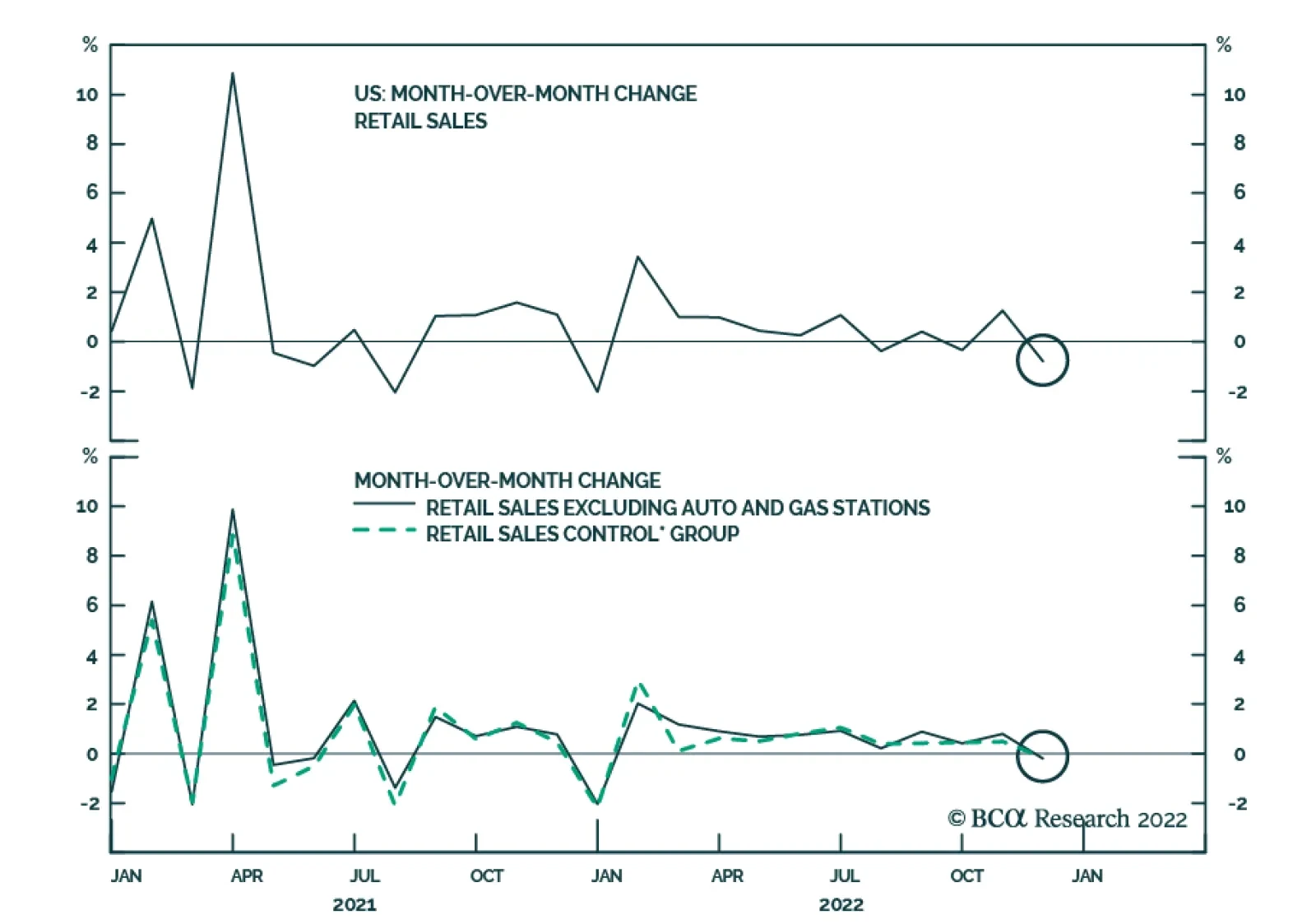

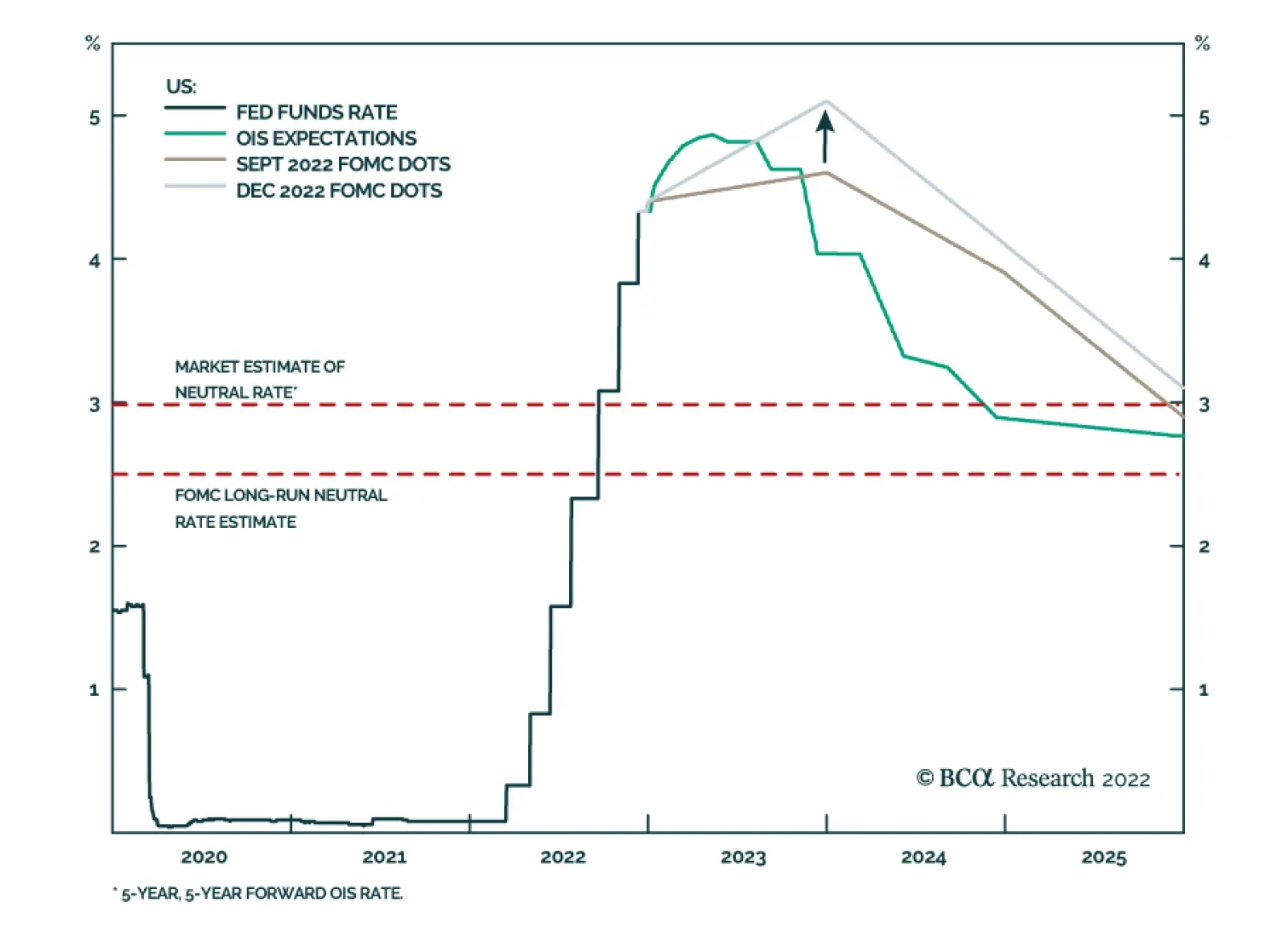

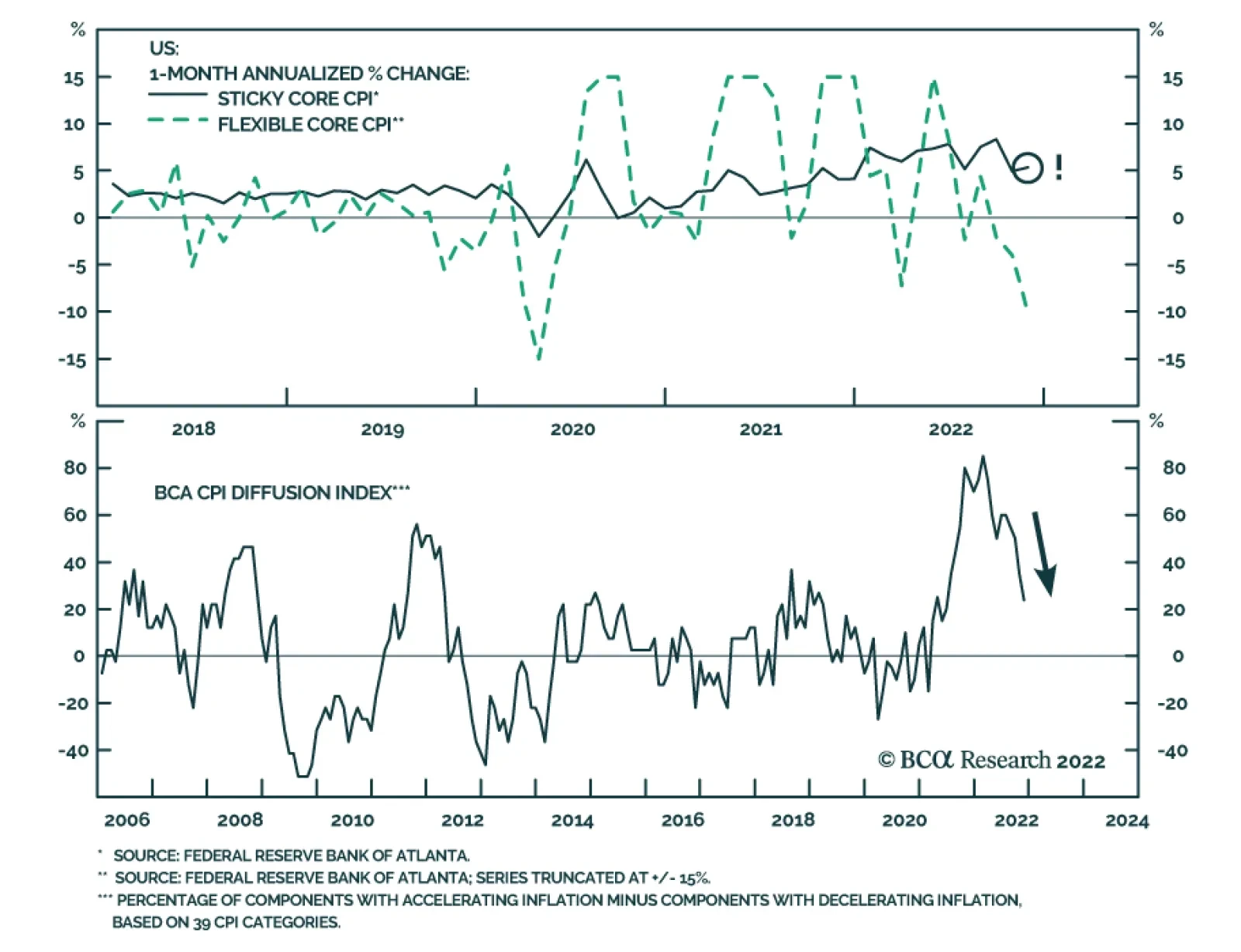

United States

Investors were heartened by the November CPI report, but the Fed said not so fast. Although it snuffed out the latest mini-rally, ongoing disinflation will set the stage for another one early next year.

