United States

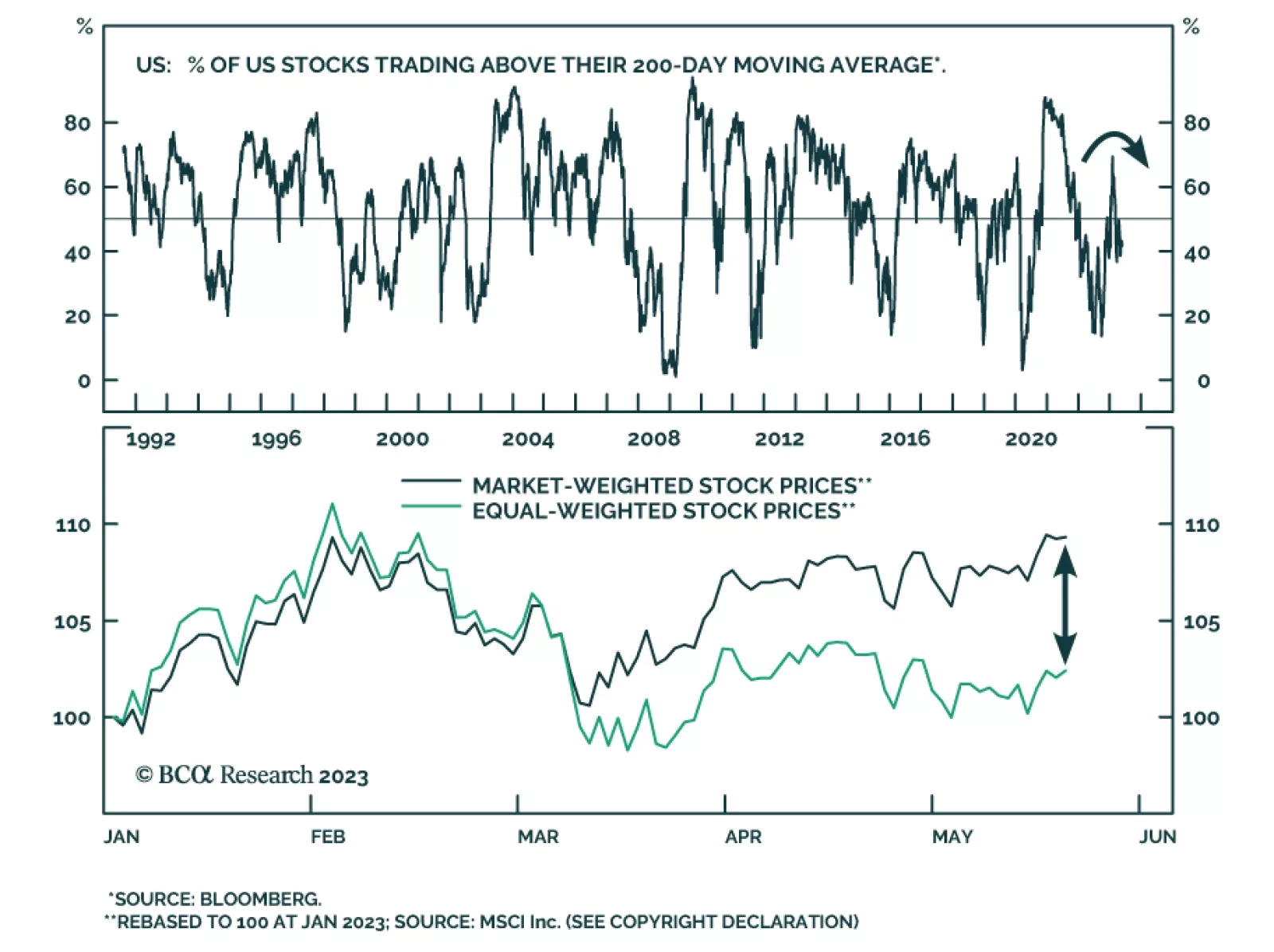

The debt ceiling game’s endpoint will avoid default only if it implies economic pain. For the Republicans, the best strategy is not to lift the debt ceiling unless the Democrats cut spending a lot, or unless the economy starts to tank. Plus: there are signs that the mania in ‘AI’ stocks has gone too far too fast.

