United States

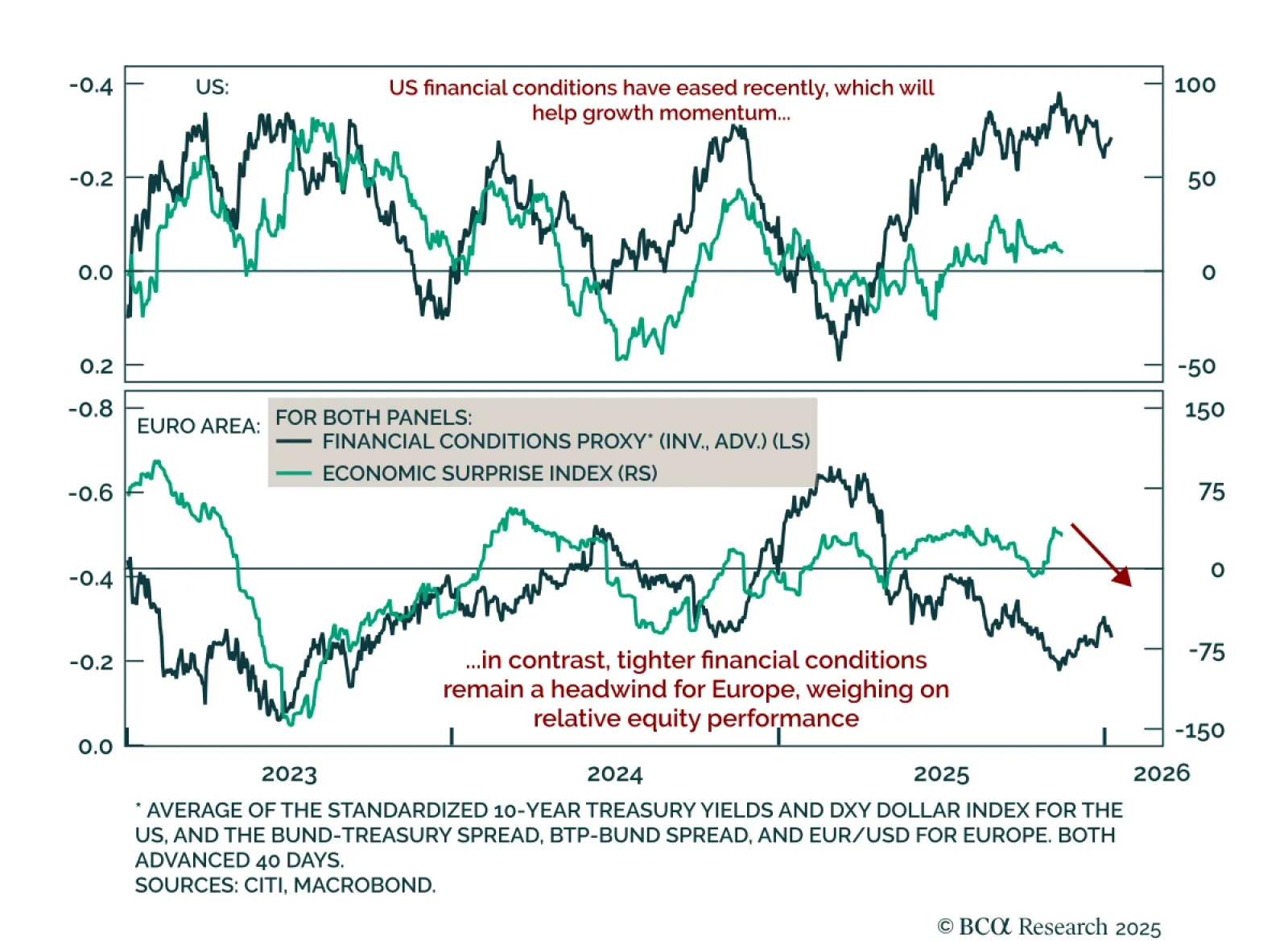

European sentiment remains mixed, with growth momentum failing to pick up despite brighter long-term prospects. Economic surprises have improved since mid-October, but tight financial conditions, driven by a strong euro and higher Bund yields since the start…

