United States

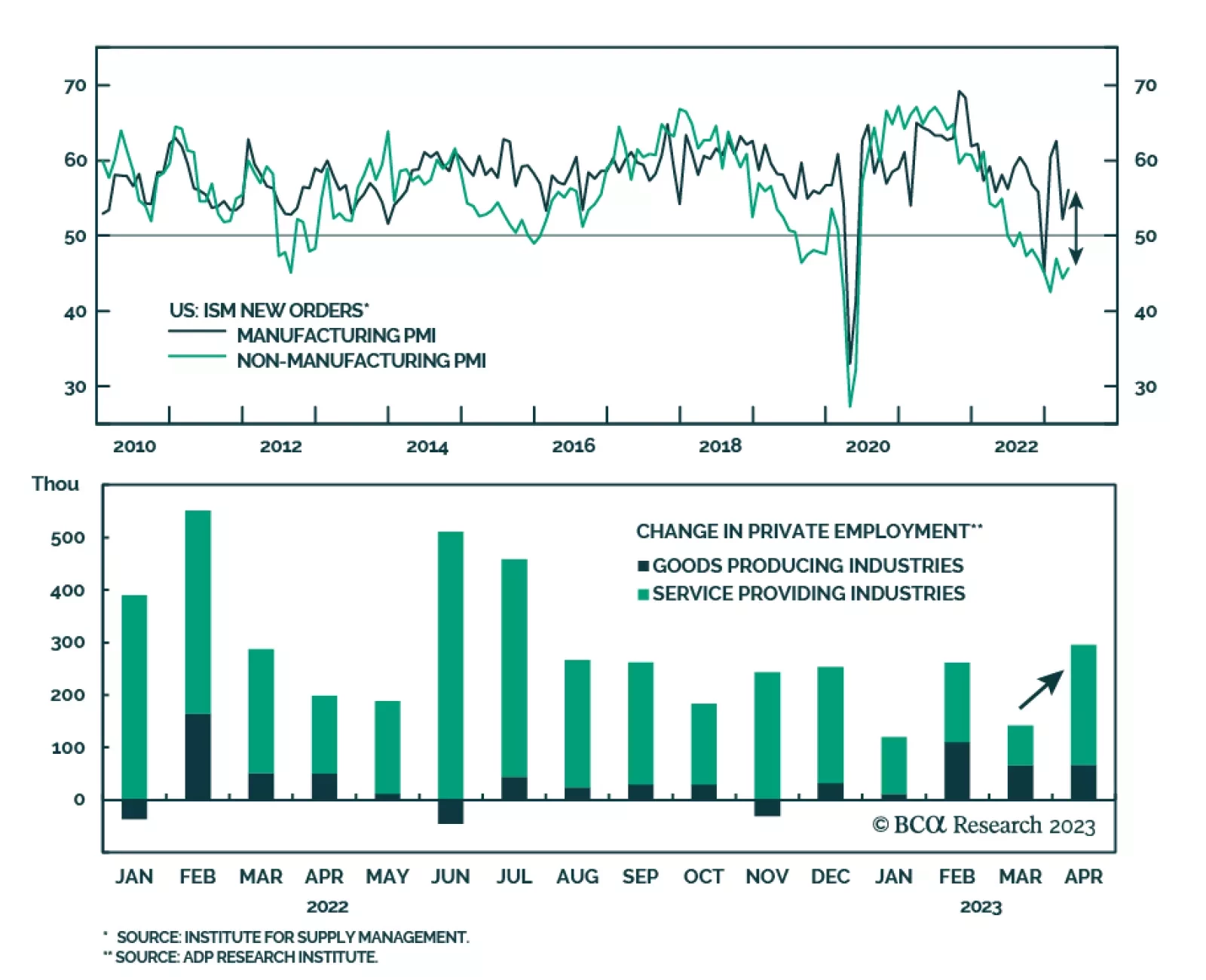

Data released on Wednesday confirm that the US services sector remains a source of resilience in the US economy. Both the ISM Services Index as well as the final estimate of the alternative S&P Global Services PMI moved further above 50 in April,…

