United States

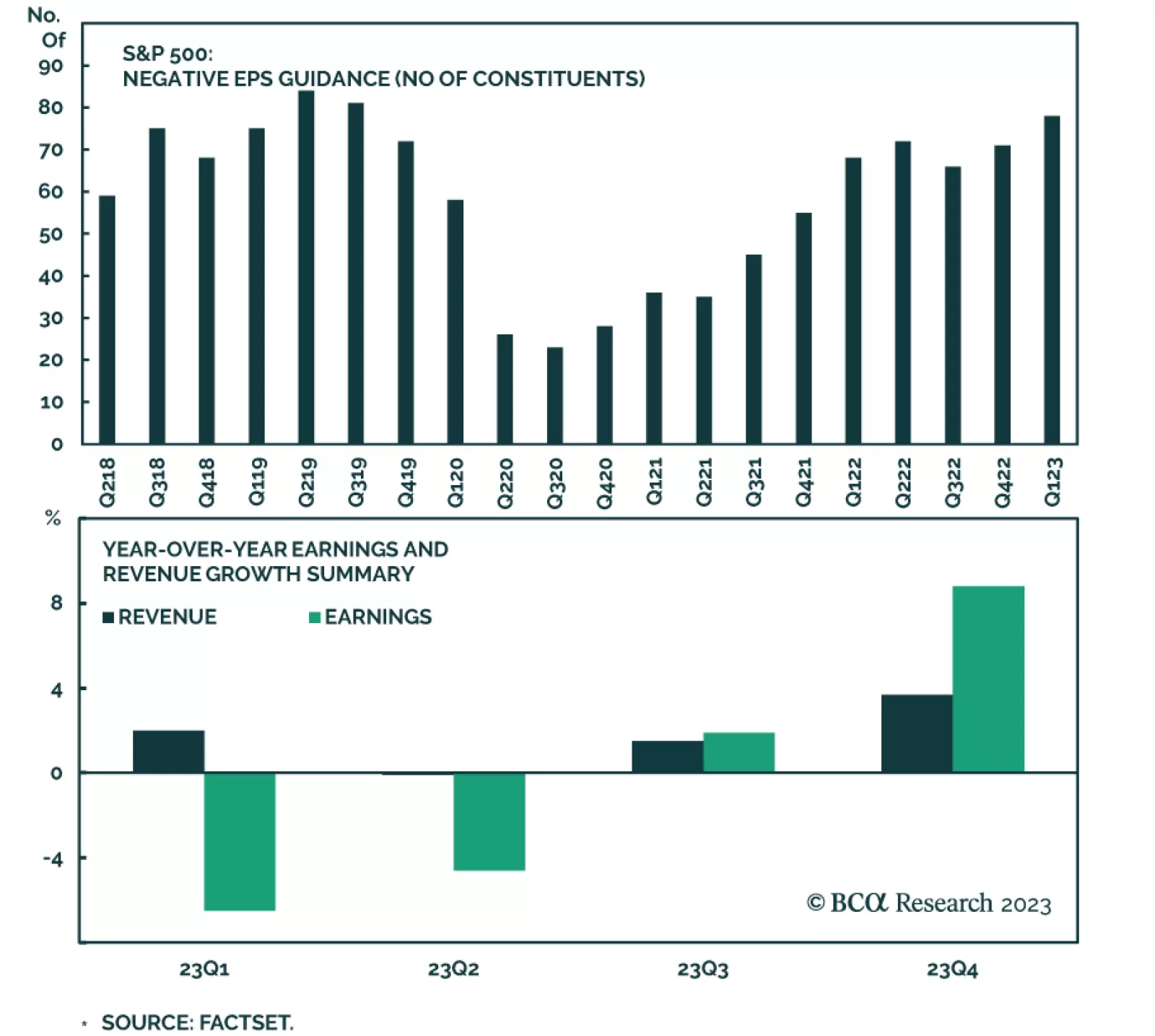

The Q1-2023 US earnings season started last Friday. As companies report, we will gauge the effects of the Fed’s monetary campaign on corporate profitability. With inflation declining, and demand faltering, sales growth is key. According to Factset,…