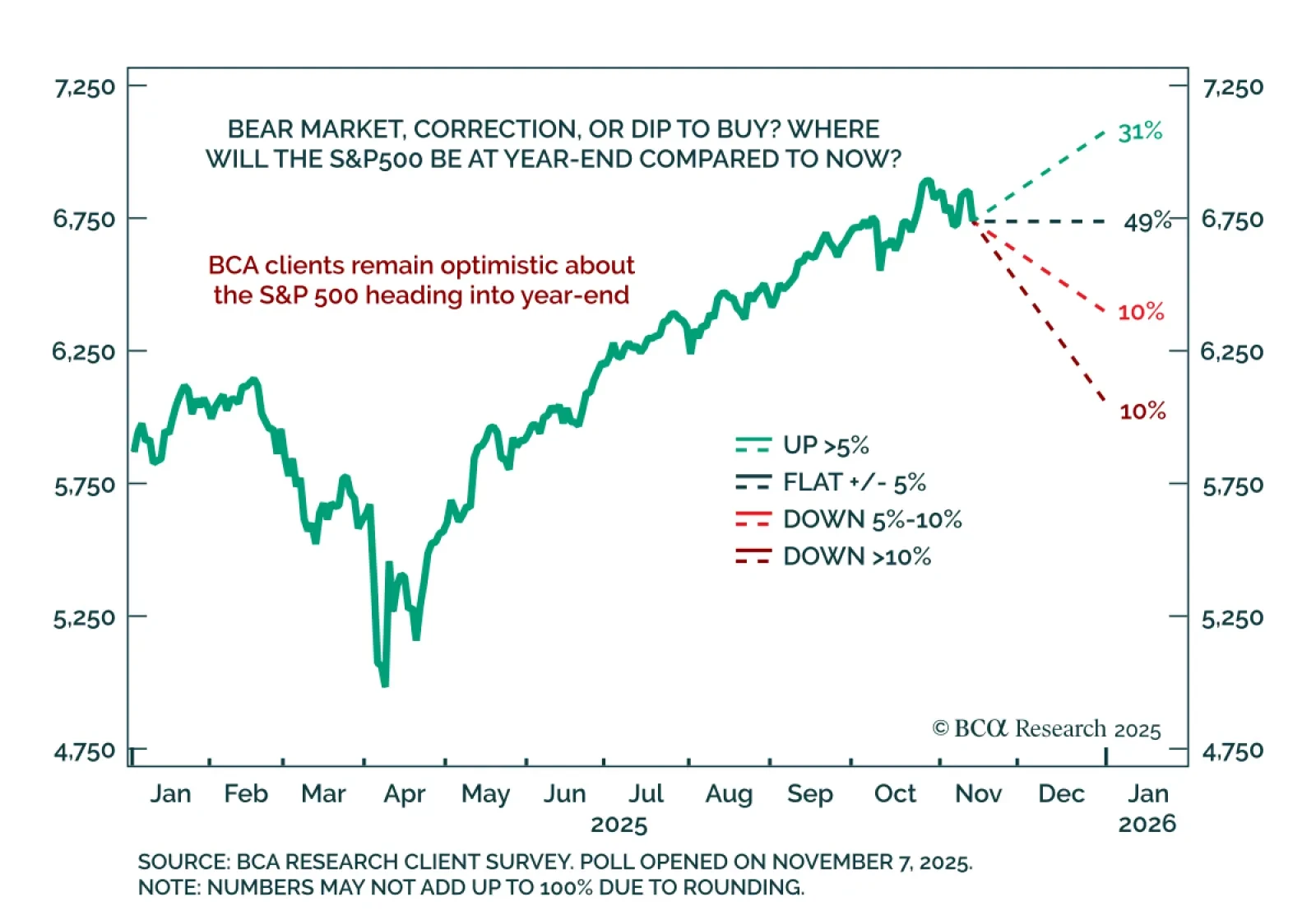

The S&P500 has fallen by 2% from its peak, but BCA clients see this as little more than a blip. In the latest weekly poll on the Have Your Say section of BCA's website, we asked our clients whether the recent stock market softness is the start of a bear…

