United States

Some quick takes from today’s FOMC meeting.

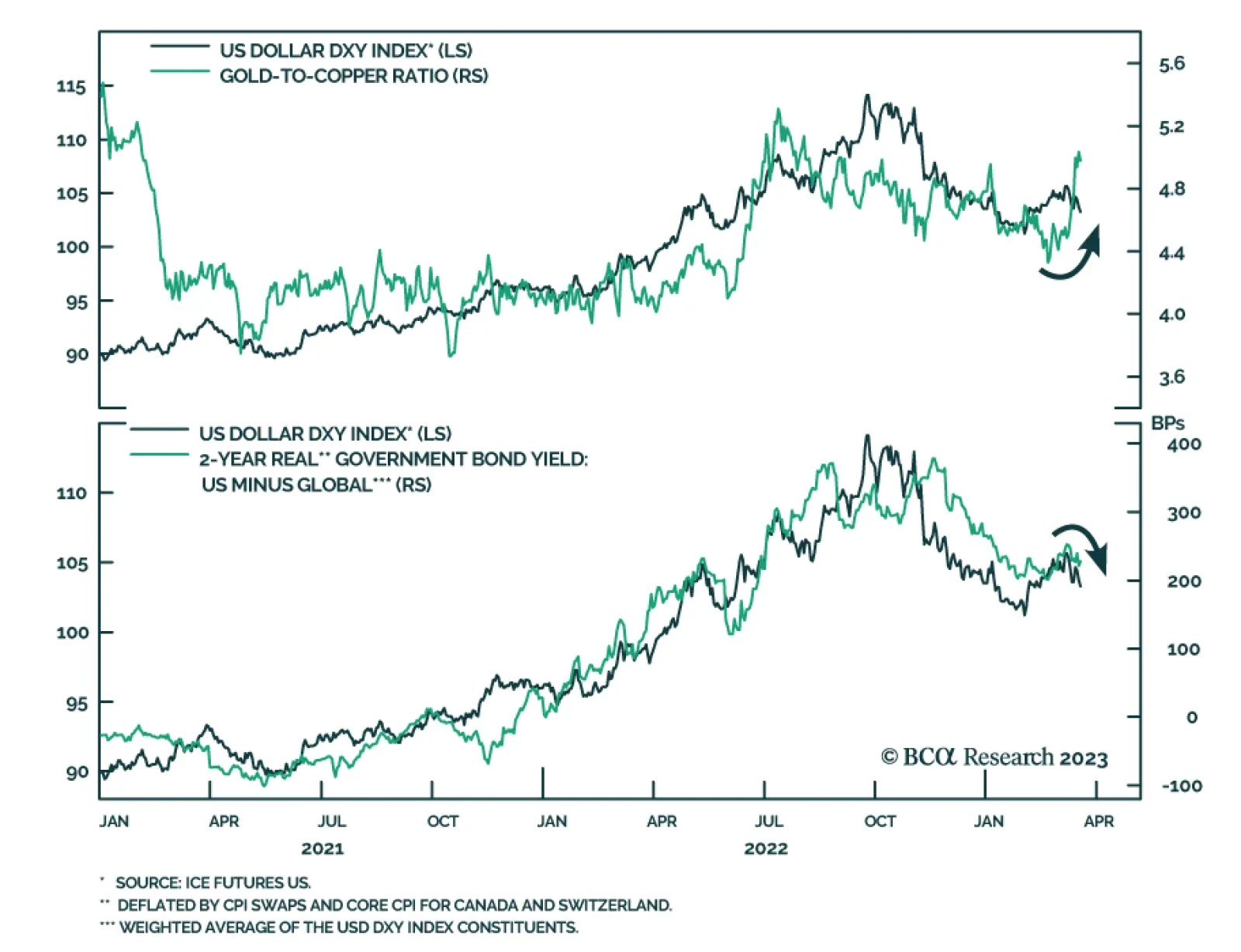

Commodity prices contain important information about the health of the global economy. For example, copper prices typically rise during periods of strong industrial activity, signaling that global growth is firm. Meanwhile, an increase in gold prices could be…