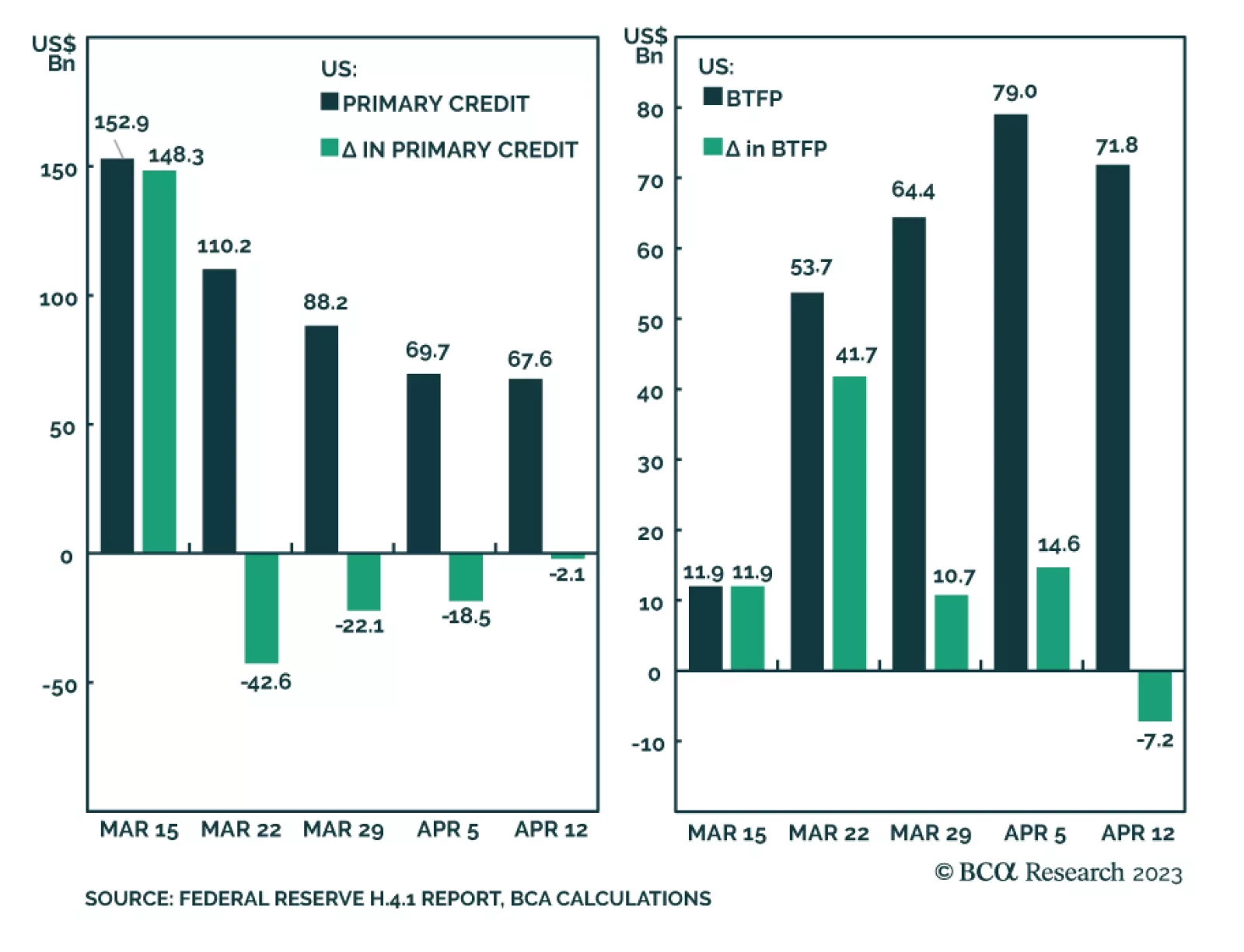

According to BCA Research’s US Investment Strategy service investors and regulators would be foolishly complacent if they didn’t consider the possibility that the banking turmoil could reduce credit availability and slow economic activity, but the most recent…