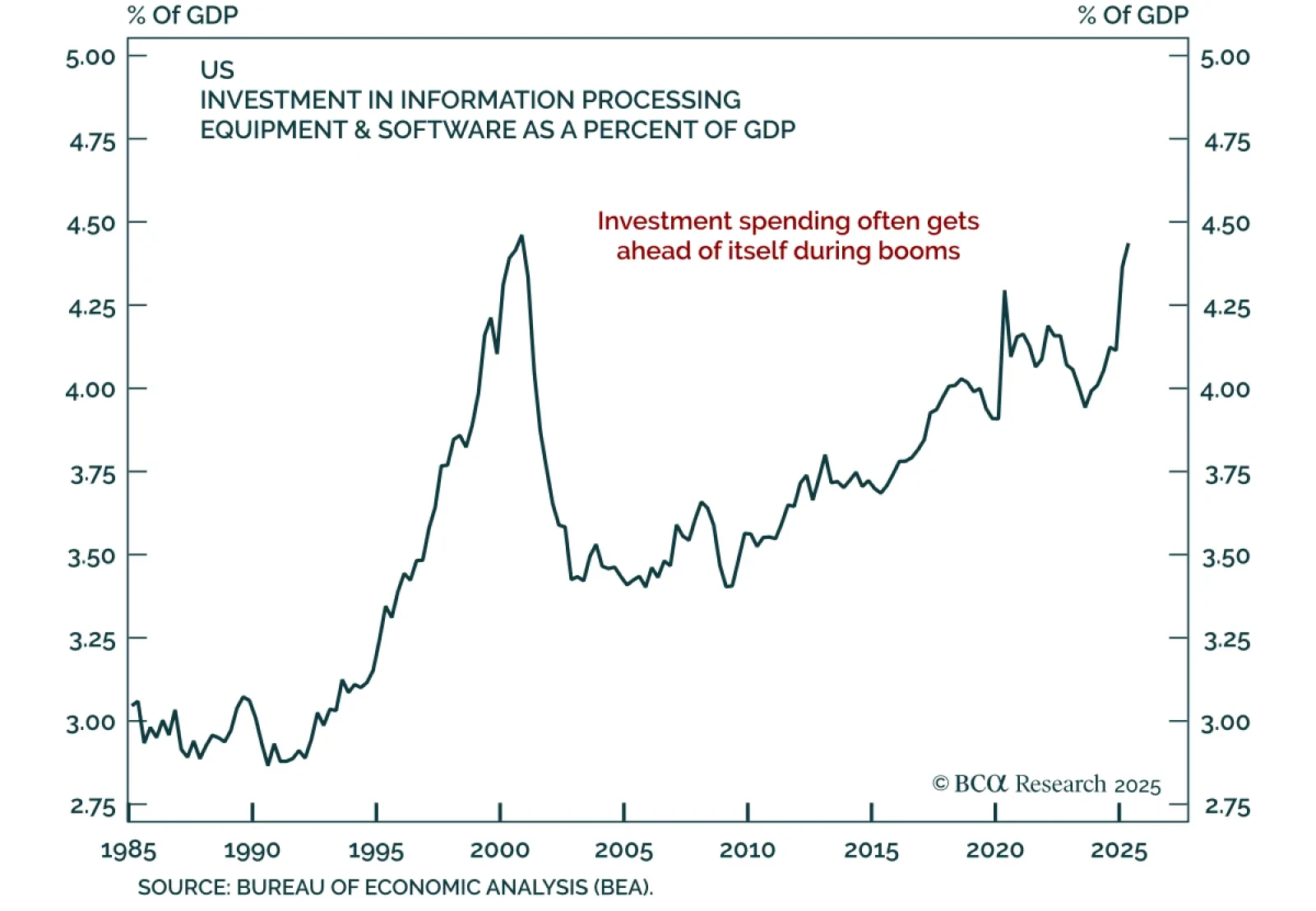

Our Global Investment strategists see the AI boom tracking historical capex bubbles and expect it to peak within the next 6 to 12 months. Drawing lessons from the railway, electrification, internet, and oil booms, they warn that investment manias tend to…