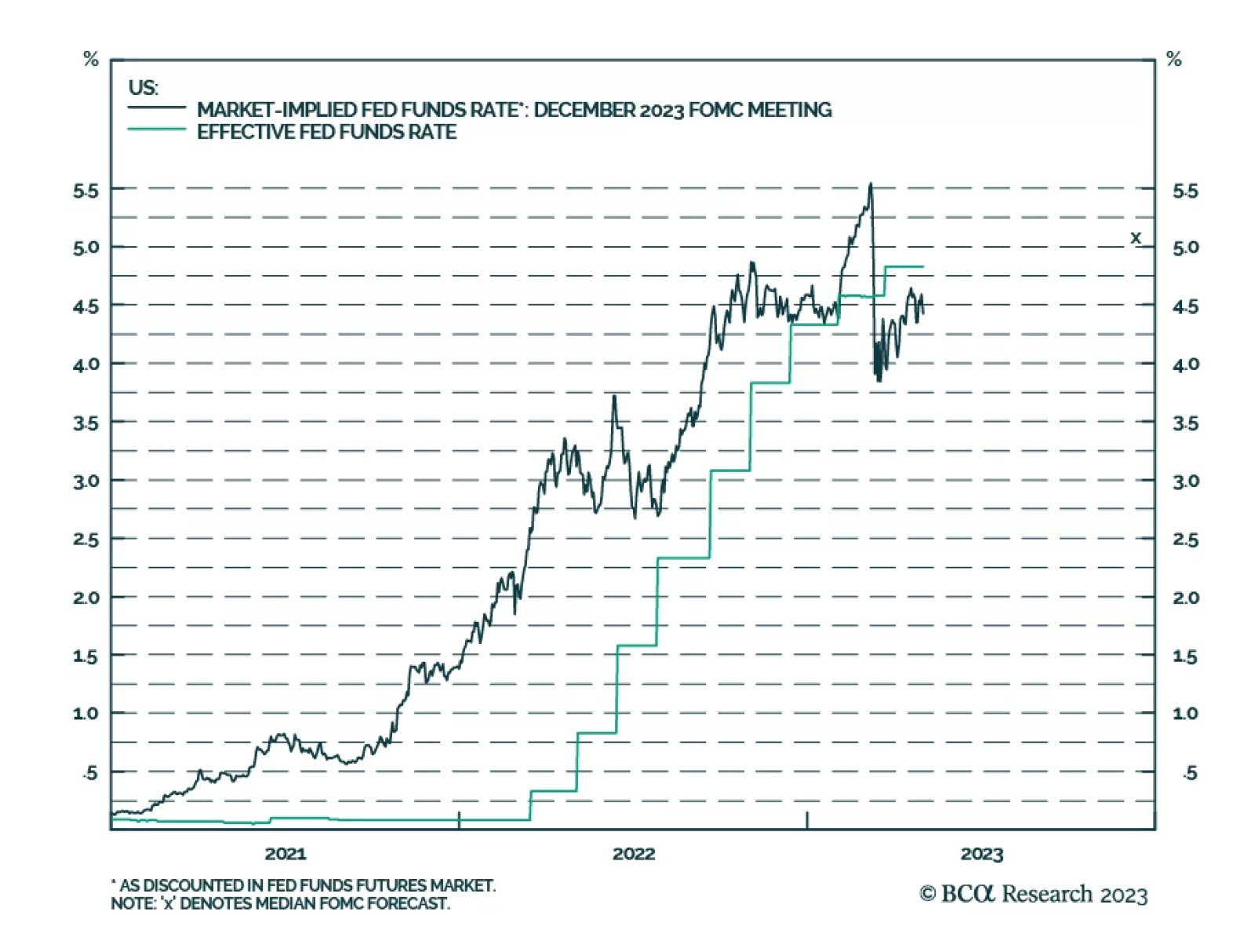

As expected, the Fed delivered a 25bps rate hike on Wednesday. However, the FOMC statement and Chair Jay Powell’s post-meeting remarks signaled that this increase may mark the end of the tightening cycle. Notably, the sentence indicating that “the…

