United States

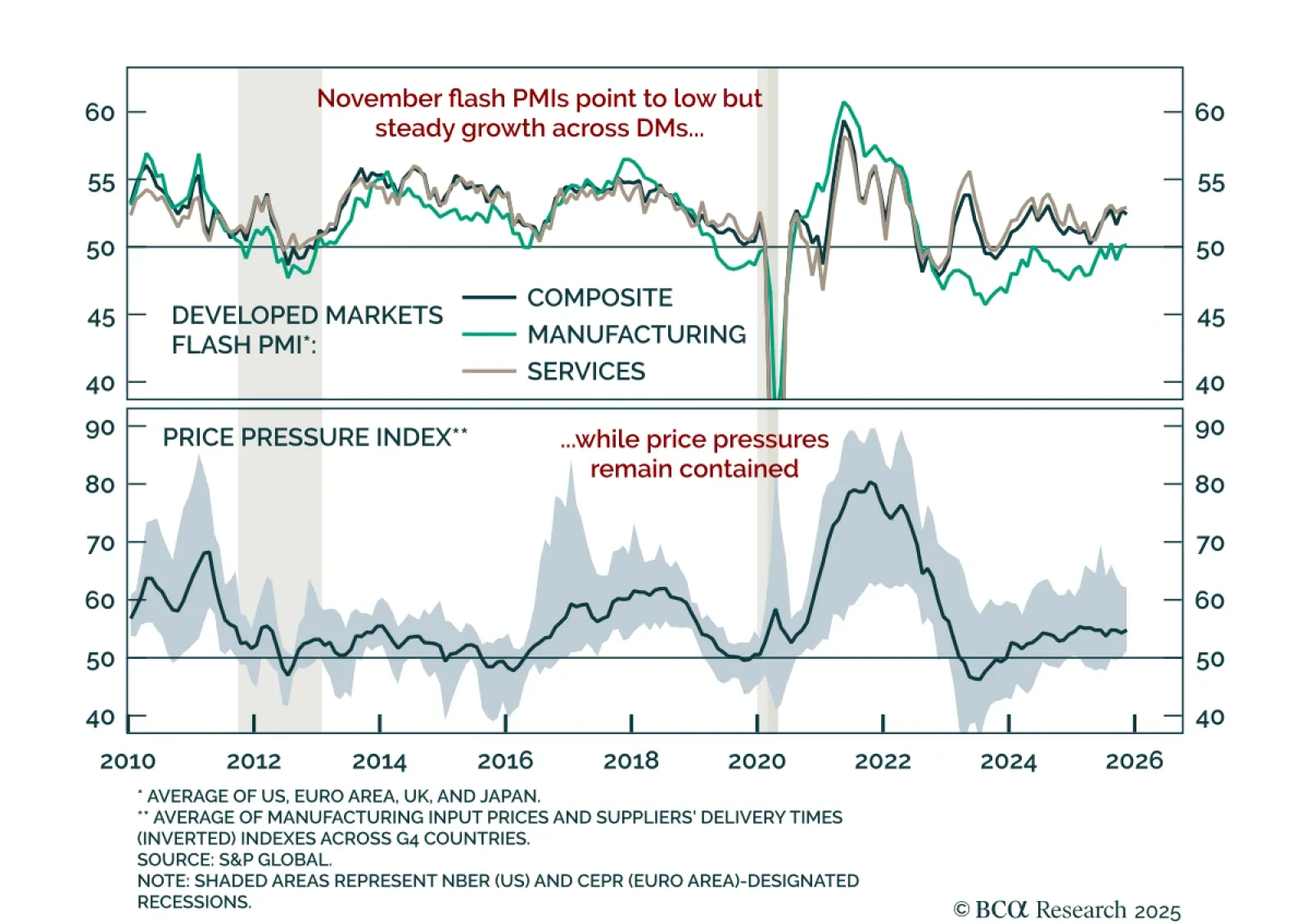

November flash PMIs confirmed sluggish global momentum, reinforcing a defensive stance with tactical support for the USD. The US composite PMI rose to 54.8, driven by stronger services but weaker manufacturing. The Euro area showed a similar pattern, with…