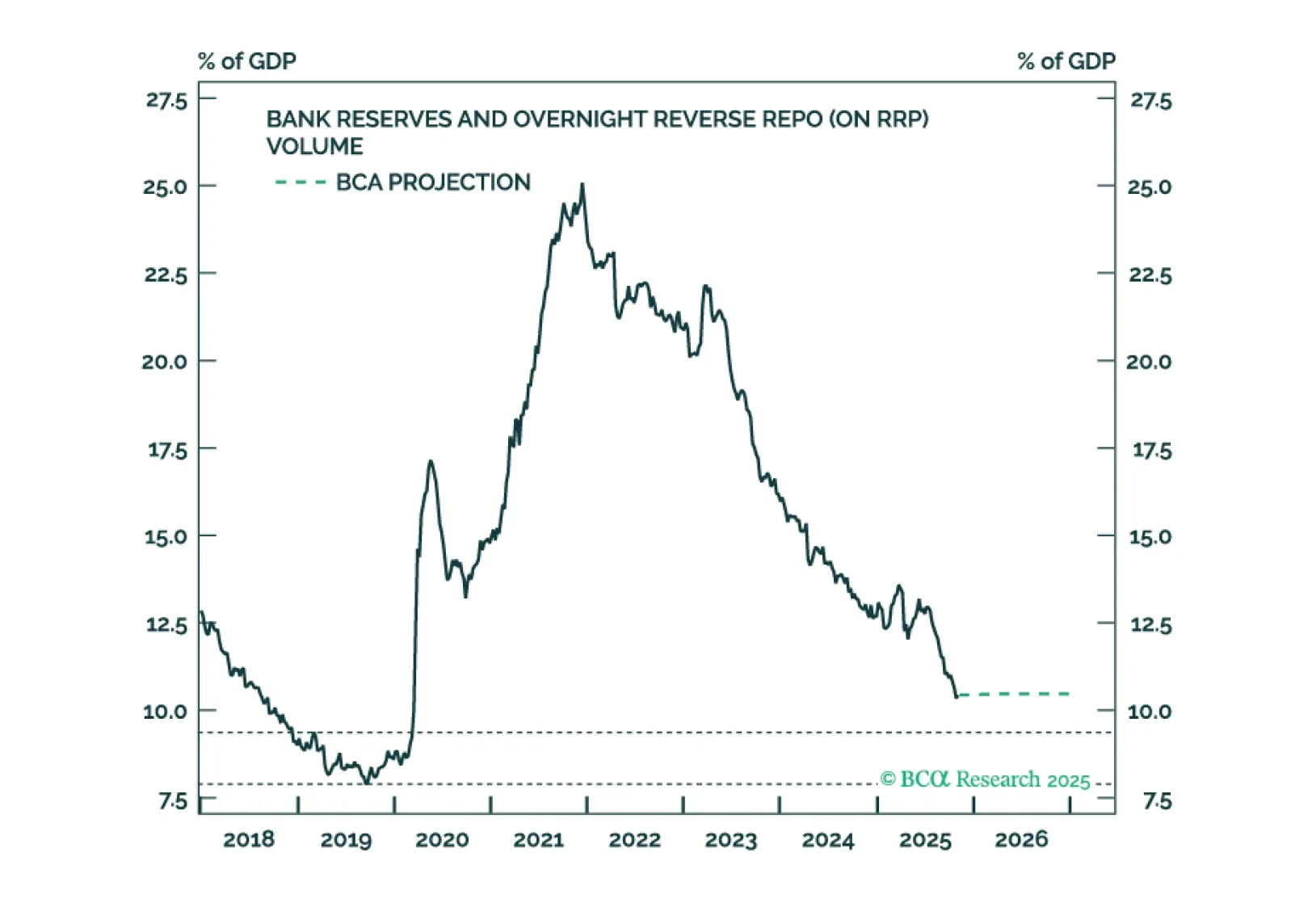

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

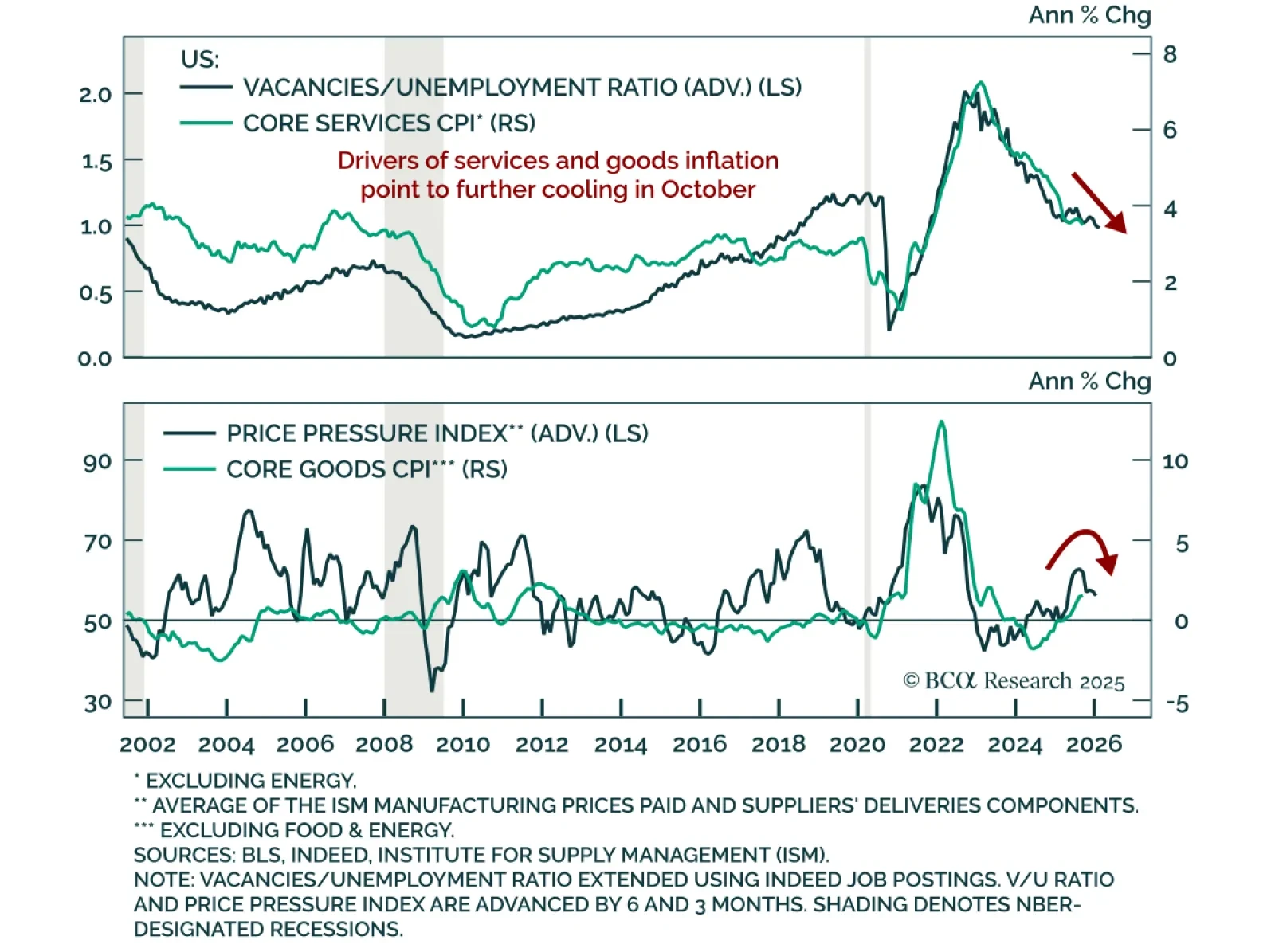

The White House announced the October jobs and CPI reports are unlikely to be released due to the government shutdown, but alternative indicators already point to weaker labor and inflation momentum. The labor market was stalling, though not collapsing,…