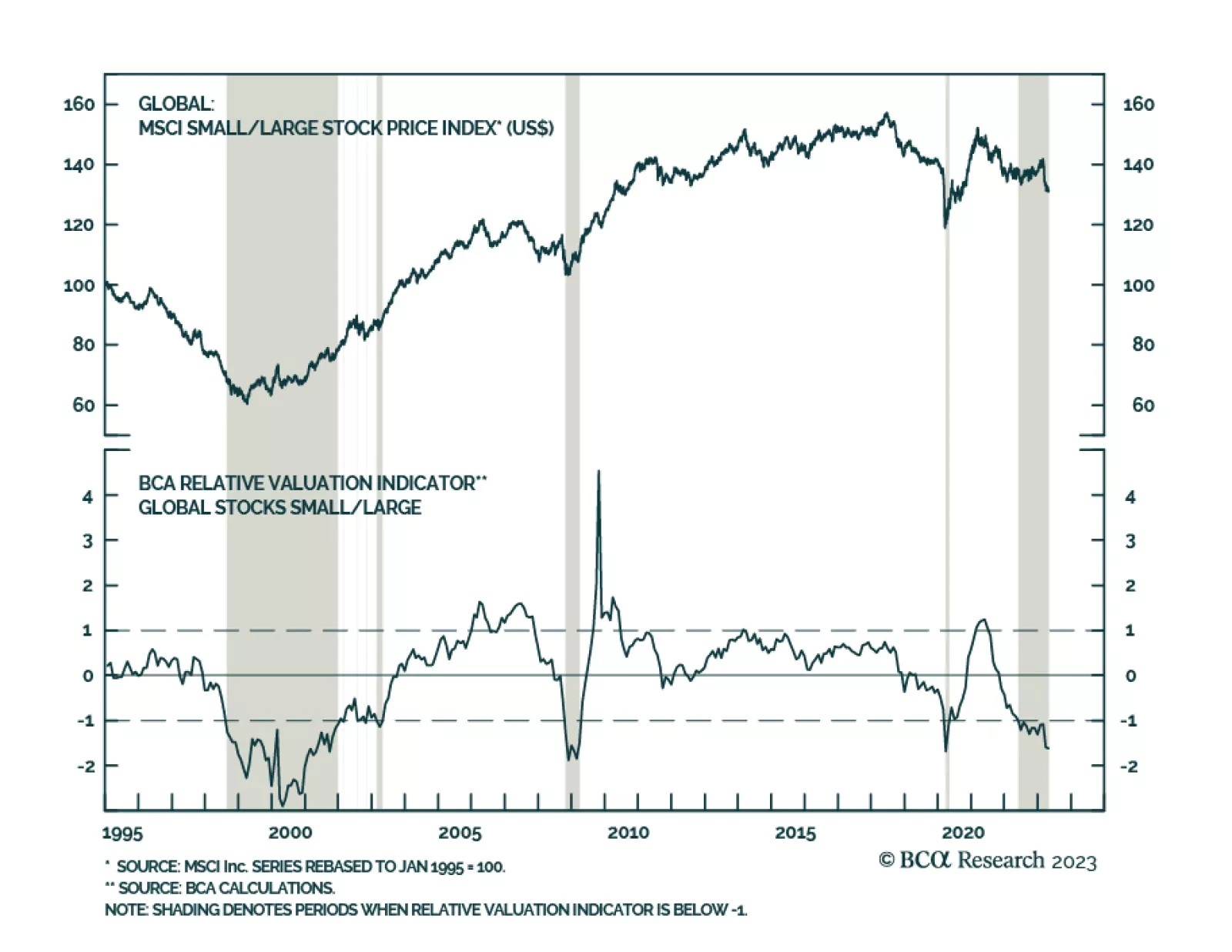

Global small cap stocks have underperformed large caps by roughly 7% since the beginning of March, in response to concerns about the global banking system. Smaller firms are generally less able to access funding through capital markets, and thus are more…