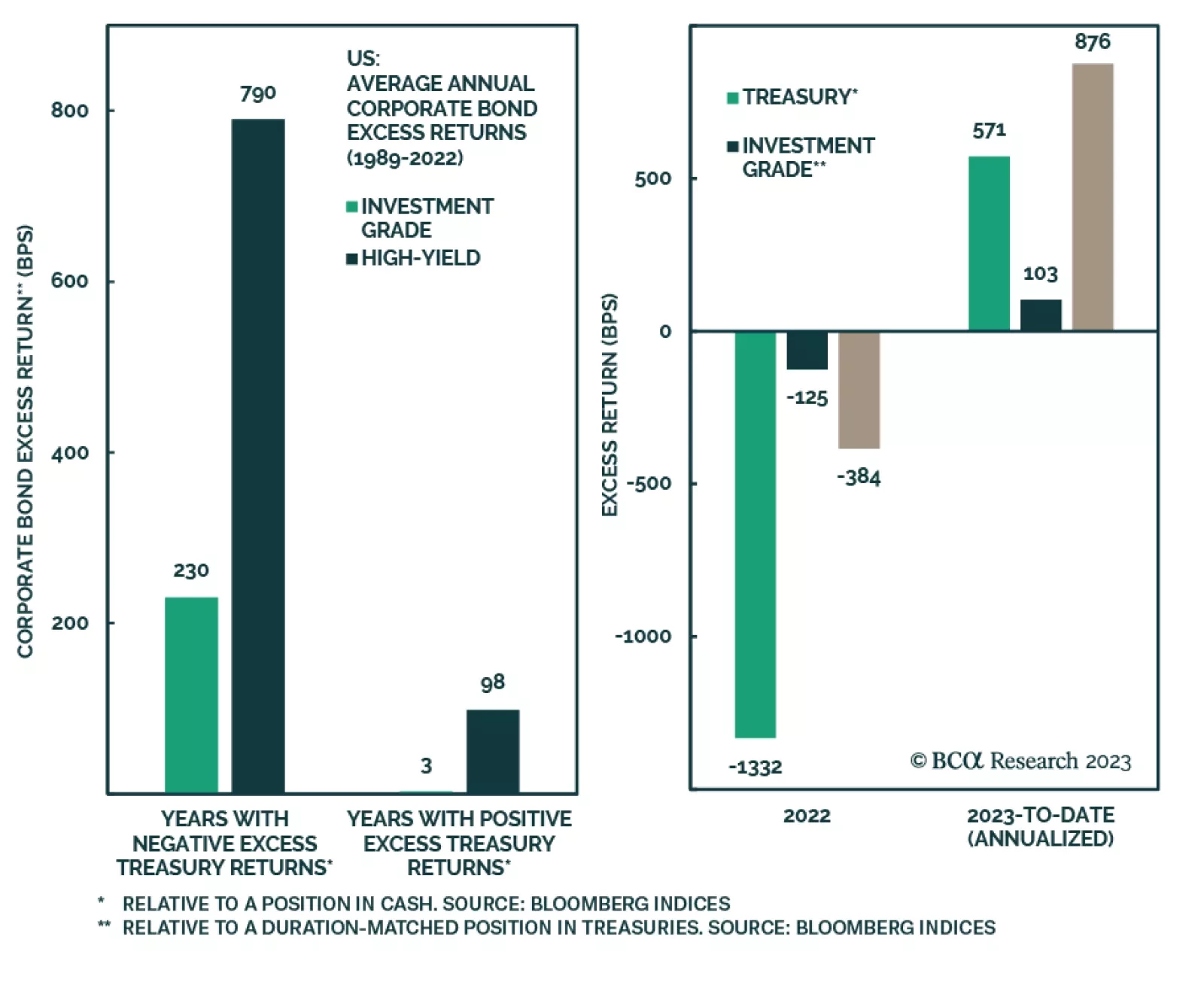

BCA Research’s US Bond Strategy service concludes that in the near-term (3-months), investors should favor bond sectors with low exposure to both rate risk and credit risk such as T-bills and agency bonds. One of the traditional relationships that fixed…