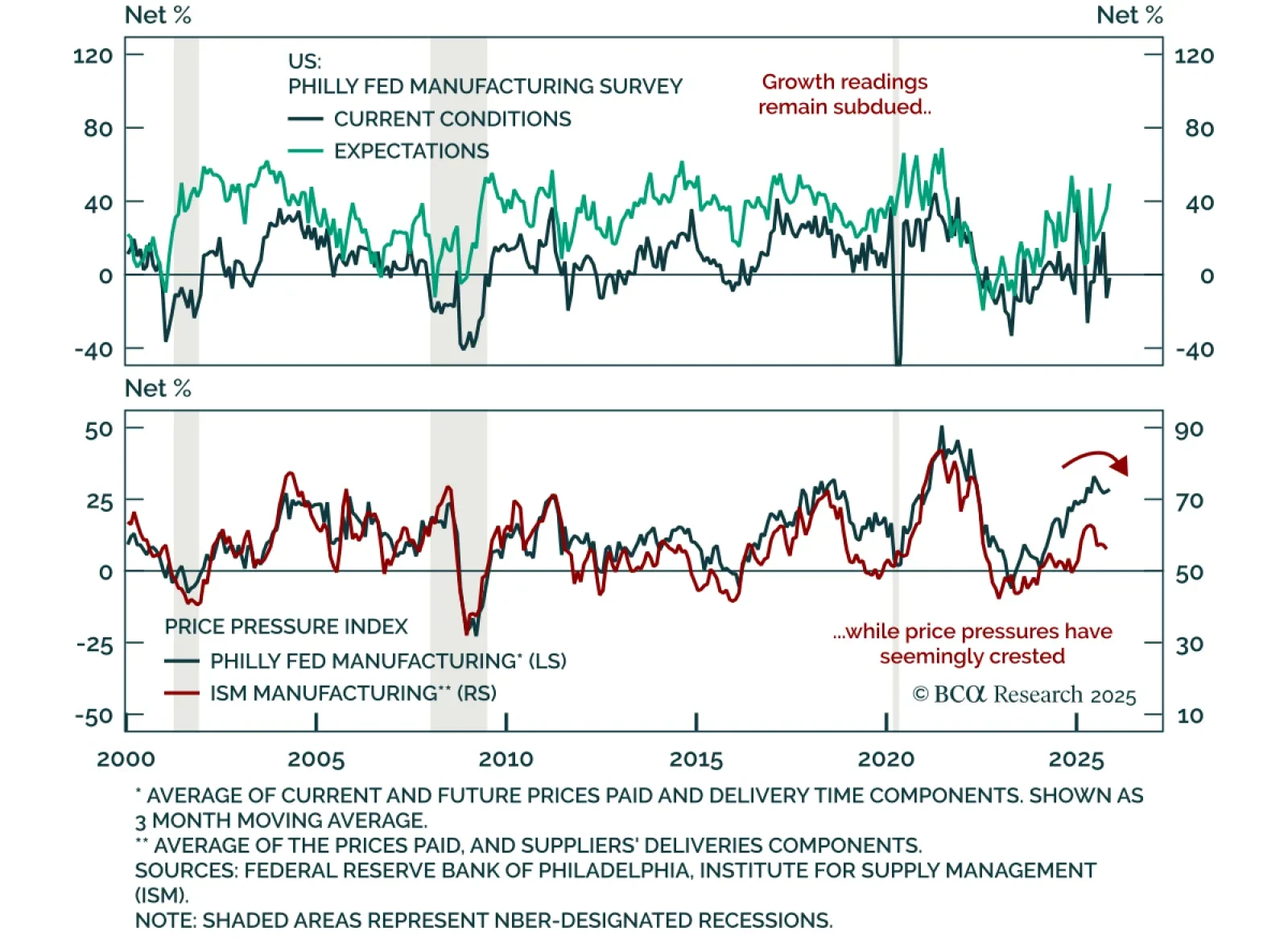

The November Philadelphia Fed survey missed expectations, showing manufacturing activity remains subdued with little momentum. Although the headline index rose to -1.7 from -12.8, new orders and shipments both slipped into contraction. Employment and hours…