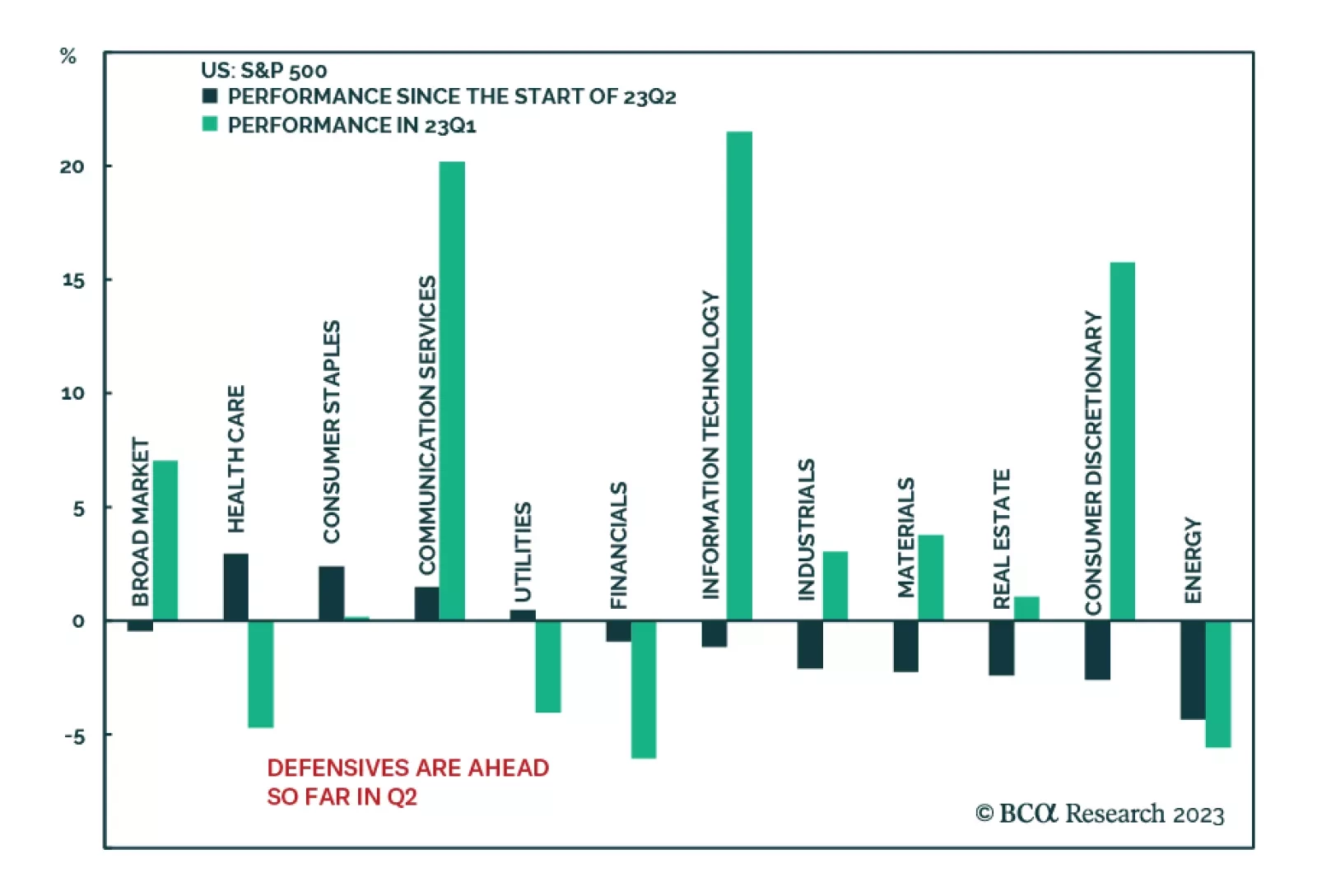

The S&P 500 is broadly unchanged from where it was at the end of Q1. It ended the day on Wednesday 0.5% below its level on the last day of March. However, the calm surface conceals some subterranean activity. Specifically, a selloff across cyclical…

As the Fed meets today, we explain what it did wrong in 1970, 1974, and 1980 that prevented inflation from being exorcised, and the lessons for 2023-24. Plus, we identify a currency cross that could rebound in the next year.