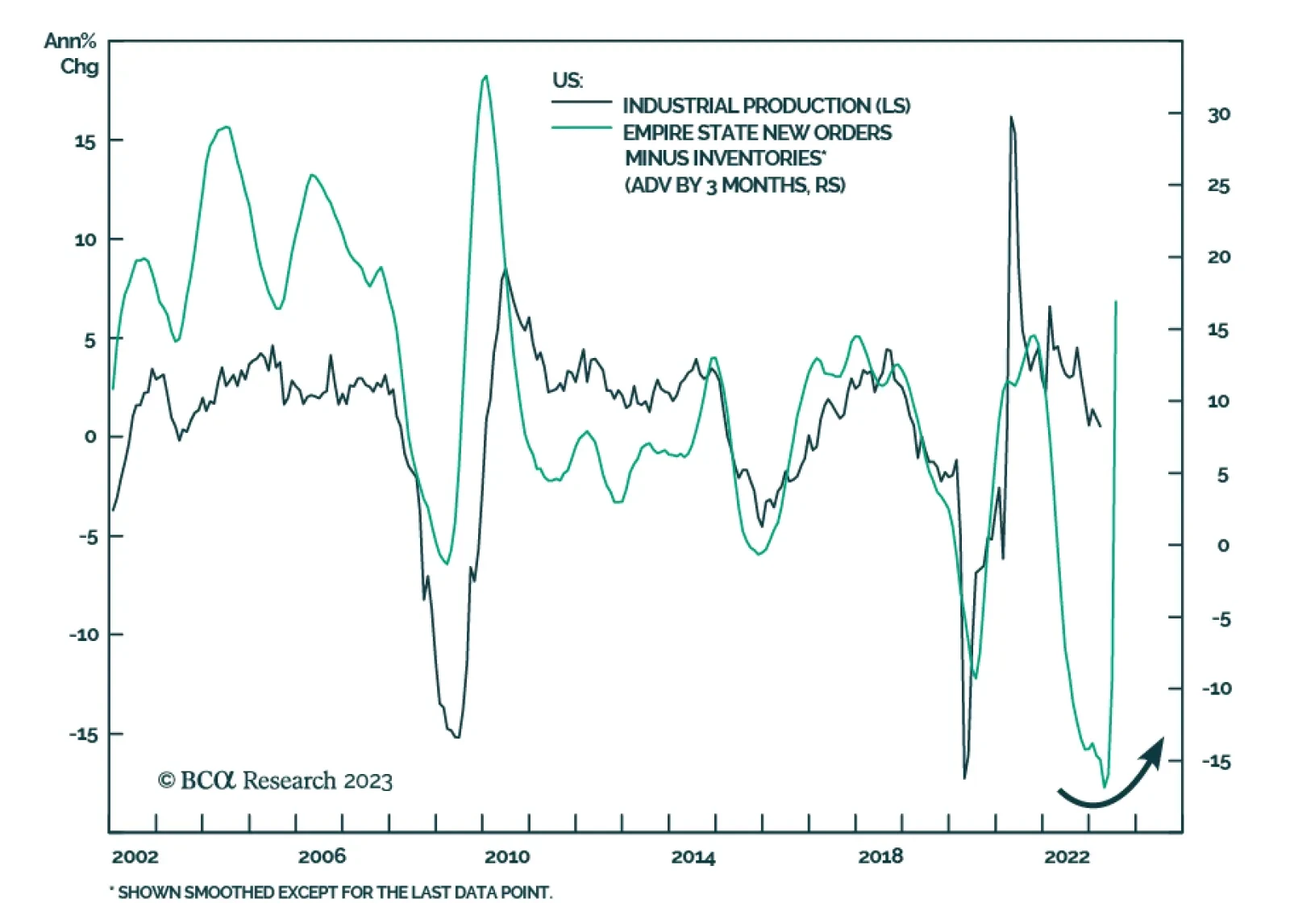

The New York Fed’s Empire State Survey delivered a positive signal about US manufacturing activity in April. The headline general business conditions index jumped 35.4 points to 10.8, unexpectedly crossing into positive territory for the first time since…