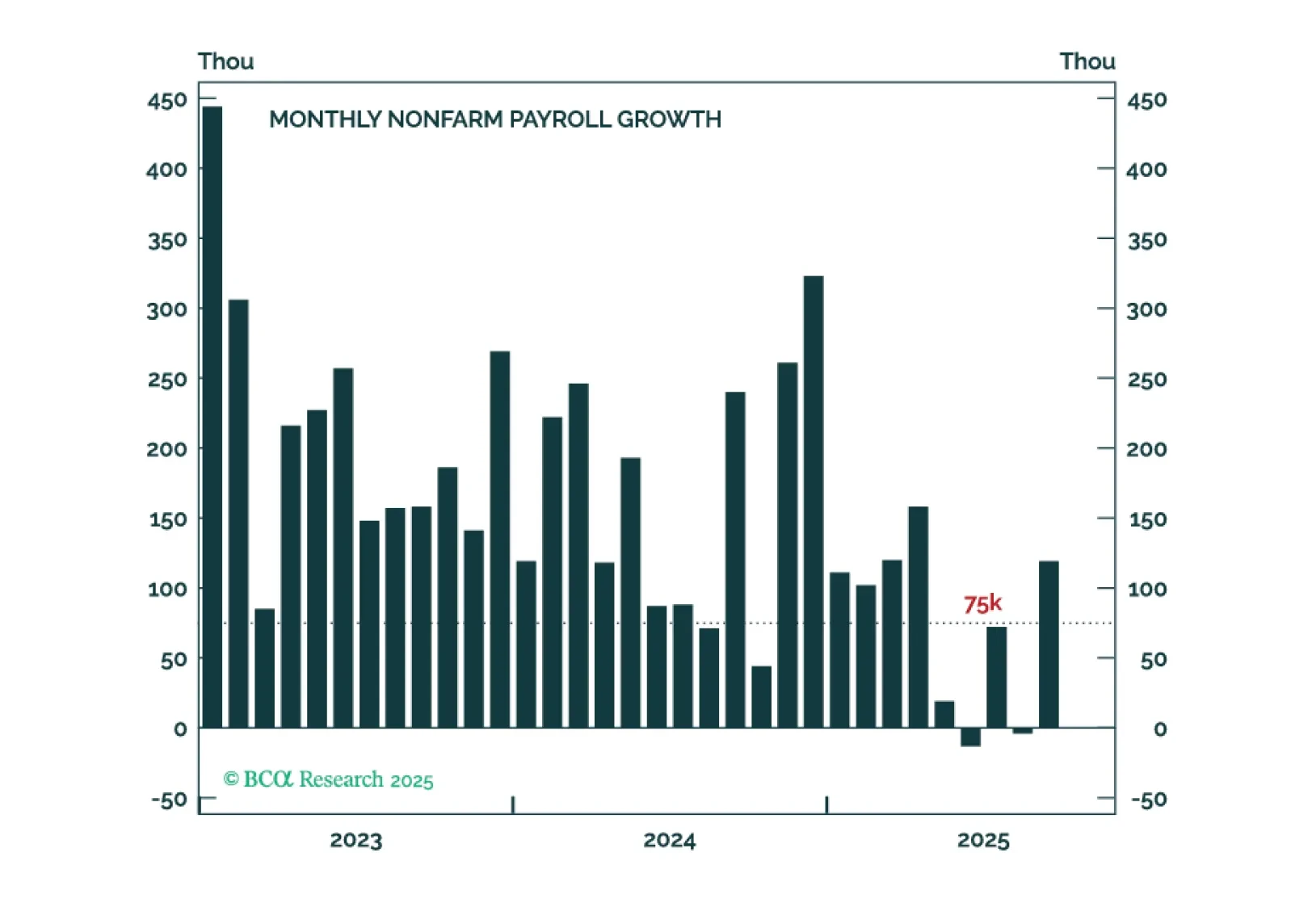

September’s stronger-than-expected jobs report is unlikely to sway a divided FOMC, but labor market trends remain weak beneath the headlines. Nonfarm payrolls rose 119k after a downwardly revised -4k in August, but net revisions subtracted 33k from prior…

