United States

China’s housing market adjustment will be protracted, causing several years of sub-par growth in the world’s second largest economy. We go through the major investment implications.

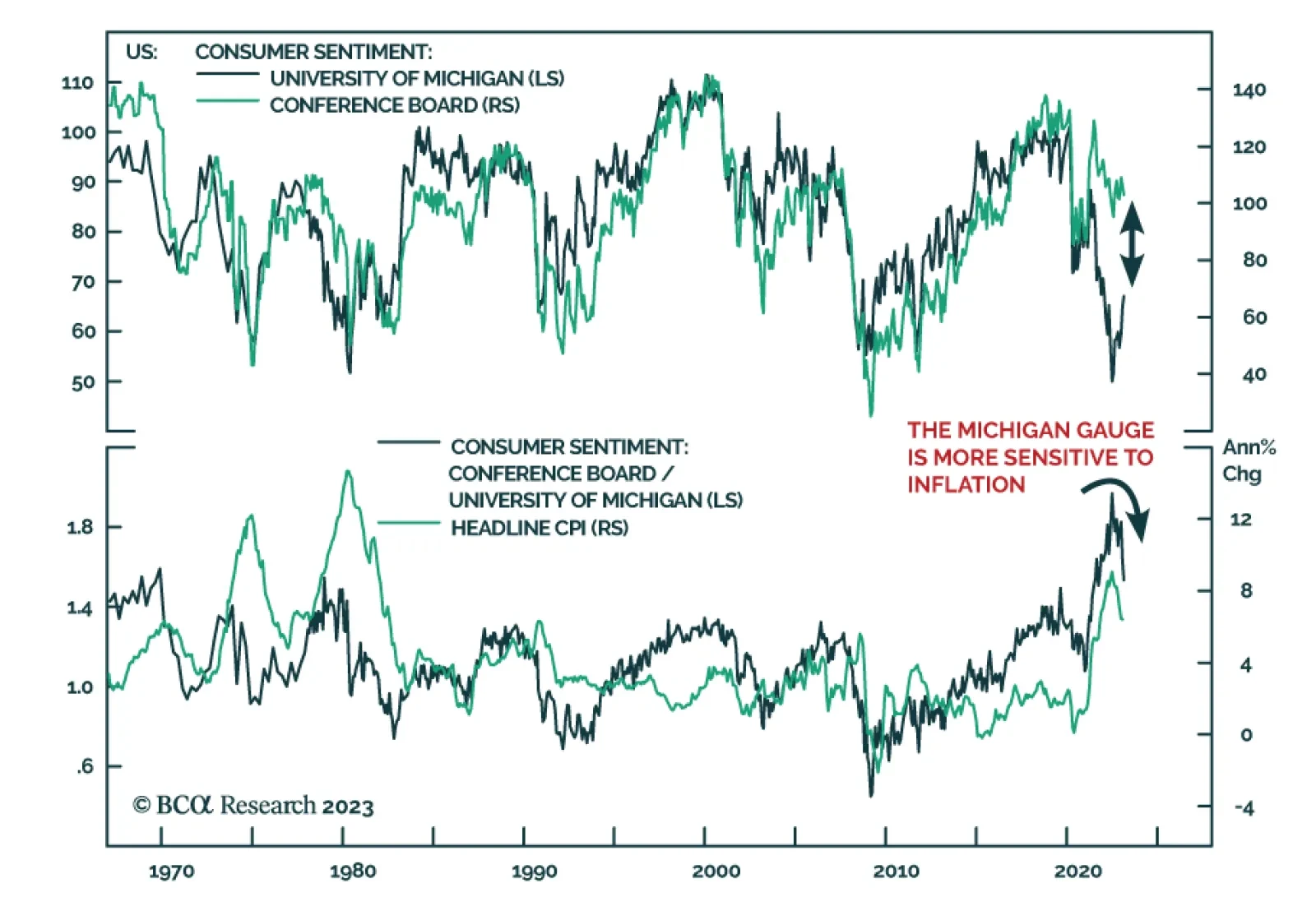

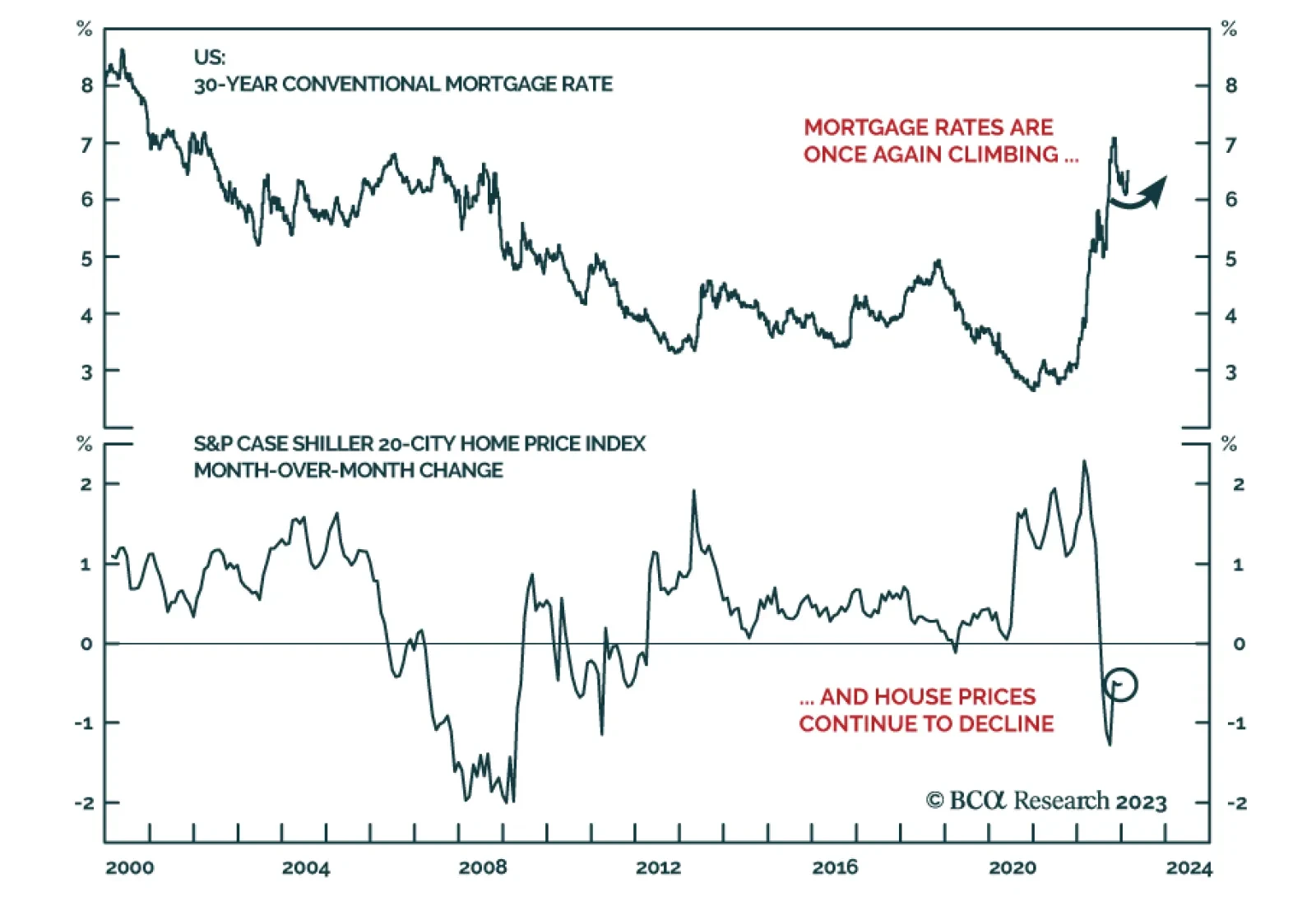

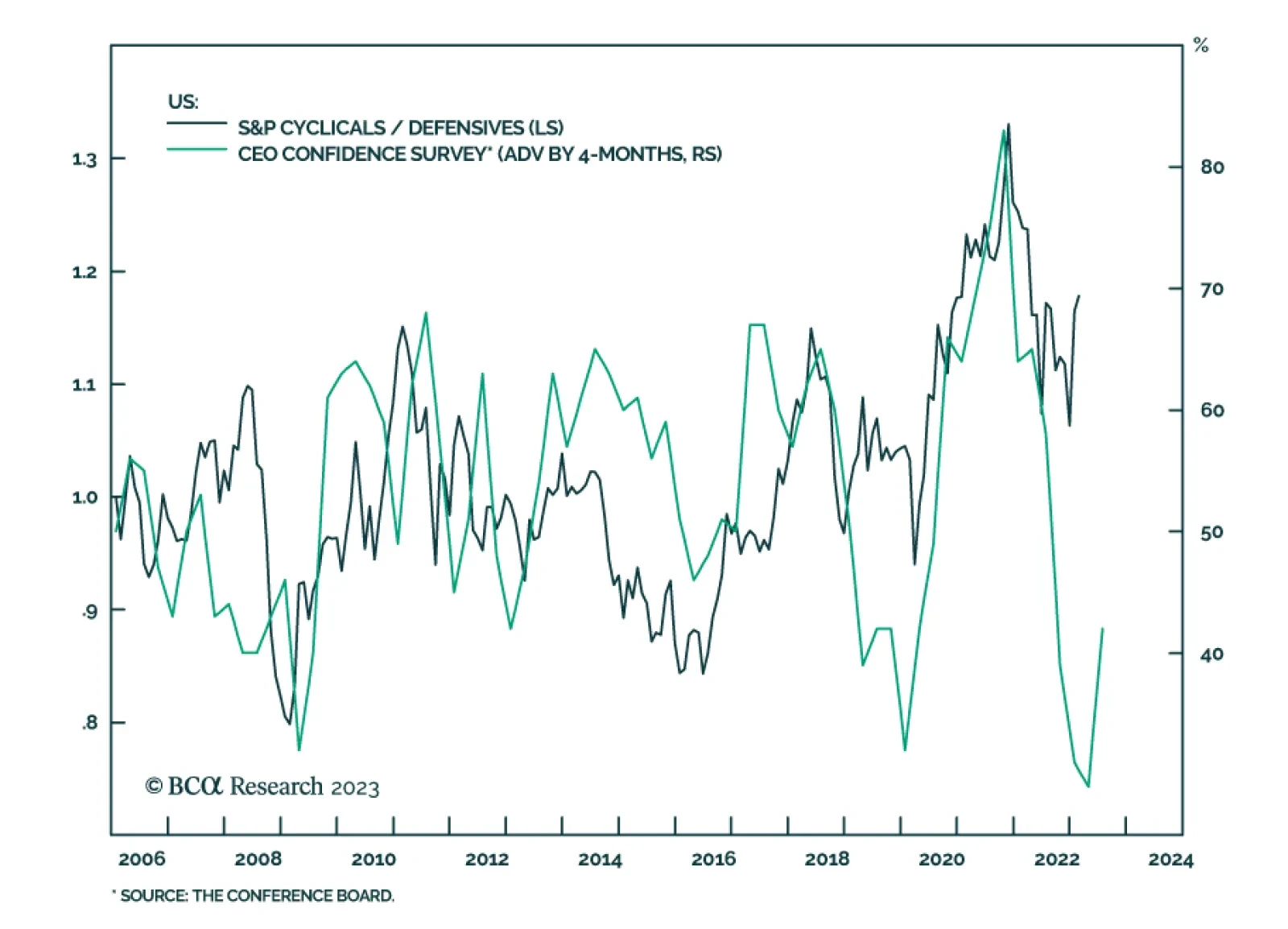

The rebound in growth is pushing up inflation. More aggressive monetary policy is likely to trigger recession over the next 12 months or so. Investors should stay defensive.