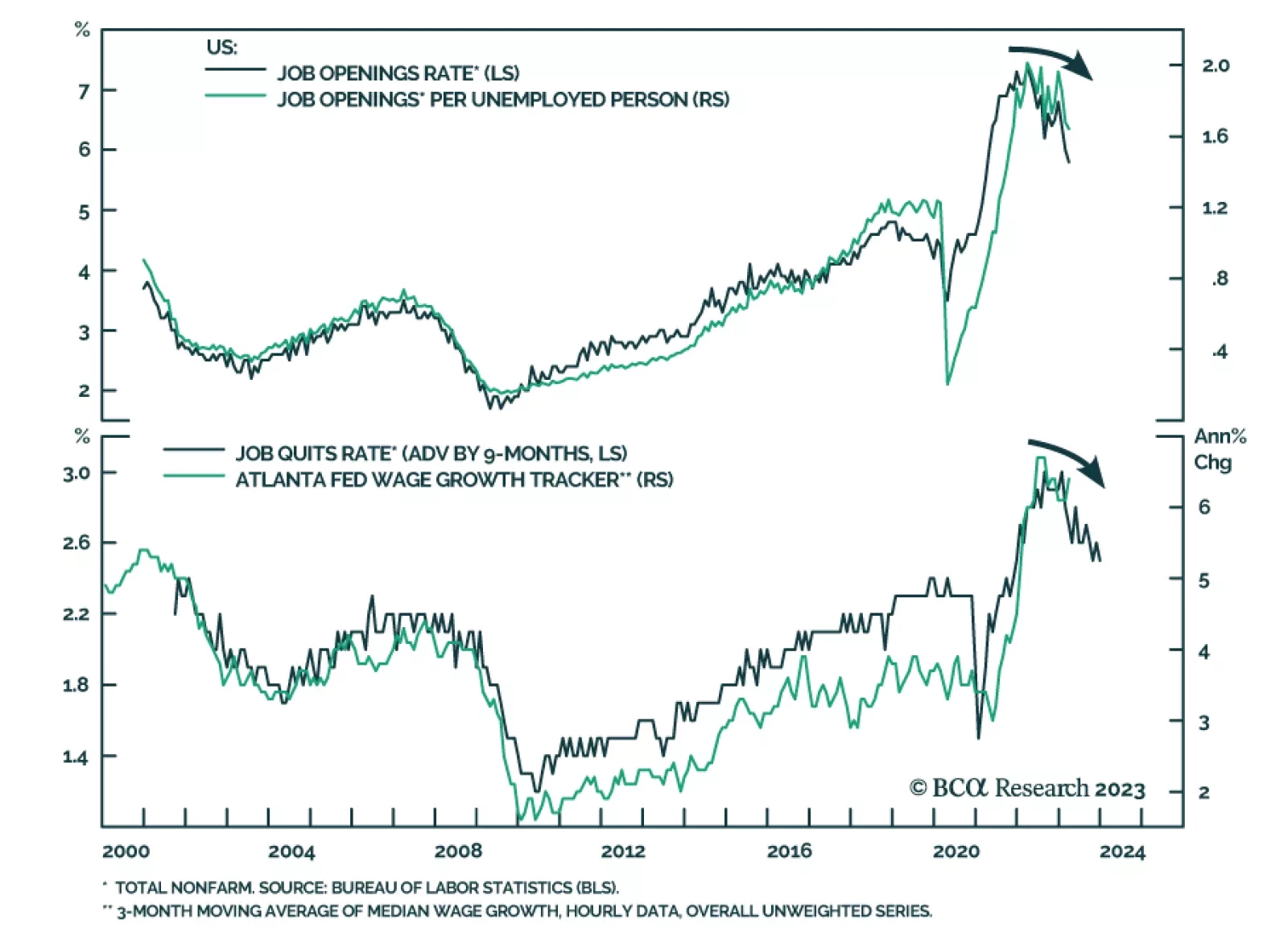

The JOLTS survey for March showed a continued softening of the US labor market. Job openings fell from 9.97 million to 9.59 million – below expectations of a more muted decline to 9.74 million. While job openings remain historically elevated, the March update…

First Republic (FRC) became the third large-cap bank to fold when regulators seized it over the weekend. Investors took the news in stride on Monday, but several large- and mid-cap regional banks sold off sharply on Tuesday. Our US Investment Strategy…