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

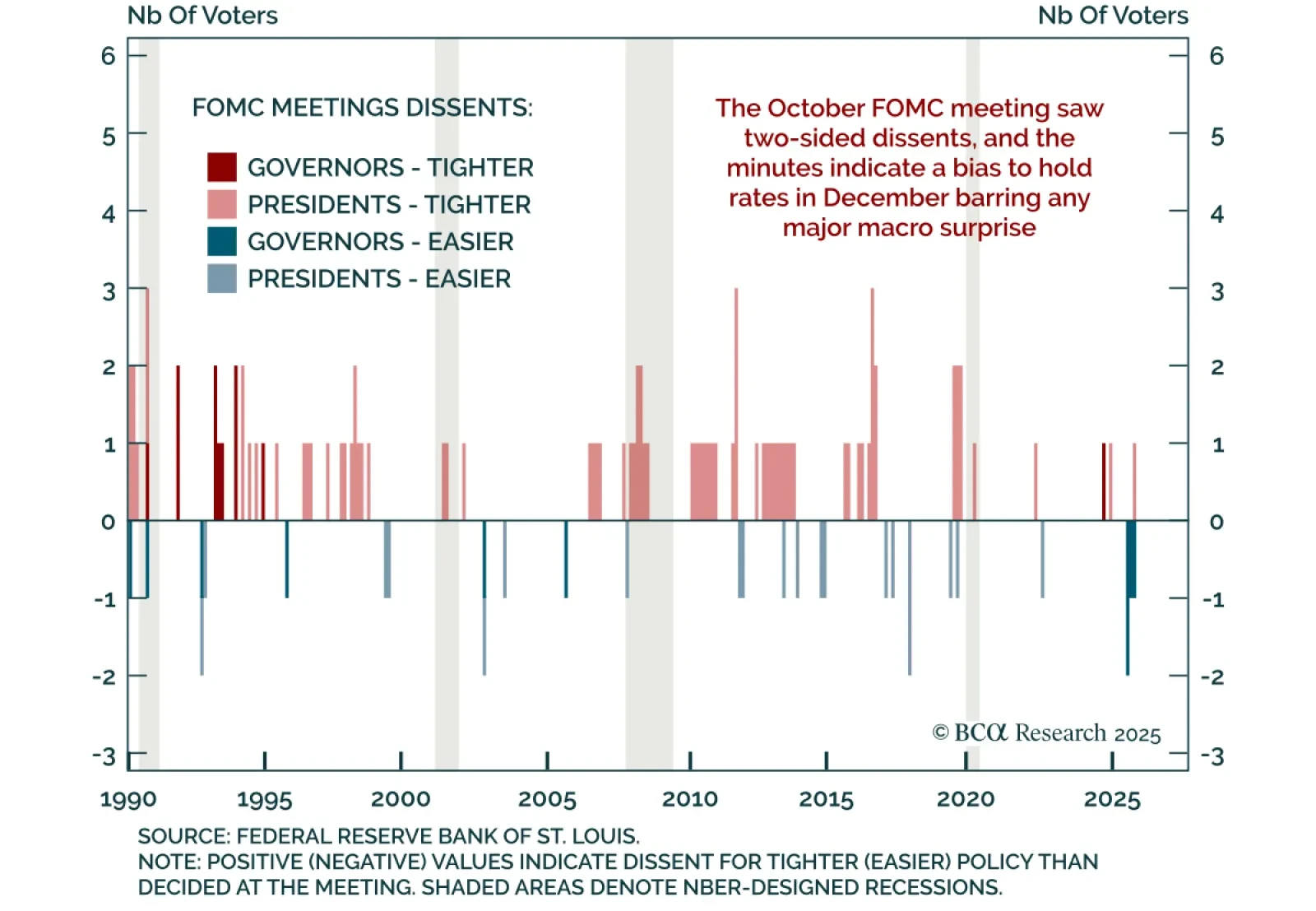

The October FOMC minutes underscored deep divisions over the Fed’s next move, reinforcing expectations for a December hold but keeping the easing bias intact. The 10–2 vote for a 25 bps cut included dissents on both sides (Governor Miran for a 50 bps move and…

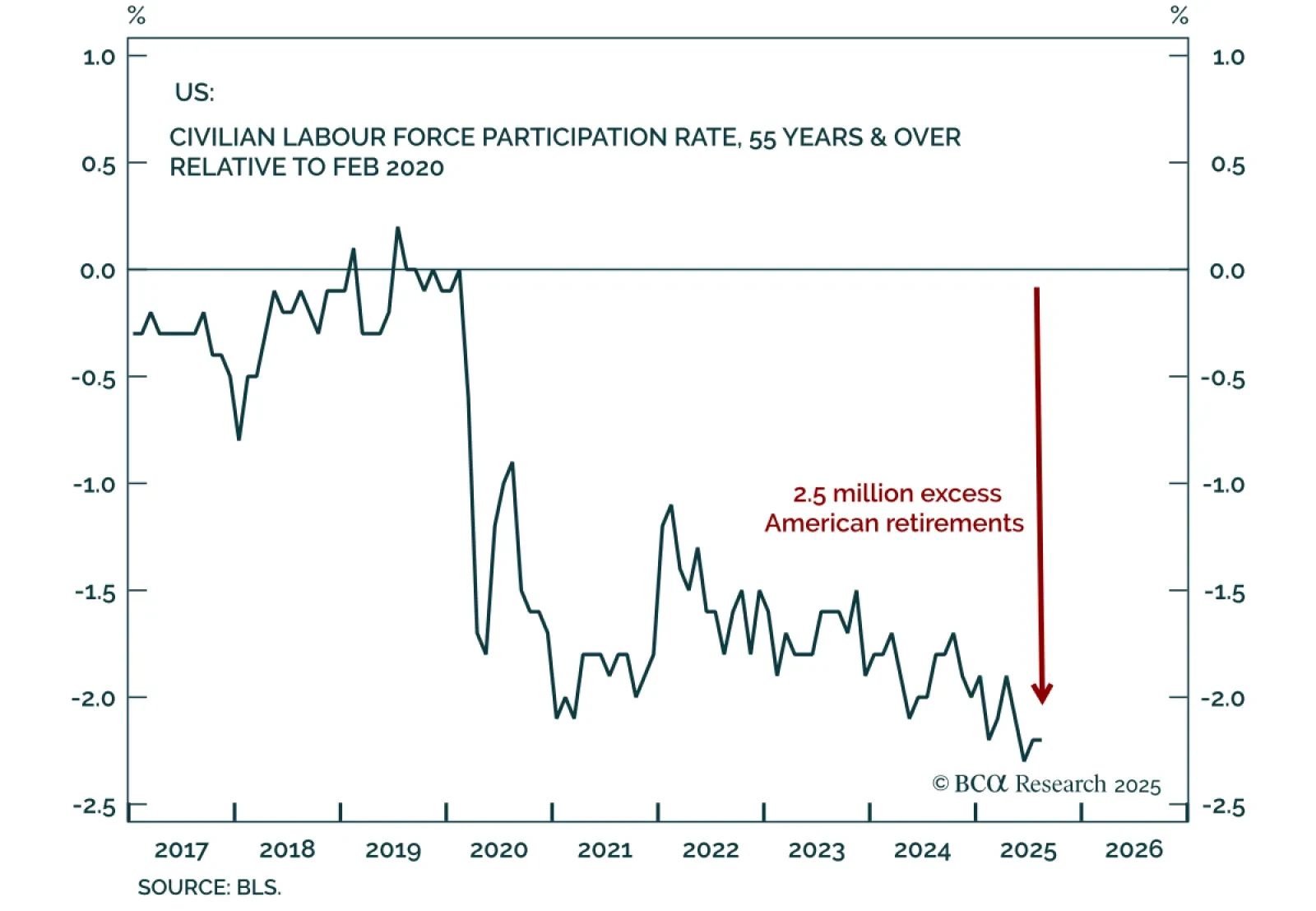

Our Counterpoint strategists recommend neutral equity exposure and underweight duration, warning that a market crash driven by fragility could drive a recession in 2026–27. A major, underappreciated structural development is the post-pandemic decline in older…