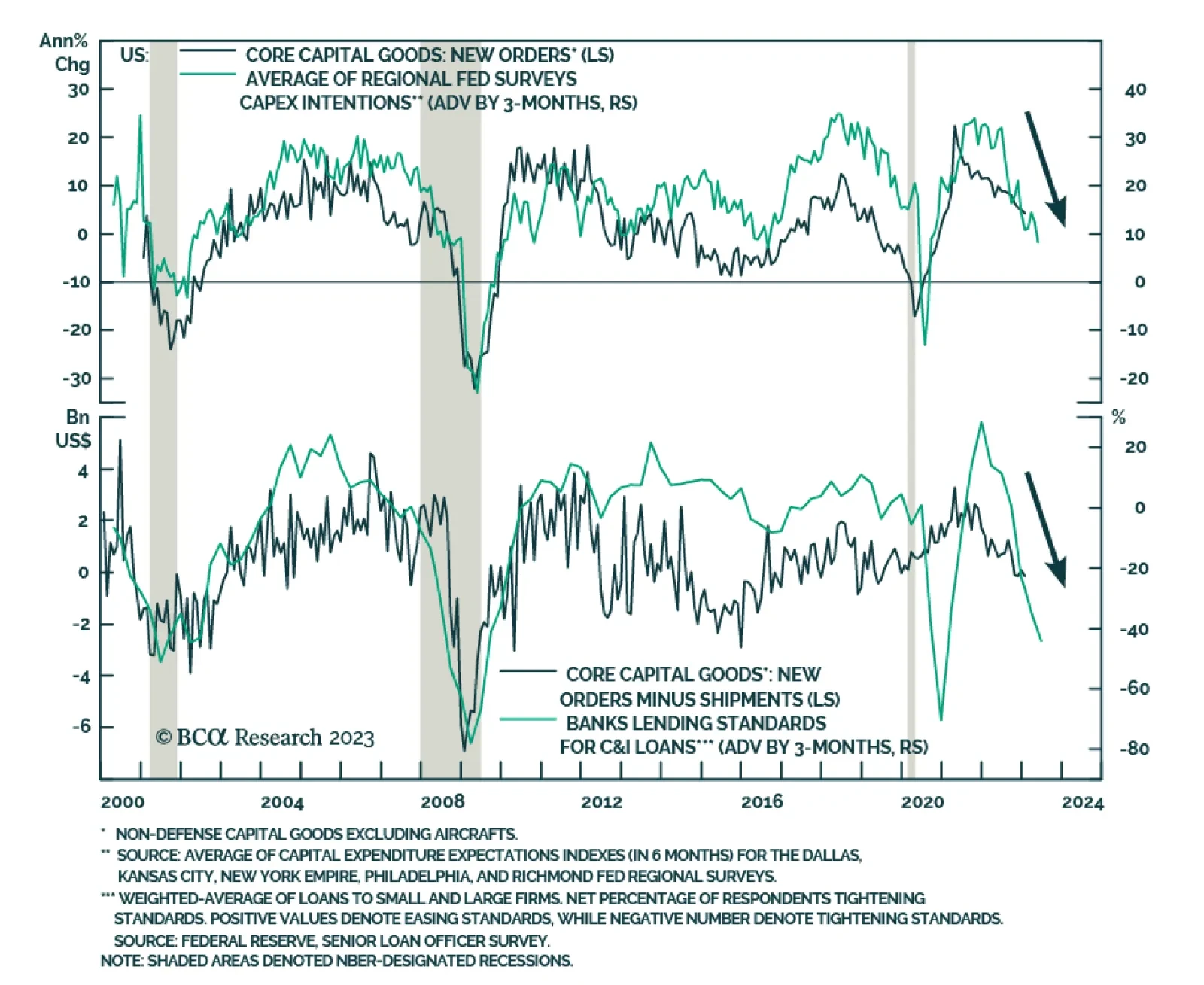

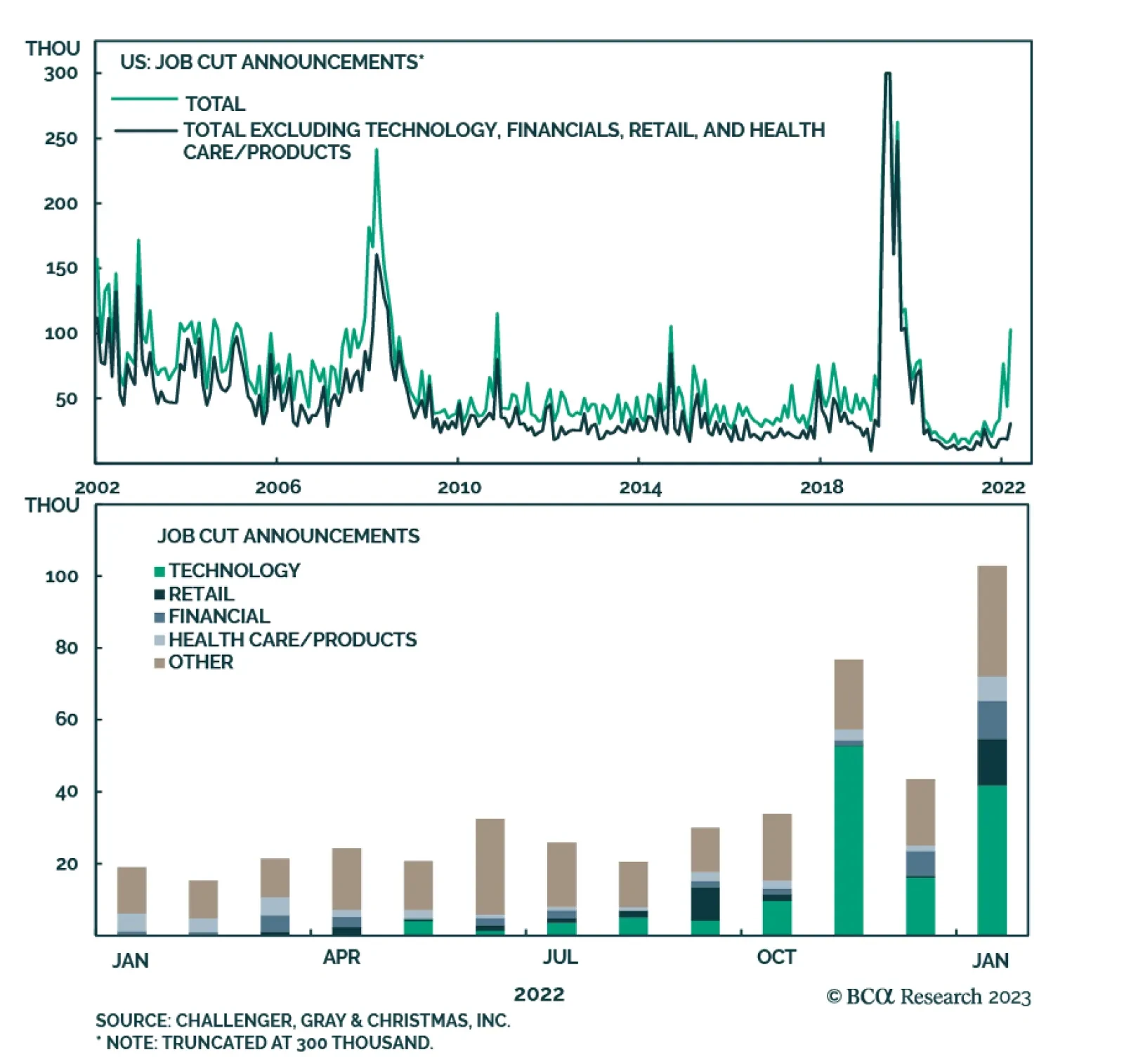

Bulls and bears are perplexed because they suffer from recency bias. The investment roadmap and framework of the past 15 to 20 years should not be used to analyze current US financial markets. US corporate earnings will likely plunge substantially even in the case of a mild recession.

This report considers the outlook for the US corporate credit cycle based on a suite of economic, monetary and corporate health indicators. We conclude that both the default rate and US corporate bond spreads will grind higher during the next 6-12 months.