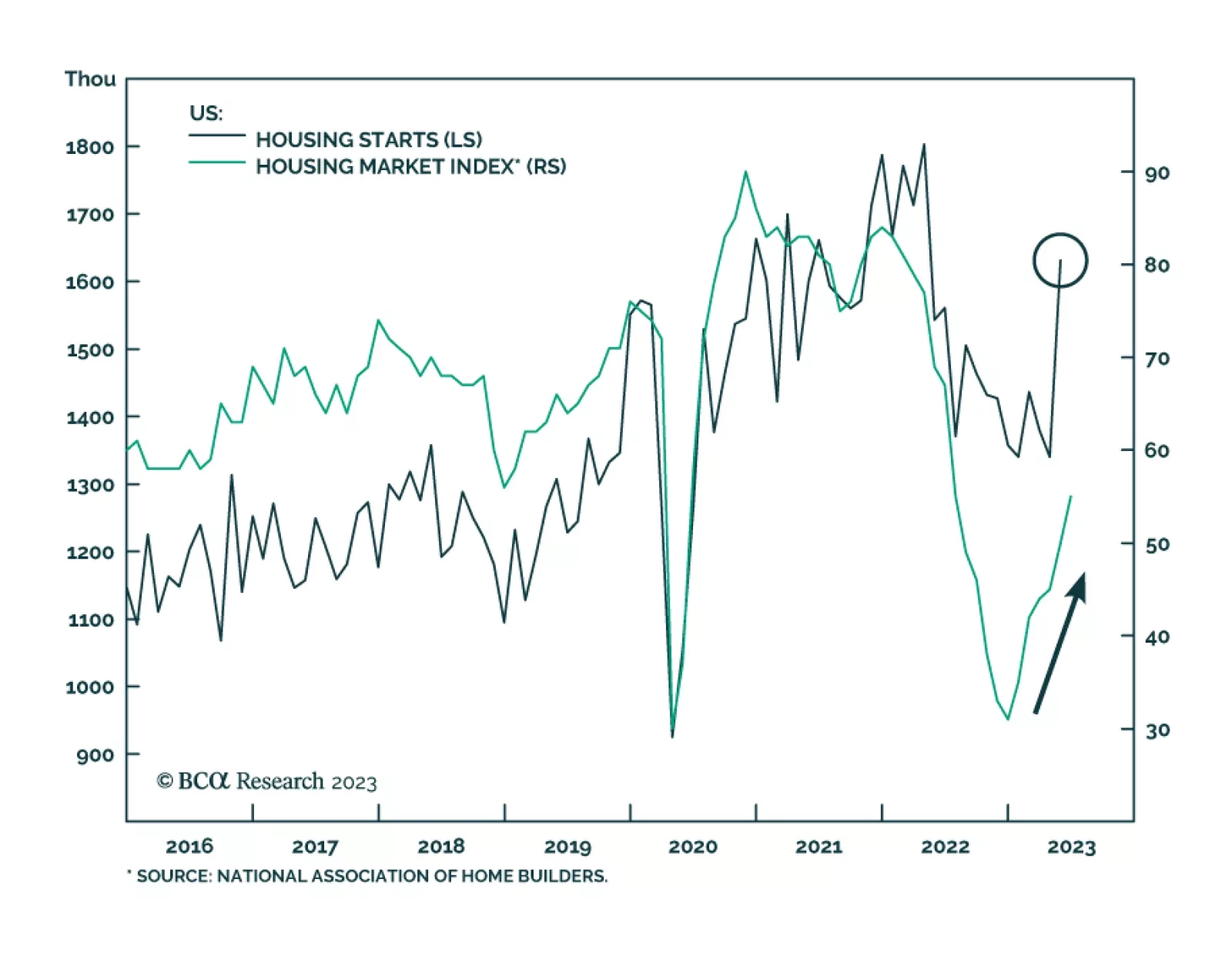

In June, the rally gained momentum and broadened due to positive economic data, particularly in the housing market. We expect cheaper cyclical sectors and styles to mark a change in leadership as the rally broadens, helped on by excess cash on the sidelines. We upgrade Banks to equal-weight, and Homebuilders to overweight. The rally may continue but a soft landing continues to be elusive - disappointment may be in store.