Recent Fedspeak reinforced the message from the last FOMC meeting, tempering December cut expectations but leaving the door open for more easing next year. The labor market remains the swing factor for upcoming decisions. Kansas City Fed President Schmid, who…

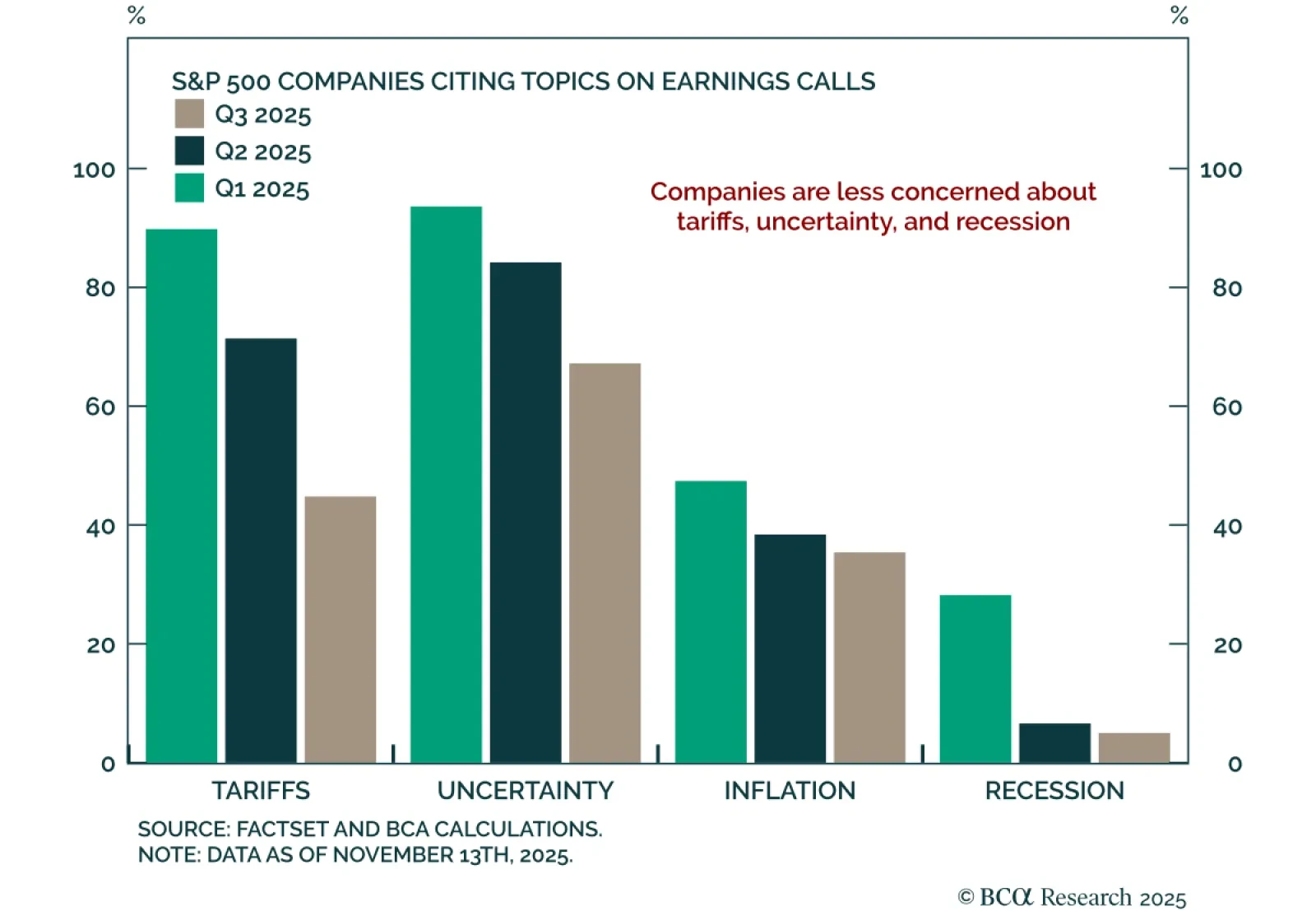

Our US Equity strategists remain constructive on equities but are watching labor market signals closely, as emerging softness could pose a risk to earnings and sentiment. With over 90% of S&P 500 companies having reported Q3 results, concerns around…

