United States

A run of hot January data shook up financial markets, but we think they overreacted. We remain constructive on equities and the economy in the near term.

Rather than teetering into recession, global growth has firmed since the start of the year. While we still expect inflation to decline, the risk that central banks will need to lift rates more than discounted has increased. Long-term focused investors should start raising cash allocations by trimming their equity holdings.

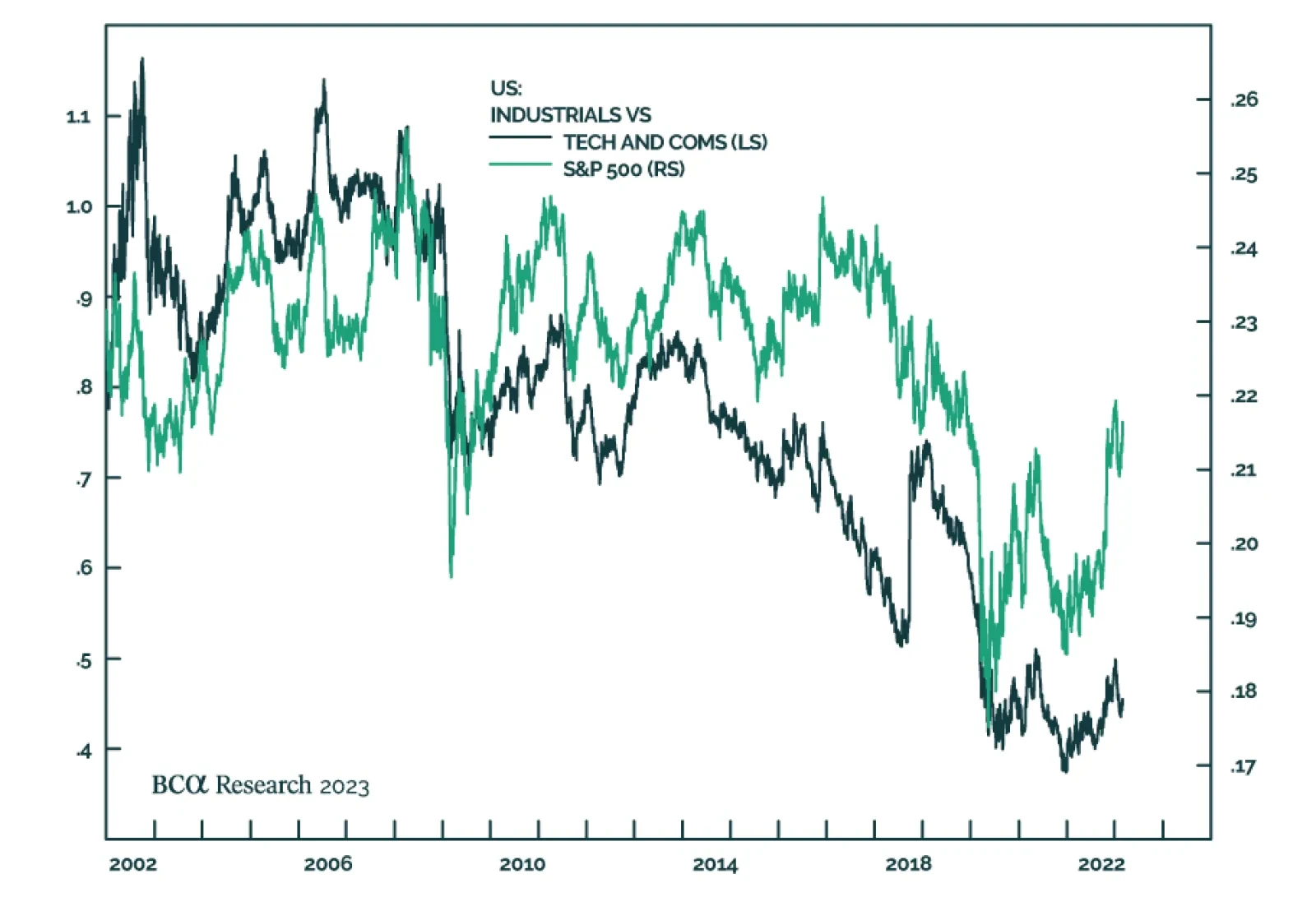

US domestic politics, hypo-globalization, and Great Power Competition favor a revival of US manufacturing capacity. The industrial sector will benefit from the attempt to rebuild US manufacturing. Go long physical infrastructure and defense stocks. Find opportunities to take a long position on the universe versus the metaverse.