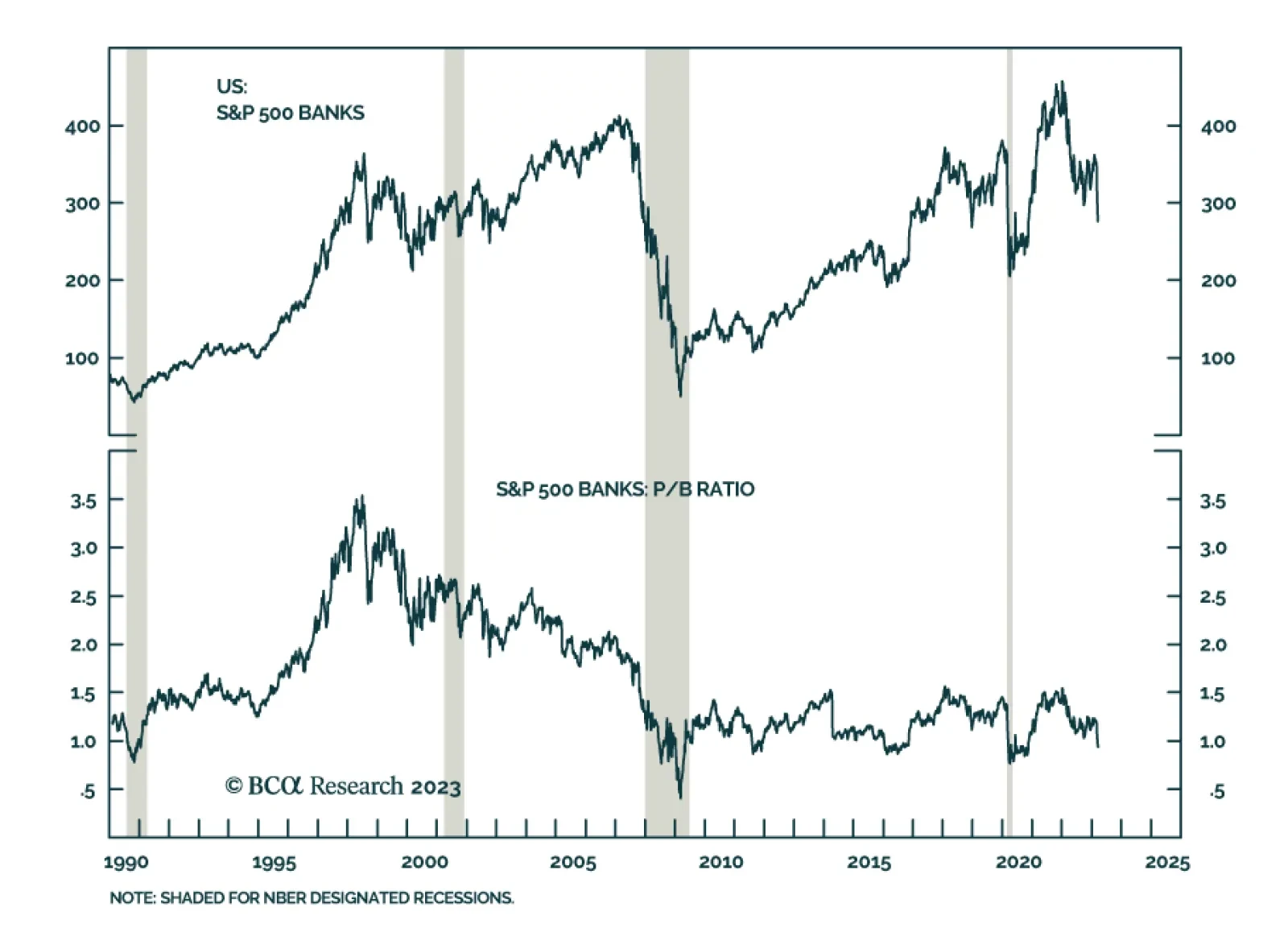

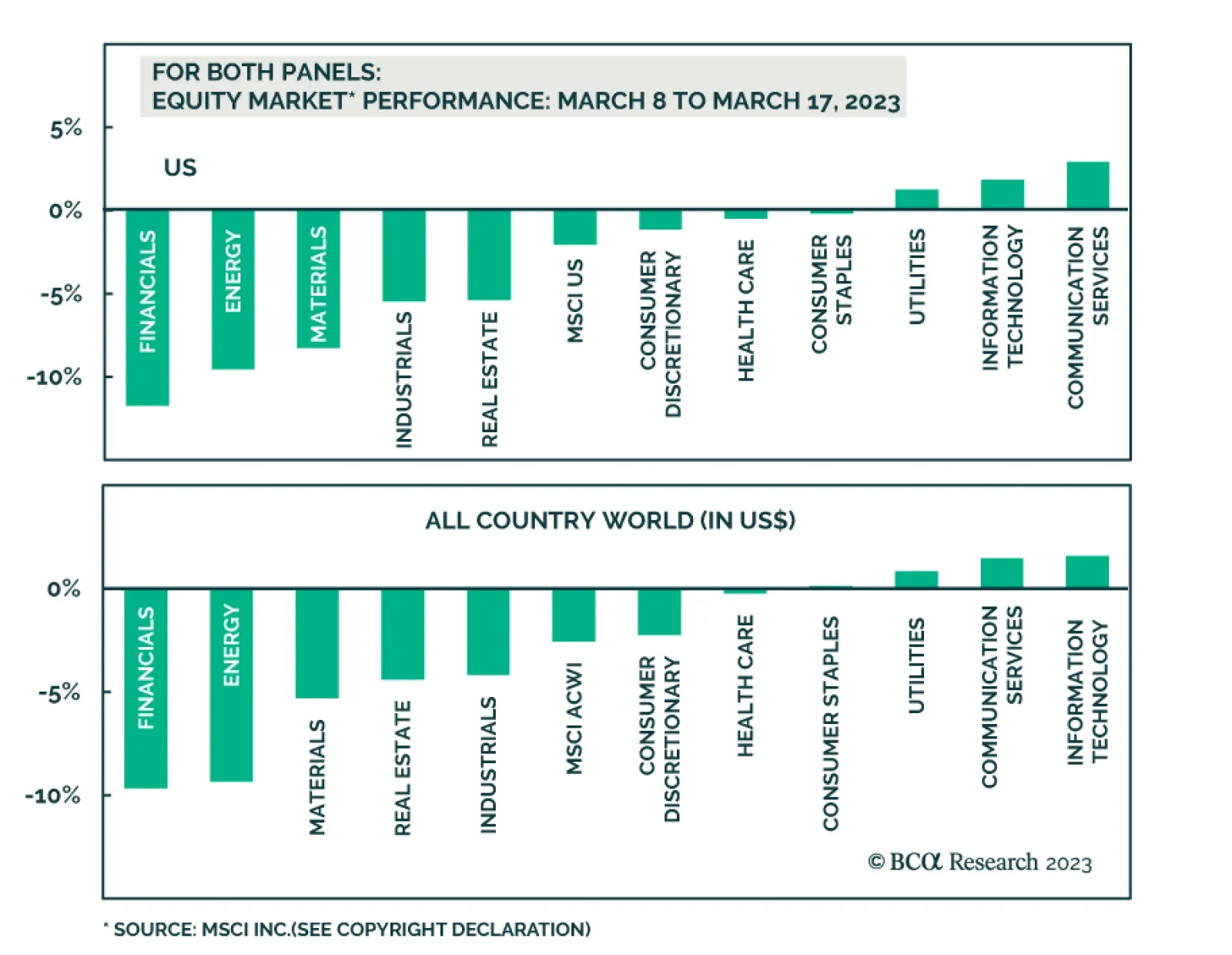

Unsurprisingly, financials are the worst performing equity sector since the fallout of SVB and Signature bank, with the S&P 500 Banks index down 17% since March 8 (see Market Focus). A question facing investors is whether bank stocks are now attractive…

Given that banks are the cause of the recent market turmoil, it is unsurprising that financials are the worst performing sector since the start of the tumult earlier this month. Yet, the equity weakness has been broad-based across most US and global equity…

The Russia-Ukraine war has prompted Europe to ramp up its defense spending. This will greatly benefit its defense industry, especially if defense coordination across the EU increases.