Investors should expect high volatility and a selloff in US stocks over the short run due to the higher-than-usual risk of technical default. Investors should seek shelter in defensive sectors and large cap stocks. Long-dated Treasuries will see yields fall due to the overall macro and geopolitical context even though short-dated Treasuries will continue to suffer from policy uncertainty.

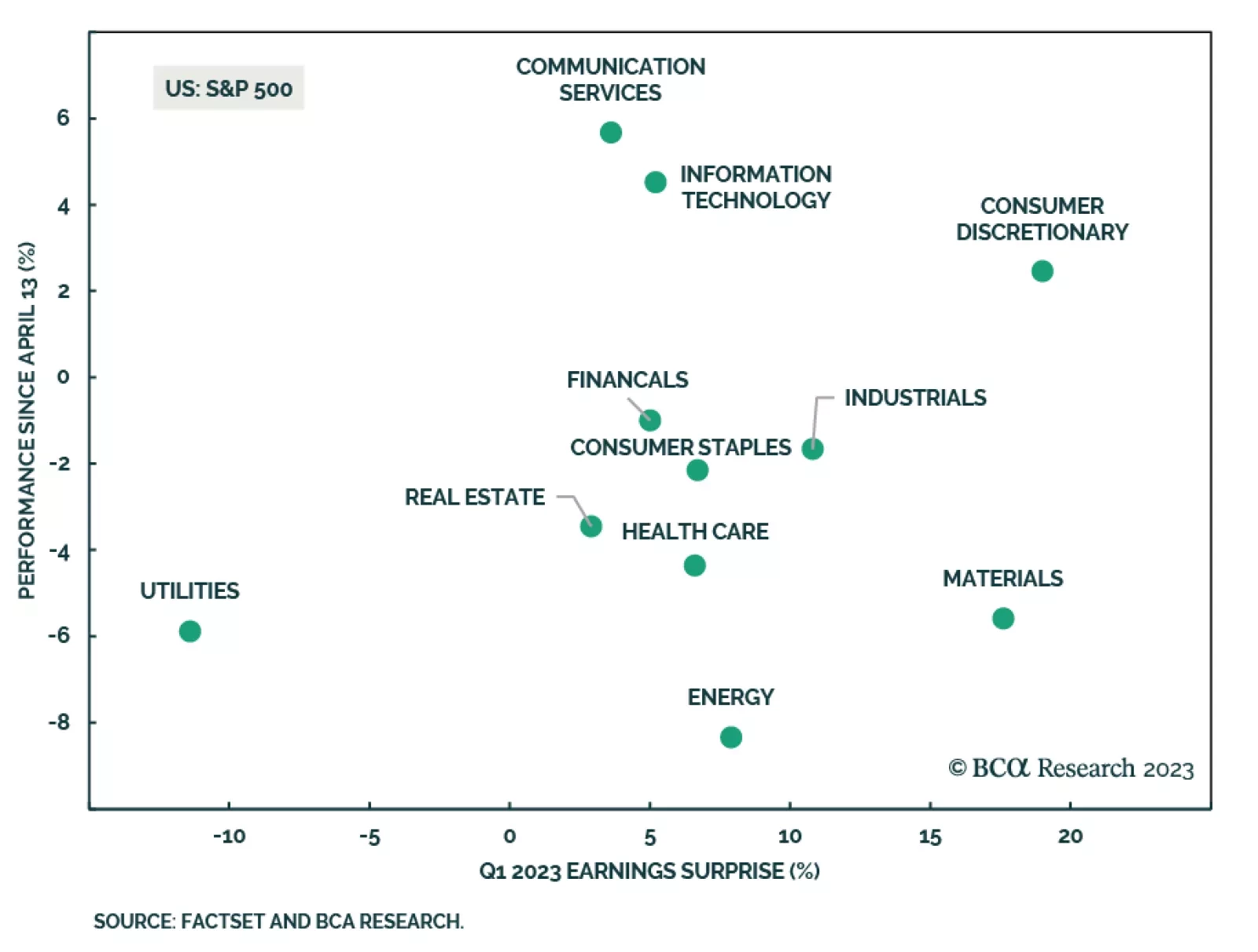

The Q1-2023 earnings season has surprised as companies’ results point to the end of the earnings recession. However, the good news is already priced in – the market has barely budged over the past six weeks. Earnings rebound may continue as long as the economy avoids a recession. However, inevitably, tighter monetary policy will weigh on demand, and recovery will come to a halt.

