United States

Ironically, increased confidence that the economy can withstand higher bond yields may be necessary to lift yields to a level that is actually detrimental to growth. Thus, until more investors are convinced that a recession will be averted, a recession will be averted. Remain tactically bullish on stocks for now. A more defensive posture will likely be necessary later this year.

The tempo of China’s and the US’s military operations is picking up sharply. The risk of a sudden, perhaps unintended, escalation of military conflict, therefore, is rising in the South China Sea. So is the risk of another shooting war in the Middle East. Against this backdrop, China’s reopening, marginally stronger GDP growth, and massive fiscal stimulus to support renewables and defense is being rolled out. In states with high debt-to-GDP ratios like the EU and US, the risk of fiscal dominance is rising, and with it higher inflation. We remain long the XOP oil and gas ETF; the XME metals and mining ETF, and long the commodity COMT ETF to hedge this risk.

Biden’s State of the Union address will mostly be blocked by a gridlocked Congress. The one point of agreement, big spending, spells trouble over the long run, even if a technical default is avoided this fall.

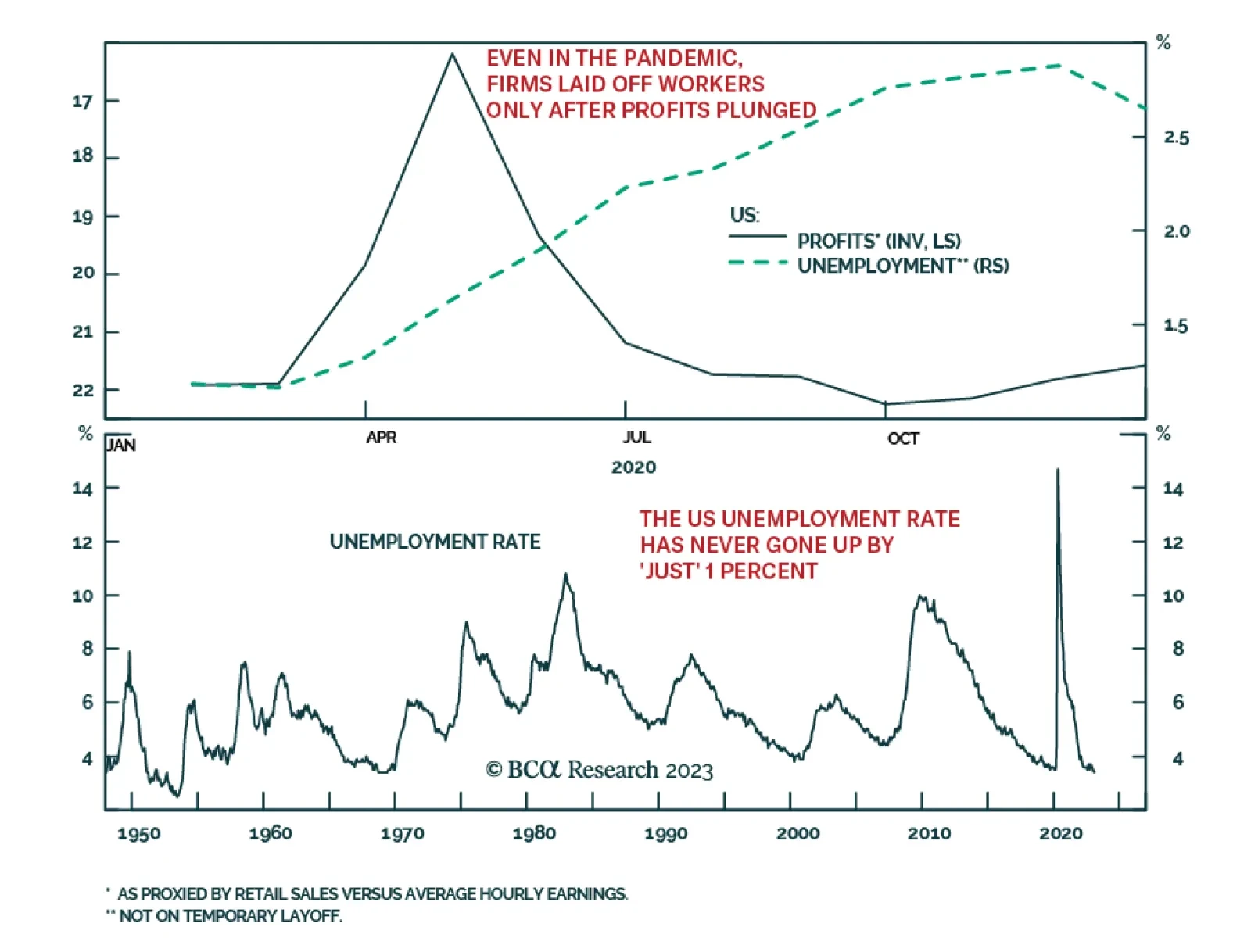

The Fed is betting that the usual non-linearity of unemployment is different this time, but so far, there is nothing to suggest that it is different. We discuss the key signposts to watch out for, plus the implications for interest rates and asset allocation.