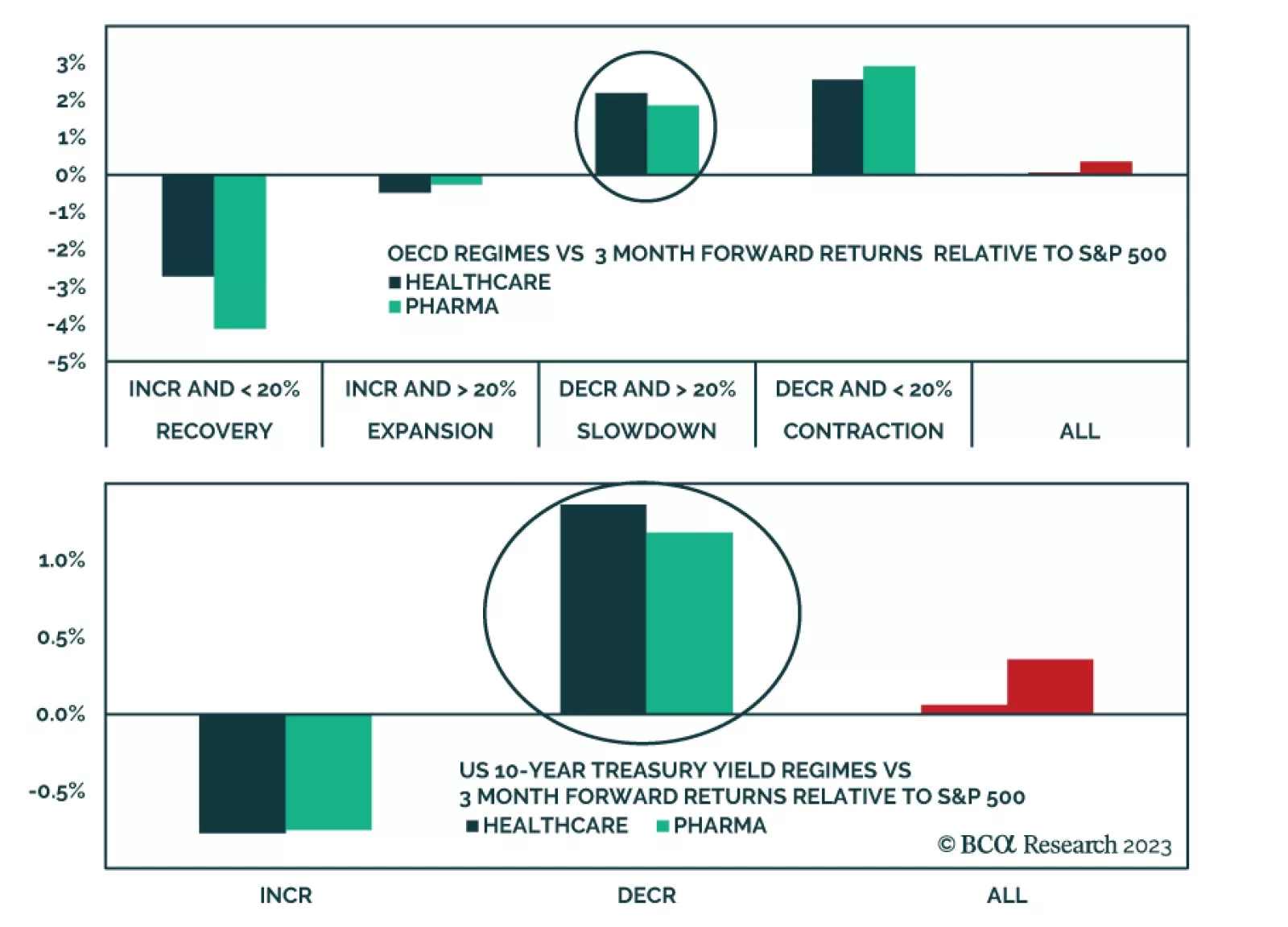

According to BCA Research’s US Equity Strategy and US Political Strategy services, the macro backdrop is favorable for Pharma. as it tends to outperform the market during the slowdown and contraction stages of the business cycle. Q1-2023 GDP came in weaker…

