United States

Stay defensive in the second quarter. We can see a narrow window for risky assets to outperform but we recommend investors stay wary amid high rates, supply risks, extreme uncertainty, peak polarization, and structurally rising geopolitical risk.

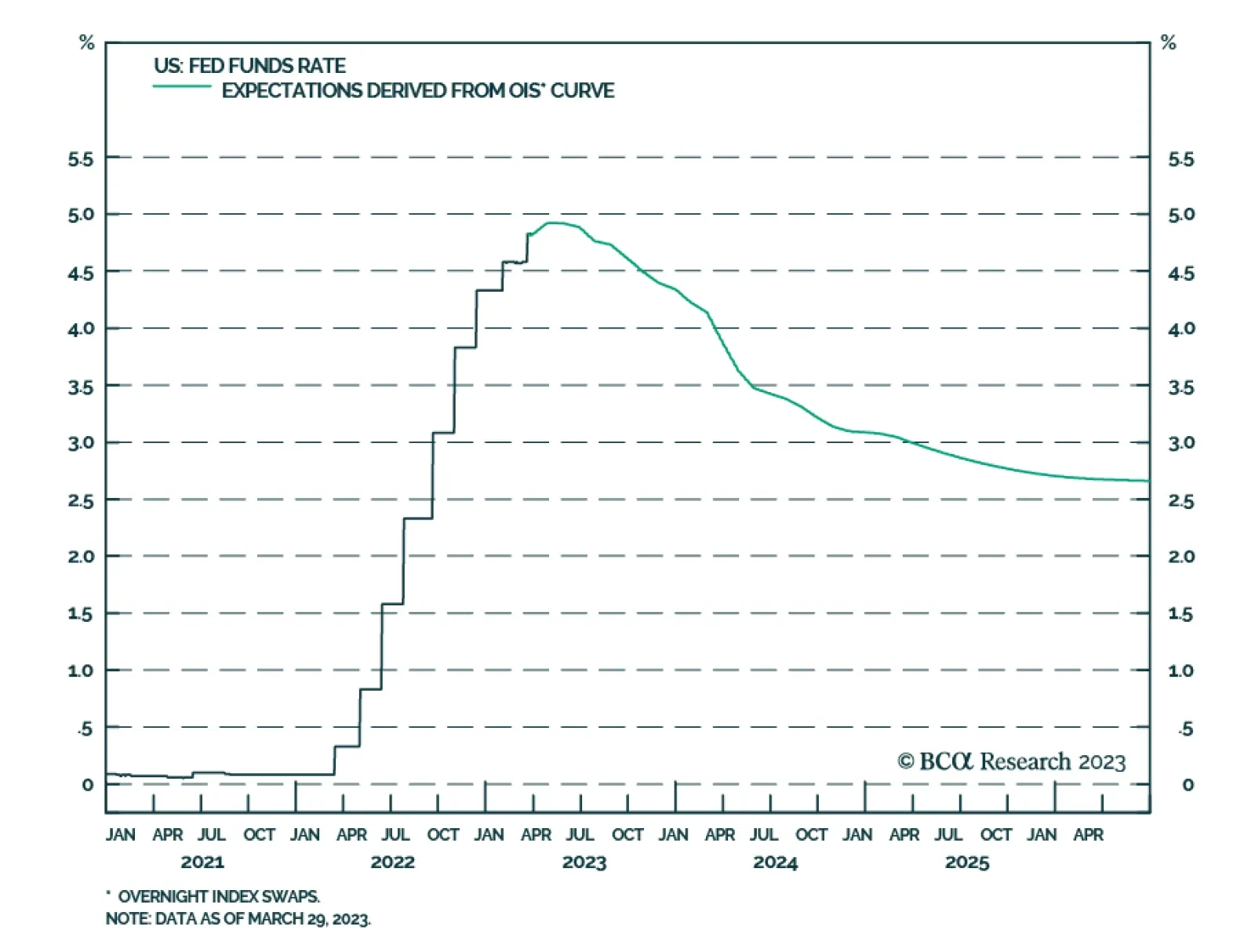

In this Special Report, we present our updated Central Bank Monitors for the US, Canada, Australia, New Zealand and Japan. We have improved the methodology used to calculate the monitors to make them more dynamic to structural changes over time. The main message from the Monitors is consistent across all five countries. The pressure to hike rates is diminishing, suggesting that the end of tightening cycles is approaching, but it is still too soon to expect rate cuts.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.