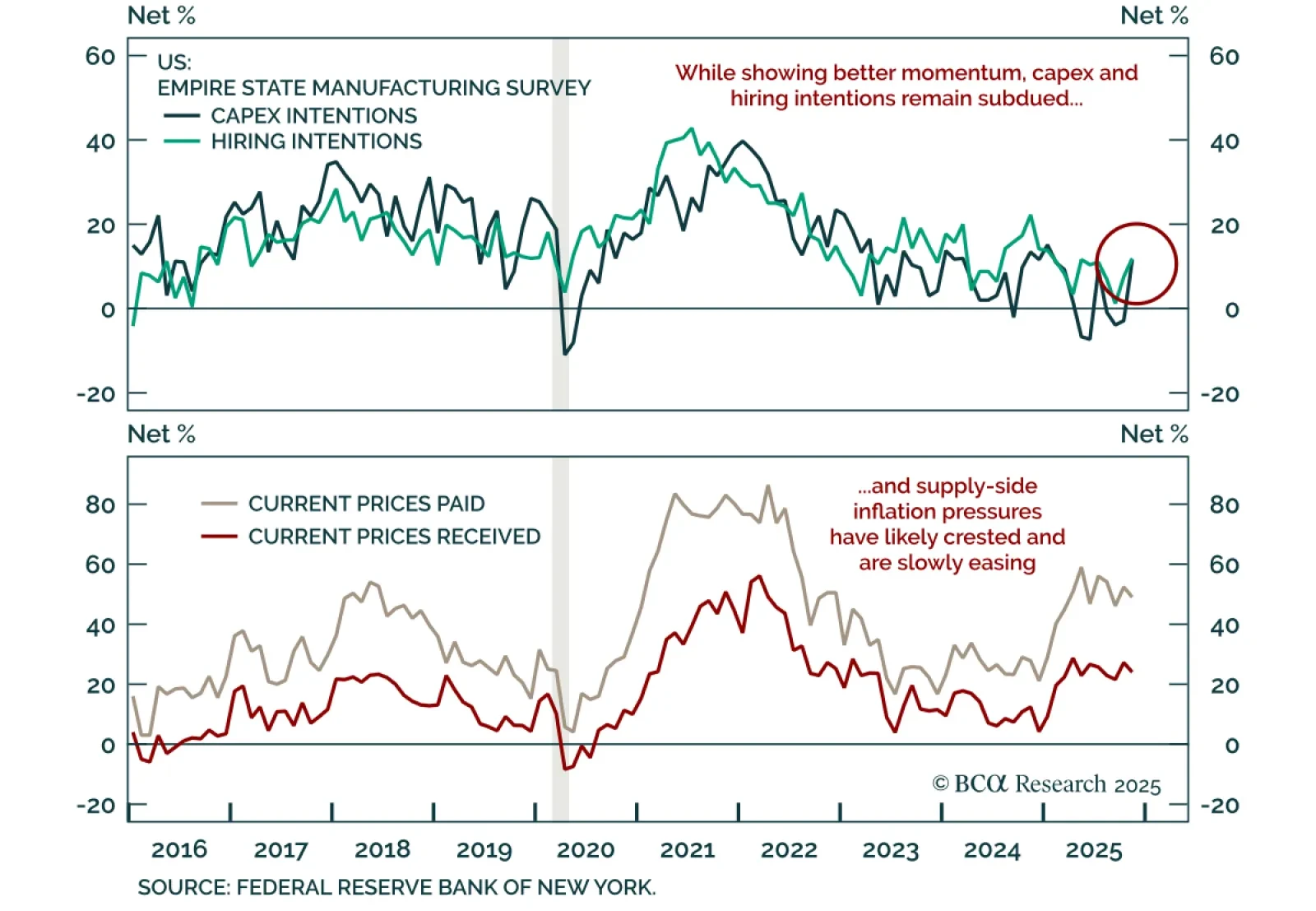

The November Empire Manufacturing survey beat expectations, rising to 18.7 from 10.7, its fourth positive reading in five months. Both new orders and shipments increased and signaled solid activity, while the employment index ticked up to 6.6. Price pressures…