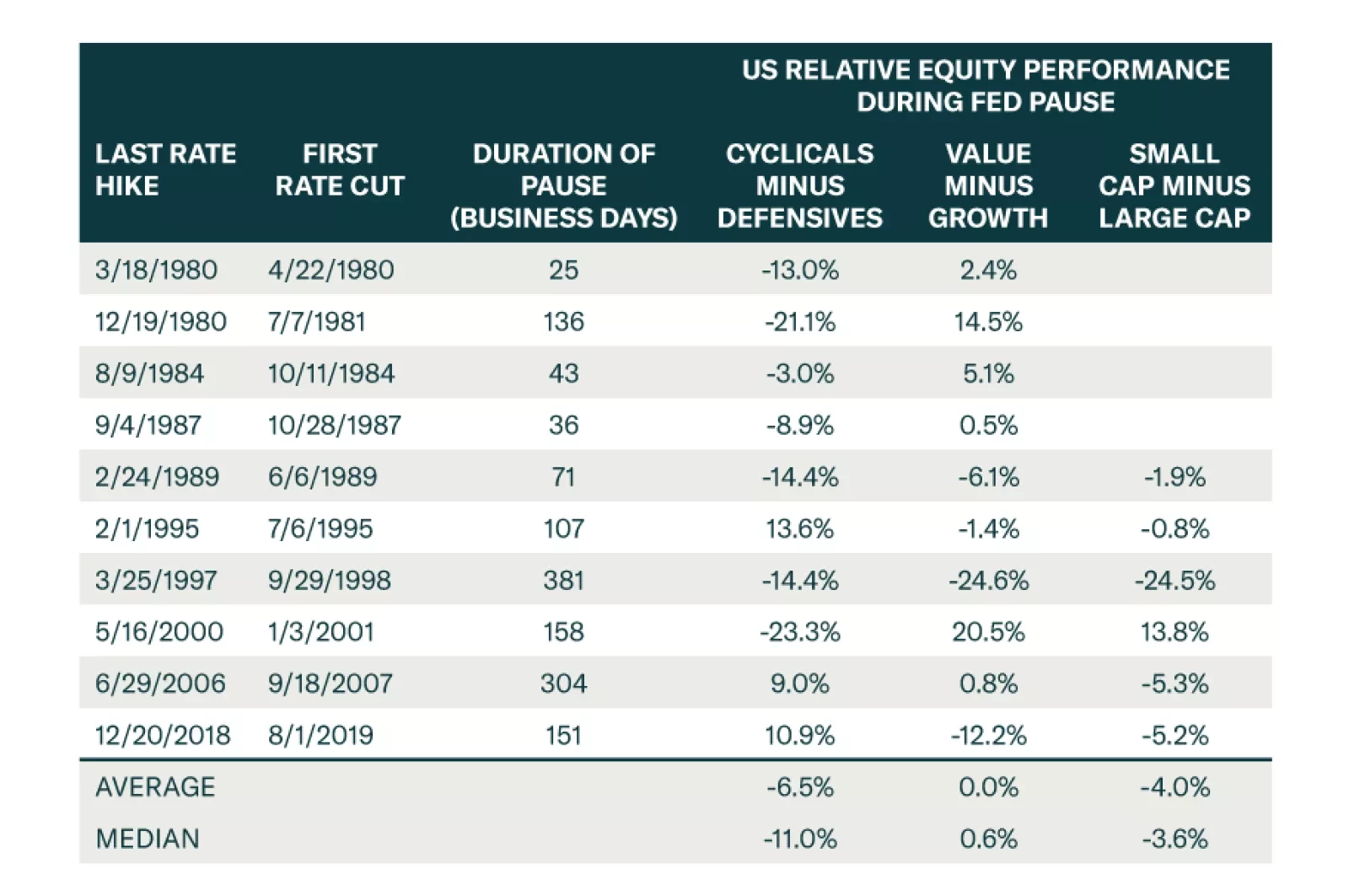

Our US Bond Strategists expect the Fed to deliver one last 25 basis point rate hike at its next FOMC meeting on May 2-3 before an extended pause. Given that rate cuts are currently priced in for 2023, the implication for US bond investors is that they should…

