United States

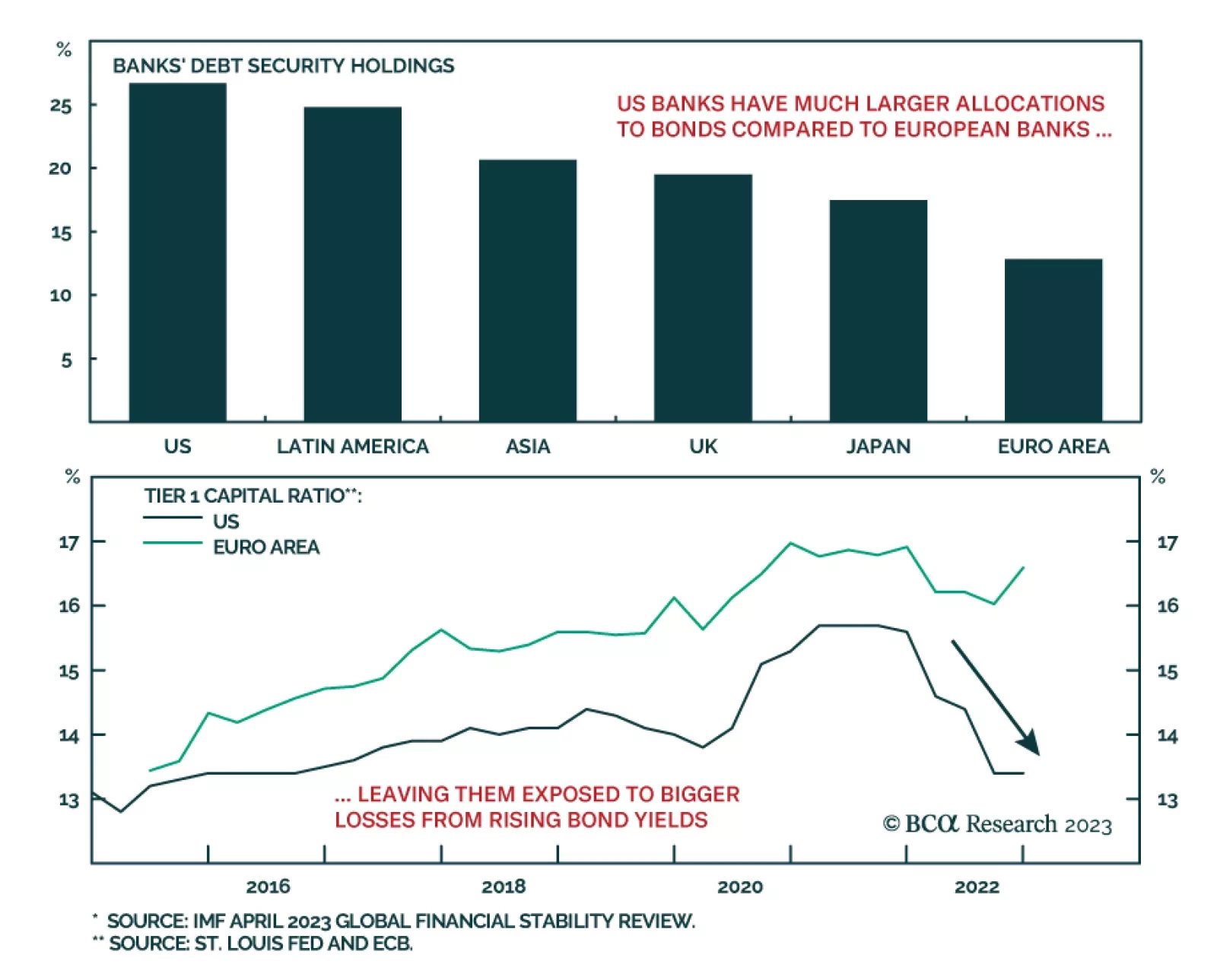

The crisis hitting regional and local banks in the US is adding to oil-price volatility and gold demand. The crisis arguably is fallout from the Fed’s aggressive monetary policy tightening, and contributes to the upending economic relationships that reliably informed policy, investments and forecasts in the past. This feeds into higher price volatility, which reduces liquidity in the short run, and impedes capex in the long run, which limits future supply growth.

April’s CPI report was soft enough to justify a Fed pause in June. However, the overall economic data still don’t justify the magnitude of rate cuts priced into the yield curve.

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.