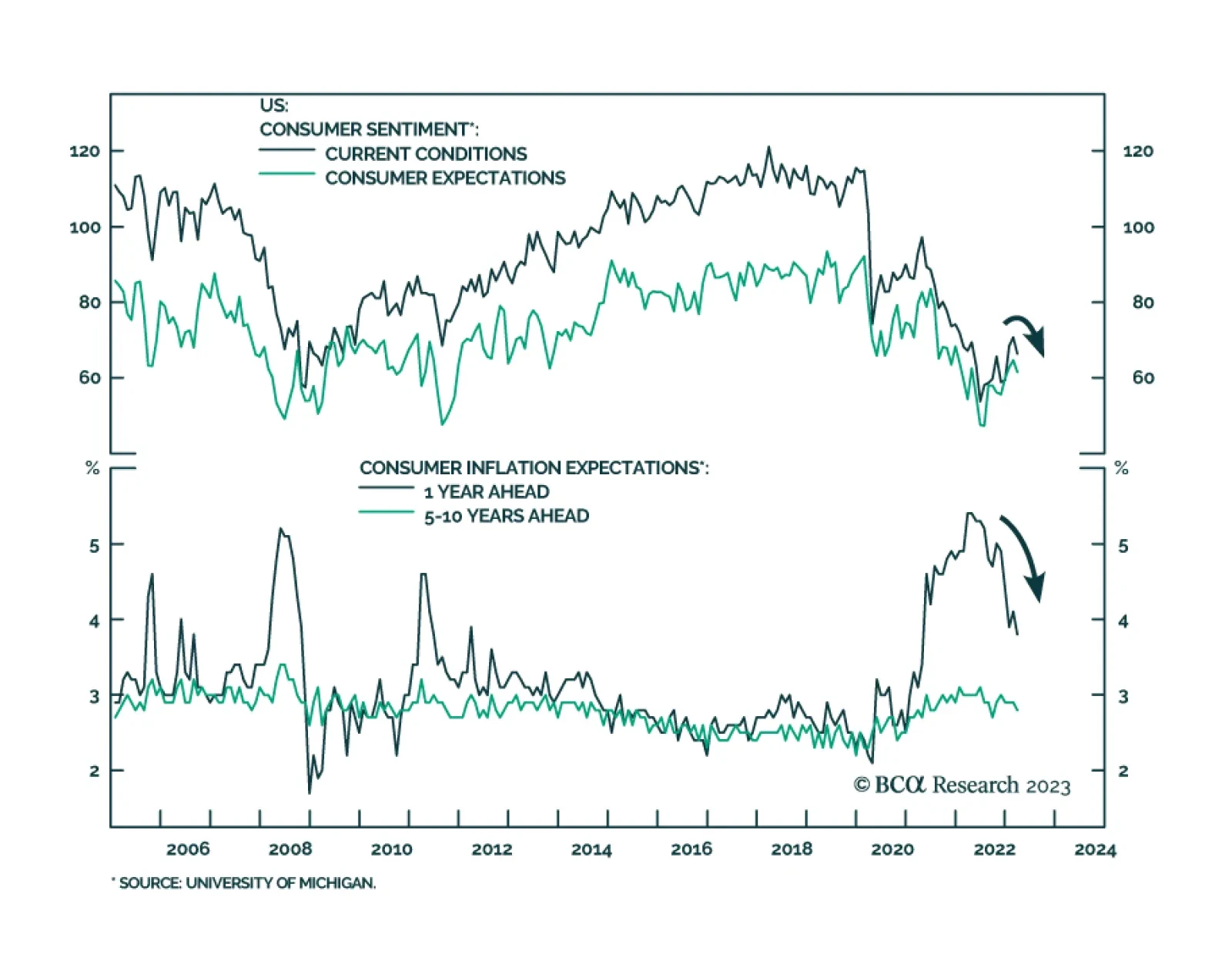

Preliminary results from the University of Michigan’s Consumer Sentiment survey showed an unexpected drop in household morale. The headline index’s 3.6-point decline to 63.4 surprised consensus estimates it would remain unchanged. The decline came on the…