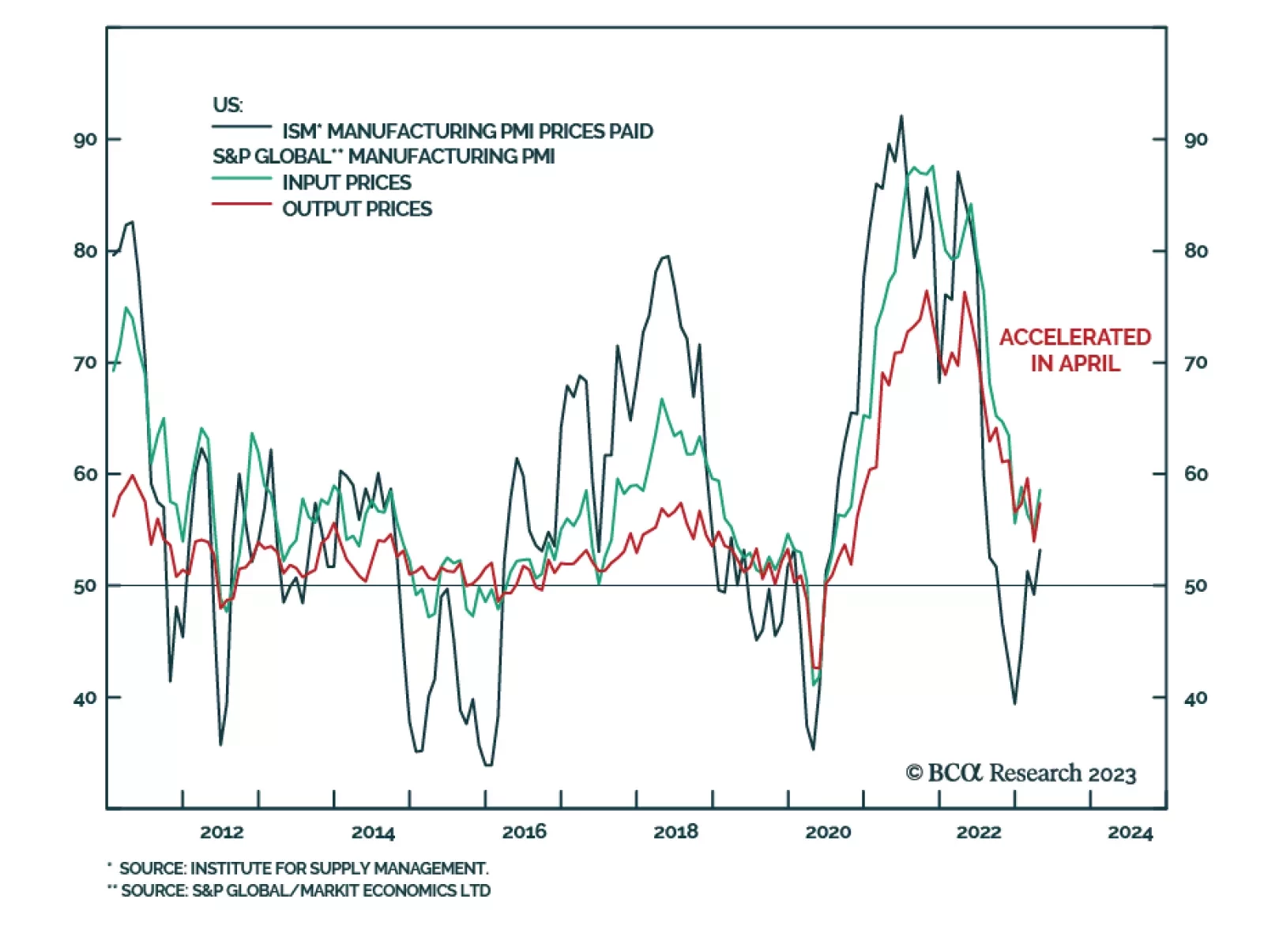

The April update of the ISM PMI continues to indicate that the US manufacturing sector is weak. Although the headline index increased 0.8 points to 47.1, it remains below 50 in contraction territory and near March’s 22-month low of 46.3. Two of the three…

The risk-reward of the US dollar is currently positive. If a US recession is not imminent, then US bond yields will move higher, thus supporting the greenback. If the US enters a recession soon, the US dollar will benefit because it is counter-cyclical. Besides, the US dollar has not been as weak as the DXY index suggests.