United States

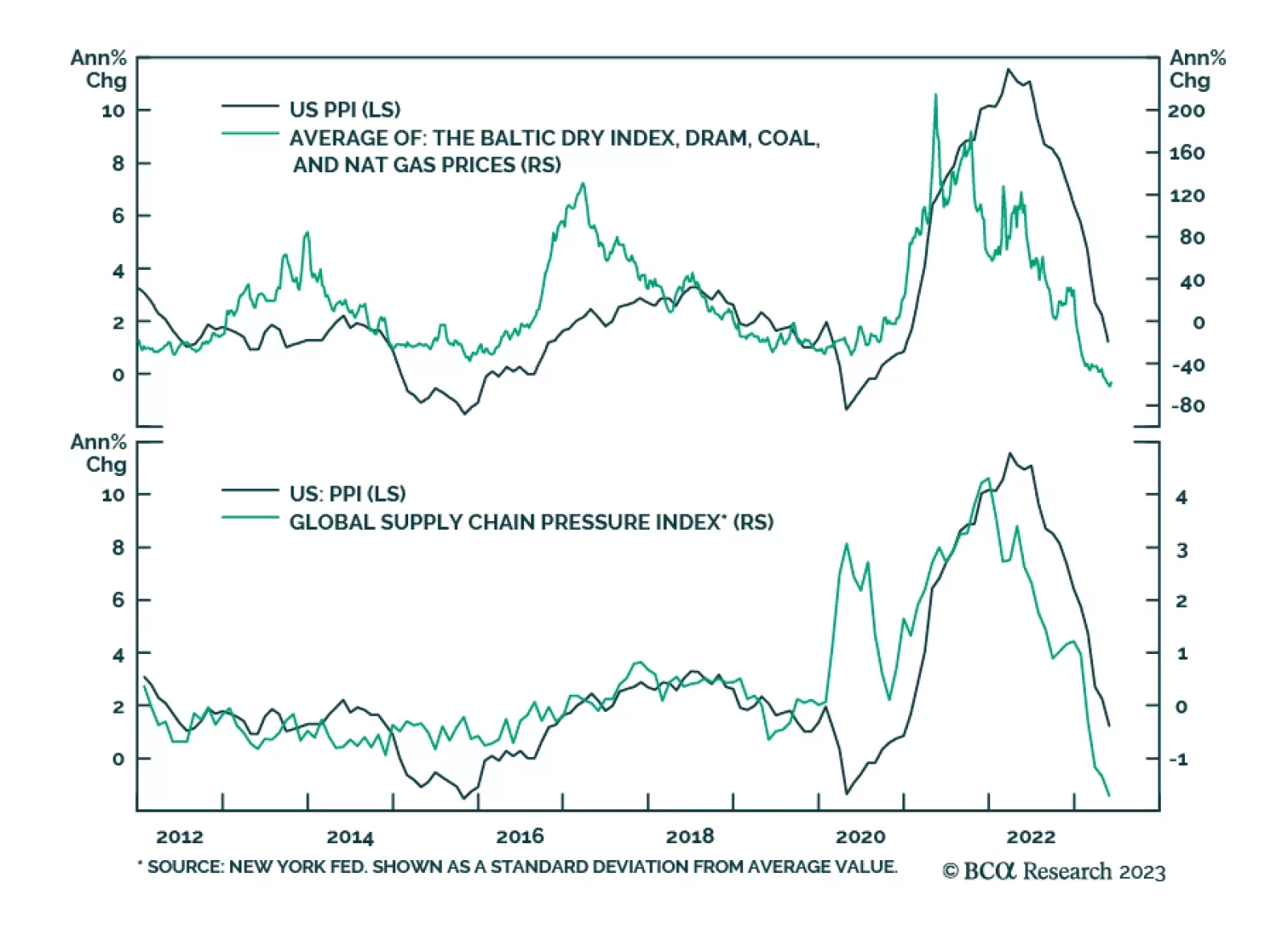

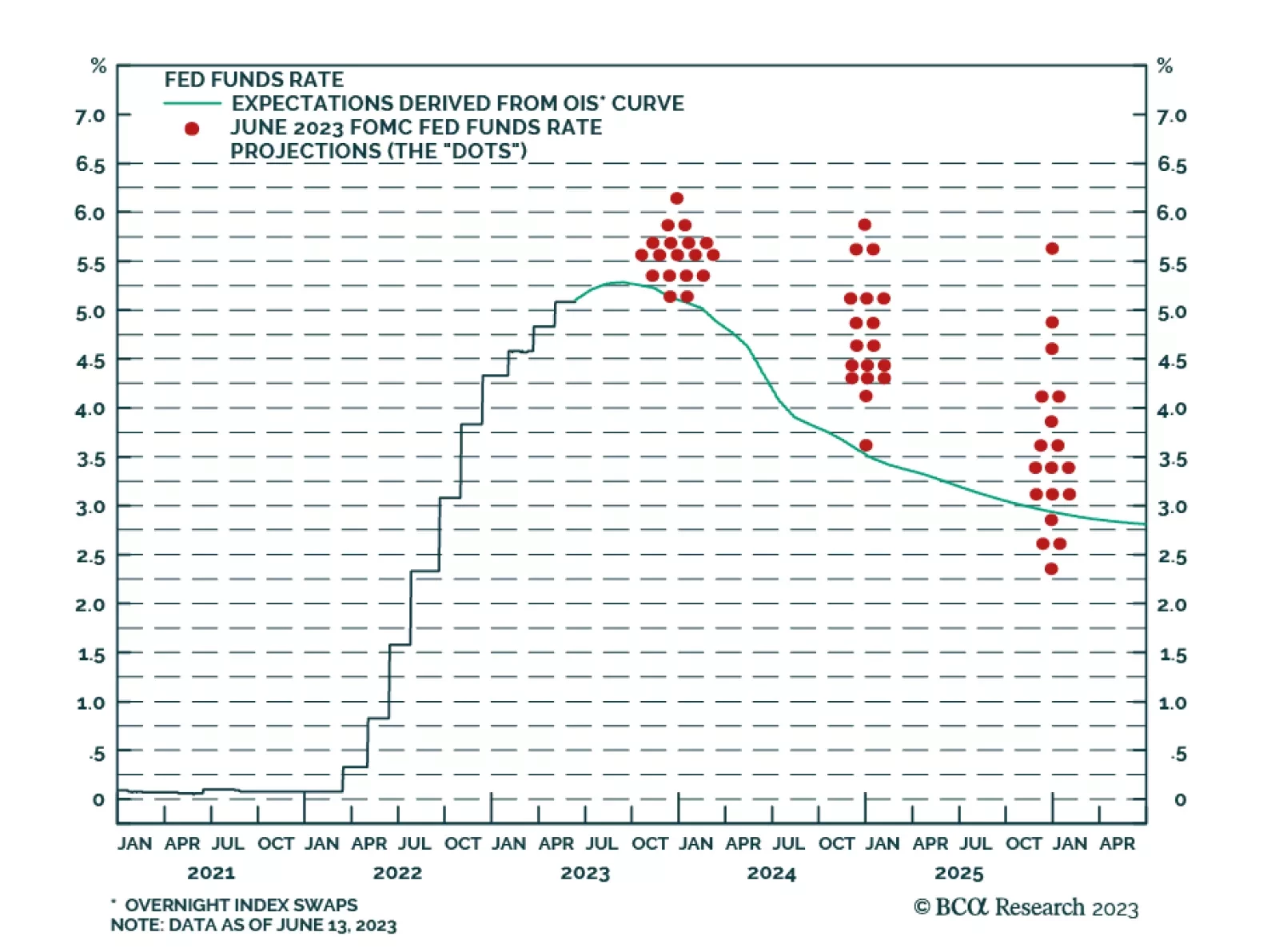

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

We are overweight Private Credit. Improvements in yield, negotiating leverage, and structuring upside are major tailwinds over the coming years. The business cycle provides an attractive backdrop for all Private Credit sub-asset classes. In this Special Report we examine Private Credit as a whole, but with more emphasis on the income-focused sub-categories of Senior and Mezzanine Debt.