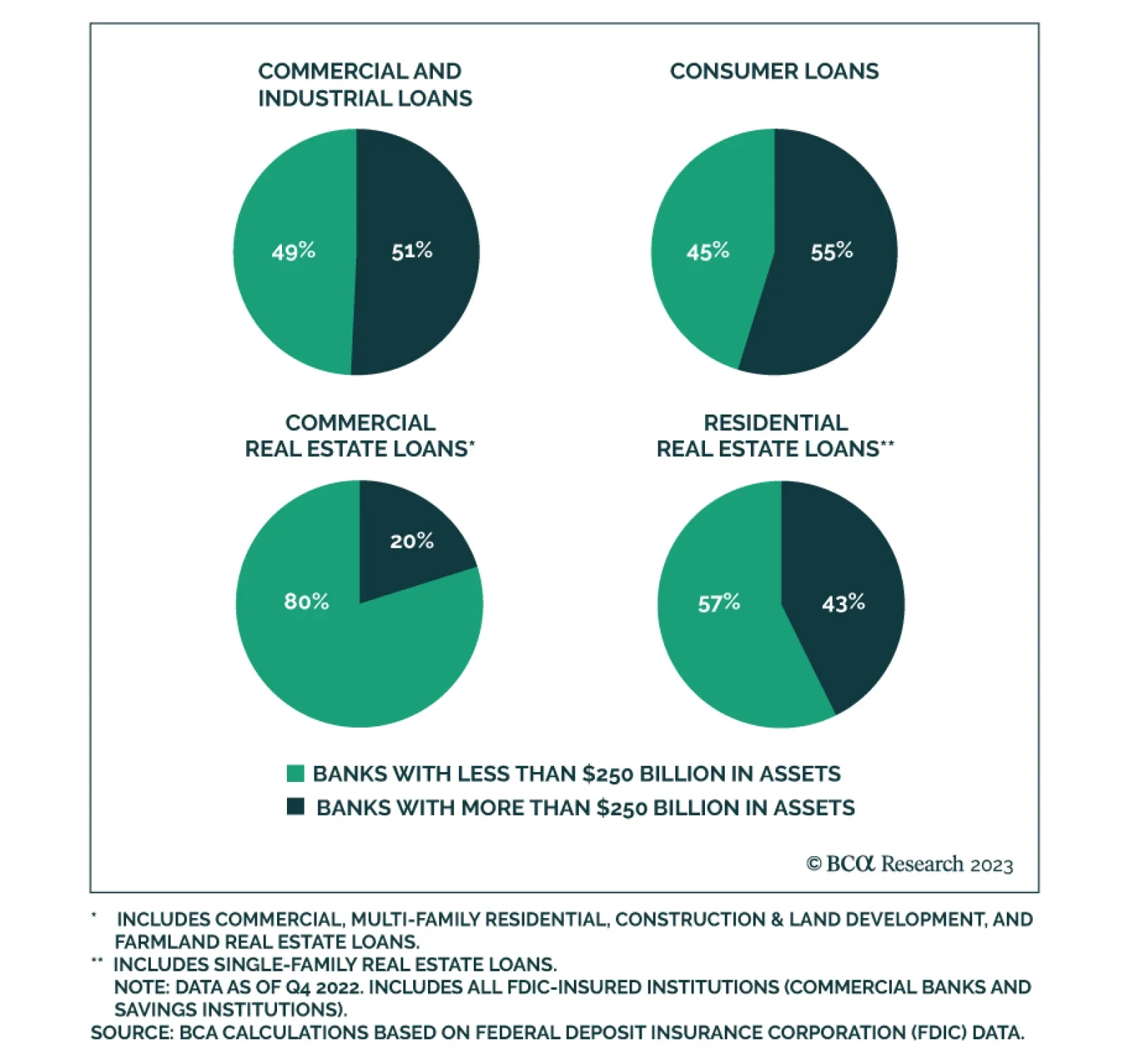

Based on FDIC data, US banks with less than $250 billion in assets account for about half of C&I lending, and over half of mortgage and commercial real estate lending. As such, the turmoil in the banking sector will inevitably weigh on economic activity.…

