United States

The backdrop for corporate bonds is turning more risky after the spread tightening seen over the past few months in the US and Europe. A tour of our favorite corporate spread valuation metrics on both sides of the Atlantic suggests a worsening cyclical risk/reward tradeoff for both investment grade and high-yield bonds, especially in the US.

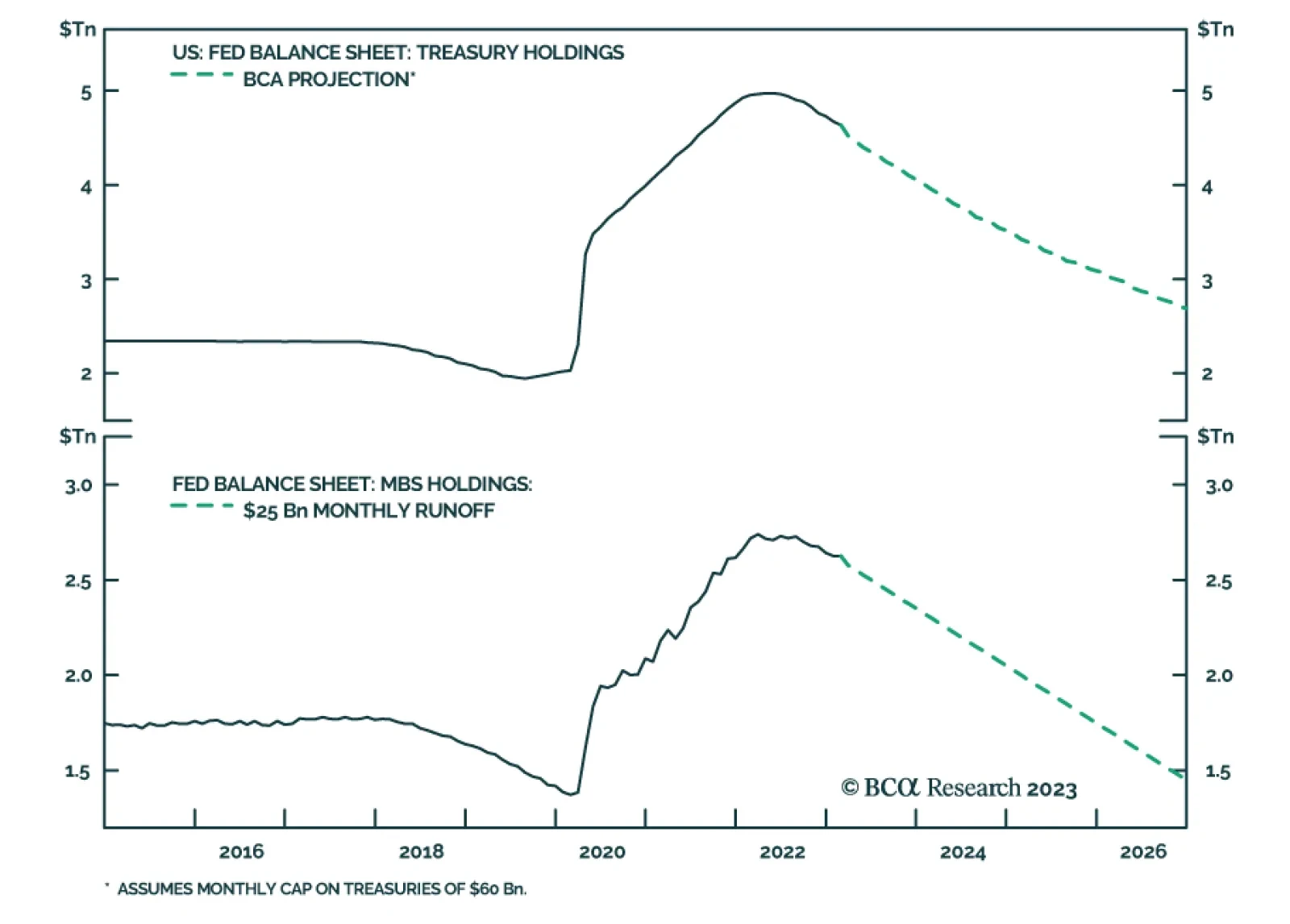

We discuss the outlook for the Fed’s balance sheet and why QT is likely to continue for at least another year.