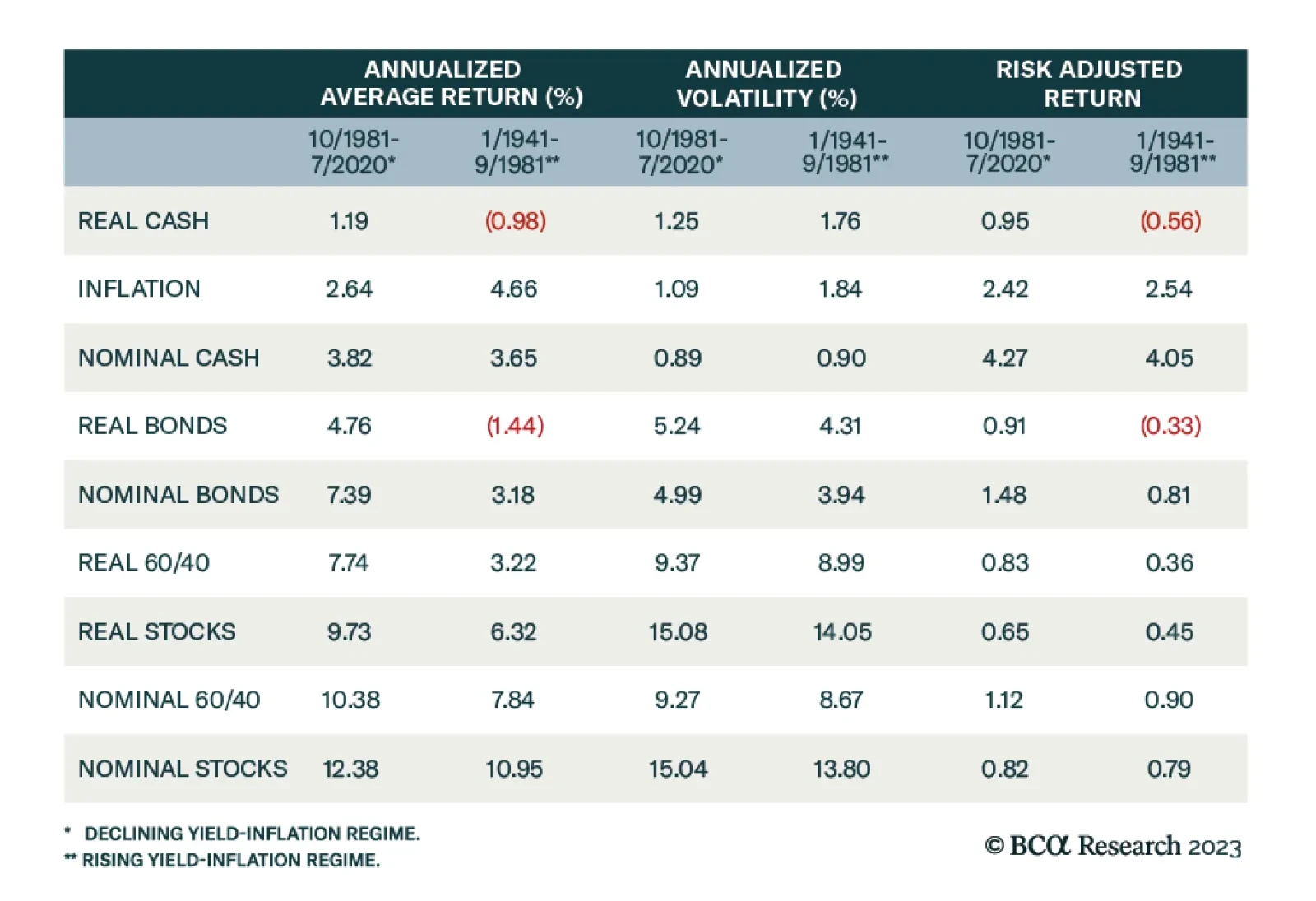

This is the first of two Special Reports aiming to answer client questions in response to the recent dramatic changes in stock-bond correlations. In this report we focus on what role US Treasurys have played since 1872, how the current regime shift in stock-bond correlation compares to 150-years of history, and how it will impact asset allocation going forward.