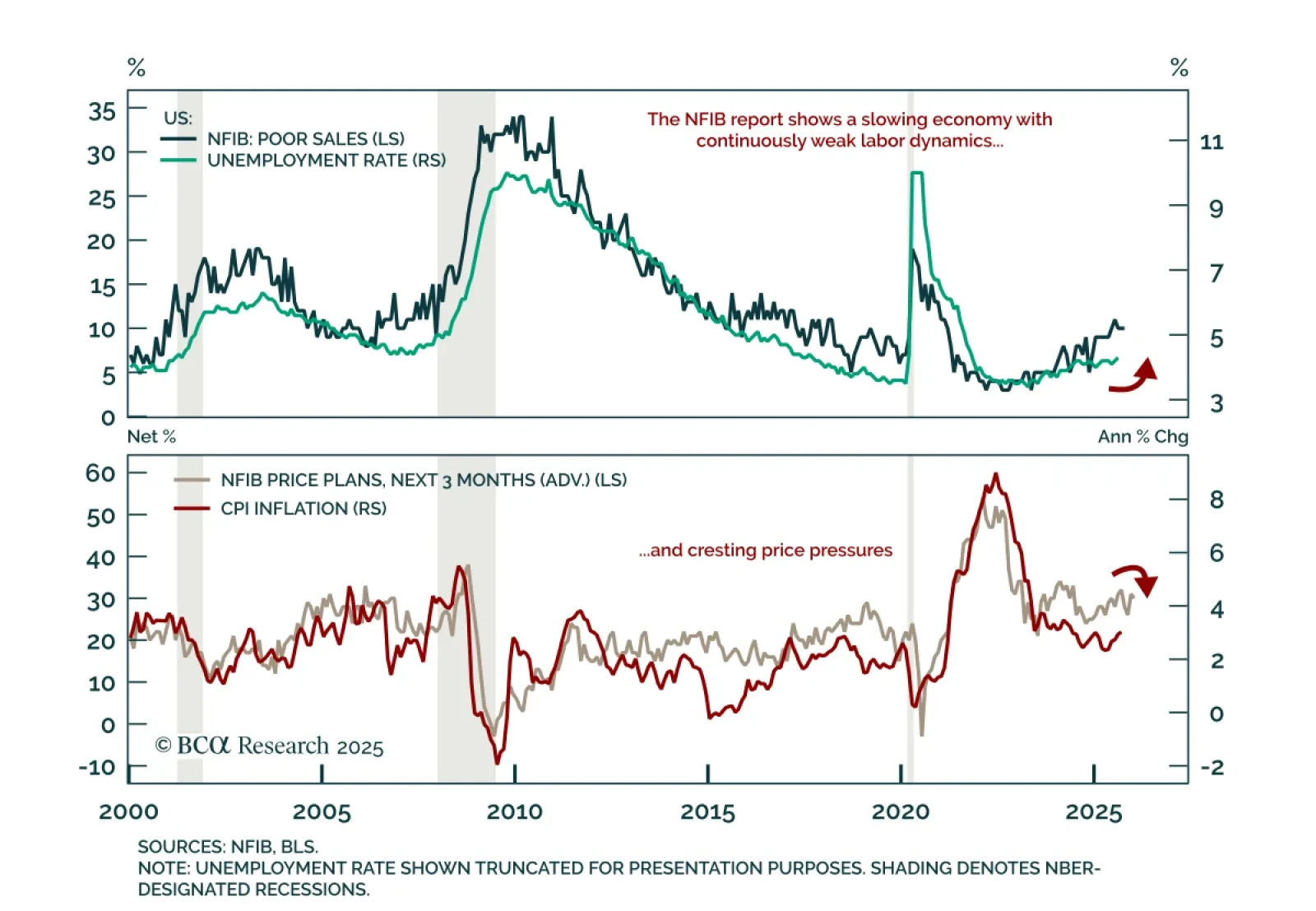

The October NFIB Small Business Optimism Index missed estimates, ticking down to 98.2 from 98.8, reflecting softer expectations and earnings. Lower earnings were driven by both weaker sales volumes and higher costs. The share of small businesses citing poor…