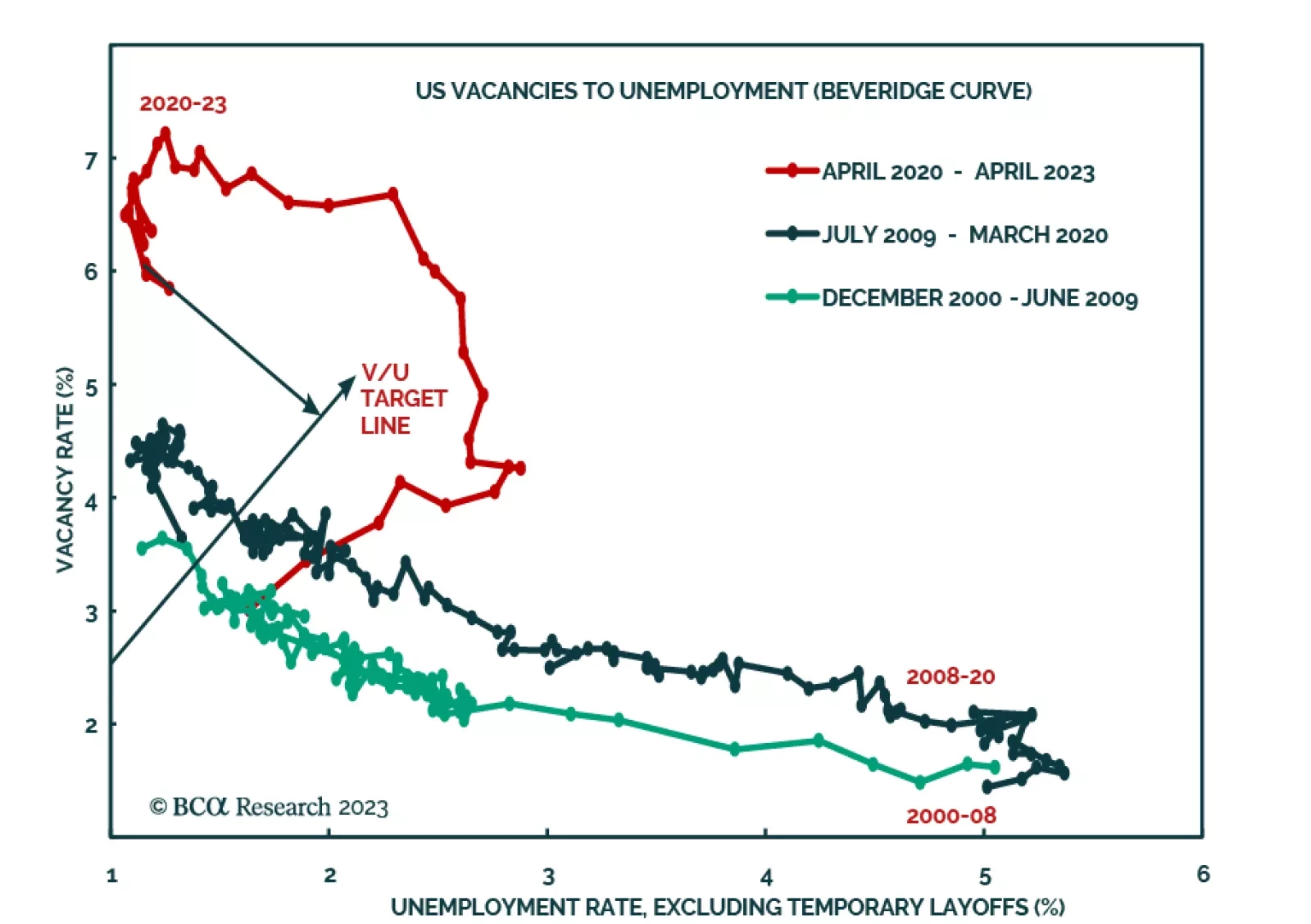

As the major central banks once again mull their policy options, they face a daunting task. They must phase-transition inflation back to imperceptible, without phase-transitioning unemployment to perceptible. This report explains why this will prove impossible, and what central banks will likely prioritise. Plus: the collapsed complexity of the recent stock market rally signals excessive trend-following. Until the complexity normalises, we are reluctant to chase the rally.

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.