United States

We expect a bullish gold environment in 2023, conditional on a more dovish Fed. We are hesitant to go strategically long gold, since our view hinges on one variable: US monetary policy. We remain tactically bullish gold to take advantage of the reduced pace of US rate hikes.

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

Investors should maintain a conservative and defensive strategy until recession risks are clearly reduced.

This week we present our Portfolio Allocation Summary for December 2022.

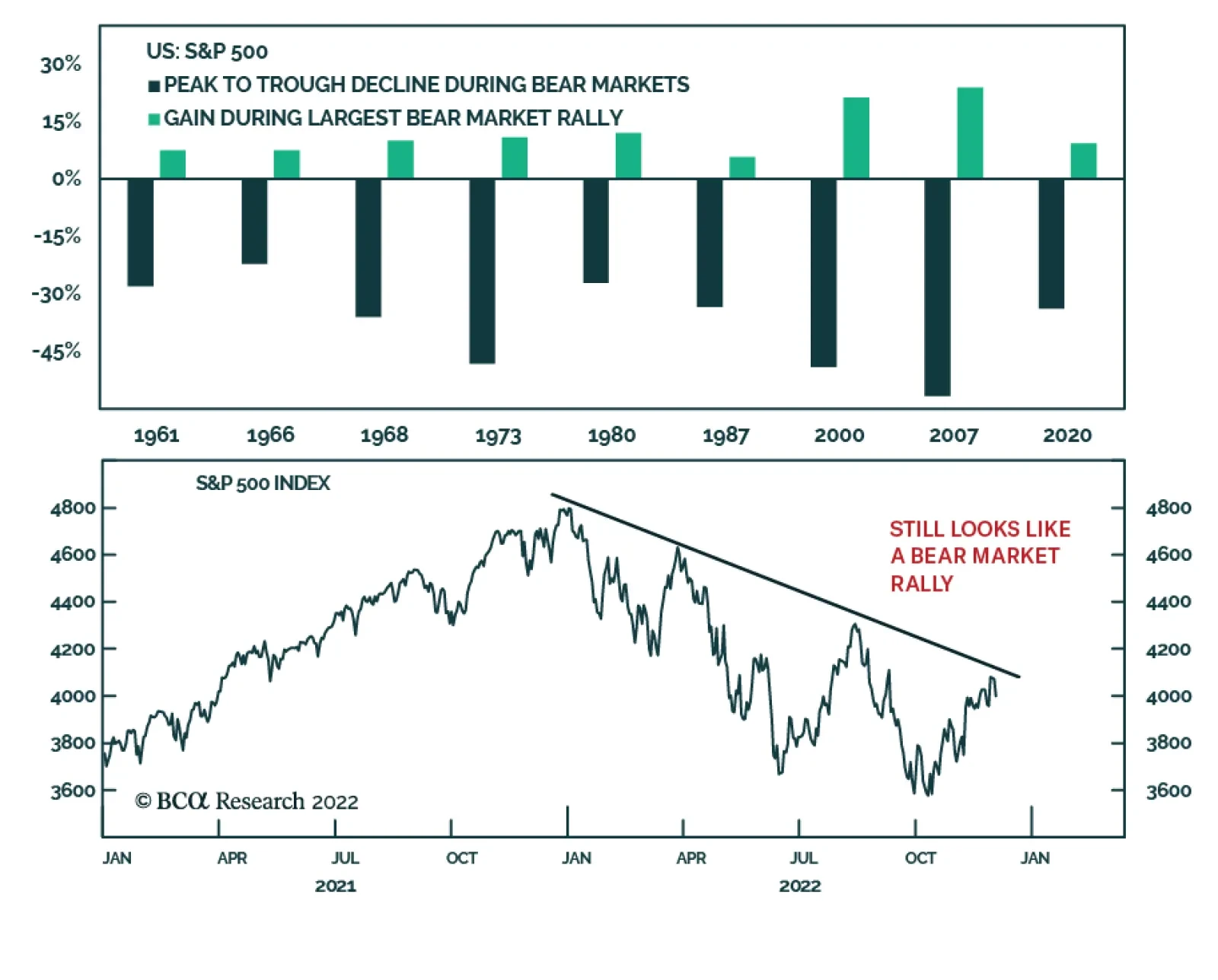

2023 will be another challenging year for the US equity market, characterized by the Fed’s battle with inflation, slowing economic growth, and earnings contraction. The S&P 500 is likely to reach new lows in the first half of the year falling as much as 20-25%, only to rebound sharply in the second half, once all the bad news is priced in.