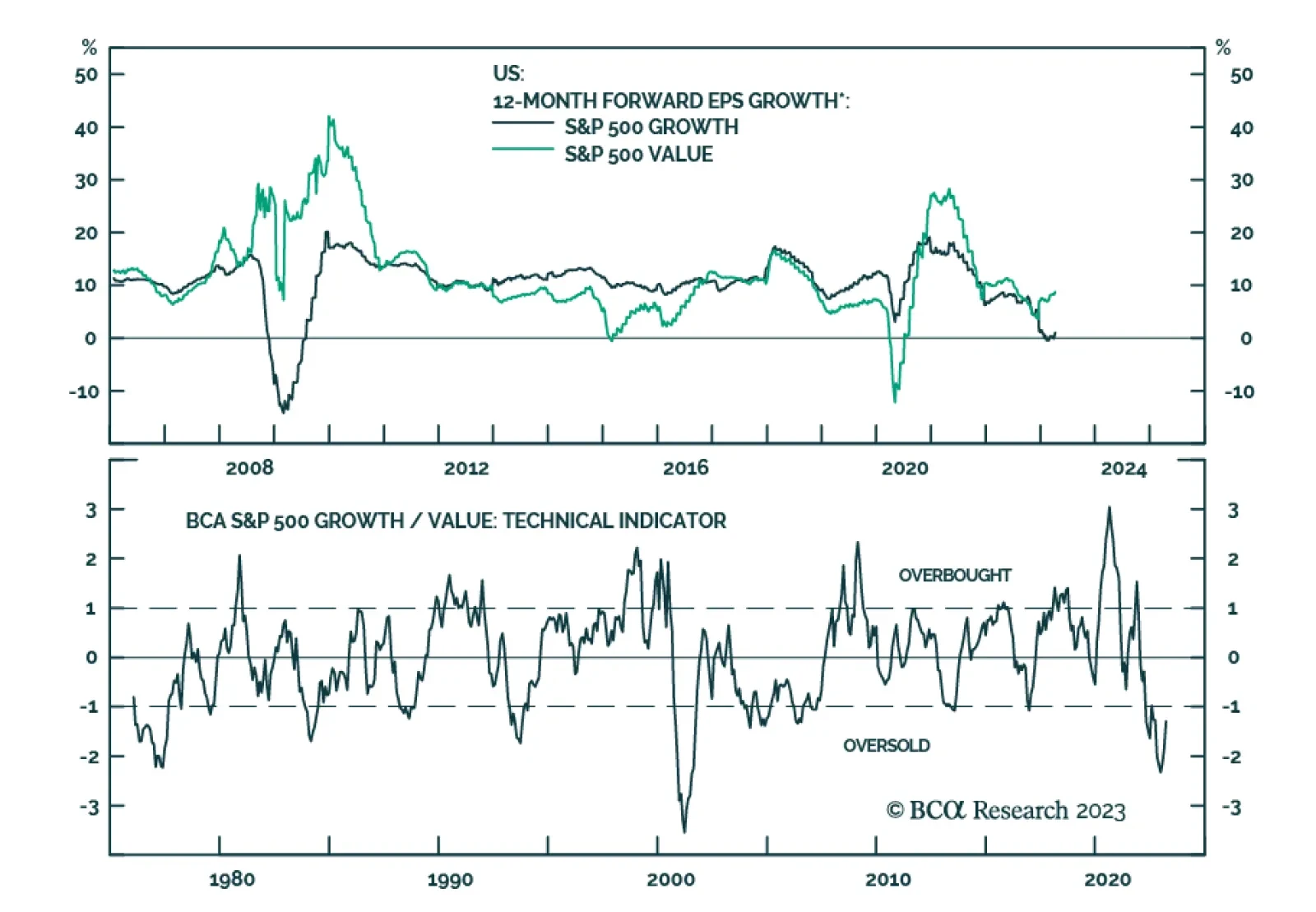

BCA Research’s US Equity Strategy service upgraded Growth to overweight and downgrade Value to underweight on a tactical investment horizon. Many growth stocks have recently disappointed investors as their sales and earnings growth is slowing. Yet,…

This report looks at the relationship between rate risk and credit risk and how it has changed over time. It also makes the case for favoring agency MBS within an underweight allocation to US spread product.

The YTD market rally was driven by outperformance of high-quality growth stocks which offer protection in uncertain times. As growth continues to slow, high-quality growth stocks should continue to do well. Hence, we are moving to overweight Growth vs. Value.

