United States

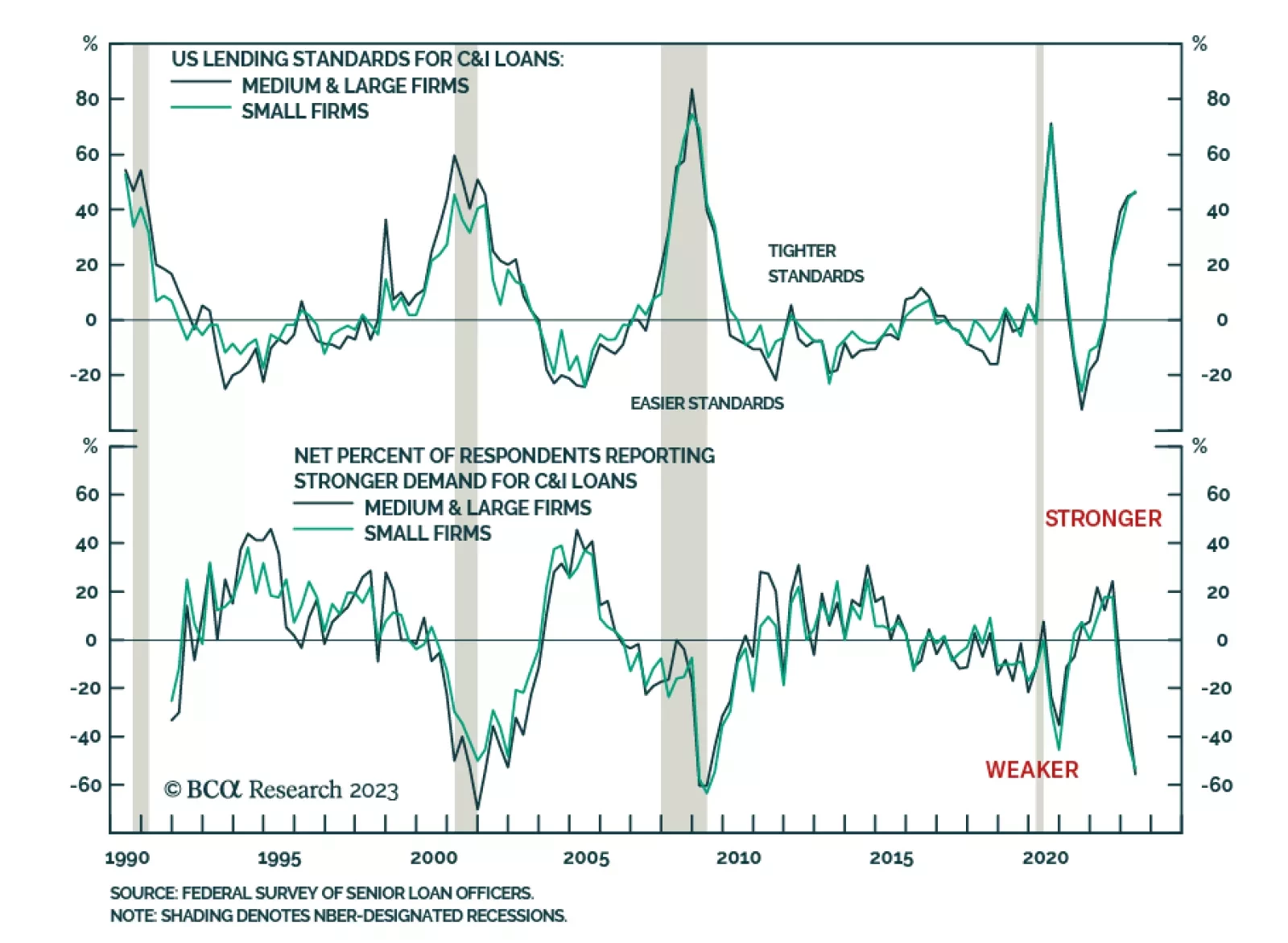

Although our take has not changed yet, the immediate emergence of a second wave of banking system stresses poses a new threat to our constructive near-term economic and market views and will have to be monitored carefully.