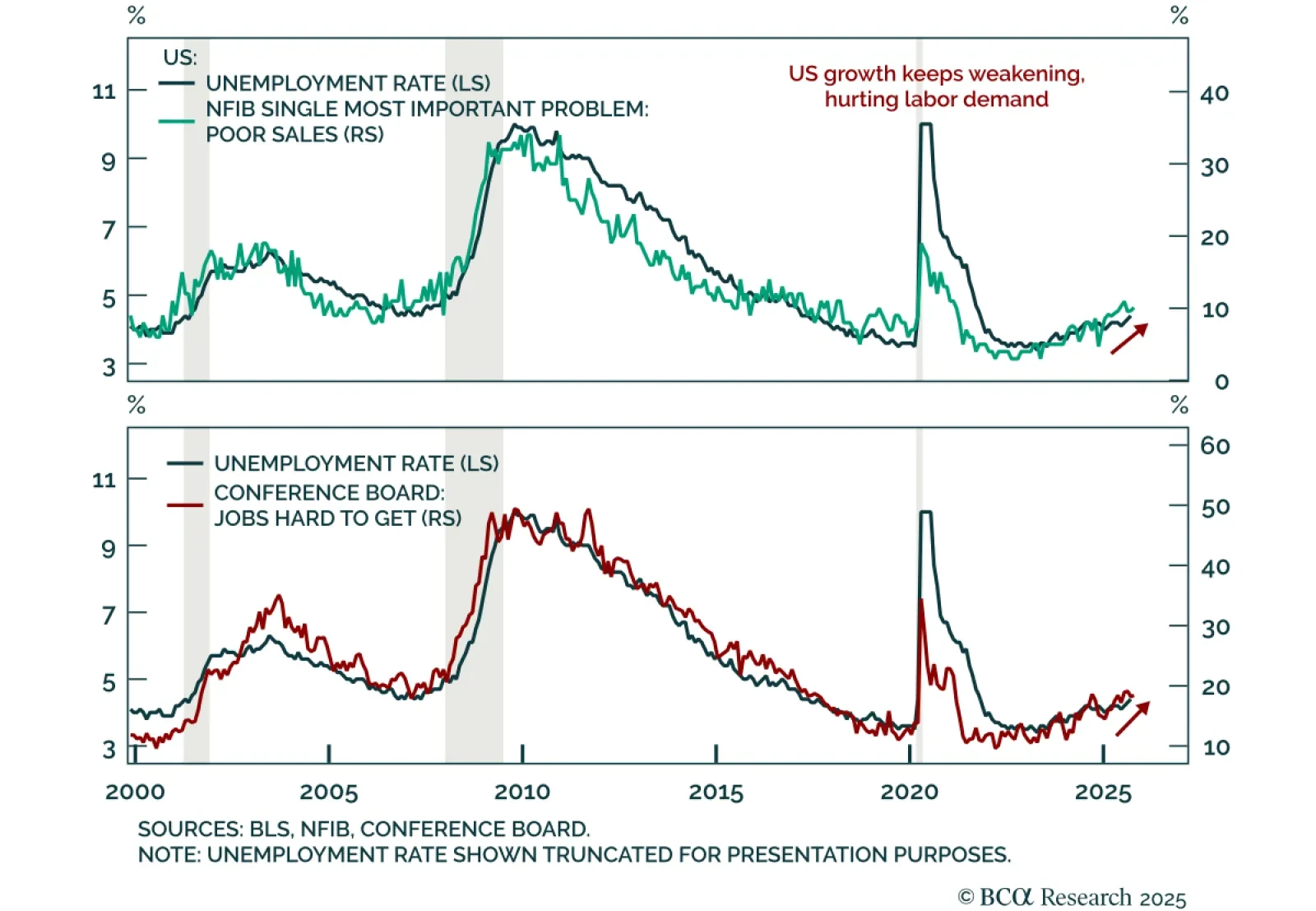

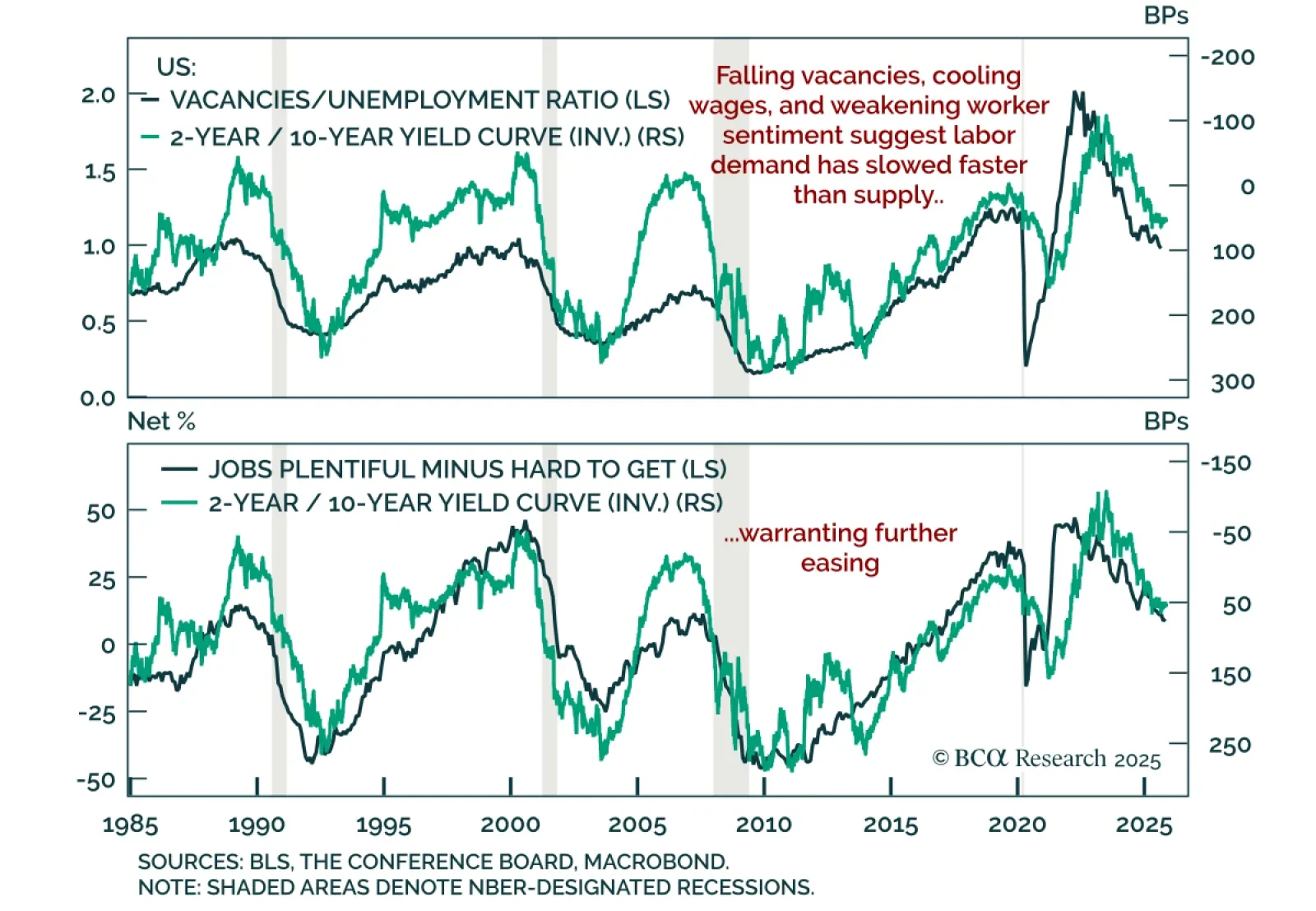

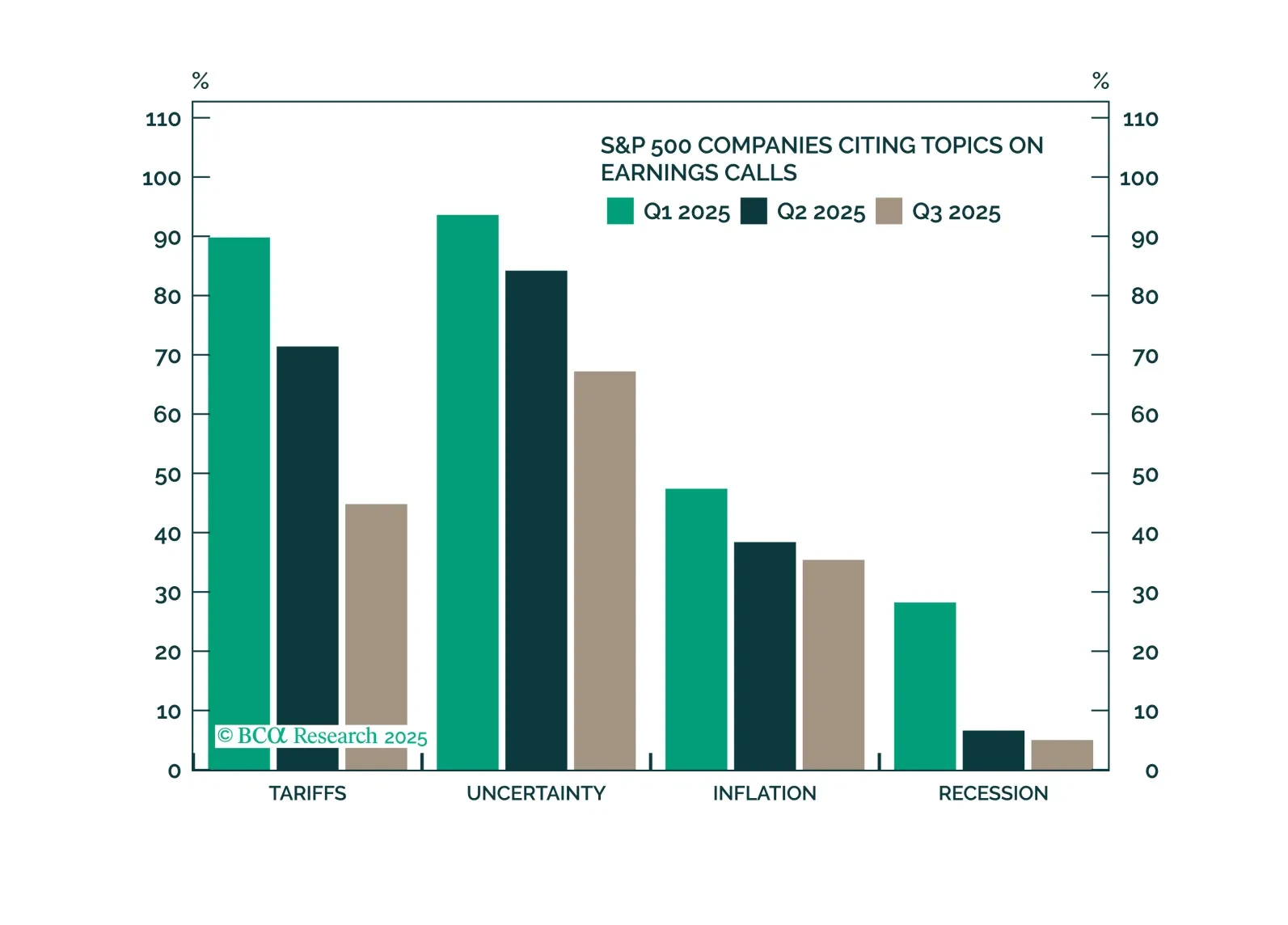

Tariffs are fading in importance as companies successfully mitigate cost pressures and preserve profitability. The recent wave of high-profile layoffs is more concerning, but there does not appear to be a systemic reason behind the announcements. However, emerging labor market softness could pose a major risk for equities. We remain vigilant.