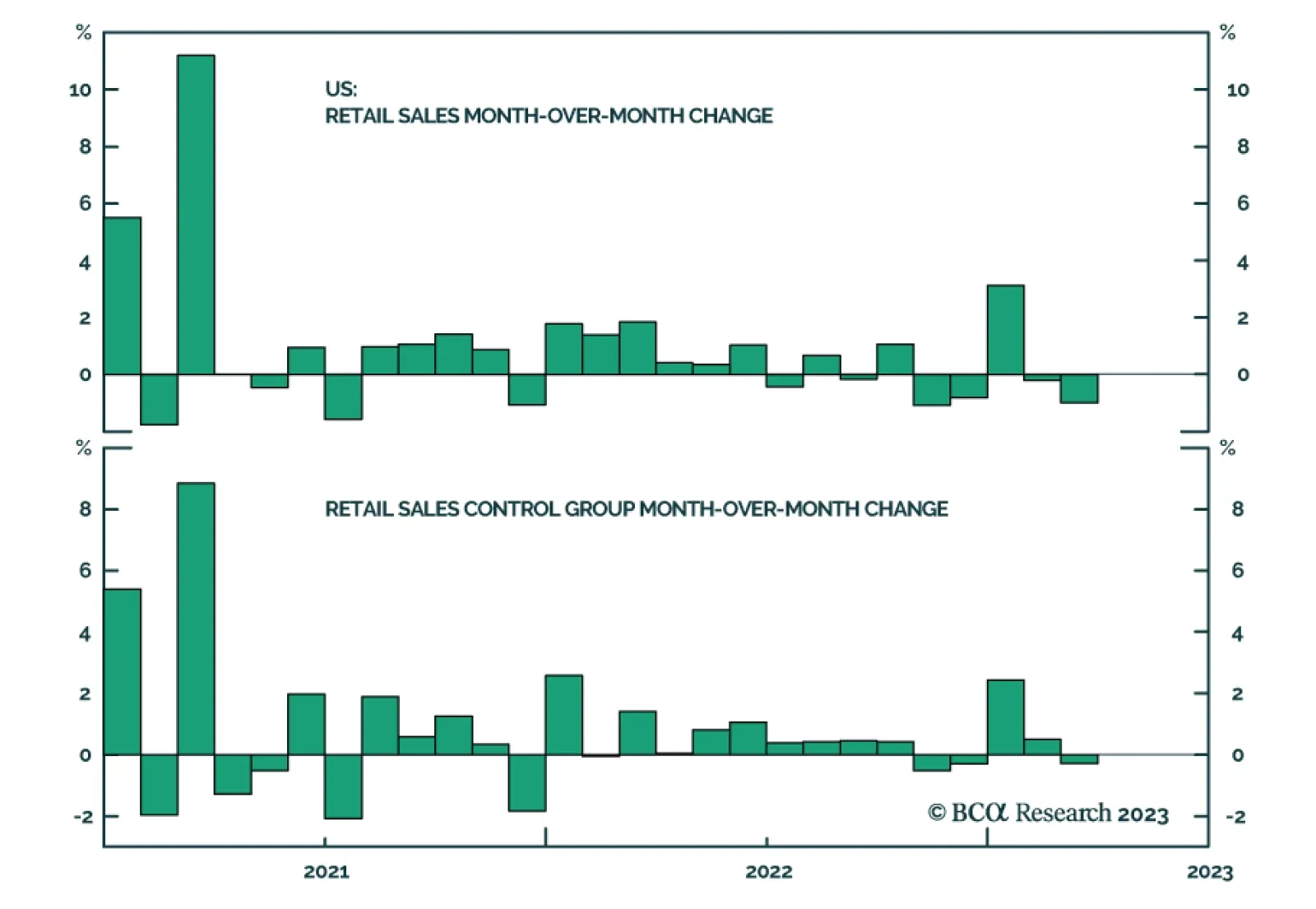

US retail sales delivered a negative signal about consumer demand in March. Overall retail sales fell by the most since November, with the 1% m/m drop coming in below expectations of a 0.5% m/m decline following February’s 0.2% m/m decrease. The monthly…