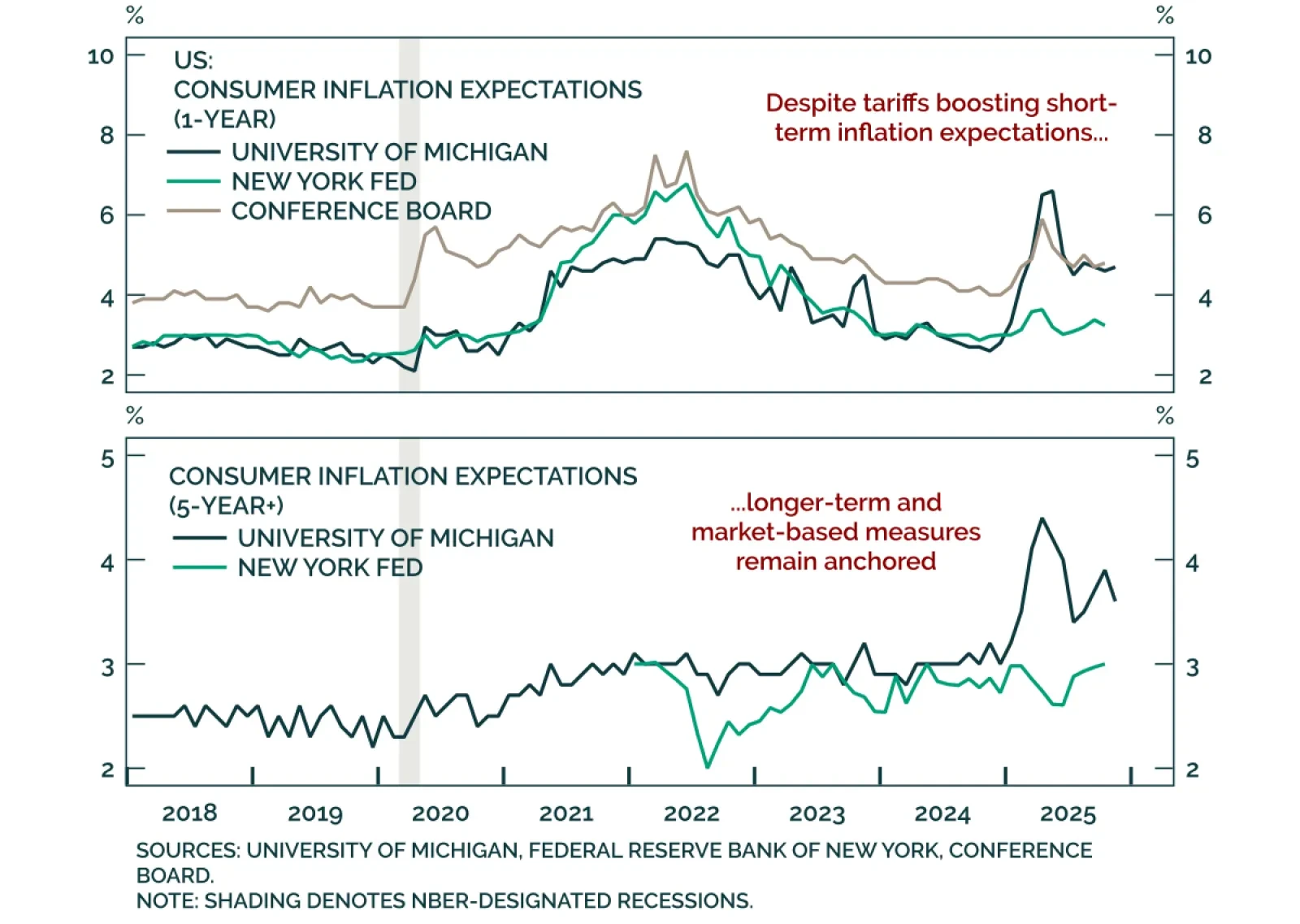

Inflation expectations remain central to monetary policy frameworks, as they hinge on central bank credibility and shape policy responses. After years of persistent disinflation and zero lower bound constraints between the GFC and the pandemic, policymakers…