If the recession begins this year, it is unlikely to be mild, because inflation will not have fallen by enough to allow the Fed to cut rates aggressively. In contrast, if the recession starts in 2024 or later, when inflation is likely to be much lower, the Fed will be able to cushion the blow. Our base case remains a 2024 recession but the risks around that view have increased in light of recent banking stresses.

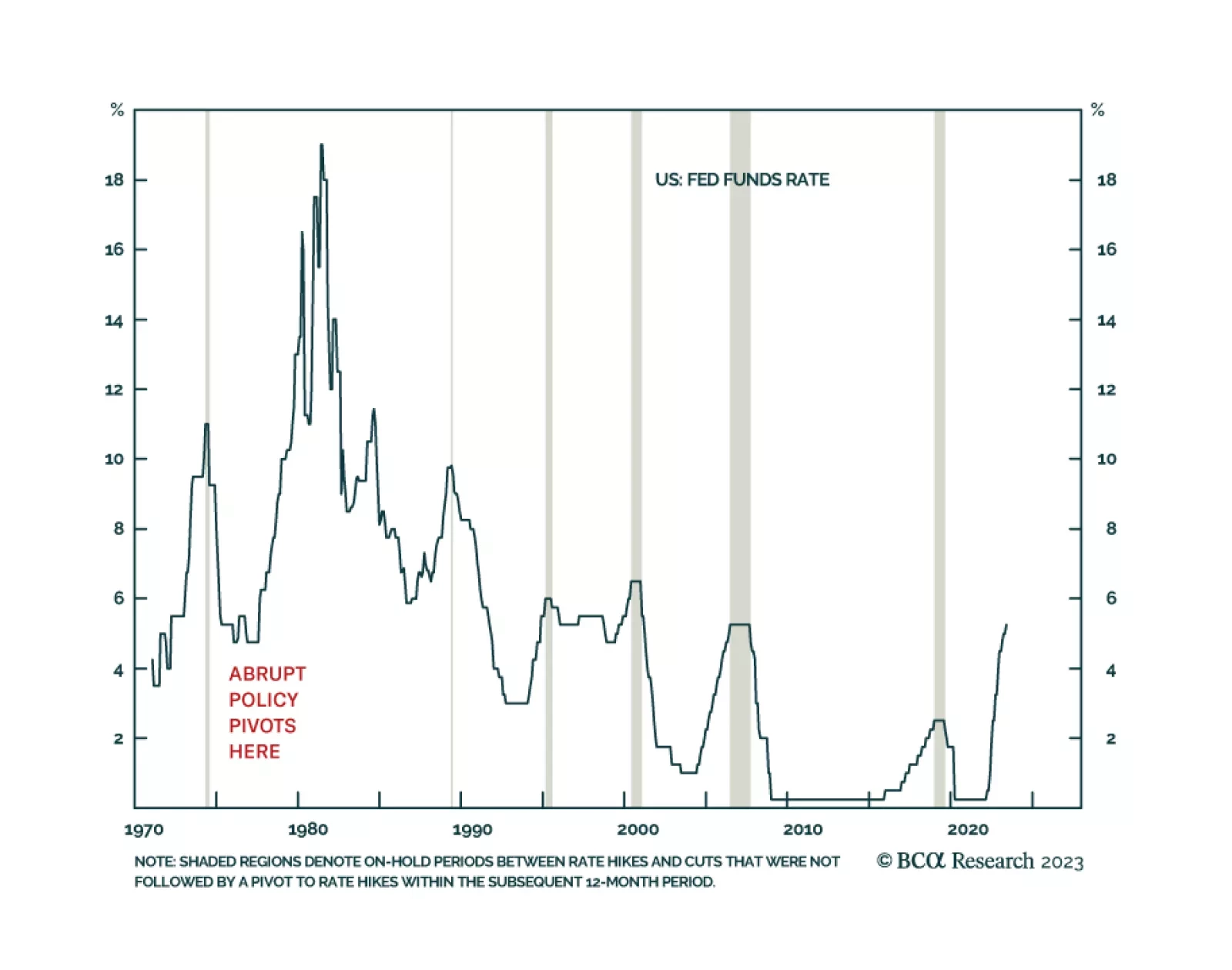

The Fed hiked 25 basis points at yesterday’s FOMC meeting while also signaling that the tightening cycle is now on hold. We discuss the short-run and long-run implications for Treasury yields.