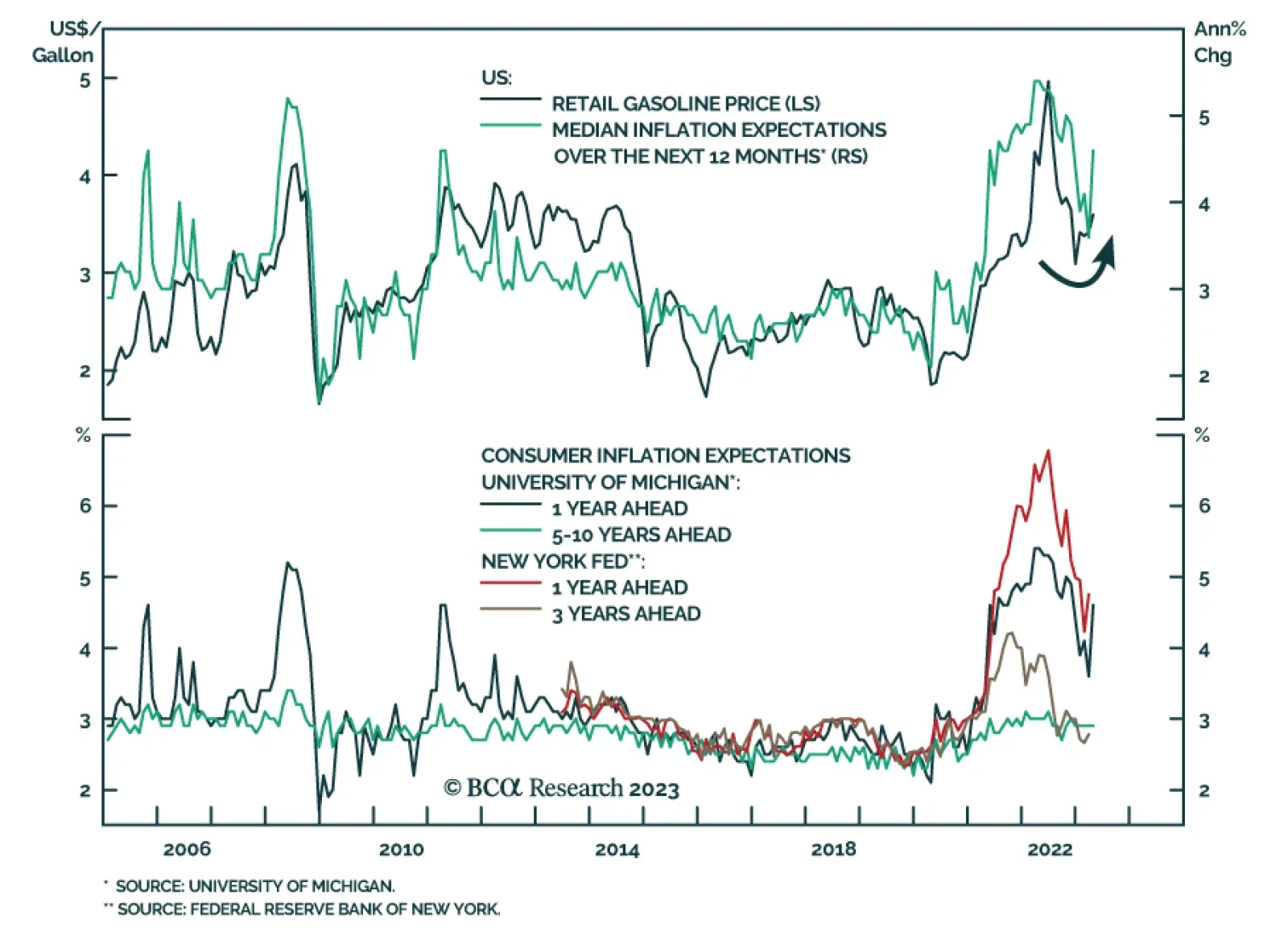

Data released over the past week show a resurgence in short-term US consumer inflation expectations. The University of Michigan Consumer Survey’s measure of year-ahead expectations jumped by 1 percentage point to a 5-month high of 4.6% in April. Similarly,…