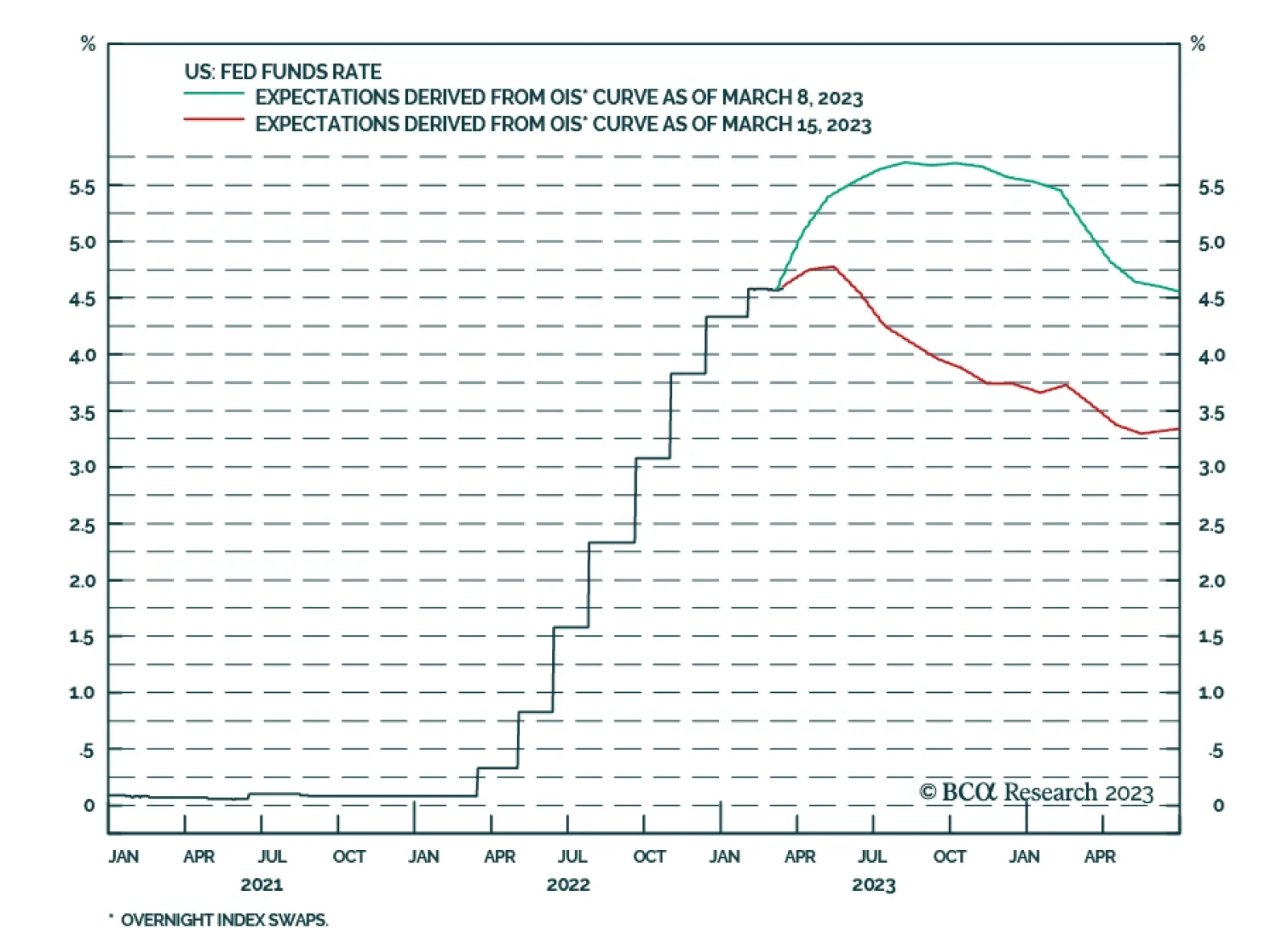

The banking tumult is shining light on the impact of the Fed’s aggressive tightening cycle. In the one year since the FOMC’s first rate hike last March, the fed funds rate has increased by a massive 450 basis points, making the current tightening cycle one of…

The turmoil in US regional banks will weigh on economic growth. Arguably, it would be better for the broader stock market if growth slowed because banks became more conservative in their lending than if it slowed because the Fed had to raise rates to over 6%. In both cases, economic growth would decelerate but at least in the former scenario, the discount rate applied to earnings would not be as high.

BCA Research’s US Bond Strategy service concludes that while the Fed’s hiking cycle is close to its peak, there will not be rate cuts anytime soon The team’s view remains that the Treasury market response to recent banking turmoil is overdone. Depending…