Recession is on track to start around year-end. Stocks usually peak shortly before recession begins. So, position defensively but be prepared for a few more months of the rally.

Our recession indicator turned red in late December. Though it has informed our 12-month caution, we are sticking with our tactical equity overweight as we expect that the lagged effects of pandemic fiscal largesse may extend the lag between Fed rate hikes and palpable economic slowing.

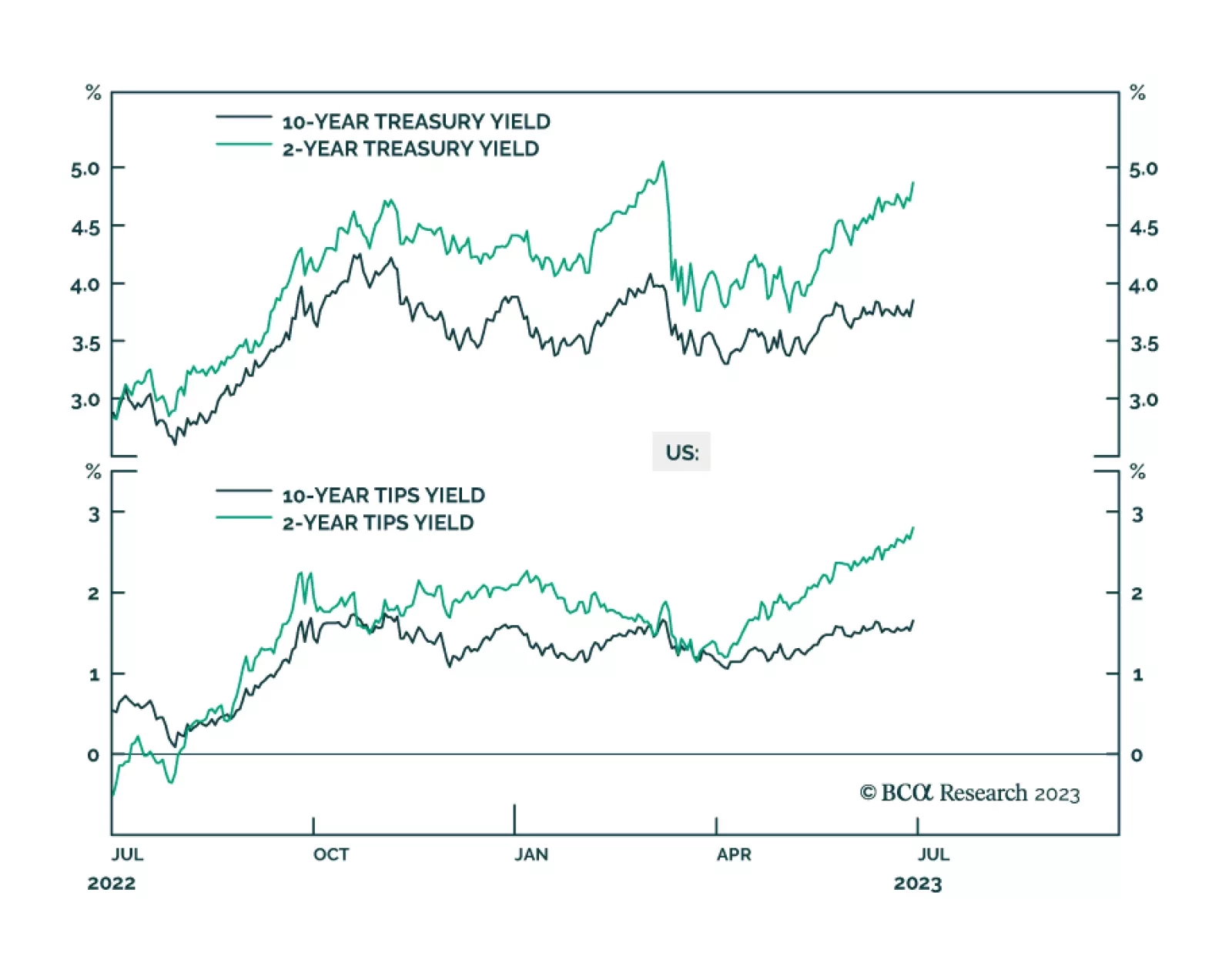

A look at how US bond yields responded to yesterday’s strong economic data and this morning’s soft inflation print.