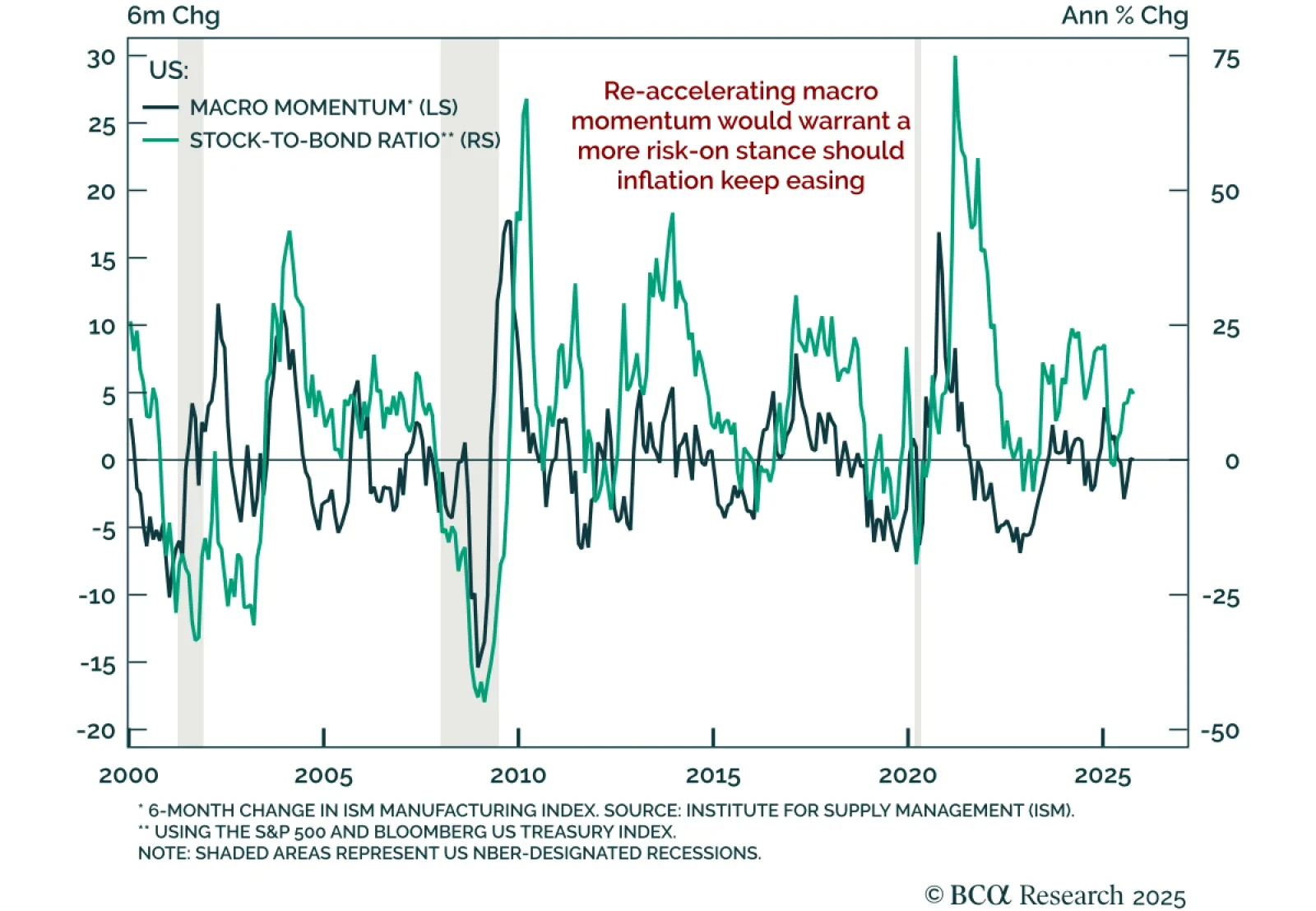

Macro momentum remains neutral, with the latest ISM Manufacturing PMI showing stabilizing yet still weak growth. The headline index missed expectations and continued to signal contraction, but new orders, which usually lead the headline, improved. Regional…

