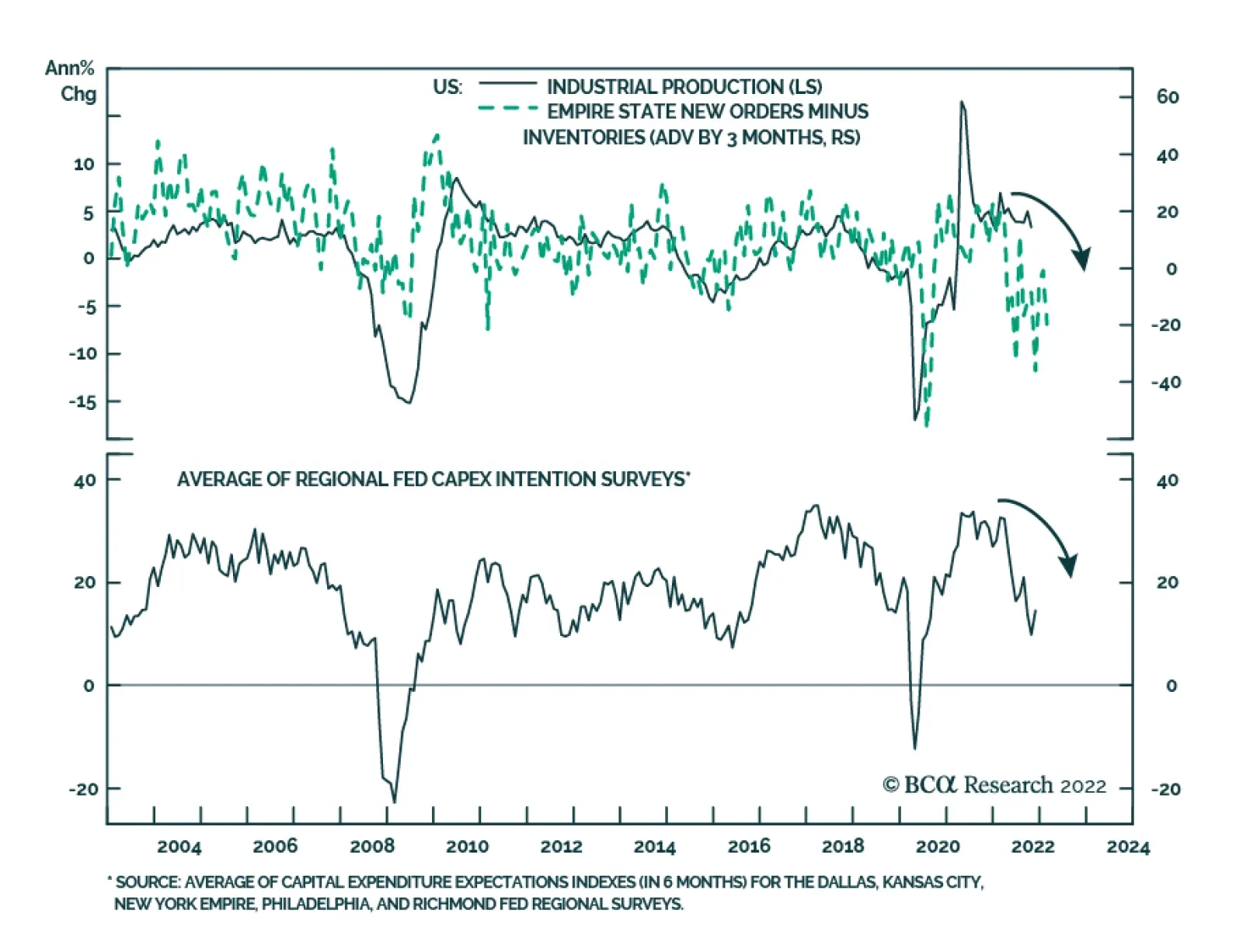

United States

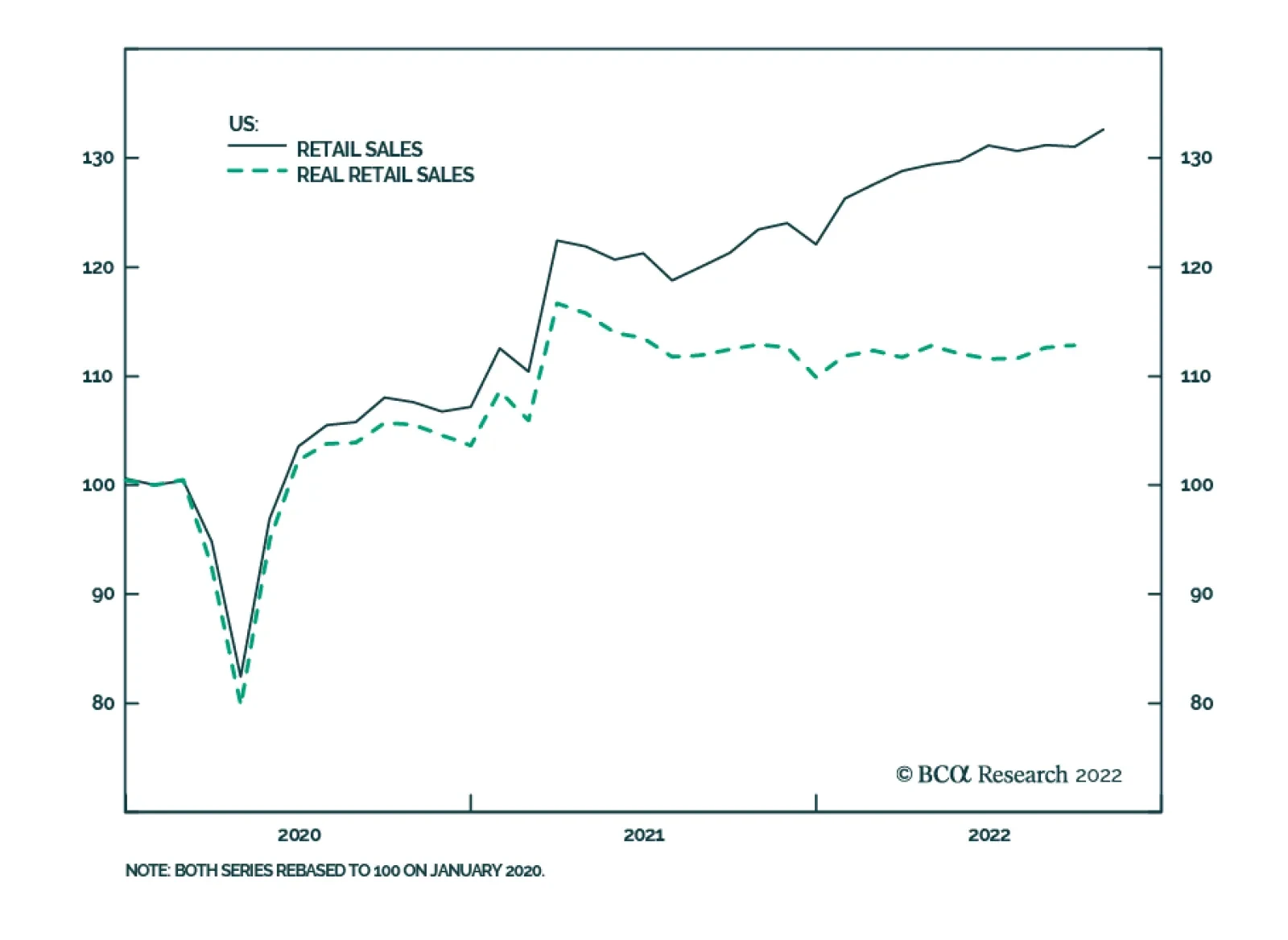

The latest CPI and PPI releases, the modestly less hawkish turn in Fed officials’ comments and evidence that consumers continue to spend with some relish support our constructive near-term views on equities and the economy.

The narrative that the US can tolerate much higher interest rates, compared to the rest of the world has helped the dollar in 2022. In this report, we examine the sustainability of this thesis, from our holistic assessment of global growth indicators.

The kinked supply framework helps explain why US inflation rose so suddenly shortly after the pandemic began and why the economy is likely to experience a benign disinflation over the next six months.

The messages from the deteriorating fundamental backdrop (tight monetary policy, slowing global growth) and improved credit valuation (elevated 12-month breakeven spreads) are giving conflicting signals on corporate bond strategy. We are putting more weight on the fundamentals and are staying with an overall underweight stance on global investment grade corporates, with a slight bias towards Europe given more attractive spread valuations. At the same time, we see selective opportunities in sectors where risk-adjusted spreads are wide as signaled by our individual country sector valuation models, like US Energy and euro area Financials.