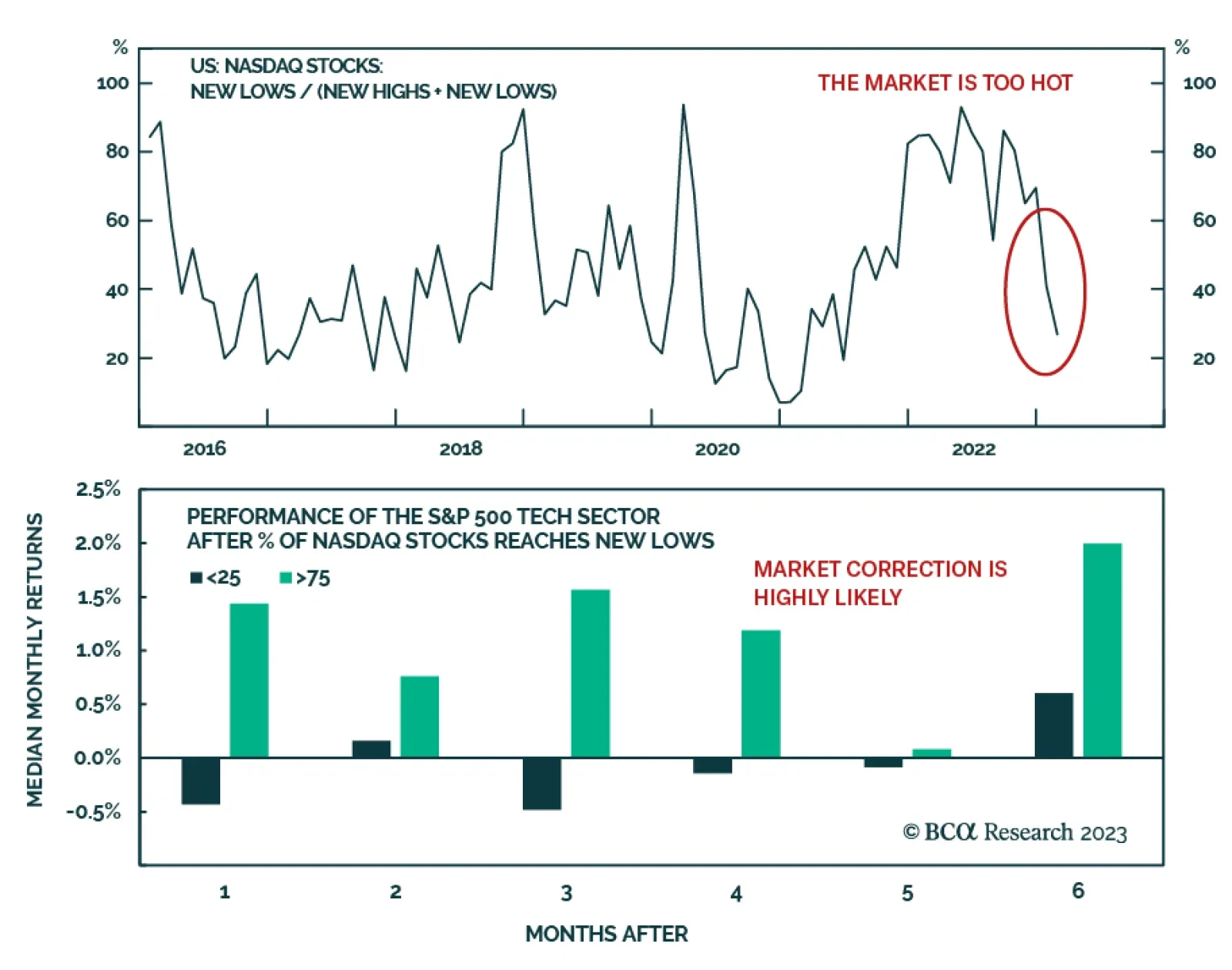

Macroeconomic and business conditions are gradually becoming more favorable for Tech as the bottoming of demand is in sight. Yet, we don’t believe that now is an attractive entry point - the good news is fully priced in, and technicals signal a pullback. However, the sector is worth monitoring as we are getting closer to a sustainable rebound. Our positioning remains unchanged.