United States

Depending on market volatility during the next few trading days, the Fed will either lift rates by 25 bps next week or pause its tightening cycle. Either way, the Fed’s hiking cycle is close to its peak but rate cuts won’t be coming anytime soon.

China’s victory in getting KSA and Iran to restore diplomatic relations is of far greater consequence to commodity markets than the past weeks’ bank failures in the US. For China, further success in sorting long-standing security issues in the Middle East could incentivize oil and gas capex and affect oil flows. With short- to medium-term fundamentals largely unchanged, we are keeping our 2023 and 2024 Brent forecasts similar to last month, at $95/bbl and $110/bbl, respectively.

The odds of achieving a goldilocks scenario in the US where inflation drops amidst robust growth are low. If US bank woes do not escalate, the Fed will continue hiking amid a contraction in US corporate profits and global trade. The recovery in China’s industrial economy will disappoint. Commodity prices are breaking down.

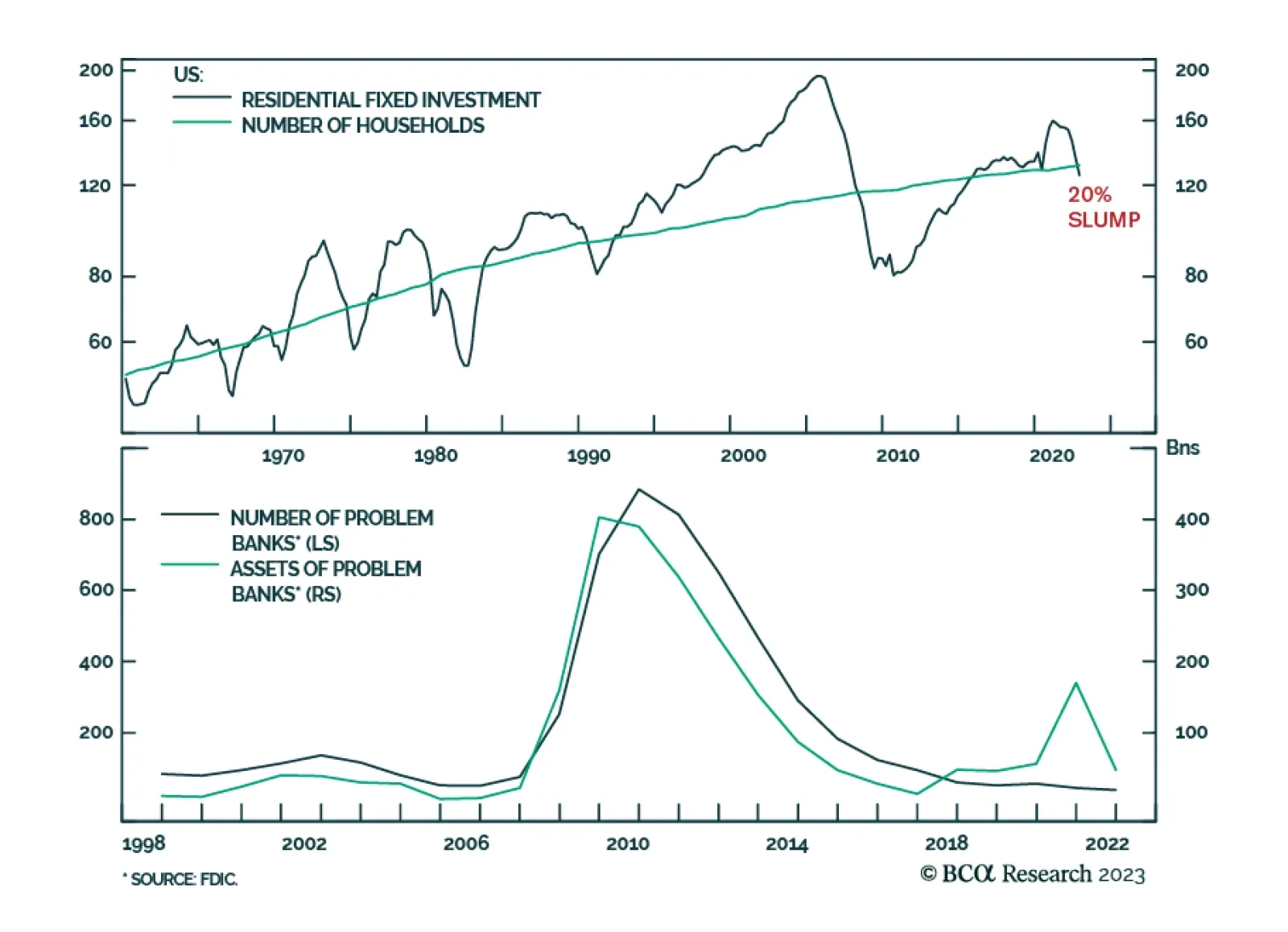

Bank failures are another ‘canary in the coal mine’ warning that a US recession is imminent, yet stocks, bonds, and the oil price are still a long way from fully pricing it.