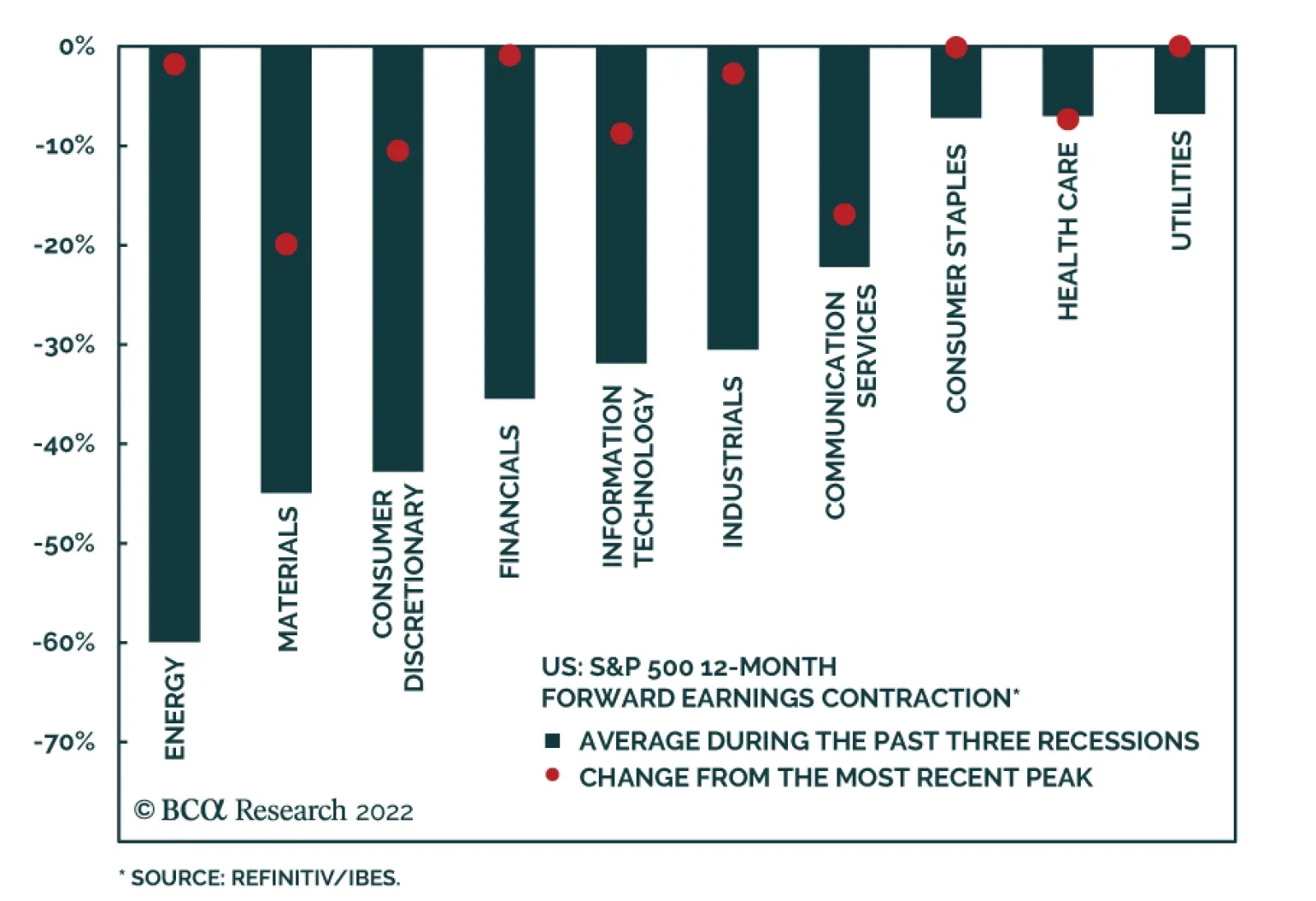

Both the US and China have structural imbalances that need correcting. The former has a structurally imbalanced labour market in which demand far outstrips supply. The latter has a massively overvalued housing market. The concurrent correction of these two structural imbalances in the world’s two largest economies will necessitate a sharp slowdown in global growth, and leads to several investment conclusions.

Following the release of the Bank Credit Analyst’s annual outlook, we unveil our key views for 2023. The investment strategy takeaway is that we want to lean into risk in the early part of the year but reduce exposure to it in the second half.