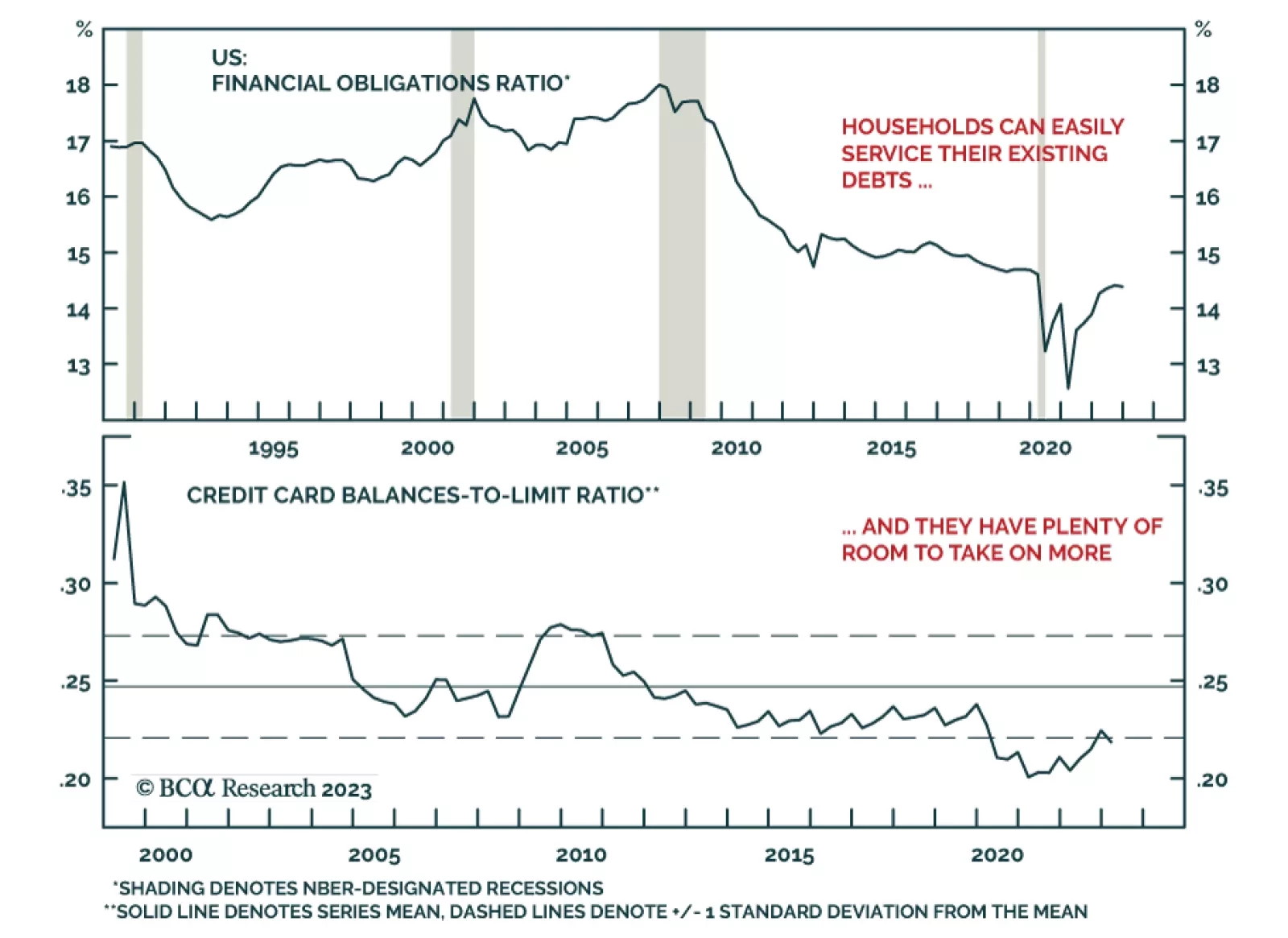

The consumption outlook remains solid thanks to households’ sizable excess savings, incomes that will be boosted by a tight labor market and ample capacity to add debt to augment their buying power.