United States

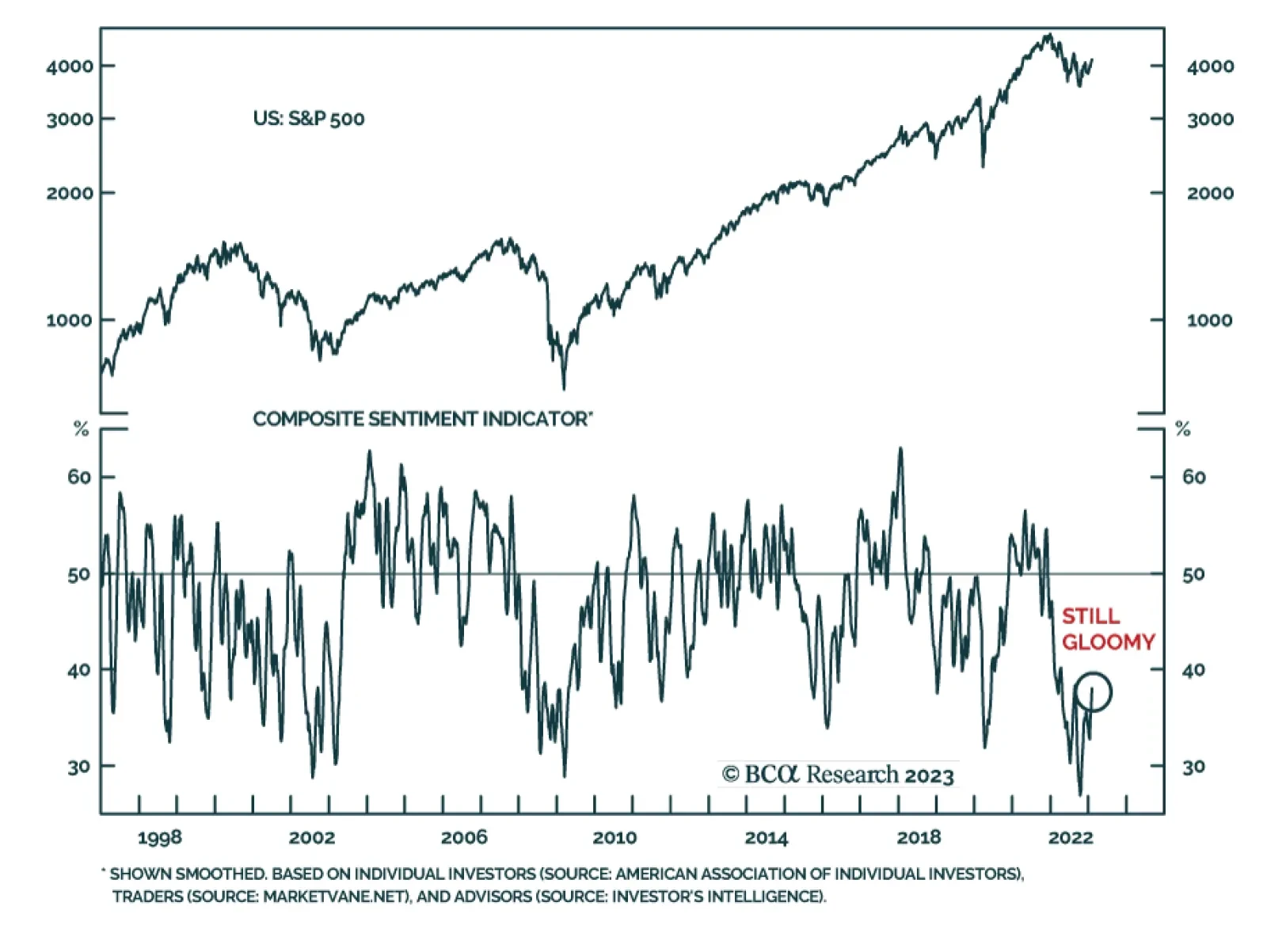

The Fed’s actions at its meeting last Wednesday were no surprise – downshifting to 25 basis points while guiding for more hikes was widely expected – but Chair Powell’s newly conciliatory tone at the press conference helped to spark a two-day equity rally. We remain overweight equities, expecting the S&P 500 to rally into the mid-4,000s at some point in the first half.

This week we present our Portfolio Allocation Summary for February 2023.

This week, we articulate what the actions of the three major central banks that met (Fed, ECB and BoE) mean for currency markets. This is within the context of our analysis of the latest data releases in the G10, that allows us to calibrate currency strategy.

Financial markets were taken on a wild ride between Wednesday and Friday of this week, with hugely important monetary policy meetings in the US, euro area and UK along with a rash of economic data. Despite all the news, noise and market volatility, the underlying message for monetary policy and bond yields in the US, euro area and UK is unchanged.