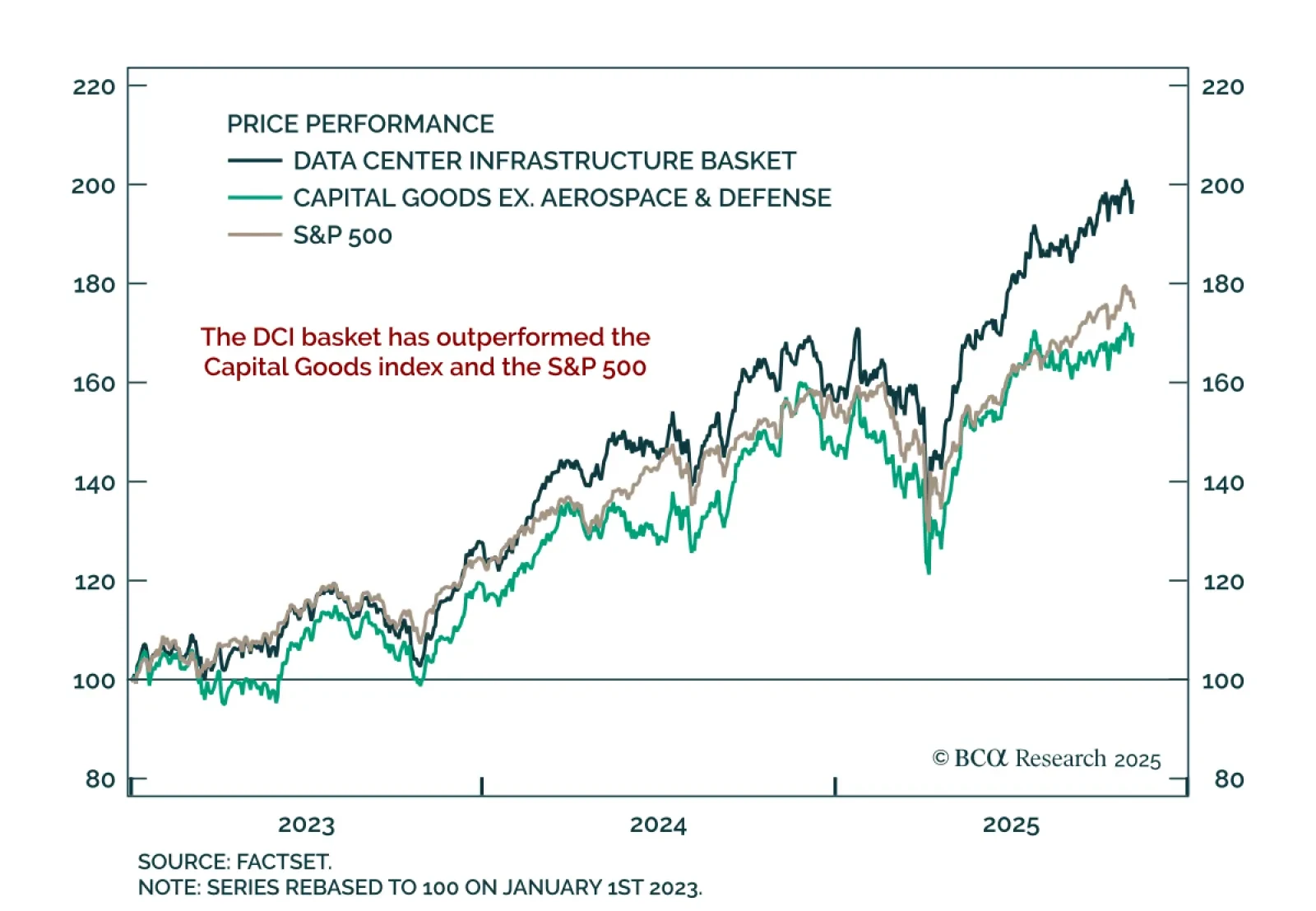

Our US Equity strategists highlight Data Center Infrastructure as a long-term investment theme, with Capital Goods and Materials companies emerging as key GenAI beneficiaries. As hyperscalers accelerate global data center expansion, demand for turbines, grid…

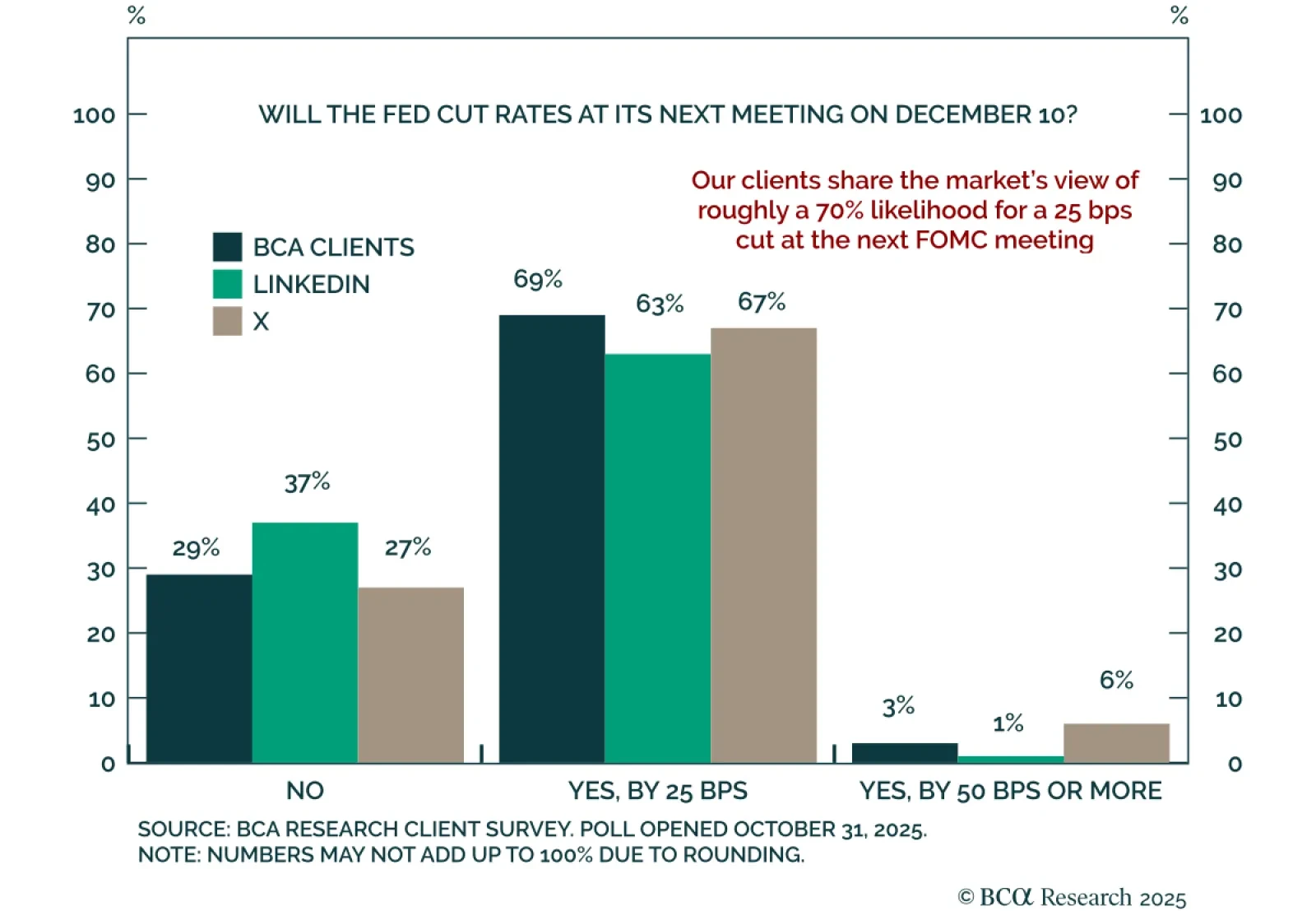

The FOMC meeting in mid-December remains live. The rates market is pricing in a 72% probability that the Fed will cut rates by 25 bps. In the latest weekly poll on the Have Your Say section of BCA's website, 69% of respondents agreed, but another 37% thought…